Liquid Nitrogen Market Size, Share & Industry Analysis, By Distribution (Bulk Liquid Supply, Microbulk, Packaged Liquids, and On-Site/Captive Production), By Application (Food & Beverage, Healthcare & Life Sciences, Electronics & Semiconductors, Industrial Manufacturing, Chemicals & Energy, and Others), and Regional Forecast, 2026-2034

Liquid Nitrogen Market Size and Future Outlook

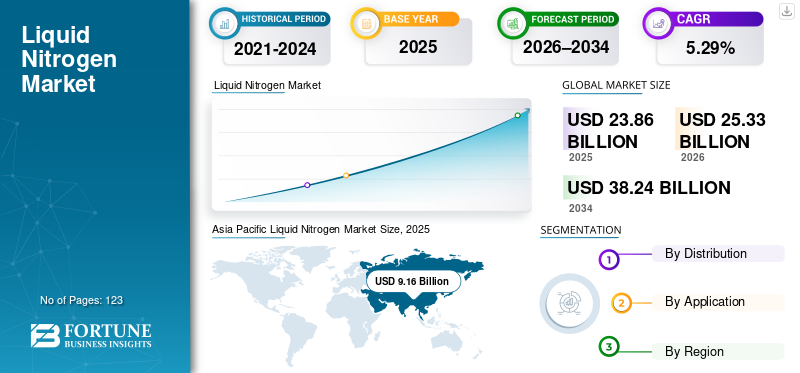

The global liquid nitrogen market size was valued at USD 23.86 billion in 2025 and is expected to reach USD 25.33 billion by 2026. Furthermore, the market is projected to reach USD 38.24 billion by 2034, exhibiting a CAGR of 5.29% during the forecast period. Asia Pacific dominated the liquid nitrogen market with a market share of 38.39% in 2025.

Liquid nitrogen is nitrogen in a liquid state at an extremely low temperature of approximately -96°C (-320°F or 77 K). It is a colorless, odorless, non-toxic, and non-flammable cryogenic liquid produced industrially by the fractional distillation of liquid air. The demand for liquid nitrogen is growing due to its wide range of applications as a coolant, refrigerant, and inert gas across various industries.

- In January 2025, the Dutch government announced plans to cut nitrogen emissions in half of vulnerable Natura 2000 habitats by 2030, following a lawsuit by Greenpeace over farming and transport pollution. Non-compliance risks a penalty, urging action across sectors to protect the country's biodiversity. Such factors are expected to impact market growth in the coming years.

Linde plc holds significant prominence in the market as the world's largest industrial gas company, leveraging its advanced air separation technology (ASUs) for large-scale production. The largest players in the global market are major industrial gas suppliers such as Air Liquide, Air Products, Praxair (now part of Linde), and Taiyo Nippon Sanso, consistently leading market share due to their extensive production, distribution, and technological expertise serving healthcare, electronics, food, and manufacturing sectors.

Moreover, the Asia Pacific region holds the largest market share in terms of revenue, driven by rapid industrialization, strong expansion in healthcare/pharma (cryopreservation and vaccines), booming electronics/semiconductors (cooling and inerting), and increasing demand in food & beverage (preservation) and chemicals.

Download Free sample to learn more about this report.

Liquid Nitrogen Market Key Takeaways

- 2025 Market Size: USD 23.86 billion

- 2026 Market Size: USD 25.33 billion

- 2034 Forecast Market Size: USD 38.24 billion

- CAGR: 5.29% from 2026–2034

- Asia Pacific dominated the liquid nitrogen market with a 38.39% share in 2025.

- The bulk liquid supply segment dominated the market with a 45.61% revenue share in 2025.

- The food & beverage segment accounted for a 30.2% market share in 2025.

Asia Pacific

Asia Pacific led the global market with a valuation of USD 9.16 billion in 2025 and is expected to reach USD 9.81 billion in 2026.

North America

North America reached USD 6.23 billion in 2025, securing its position as the second-largest regional market.

Europe

Europe was valued at USD 9.15 billion in 2025 and is projected to grow at a CAGR of 4.45% in the coming years.

U.S.

The market was analytically approximated at around USD 5.12 billion in 2025, accounting for roughly 21.5% of the global market size.

Japan

The market value was around USD 1.32 billion in 2025, representing approximately 5.94% of global revenues.

