Marine Composites Market Size, Share & Industry Analysis, By Fiber Type (Glass fiber (GFRP), Carbon fiber (CFRP), and Others), By Resin Type (Polyester, Vinyl Ester, Epoxy, and Others), By Application (Power Boats, Sailboats & Yachts, Commercial & Workboats, Cruise ships & Large Passenger Vessels, Offshore & Marine Structures, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

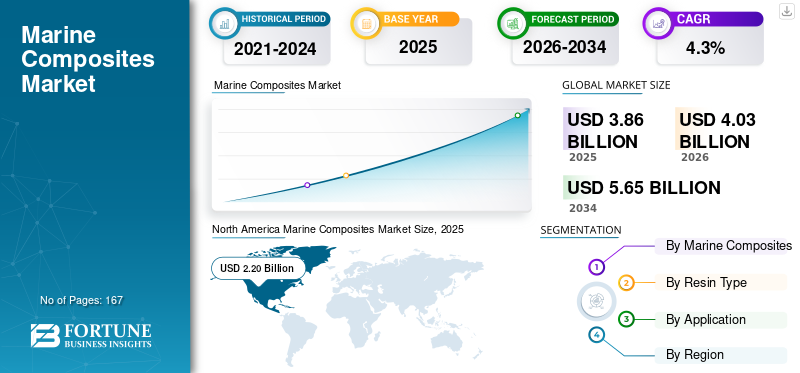

The global marine composites market size was valued at USD 3.86 billion in 2025. The market is projected to grow from USD 4.03 billion in 2026 to USD 5.65 billion by 2034, exhibiting a CAGR of 4.3% during the forecast period. North America dominated the global marine composites market with a market share of 56.99% in 2025.

Marine composites are engineered structural materials designed to deliver high strength, durability, and weight reduction across a wide range of vessel types. Their ability to improve load-bearing performance, resist corrosion, and enhance fuel efficiency makes them increasingly essential in powerboats, sailboats, and yachts, commercial and workboats, and cruise and passenger vessels, where traditional metals increasingly fall short against modern performance and lifecycle expectations. As designers push for lighter hulls, improved hydrodynamics, and reduced maintenance requirements, composites provide the structural reliability and manufacturing flexibility needed for next-generation marine platforms.

The market is shaped by leading global composite producers with strong capabilities across fiber reinforcements, resin chemistry, and core-material engineering. Top players include Owens Corning, Toray Industries, Hexcel Corporation, Gurit Holding, and Mitsubishi Chemical Group. Their portfolios span glass and carbon fibers, epoxy and polyester resin systems, and advanced core solutions that support evolving design and performance demands across both leisure and commercial marine applications. Close collaboration with boatbuilders and sustained investment in infusion-ready materials, recyclability, and higher-strength laminates reinforce their influence as composite adoption accelerates across the marine industry.

Download Free sample to learn more about this report.

Marine Composites Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.86 billion

- 2026 Market Size: USD 4.03 billion

- 2034 Forecast Market Size: USD 5.65 billion

- CAGR: 4.3% from 2026–2034

- North America dominated the marine composites market with a 56.99% share in 2025.

- The Glass Fiber Reinforced Plastic (GFRP) segment held the largest market share in 2025.

- The polyester resin segment accounted for the leading share of the market in 2025.

North America

North America led the global market in 2025, supported by a strong recreational boating industry and high composite adoption.

Europe

Europe maintained significant demand due to its established yacht and sailboat manufacturing sector.

Asia Pacific

Asia Pacific emerged as a fast-growing market driven by expanding boatbuilding activities and coastal tourism.

U.S.

U.S. The country remains the largest consumer of marine composites, supported by extensive production of recreational and performance boats.

Japan

Japan Demand is supported by advanced shipbuilding capabilities and increasing use of composites in specialized marine applications.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Lightweight and Fuel-Efficient Vessel Designs Is Accelerating the Product Adoption

Rising performance and efficiency expectations across the marine industry are encouraging builders to shift toward composite materials that deliver meaningful weight reduction and improved hydrodynamics. Glass-and carbon-fiber composite systems offer higher strength-to-weight ratios than steel or aluminum, enabling manufacturers to lower fuel consumption, enhance speed, and meet emerging environmental and operational requirements. These advantages are becoming increasingly important across power boats, sailboats and yachts, commercial and workboats, and offshore structures where weight optimization directly influences cost and performance outcomes.

