Low-Cost Electronic Warfare Drone Market Size, Share & Industry Analysis, By End User (Border & Homeland Security and Government & Military), By Platform Type (Multirotor, Fixed-Wing, and Hybrid VTOL), By Mission Type (Electronic Attack (EA), Electronic Support (ES), Electronic Protection (EP), and Multi-Function Electronic Warfare (EW)), By Payload Type (Communications Jamming, SIGINT, GNSS, Radar Warning/Sensing, and Others), By Operational Model (Reusable, Attritable, Expendable/One-Way, Swarm/Collaborative, and Persistent/Tethered), and Regional Forecast, 2026-2034

Low-Cost Electronic Warfare Drone Market Size and Future Outlook

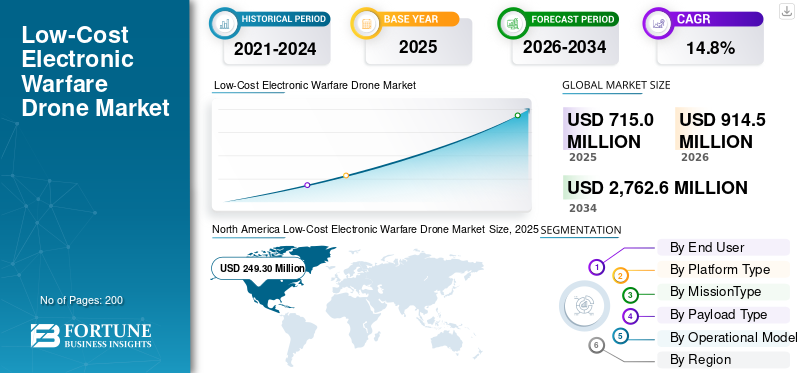

The global low-cost electronic warfare drone market size was valued at USD 715.0 million in 2025. The market is projected to grow from USD 914.5 million in 2026 to USD 2,762.6 million by 2034, exhibiting a CAGR of 14.8% during the forecast period. North America dominated the low-cost electronic warfare drone market with a market share of 34.87% in 2025.

The market centers on affordable unmanned aerial systems designed for electronic attack, protection, and support missions. These drones deliver jamming, spoofing, deception, and signal intelligence capabilities at a fraction of traditional platform costs, enabling militaries to deploy attritable assets in high-threat environments. Key innovations include miniaturized RF payloads, artificial intelligence driven autonomy for swarm operations, modular designs for rapid mission adaptation, and lightweight composites for extended endurance. The market thrives on asymmetric warfare demands, where inexpensive EW drones counter advanced air defenses, disrupt communications, and provide spectrum dominance without risking manned aircraft. Growth reflects the rising adoption of unmanned systems for real-time electronic countermeasures in modern battlefields.

Key players in the market include Anduril, AeroVironment including BlueHalo, Northrop Grumman, Shield AI, TEKEVER, Leonardo, Elbit Systems, CACI, Kratos Defense, and Israel Aerospace Industries. These companies are active through low-cost drone platforms, electronic warfare payloads, modular integration, and attritable mission-focused defense solutions.

Download Free sample to learn more about this report.

Low-Cost Electronic Warfare Drone Market Takeaways

- 2025 Market Size: USD 715.0 million

- 2026 Market Size: USD 914.5 million

- 2034 Forecast Market Size: USD 2,762.6 million

- CAGR: 14.8% from 2026–2034

- North America dominated the low-cost electronic warfare drone market with a 34.87% share in 2025.

- The hybrid VTOL (vertical takeoff) segment is projected to grow at a 15.5% CAGR during the forecast period.

- The swarm/collaborative segment is expected to register the fastest growth at a 17.1% CAGR during the forecast period.

North America

North America maintained its leading position with a market value of USD 249.30 million in 2025 and is expected to remain the largest regional market.

Europe

Europe is projected to become the second-largest regional market, reaching USD 289.3 million by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 234.1 million by 2026, expanding at a 14.9% CAGR during the forecast period.

U.S.

The market is estimated to reach USD 293.8 million by 2026, accounting for approximately 14.4% of global sales.

Japan

The market is projected to reach USD 38.1 million by 2026, growing at a 15.0% CAGR during the forecast period.