Read More

LIQUID NITROGEN MARKET TRENDS

Increasing Focus on High-Purity and Specialty Grades is Shaping Market Trends

The increasing focus on high-purity and specialty grades is driving market growth in the liquid nitrogen sector, as industries demand ultra-clean variants for precision applications. Electronics manufacturing relies on impurity-free nitrogen for semiconductor wafer cooling and oxide etching, while the pharmaceutical industry requires specialty cryogenic grades for biologics preservation and vaccine transport. Food processors seek tailored formulations to enhance flash freezing without residue contamination. This shift spurs innovation in air separation technologies and on-site generation, enabling customized purity levels that meet stringent regulatory standards and boost operational efficiency across high-tech supply chains.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Food Processing and Cold-Chain Infrastructure is Driving Market

The expansion of food processing and cold-chain infrastructure drives demand for liquid nitrogen as industries prioritize food safety, extended shelf life, and efficient preservation. This cryogenic agent enables rapid flash freezing, preserving texture, flavor, and nutritional value in meats, seafood, fruits, and vegetables far better than traditional methods.

- In December 2025, Cencora announced an expansion with a new 500,000 sq ft Texas facility set to open in 2028, its fifth U.S. site, offering room-temperature cryogenic storage. The company commits USD 1 billion to U.S. distribution modernization through 2030 and enhances its European cold chain, including cryogenic capabilities in the Netherlands.

In sprawling cold-chain networks from harvest to retail, liquid nitrogen supports seamless cryogenic transport and storage, minimizing spoilage and waste. As global supply chains become increasingly complex and consumer demand surges for fresh and frozen goods, food processors are increasingly relying on this versatile coolant to streamline operations, ensure quality, and meet rising volumes without compromising standards.

MARKET RESTRAINTS

Cryogenic Storage and Transportation Costs to Restraint Market Growth

Cryogenic storage and transportation costs hinder the growth of the market by imposing significant economic hurdles to widespread adoption. Specialized vessels, insulation, and continuous refrigeration demand escalate expenses, making the supply chain complex and costly compared to conventional cooling alternatives. High upfront investments in cryogenic infrastructure, coupled with ongoing operational outlays for energy-intensive liquefaction and delivery, deter small-scale users and emerging markets. Volatility in raw material sourcing and logistics further amplifies these burdens, limiting scalability. As a result, industries weigh these prohibitive costs against benefits, slowing expansion despite liquid nitrogen's superior performance in preservation and processing applications.

MARKET OPPORTUNITIES

Expansion of Microbulk and Decentralized Supply Models is Expected to Create Lucrative Opportunities

The expansion of microbulk and decentralized supply models presents strong opportunities for liquid nitrogen market growth, overcoming traditional limitations of bulk delivery. These innovative systems deliver on-site, smaller-volume supplies via portable tanks, reducing transportation costs, logistics complexity, and lead times for end-users.

Food processors, pharmaceutical manufacturers, and industrial companies gain flexibility, minimizing storage needs and enabling just-in-time access to cryogenic cooling. Decentralized models empower remote or high-demand sites with reliable, efficient replenishment, fostering adoption in emerging regions. As supply chains evolve toward agility and sustainability, microbulk solutions drive broader market penetration and long-term demand.

MARKET CHALLENGES

Logistics Disruptions and Supply Chain Volatility May Create Market Challenges

Supply chain and logistics disruptions pose significant challenges to the market growth, as they undermine reliable delivery and availability. Geopolitical tensions, natural disasters, and port congestion disrupt raw material flows and cryogenic transport, leading to shortages and price surges. The product's extreme sensitivity to temperature requires specialized, uninterrupted handling, which amplifies vulnerabilities in global networks.

Fuel scarcity and regulatory hurdles further complicate fleet operations, resulting in delayed supplies to critical sectors such as food processing and healthcare. These persistent disruptions erode confidence, inflate costs, and hinder scalability, compelling industries to seek costlier alternatives or stockpile reserves amid uncertain reliability.

Liquid Nitrogen Market Segmentation Analysis

By Distribution

Bulk Liquid Supply Dominated Due to High Demand in Food Processing & Chemicals Industries

Based on distribution, the market is divided into bulk liquid supply, microbulk, packaged liquids, and on-site/captive production.

The bulk liquid supply segment in 2025 dominated the market, with a revenue share of 45.61%, as the go-to mode for large-scale industries such as food processing and chemicals, offering cost-effective, high-volume delivery through tankers and on-site storage.

Meanwhile, microbulk stands out as the fastest-growing segment, with a CAGR of 7.47% over the coming years. It provides flexible, on-demand dispensing via portable containers that reduce logistics costs and enable decentralized access for smaller users in the pharmaceuticals and manufacturing industries.