Beyond performance gains, composites support more versatile design approaches, longer material lifespans, and reduced corrosion-related maintenance, making them well-suited for operators seeking reliable materials with lower upkeep demands over the vessel’s service life. With efficiency regulations tightening and builders looking for performance-led differentiation, composite materials are steadily moving from specialized applications into mainstream marine construction.

- The International Maritime Organization’s EEXI and CII measures are encouraging vessel owners to adopt technologies that improve operational efficiency, reinforcing the shift toward composite-based marine designs.

MARKET RESTRAINTS

High Material Costs and Complex Production Processes to Limit Market Development

Marine composites remain significantly more expensive than traditional materials such as steel and aluminum due to higher raw material prices, specialized tooling needs, and labor-intensive fabrication methods. These cost pressures are particularly challenging for commercial and workboat builders, which typically operate on tight budgets and prioritize predictable, low-variance production cycles. The requirement for skilled technicians and controlled manufacturing environments adds another barrier, making it difficult for smaller yards to scale composite usage beyond selective components. As a result, cost sensitivity and manufacturing complexity continue to slow broader adoption of composite structures across cost-driven marine segments.

- Composite manufacturing often requires additional labor and processing steps compared with metals, leading to higher production costs in many marine applications, as noted by industry assessments from the American Composites Manufacturers Association.

MARKET OPPORTUNITIES

Growing Interest In Electric and Hybrid Propulsion Systems is Opening New Pathways for Market Expansion

The shift toward lower-emission and environmentally responsible marine operations is creating strong opportunities for composite materials, which offer longer service life, reduced corrosion, and improved fuel efficiency. Shipyards and vessel operators are increasingly evaluating and prioritizing materials that enable cleaner operations and lower lifecycle impacts, and composites align well with these priorities through lighter structures and reduced maintenance needs. Rising interest in electric and hybrid propulsion systems also supports composite uptake, as lighter hulls extend range and improve energy efficiency. These trends position composites as strategic materials for next-generation leisure, commercial, and offshore vessels as sustainability moves from a competitive advantage to an industry requirement.

- The International Maritime Organization has set targets to reduce greenhouse gas emissions from international shipping by at least 20 percent by 2030, encouraging the use of lighter and more efficient vessel materials.

MARINE COMPOSITES MARKET TRENDS

Increasing Use of Automation Technologies is Reshaping the Marine Sector

Marine builders are steadily adopting advanced processes such as resin infusion, vacuum-assisted molding, and automated fiber placement to improve part consistency, reduce labor intensity, and enhance structural performance. These technologies allow more precise control over fiber orientation and resin distribution, which results in lighter and stronger components while also reducing material waste. As quality expectations rise across leisure and commercial segments, automated and closed-mold techniques are becoming key enablers for scaling composite production and supporting more complex vessel designs. Automation is gaining traction as yards seek greater process repeatability, cleaner production environments, and reduced dependency on manual lay-up for high-performance composite structures.

MARKET CHALLENGES

Limited Repair Infrastructure and Skill Availability to Limit Market Growth

A major challenge for the market is the shortage of repair facilities and technicians trained to diagnose and restore composite damage. Unlike metal structures, composite components require specialized inspection methods, controlled repair environments, and skilled laminators to ensure structural integrity after impact or fatigue events. Many commercial operators and regional shipyards lack this capability, which increases perceived operational risk and discourages wider adoption, especially in segments where fast turnaround times and predictable maintenance are critical.

Industry associations note that composite repair demands specialized expertise and tightly controlled processes, and the lack of standardized repair networks continues to limit adoption across commercial marine fleets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Fiber Type

GFRP Segment Led the Market Due to Its Property

Based on fiber type, the market is segmented into Glass fiber (GFRP), Carbon fiber (CFRP), and others.