Read More

LOW-COST ELECTRONIC WARFARE DRONE MARKET TRENDS

Shift toward Automation and Lightweight Materials is a Key Trend in the Market

The market is rapidly evolving with a strong shift toward automation and lightweight materials. Manufacturers increasingly integrate AI-driven autonomy for real-time jamming, spoofing, and spectrum dominance, reducing operator dependency in contested environments. Composite materials such as carbon fiber and advanced polymers slash weight by up to 40%, boosting payload capacity and endurance without inflating costs. Modular designs enable quick upgrades for counter-UAV missions, while swarm tactics leverage cheap EW payloads for mass disruption. This trend aligns with militaries seeking affordable alternatives to high-end platforms, fostering innovation in miniaturized radar warning receivers and directed energy systems. The proliferation of open-source software accelerates prototyping, democratizing access for smaller nations and non-state actors.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Demand for Lightweight Materials and Precision Assembly to Drive Market Growth

Intensifying demand for lightweight materials and precision assembly propels the low-cost electronic warfare drone market growth. Militaries require drones that deliver potent EW effects such as broadband jamming and decoy generation while maintaining low signatures and extended loiter times. Advanced composites and 3D-printed components cut structural weight, allowing the integration of high-power RF payloads in compact airframes. Precision assembly techniques, including robotic soldering and automated testing, ensure reliability in harsh electromagnetic environments. Geopolitical tensions drive the procurement of attritable assets for high-risk missions, while supply chain localization reduces lead times and costs, fueling scalable production for rapid deployment.

MARKET RESTRAINTS

High Costs and Regulatory Compliance May Hinder Market Growth

High development and production costs, coupled with stringent regulatory compliance, significantly restrain the low-cost EW drone market. Even "low-cost" variants demand expensive spectrum analyzers, gallium nitride amplifiers, and secure encryption, pushing per-unit prices beyond affordability for many buyers. Compliance with ITAR, export controls, and frequency allocation standards delays certifications and inflates overheads. The intellectual property protections limit component sourcing, while volatile raw material prices for rare earths used in EW antennas exacerbate margins. Smaller firms struggle against established primes, hindering market entry and innovation pace despite the low-cost label.

MARKET OPPORTUNITIES

Expansion in Emerging Markets and Aftermarket Services to Offer New Growth Avenues

Significant opportunities abound in emerging markets such as Asia Pacific, Latin America, and the Middle East, where defense budgets prioritize cost-effective EW capabilities against regional threats. Nations such as India, Brazil, and Saudi Arabia seek indigenous production to bypass export restrictions, spurring local assembly and tech transfers. Aftermarket services present another frontier, including retrofitting legacy drones with low-cost EW suites, maintenance contracts, and training programs. Partnerships with commercial drone makers enable dual-use adaptations for border surveillance and electronic countermeasures. Rising urban warfare needs amplify the demand for compact, disposable EW swarms, while export-friendly designs open doors for volume sales to allied forces.

MARKET CHALLENGES

Skilled Workforce Shortages and Cyclical Demand to Challenge the Market Growth

Skilled workforce shortages and cyclical demand pose major challenges to the low-cost EW drone market. RF engineering, embedded systems, and autonomy expertise remain scarce, with talent concentrated in high-end defense hubs, slowing prototyping and scaling. Training gaps in electromagnetic spectrum operations hinder effective deployment. Demand fluctuates with geopolitical events and budget cycles, creating boom-bust cycles that disrupt supply chains and R&D investments. Integrating commercial-off-the-shelf components risks performance shortfalls in contested spectra, while cybersecurity vulnerabilities in low-cost designs invite exploits, demanding ongoing mitigations amid resource constraints.

Segmentation Analysis

By End User

Rising Defense Modernization Needs to Boost Government & Military Segment Growth

Based on end user, the market is segmented into border & homeland security and government & military.

The government & military segment is anticipated to account for the largest low-cost electronic warfare drone market share. Rising defense modernization, battlefield digitization, and the need for low-cost attritable electronic warfare capabilities are pushing government and military procurement higher. Armed forces want drones that can jam, sense, deceive, and survive in contested environments without risking expensive crewed platforms. Owing to these factors, this segment depicts an accelerated expansion globally.

The border & homeland security segment is anticipated to rise at a CAGR of 11.6% over the forecast period.

By Platform Type

Longer-Range and Higher-Endurance Mission Needs to Bolster Fixed-Wing Segment Growth

Based on platform type, the market is segmented into multirotor, fixed-wing, and hybrid VTOL.