By Application

To know how our report can help streamline your business, Speak to Analyst

Electronics & Semiconductors Appeared as Growing Segment Owing to Large-Scale Production

Based on application segmentation, the market is classified into food & beverage, healthcare & life sciences, electronics & semiconductors, industrial manufacturing, chemicals & energy, and others.

In 2025, the global market was dominated by the food & beverage segment, accounting for a 30.2% market share, primarily due to its heavy reliance on cryogenic freezing for preserving perishables, extending shelf life, and ensuring quality across global supply chains.

- For instance, India's MoFPI is accelerating cold chain expansion under PMKSY to strengthen post-harvest infrastructure, reducing losses for perishables. Key efforts include integrated projects from farm to retail, financial aid for storage and reefer vans, and boosting farmer incomes and sector competitiveness.

Meanwhile, electronics & semiconductors appears as the fastest-growing segment, projected to grow at the highest CAGR of 7.70% during the forecast period. Such growth is driven by demand for ultra-pure cooling in manufacturing precise components, such as chips and wafers. This shift highlights the versatility of liquid nitrogen in high-stakes precision applications amid surging technological innovation.

Liquid Nitrogen Market Regional Outlook

By region, the market is categorized into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Liquid Nitrogen Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant liquid nitrogen market share in 2025, valued at USD 9.16 billion, and also expected to take the leading share in 2026 with USD 9.81 billion. Asia Pacific leads the global market, holding the largest regional share driven by rapid industrialization, booming food processing, and semiconductor manufacturing in China, India, and Japan. Key sectors, such as metal fabrication, pharmaceuticals, and electronics, fuel demand through cryogenic applications in freezing, preservation, and precision cooling. The expansion of cold-chain infrastructure and microbulk supply models further accelerates adoption amid rising exports and technological innovation.

China Liquid Nitrogen Market

The China market in 2025 was valued at around USD 3.49 billion, accounting for roughly 14.67% of the global Liquid Nitrogen revenues. China's market is growing at a strong pace, supported by robust steel production, chemicals, and pharmaceutical R&D. The steady integration of advanced technology enhances efficiency across various industries.

India Liquid Nitrogen Market

India’s market is projected to be one of the largest worldwide, with 2025 revenues at around USD 1.30 billion, representing approximately 5.47% of the global market.

Japan Liquid Nitrogen Market

The Japan market value in 2025 was around USD 1.32 billion, accounting for approximately 5.94% of global revenues.

North America

North America reached USD 6.23 billion by 2025, securing the position of the second-largest market region. North America dominates the market, holding a substantial share and experiencing steady growth of around six percent annually, driven by the advanced healthcare, food processing, and manufacturing sectors. The U.S. leads regionally, leveraging cryogenic applications in biologics preservation, flash freezing, and semiconductor cooling.

U.S. Liquid Nitrogen Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market in 2025 analytically approximated at around USD 5.12 billion, accounting for roughly 21.5% of the global market size. The U.S. market exhibits robust growth, with North America leading the way and holding a dominant share, driven by the advanced healthcare, food processing, and semiconductor sectors.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 1.78 billion in 2025.

Latin America exhibits moderate yet promising growth in the market, driven by the expansion of the food processing, agriculture, and healthcare sectors in Brazil, Mexico, and Argentina. Demand rises from cryogenic freezing for exports, medical cryopreservation, and industrial applications, such as mining and chemicals.

Brazil Liquid Nitrogen Market

Brazil's market reached approximately USD 1.38 billion by 2025, accounting for roughly 5.82% of the global market.

Europe

Europe is projected to record a growth rate of 4.45% in the coming years, which is the third highest among all regions, and reach a valuation of USD 9.15 billion in 2025. Europe's market is growing steadily at around 6% annually, driven by food preservation, healthcare cryopreservation, and manufacturing needs in countries such as Germany and France. Key sectors include pharmaceuticals for biologics storage and food & beverage for flash freezing, amid sustainability pushes for efficient cooling.

Germany Liquid Nitrogen Market

The German market size in 2025 was around USD 1.39 billion. It is projected to reach USD 1.42 billion by 2026, representing approximately 5.61% of the global liquid nitrogen revenues.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market reached a valuation of USD 0.95 billion in 2025. The Middle East & Africa market is driven by Urbanization, renewable energy integration, and the adoption of prepaid metering, despite high costs and cyber risks. Government investments fuel residential and utility upgrades.