To know how our report can help streamline your business, Speak to Analyst

The Glass fiber (GFRP) segment accounted for a dominant marine composites market share in 2025. GFRP dominates the market as it offers an optimal combination of mechanical performance, corrosion resistance, and cost efficiency, making it suitable for high-volume production across power boats, sailboats, workboats, and a wide range of structural and semi-structural components. Its processing flexibility in methods such as infusion and hand layup allows builders to achieve consistent quality at manageable production costs, which is especially important for mid-size and recreational vessels. As design demands evolve toward lighter and more durable hulls, GFRP continues to provide the most practical pathway for balancing performance with manufacturability across both leisure and commercial segments.

GFRP is widely recognized by industry bodies such as the American Composites Manufacturers Association for delivering the best cost-to-performance ratio in marine applications, reinforcing its position as the most commonly used composite material in boatbuilding.

By Resin Type

Polyester Segment Led the Market Due to Its Cost Efficiency

In terms of resin type, the market is categorized into polyester, vinyl ester, epoxy, and others.

The polyester segment accounted for the largest share in 2025 as it offers a strong balance of affordability, durability, and processing ease, which supports large-scale production across hulls, decks, and structural components. Its compatibility with GFRP and conventional open- and closed-mold processes allows builders to achieve consistent laminate quality without significant cost escalation, making it the preferred choice for recreational boats and workboat platforms. As manufacturers prioritize dependable performance and predictable curing behavior for medium to high-volume production, polyester resin continues to anchor the material selection in mainstream marine construction.

Polyester remains the most widely used resin system in fiberglass-reinforced composites, as reported across industry references such as the American Composites Manufacturers Association, due to its combination of low cost and reliable mechanical performance.

By Application

Power Boats Segment Held the Leading Share Due to High Composite Usage in Performance-Driven Hull and Deck Structures

In terms of application, the market is categorized into power boats, sailboats & yachts, commercial & workboats, cruise ships & large passenger vessels, offshore & marine structures, and others.

The power boats segment accounted for the largest share in 2025 as manufacturers rely extensively on lightweight GFRP and advanced resin systems to achieve higher speeds, improved fuel efficiency, and better handling characteristics. Composites enable complex hull geometries, superior corrosion resistance, and reduced maintenance requirements, all of which are critical in recreational and performance boating. With sustained demand for sport boats, fishing vessels, and leisure craft, power boat builders continue to integrate more composite-intensive designs to meet customer expectations for durability and on-water performance.

Advances in resin infusion and vacuum molding have enabled power boat manufacturers to produce larger, stiffer one-piece hulls, improving structural integrity and reducing assembly time compared with traditional multi-part hull construction.

The offshore & marine structures segment is expected to grow at a CAGR of 4.9% over the forecast period.

Marine Composites Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Marine Composites Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 2.20 billion. North America holds the dominant share of the marine composites market, supported by a large and mature recreational boating industry and strong demand for composite-intensive power boats and sport craft. The U.S. leads regional consumption, with extensive use of GFRP and polyester resin systems across runabouts, fishing boats, pontoons, and performance vessels. Composite materials remain central to builder strategies focused on weight reduction, durability, and cost-effective manufacturing.

- According to the National Marine Manufacturers Association, the U.S. produces more than 95 % of its recreational boats domestically, and the majority of these vessels are fiberglass-based, directly reinforcing North America’s high composite consumption.

To know how our report can help streamline your business, Speak to Analyst

Europe's marine composites market maintains solid demand, supported by its strong yacht and sailboat manufacturing footprint and continuous advancement in composite technologies. Italy, France, Germany, and the Netherlands host many of the world’s leading yacht and performance boat builders, where carbon fiber and high-performance resin systems are increasingly adopted to improve stiffness, speed, and fuel efficiency. Strengthening environmental expectations around vessel efficiency further strengthens composite relevance in the region.

Europe is home to several of the world’s largest yacht manufacturers, including builders in Italy, France, and Germany, collectively producing tens of thousands of composite-intensive boats annually, which supports high demand for advanced GFRP and CFRP systems.