In 2025, the fixed-wing segment dominated the global market. Militaries need longer range, greater endurance, and deeper stand-in electronic warfare reach, fixed-wing drones are seeing stronger adoption. They cover larger areas, carry heavier payloads, and support persistent surveillance, situational awareness or jamming missions more efficiently than multirotors. This operational advantage is steadily lifting the demand for the fixed-wing segment overall.

The hybrid VTOL (vertical takeoff) segment is projected to grow at a CAGR of 15.5% over the forecast period.

By Mission Type

Product Usage for Disrupting Enemy Communication Systems to Boost Electronic Attack (EA) Segment Growth

Based on mission type, the market is segmented into electronic attack (EA), electronic support (ES), electronic protection (EP), and multi-function electronic warfare (EW).

The electronic attack (EA) segment is anticipated to witness a dominating market share over the forecast period. As armed forces prioritize disrupting enemy communications, navigation, and radar systems, electronic attack drones are becoming more important. These systems offer a cheaper way to create tactical electromagnetic effects close to the battlefield. Their ability to suppress threats and support maneuver operations is directly driving stronger demand for the EA segment.

The electronic support (ES) segment is projected to grow at a high CAGR of 14.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Payload Type

Need to Disrupt Enemy Communications to Bolster Communications Jamming Segment Growth

Based on payload type, the market is segmented into communications jamming, SIGINT, GNSS, radar warning/sensing, and others.

The communications jamming segment dominated the global market share in 2025. The demand for communications jamming is increasing as it gives forces a practical way to disrupt command links, tactical radios, and drone control channels. In modern conflicts, denying communication often creates immediate battlefield advantage. That direct operational payoff, combined with relatively simple integration, is pushing this segment upward across users.

In addition, the SIGINT segment is projected to grow at a CAGR of 15.9% during the study period.

By Operational Model

Cost Efficiency and Repeat Mission Use to Fuel Reusable Segment Growth

Based on operational model, the market is segmented into reusable, attritable, expendable/one-way, swarm/collaborative, and persistent/tethered.

The reusable segment dominated the global market share in 2025. Reusable low-cost electronic warfare drones are gaining demand as operators want systems that can fly multiple missions without constant replacement. They reduce lifecycle cost, improve training value, and support routine tactical deployment better than expendable models. That balance between affordability and sustained utility is keeping demand for reusable platforms strong.

In addition, the swarm/collaborative segment is projected to grow at a CAGR of 17.1% during the study period.

Low-Cost Electronic Warfare Drone Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Low-Cost Electronic Warfare Drone Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 187.75 million, and also maintained the leading share in 2025, with USD 249.30 million. North America sees strong demand as the U.S. dominates defense budgets and Replicator is pushing attritable autonomous systems at scale, while Canada is steadily lifting spending and modernization commitments.

U.S. Low-Cost Electronic Warfare Drone Market

Based on North America’s strong contribution and the U.S.’s dominance within the region, the U.S. market can be analytically approximated at around USD 293.8 million in 2026, accounting for roughly 14.4% of global sales. Demand in the U.S. is the strongest globally due to vast defense budgets and Replicator’s push for attritable autonomous systems. Furthermore, the interest in brigade-level airborne electronic warfare is accelerating procurement and experimentation across services.

Europe

The Europe market is estimated to reach USD 289.3 million in 2026 and secure the position of the second largest region in the market. Europe is experiencing the fastest surge in demand as war-driven rearmament accelerates spending, electronic warfare urgency rises, and programs such as the RAF’s Storm Shroud prove small EW drones are moving into service.

U.K. Low-Cost Electronic Warfare Drone Market

The U.K. market growth is estimated to reach around USD 56.0 million in 2026, representing CAGR of 15.9% over the forecast period. The product demand in the U.K. is strengthening as defense spending remains elevated and the RAF’s Storm Shroud program demonstrates real operational appetite for small drones carrying stand-in jamming payloads and autonomous electronic warfare effects.

Germany Low-Cost Electronic Warfare Drone Market

The Germany market is projected to reach approximately USD 52.8 million in 2026. The product demand in the country is rising as Berlin expands military expenditure, funds procurement through its special defense package, and prioritizes modernization. This creates room for tactical drones, survivable sensing, and electronic warfare integration.

Asia Pacific

Asia Pacific is projected to record a growth rate of 14.9% during the forecast period, which is the third highest among all regions, and reach a valuation of USD 234.1 million by 2026. The product demand in the region is rising quickly as China modernizes across domains, Japan expands strike and air-defense spending, and India pushes indigenous defense procurement, making tactical EW drones increasingly attractive region-wide.