GCC Liquid Nitrogen Market

The GCC market value reached approximately USD 0.46 billion by 2025, accounting for around 1.95% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding Market Share Through Partnerships, Business Expansion, and Technological Advancements

The global market has a fragmented market structure, comprising prominent players such as Linde plc, Air Liquide, Air Products and Chemicals, Inc., Taiyo Nippon Sanso Corporation, and Messer Group, among others. For instance, in February 2025, Air Liquide announced plans to build and operate a large-scale Air Separation Unit on Naoshima Island, Japan, to supply oxygen, nitrogen, argon, and neon. The facility supports Mitsubishi Materials' copper production ramp-up to meet energy transition needs and strengthens rare gas supply for semiconductors, transportation, and construction, with operations scheduled to begin in 2027. Such developments are expected to fuel market growth over the forecast period.

LIST OF KEY LIQUID NITROGEN COMPANIES PROFILED

- Linde plc (Ireland)

- Air Liquide (France)

- Air Products and Chemicals, Inc. (U.S.)

- Taiyo Nippon Sanso Corporation (Japan)

- Messer Group (Germany)

- SOL Group (Italy)

- Air Water Inc. (Japan)

- Gulf Cryo (UAE)

- Matheson Tri-Gas (U.S.)

- Iwatani Corporation (Japan)

- Yingde Gases Group (China)

- Messer Americas (U.S.)

- BASF SE (Germany)

- INOX Air Products (India)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Taiyo Nippon Sanso launched “Green Liquid Nitrogen,” Japan’s first third-party certified CO2-free gas, produced via renewable energy-powered air separation. This innovation supports decarbonization in the food and beverage industry, healthcare, and electronics by offering sustainable cryogenic cooling with zero carbon emissions. The move aligns with global net-zero goals.

- May 2025: F4E and Air Liquide advanced ITER cryoplant commissioning by successfully testing and cooling liquid nitrogen refrigerators after mechanical acceptance. This pre-cooler for helium supports fusion operations, with full integration expected by mid-2026 through collaborative efforts.

- April 2024: N2 Solutions acquired PFS Nitrogen Services, thereby expanding its nitrogen offerings to the energy, industrial, chemical, and pipeline sectors. The deal includes the addition of pipe freezing technology, utilizing liquid nitrogen for leak detection and repairs, as well as new Gulf Coast locations in Highlands, TX; Broussard, LA; and Petal, MS. This enhancement enhances fleet capabilities, operational efficiency, and provides cost-effective solutions for clients.

- June 2024: NASA awarded contracts to six companies, including Linde, Air Products, and Messer, to supply liquid nitrogen and oxygen to U.S. centers from 2024 to 2029. These gases support pneumatic actuation, purging, cooling, and rocket propulsion for aerospace research and missions.

- May 2024: DanClan Biotech entered a strategic partnership with Nitrogen Danmark to enhance cryogenic storage solutions. The collaboration ensures a reliable supply of liquid nitrogen for biobanks and medical applications, improving sample preservation efficiency and operational reliability across biotech facilities in Denmark.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.29% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Distribution, Application, and Region |

|

By Distribution |

· Bulk Liquid Supply · Microbulk · Packaged Liquids · On-Site/Captive Production |

|

By Application |

· Food & Beverage · Healthcare & Life Sciences · Electronics & Semiconductors · Industrial Manufacturing · Chemicals & Energy · Others |

|

By Region |

· North America (By Distribution, By Application, and Country) o U.S. o Canada · Europe (By Distribution, By Application, and Country) o U.K. o Germany o France o Italy o Spain o Rest of Europe · Asia Pacific (By Distribution, By Application, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Latin America (By Distribution, By Application, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Distribution, By Application, and Country) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 23.86 billion in 2025 and is projected to reach USD 38.24 billion by 2034.

In 2025, the market value stood at USD 9.16 billion.

The market is expected to exhibit a CAGR of 5.29% during the forecast period.

The food & beverage sector led the nitrogen segment, which in turn led the market by application.

The expanding food processing and cold-chain infrastructure is driving the market.

H Linde plc, Air Liquide, Air Products and Chemicals, Inc., Taiyo Nippon Sanso Corporation, and Messer Group, among others, are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Liquid nitrogen is widely used for cryogenic freezing, chilling, and grinding in food processing due to superior product quality, reduced dehydration, and faster throughput. The growth in ready-to-eat foods, frozen foods, and protein processing is a primary demand driver, particularly in Asia Pacific and Latin America.

- 2021-2034

- 2025

- 2021-2024

- 123

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us