Magnesium Carbonate Market Size, Share & Industry Analysis, By Type (Light Magnesium Carbonate, Heavy Magnesium Carbonate, and Others), By Application (Rubber, Plastics & Chemicals, Food Additives & Food Processing, Pharmaceuticals, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

MAGNESIUM CARBONATE MARKET SIZE AND FUTURE OUTLOOK

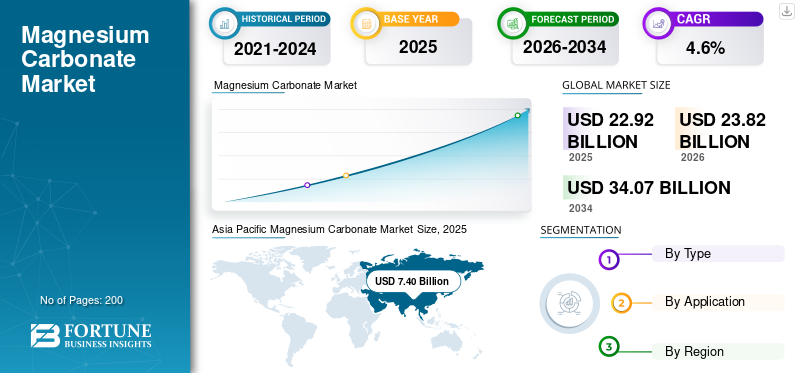

The magnesium carbonate market size was valued at USD 22.92 billion in 2025. The market is projected to grow from USD 23.82 billion in 2026 to USD 34.07 billion by 2034 at a CAGR of 4.6% during the 2026-2034 forecast period. Asia Pacific dominated the magnesium carbonate market with a market share of 32.29% in 2025.

Magnesium carbonate has light, heavy, and various other specialty/basic grades, which are significant in functions such as anticaking, absorption, pH adjustment, formulation support, and filler performance. Market growth is mainly supported by rising demand from food, pharmaceutical, nutraceutical, and personal care applications, where magnesium carbonate benefits from regulatory acceptance and higher-purity grade demand. Key players operating in the market include ICL Group Ltd., Konoshima Chemical Co. Ltd., Naikai Salt Industries Co. Ltd., Garrison Minerals LLC, and AMS Fine Chemicals.

Download Free sample to learn more about this report.

MAGNESIUM CARBONATE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 22.92 billion

- 2026 Market Size: USD 23.82 billion

- 2034 Forecast Market Size: USD 34.07 billion

- CAGR: 4.60% from 2026–2034

- Asia Pacific dominated the magnesium carbonate market with a market share of 32.29% in 2025.

- The segment expected to grow at a CAGR of 4.3% during the forecast period.

- Food additives & food processing expected to grow at a CAGR of 4.7% during the forecast period.

North America

North America is expected to register steady growth, supported by stable demand from food, pharmaceutical, and specialty industrial sectors, along with favorable regulatory recognition for magnesium carbonate applications.

Europe

Europe maintains a significant market position due to its well-established industrial minerals industry, strong specialty chemicals demand, and extensive use of magnesium carbonate in cosmetics and formulation applications.

Asia Pacific

Asia Pacific is expected to witness strong growth during the forecast period, supported by expanding food processing, pharmaceutical, personal care, and industrial manufacturing sectors across developing economies.

U.S.

In 2025, the U.S. represented a USD 3.44 billion market, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 15.0% of global market sales.

Japan

Japan’s magnesium carbonate market benefits from demand across pharmaceutical, food, and specialty chemical applications, supported by high-quality manufacturing standards and increasing focus on advanced industrial formulations.

Read More

MAGNESIUM CARBONATE MARKET TRENDS

Shift Toward Higher-Purity, Regulated, and Application-Specific Product Grades is Emerging Market Trend

The magnesium carbonate market growth is associated with growing inclination toward higher-purity, application-specific grades rather than simple commodity positioning. This is further supported by regulatory and product evidence. The U.S. eCFR recognizes magnesium carbonate, specifically magnesium carbonate hydroxide, for direct food use, while ICL Group Ltd. offers basic magnesium carbonate grades for food, nutraceutical, and pharmaceutical applications with Food Chemicals Codex (FCC), Good Manufacturing Practices (GMP), and pharmacopeia-linked compliance. This shows that the market is increasingly shaped by end-use requirements such as purity, flow behavior, particle characteristics, and regulatory suitability, especially in food, pharma, and specialty formulations.