China Low-Cost Electronic Warfare Drone Market

The China market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated to touch around USD 107.2 million. China shows strong demand as military modernization continues across aerospace, cyber, and unmanned systems, while regional competition encourages investment in affordable drones that can sense, jam, deceive, and saturate defenses.

Japan Low-Cost Electronic Warfare Drone Market

The Japan market share is estimated to touch around USD 38.1 million in 2026, accounting for a CAGR of 15.0% during the forecast period. The product demand in the country is rising rapidly as defense spending recorded its largest increase in decades, long-range strike and air-defense investments expand, and unmanned electronic support capabilities gain strategic relevance for deterrence.

India Low-Cost Electronic Warfare Drone Market

The India market is estimated to reach around USD 36.0 million in 2026. The product demand in the country is accelerating as defense spending rises, indigenous procurement is prioritized, and armed forces seek cost-effective drones for border surveillance, communications disruption, and broader electronic warfare missions across services.

Rest of the World

The rest of the world includes the Middle East and Africa and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 57.5 million and USD 15.5 million in 2026. The demand in the rest of the world is smaller but rising, led by the Middle East conflict-driven procurement, border-security needs, and selective Latin American adoption where budgets favor lower-cost, multi-mission systems for surveillance.

COMPETITIVE LANDSCAPE

Key Industry Players

Competition among Key Players to Surge with Rising Demand for Attritable Autonomous Electronic Warfare Capability

The market is being shaped by Anduril, AeroVironment including BlueHalo, Northrop Grumman, Shield AI, TEKEVER, Leonardo, Elbit Systems, CACI, Kratos Defense, and Israel Aerospace Industries as defense customers shift toward lower-cost drones that can deliver jamming, sensing, decoy, and stand-in effects. Their strength comes from combining tactical airframes, modular payload integration, attritable economics, and battlefield-ready autonomy. Anduril’s Ghost is positioned for electronic warfare missions, Northrop’s Lumberjack explicitly links attritable design with electronic warfare, and TEKEVER’s AR3 with Leonardo’s payload shows real operational fielding. These factors are leading to an increased competition among key players.

LIST OF KEY LOW-COST ELECTRONIC WARFARE DRONE COMPANIES PROFILED

- Anduril (U.S.)

- AeroVironment (including BlueHalo) (U.S.)

- Northrop Grumman (U.S.)

- Shield AI (S.)

- TEKEVER (Portugal)

- Leonardo (Italy)

- Elbit Systems (Israel)

- CACI (U.S.)

- Kratos Defense (U.S.)

- Israel Aerospace Industries (IAI) (Israel)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The Pentagon announced plans to mass-produce the LUCAS (Low-Cost Uncrewed Combat Attack System) drone, designed to disrupt enemy drone operations, manufactured by U.S.-based SpektreWorks.

- January 2026: EIL Arms & Ammunitions Ltd and CSIR–National Aerospace Laboratories (CSIR-NAL) signed a transfer-of-technology agreement to scale up the production of indigenous multicopter drone platforms.

- January 2026: Shield AI and JSW Defence announced a USD 90-million joint venture for the transfer of technology of V-BAT drones, which are designed for ISR in contested environments.

- January 2026: XTEND (Israel) partnered with an Indian firm to manufacture AI-powered, next-gen autonomous drones in India, focusing on defense, surveillance, and high-risk operations.

- November 2025: ideaForge Technology Limited secured a USD 8.5 million emergency procurement order from the Indian Army for its ZOLT tactical UAV, following tests in EW-contested environments.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.8% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By End User, By Platform Type, By Mission Type, By Payload Type, By Operational Model, and Region |

| By End User |

|

| By Platform Type |

|

| By Mission Type |

|

| By Payload Type |

|

| By Operational Model |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 715.0 million in 2025 and is projected to reach USD 2,762.6 million by 2034.

In 2025, the North America market value stood at USD 249.30 million.

The market is expected to exhibit a CAGR of 14.8% during the forecast period of 2026-2034.

By end user, the government & military segment is expected to dominate the market.

The demand for lightweight materials and precision assembly is a key factor driving market growth.

Anduril (U.S.), AeroVironment (including BlueHalo) (U.S.), Northrop Grumman (U.S.), Shield AI (U.S.), TEKEVER (Portugal), and Leonardo (Italy) are major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us