Another prominent market trend is the rising product use in personal care and specialty formulation systems. For instance, ICL provides magnesium carbonate for cosmetics under its CareMag line, while the European Commission’s CosIng database confirms product’s presence as a cosmetic ingredient in the EU framework. This represents growing product demand in oil-absorbing, texture-enhancing, and specialty powder applications, especially where sensory performance and formulation stability is significant.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand from Food, Pharma, and Personal Care Sectors Supports Market Expansion

A major drivers for the market is its growing demand in regulated and formulation-sensitive applications. In the U.S., magnesium carbonate is recognized for direct food use under 21 CFR 184.1425, and different companies position basic magnesium carbonate for industrial baking, pH control, food systems, tablets, powders, and liquid suspensions. This gives the market an important growth base in food processing, nutraceuticals, and pharmaceutical sector, where quality standards and ingredient consistency is crucial.

Additionally, the product is highly demanded in personal care applications. ICL highlights MgCO3 in skin care and makeup applications, while CosIng supports its cosmetic relevance in the EU ingredient framework. These applications lifts market value as they are typically more application-sensitive than bulk mineral demand. As a result, the market growth is not only supported by volume expansion but also by movement toward higher-value specialty grades.

MARKET RESTRAINTS

Market Fragmentation and Product Overlap Limits Development

A major restraint in the market is fragmented product category across natural, basic, light, heavy, and hydroxide-linked commercial forms, which limits proper market measurement. The U.S. food regulation described magnesium carbonate as magnesium carbonate hydroxide, while ICL sells basic magnesium carbonate in multiple density and compliance grades. This creates ambiguity in how manufacturers, regulators, and buyers classify the product, especially while comparing bulk mineral-grade demand with specialty processed grades.

This is commercially impacts the market as weak category visibility makes it difficult to benchmark. Official trade data effectively identifies natural magnesium carbonate (magnesite) under HS 251910, but it does not isolate all specialty MgCO3 streams in the same way. This reflects that the demand, pricing, and competitive positioning are often less transparent than in chemicals with cleaner reporting structures.

MARKET OPPORTUNITIES

Premium Specialty Grades and Compliance-Led Applications Create Market Growth Potential

A significant market opportunity lies in the expansion of premium specialty grades for food, nutraceutical, pharmaceutical, and personal care applications. ICL explicitly offers basic MgCO3 as compliant with food and pharma standards and also offers cosmetic-focused grades. Konoshima similarly positions product across industrial, food, and pharma uses. This indicates that suppliers can create value by targeting purity, low-impurity performance, and compliance rather than competing only in lower-value bulk mineral channels.

Another market opportunity is regional manufacturing and downstream formulation growth in Asia. ICL notes China manufacturing capability for compliant grades, and Asia dominates the visible natural magnesium carbonate trade base through countries such as China and major regional importers including Indonesia and Japan. This showcases continued growth potential for suppliers that combine cost-competitive production with reliable quality for downstream food, pharma, and industrial customers.

MARKET CHALLENGES

Difficulty in Balance Between Specialty Demand Growth and Broad Mineral-Use Challenges Market Growth

A major challenge for the market is that specialty applications are attractive in value terms, but broad industrial and mineral uses can dominate the wider magnesium compounds landscape. United States Geological Survey (USGS) notes that magnesium compounds are used mainly in refractory and industrial systems, and that commercial magnesium compounds can come from magnesite, brines, and seawater-derived sources. This means product suppliers must compete within a broader magnesium chemistry ecosystem where end users may shift toward other magnesium compounds depending on function and cost.

The challenge is especially related to industrial uses such as chemicals, fillers, and formulation systems, where MgCO3 may be technically suitable but not always reliable. As a result, the market’s growth is often stronger in defined specialty niches than in open-ended bulk substitution markets. That creates a market structure with good value potential, but more limited visibility on breakout volume growth.

IMPACT OF TRADE PROTECTIONISM AND GEOPOLITICS

Trade protectionism and geopolitical disruptions can impact the market by disturbing mineral supply chains, cross-border chemical trade, and downstream manufacturing costs. The market’s natural magnesium carbonate stream is clearly international, with China, Spain, and Turkey among the leading exporters in 2024, while Indonesia and Japan were among the largest importers. This indicates that the market remain exposed to trade-route instability, freight costs, and regional industrial policy changes.

This impact is significant in Asia Pacific, where both supply and demand are focused. Any disruption involving Chinese exports, Southeast Asian imports, or Japanese industrial demand can hamper availability and delivered pricing more quickly than the market’s moderate visibility might suggest. For specialty grades, cross-border compliance and sourcing reliability is also crucial as many customers in food, pharma, and cosmetics are less tolerant of supplier disruption.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly focused on purity control, density management, particle engineering, and application-specific performance. ICL’s product positioning around heavy/basic grades, low impurities, and multiple regulated applications shows that development is centered on making the material more suitable for tablets, powders, food processing, and specialty formulations. Konoshima also highlights high-purity magnesium carbonate and application reach across industrial, food, and pharma uses, showcasing that the market is evolving through formulation fit rather than breakthrough chemistry.

Growing product use in personal care and advanced formulation systems is also leading to higher investment in R&D. ICL’s CareMag line emphasizes sensory and handling properties for cosmetics, suggesting that future innovation will continue to focus on absorbency, flow, bulk density, and skin-feel performance. This makes R&D more application-led than commodity-led, especially for higher-margin end uses.

SEGMENTATION ANALYSIS

By Type

Light Magnesium Carbonate Leads Due to Its Broader Suitability in Regulated and Specialty Applications

Based on type, the market is segmented into light magnesium carbonate, heavy magnesium carbonate, and others.

Among these, light magnesium carbonate is expected to hold the dominant share as lighter and lower-bulk-density grades are better aligned with food, pharmaceutical, nutraceutical, and personal care formulations, where dispersibility, texture, and controlled handling are important. ICL’s basic magnesium carbonate portfolio and its pharma/nutra/food positioning support the segment growth.

Heavy magnesium carbonate also accounts for a significant market share, supported by its use in broader industrial applications and in selected regulated-use products where denser material characteristics are preferred. The segment expected to grow at a CAGR of 4.3% during the forecast period.

The others segment includes basic magnesium carbonate, magnesium carbonate hydroxide, and specialty synthetic grades, which remain important but more fragmented across niche end uses.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rubber, Plastics & Chemicals Lead Due to Wide Use in Industrial Filler and Formulation Systems

Based on application, the market is segmented into rubber, plastics & chemicals, food additives & food processing, pharmaceuticals, personal care & cosmetics, and others.

Among these, rubber, plastics & chemicals segment is expected to hold the leading magnesium carbonate market share. This dominance is supported by product’s wide use into industrial filler and formulation systems, and suppliers such as LEHVOSS position MgCO3 within broader industrial minerals and chemical application portfolios.

Food additives & food processing segment covers the product use in food manufacturing, baking, pH control, and free-flowing/anticaking functions. ICL specifically offers basic magnesium carbonate for industrial-scale baking, pH control in food, and as a free-flowing agent, while the U.S. eCFR recognizes magnesium carbonate hydroxide for direct food use under good manufacturing practice. This segment is commercially important as it is tied to regulated ingredient demand and tends to demand higher purity and tighter quality consistency than broad industrial uses. The segment expected to grow at a CAGR of 4.7% during the forecast period.

Personal care & cosmetics segment showcases the product use in skin care, makeup, cosmetic powders, and other personal care formulations where absorbency, texture, and formulation performance is crucial.

The others segment includes smaller but commercially relevant applications such as construction materials, nutraceuticals, refractory-related uses, environmental uses, and additional specialty industrial formulations.

MAGNESIUM CARBONATE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Magnesium Carbonate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region combines large-scale mineral supply, major trade activity, and growing downstream demand in food, chemicals, and specialty formulations. In 2024, China was the leading exporter of natural magnesium carbonate, while Indonesia and Japan ranked among the major importers. ICL highlights China-linked compliant manufacturing for basic MgCO3, strengthening the region’s specialty position in addition to its mineral role.

China Magnesium Carbonate Market

China’s market is one of the largest globally, with 2025 revenue at USD 3.63 billion, representing roughly 15.8% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America to register positive growth during the forecast period. North America remains an important market due to stable food, pharmaceutical, and specialty industrial demand. The U.S. regulatory framework explicitly recognizes MgCO3 for direct food use, which supports demand in food processing and nutraceutical-linked applications. The region also benefits from established specialty ingredient distribution and pharmaceutical formulation demand.

U.S. Magnesium Carbonate Market

In 2025, the U.S. represented a USD 3.44 billion market, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 15.0% of global market sales.

Europe

Europe maintains a significant market position due to its mature industrial minerals base, cosmetics regulation framework, and specialty chemicals demand. The EU CosIng system reinforces the relevance of product in cosmetics, while companies such as LEHVOSS offers MgCO3 across industrial minerals, chemicals, and formulation-oriented applications in Europe. This supports both industrial and specialty demand across the region.

Germany Magnesium Carbonate Market

The Germany market in 2025 was valued at around USD 2.28 billion, representing roughly 9.8% of global market revenues.

U.K. Magnesium Carbonate Market

The U.K. market in 2025 was valued at around USD 1.07 billion, representing roughly 4.6% of global market revenues.

Latin America

Latin America is a smaller but relevant market, supported by food processing, personal care, and industrial chemicals. The region is less visible as a major global supply center, hence demand is more likely to be supported through imports and downstream formulation activity rather than dominant local MgCO3 production.

Brazil Magnesium Carbonate Market

Brazil market in 2025 was valued at around USD 1.00 billion, representing roughly 4.3% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller, but opportunities exist in industrial chemicals, food applications, and selected cosmetics and specialty formulations. Growth is likely to depend more on import accessibility and regional industrial development than on a large, highly visible product manufacturing base.

GCC Magnesium Carbonate Market

GCC market in 2025 was valued at around USD 0.82 billion, representing roughly 3.5% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Specialty-Grade Purity, Food/Pharma Compliance, and Application-Led Product Positioning Propels Higher Competition

The global market is moderately fragmented across specialty minerals producers, magnesium-compounds manufacturers, reagent suppliers, and regional marine-chemicals companies. Competition is shaped by purity control, bulk-density range, regulatory compliance for food/pharma/cosmetics, and the ability to supply light, heavy, basic, and specialty magnesium carbonate grades for rubber, food processing, pharmaceuticals, personal care, and industrial chemicals. ICL positions itself as a leading producer of basic magnesium carbonate for pharma, nutraceutical, food, and personal care uses. Additionally, Konoshima markets multiple product grades and newer specialty variants such as plate-shaped magnesium carbonate and synthetic magnesite. Naikai, Dr. Paul Lohmann, and several Indian manufacturers compete through application-specific grades and compliance-linked supply.

LIST OF KEY MAGNESIUM CARBONATE COMPANIES PROFILED

- ICL Group Ltd. (Israel

- Konoshima Chemical Co., Ltd. (Japan)

- Naikai Salt Industries Co., Ltd. (Japan)

- Garrison Minerals, LLC (U.S.)

- AMS Fine Chemicals (India)

- Osian Marine Chemicals Pvt. Ltd. (India)

- Hari Om Fine Chem (India)

- KANTO CHEMICAL CO. INC. (Japan)

- KISHIDA CHEMICAL Co. Ltd. (Japan)

- Lorad Chemical Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: ICL reported that it had introduced various innovative specialties products, while continuing to build its specialties-driven portfolio. Its official product pages show magnesium carbonate within its pharma, food, and personal-care mineral systems, making this relevant to its magnesium carbonate positioning.

- December 2025: AMS Fine Chemicals published multiple magnesium-carbonate-focused product application updates, including articles on food additive uses dated December 22nd, 2025, and on heavy magnesium carbonate in coatings and inks dated December 24th, 2025, showing active commercialization and application development around the product.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several drivers contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 4.6% from 2026 to 2034 |

| Segmentation | By Type, By Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 22.92 billion in 2025 and is projected to reach USD 34.07 billion by 2034.

Recording a CAGR of 4.6%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The rubber, plastics & chemicals segment is expected to lead market during the forecast period.

Asia Pacific held the highest market share in 2025.

Rising demand from food, pharma, and personal care applications supports market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us