Asia Pacific follows as a major and fast-growing market, driven by an expanding boatbuilding base, rising coastal tourism, and increasing use of composites in commercial and offshore applications. China anchors regional demand, while Japan and South Korea support higher-value segments through shipbuilding and specialized marine platforms. Composites are gaining traction across the region due to their corrosion resistance and ease of maintenance, characteristics well-suited to warm and high-salinity operating environments.

Latin America remains a developing but gradually expanding market, supported by coastal tourism, sport fishing, and increased interest in small recreational craft. Brazil and Mexico lead regional demand, with composite boats favored for their lower maintenance requirements and resistance to corrosion in tropical marine environments. Latin America's marine composites market growth is moderate and tends to correlate with broader economic and tourism trends across key coastal regions.

The Middle East & Africa region remains in the early stages of broader composite adoption, but it shows clear pockets of opportunity. Gulf countries support demand through marina expansion, yacht ownership growth, and offshore service operations where composite durability is valued. In Africa, the composite market is more selective but growing, particularly in small-boat production. Fiberglass is favored for its resilience and lower lifecycle, reduced upkeep compared with traditional materials, making it well-suited to local operating conditions. As regional infrastructure and marine recreation evolve, composite usage is expected to rise gradually.

Countries such as the UAE and Saudi Arabia are investing in marinas and waterfront tourism, leading to a rising number of composite leisure boats entering the regional fleet, particularly in premium yacht segments and charter operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation and Structural Performance are Defining Competitive Positioning

Advances in fiber reinforcements, resin chemistries, and optimized processing methods are intensifying competition in the marine composites market. Suppliers are differentiating by delivering materials that improve lightweighting, durability, and production efficiency across power boats, sailboats and yachts, commercial vessels, and offshore structures. As builders focus on fuel efficiency, corrosion resistance, and lifecycle performance, companies offering strong technical support and application expertise are gaining a meaningful competitive edge.

The top players include Owens Corning, Toray Industries, Hexcel Corporation, Gurit Holding, and Mitsubishi Chemical Group. These firms anchor the market with broad portfolios spanning glass and carbon fibers, epoxy and polyester resins, core materials, and engineered prepregs used in structural and semi-structural marine components. Their global scale, depth in marine-grade material, and continuous investment in infusion-ready systems and higher-strength laminates reinforce their leadership positions.

Moreover, competitive focus centers on lighter core technologies, more efficient resin systems, and advanced fiber formats that support next-generation vessel designs. Companies that combine material innovation with processing know-how and design-stage collaboration are best positioned to capture growth as composite adoption expands across both leisure and commercial marine segments.

LIST OF KEY MARINE COMPOSITES COMPANIES PROFILED

- Owens Corning. (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- Hexcel Corporation (U.S.)

- Gurit Services AG (Switzerland)

- Mitsubishi Chemical Corporation (Japan)

- SGL Carbon (Germany)

- Hexion Inc (U.S.)

- Huntsman International LLC. (U.S.)

- AOC (U.S.)

- Scott Bader Company Ltd (UK)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Hexcel and HyPerComp unveiled an advanced Type IV composite pressure vessel built with HexTow IM11-R carbon fiber. Although targeted at high-pressure gas storage, such technologies are increasingly relevant to next-generation marine propulsion systems, particularly hydrogen-powered vessels requiring lightweight, robust storage modules.

- September 2025: Gurit announced a multi-year contract to supply its Corecell SAN structural foam to the subsea sector and confirmed plans to open a new manufacturing site near Brisbane. Corecell’s proven performance in wet, pressure-intensive environments reinforces its strong position in marine hulls, decks, and offshore structures where damage tolerance and long-term durability are essential.

- June 2025: Hexcel signed a five-year partnership agreement with Kongsberg Defence & Aerospace for the supply of HexWeb honeycomb and HexPly prepregs. While primarily supporting defense platforms, the agreement strengthens Hexcel’s broader composite supply capabilities, which benefit marine builders relying on similar honeycomb and prepreg technologies for high-strength, lightweight structural components.

- March 2025: Arkema entered a circular-economy alliance with Groupe Beneteau, Veolia, Composite Recycling, Owens Corning, and Chomarat to advance recyclable composite solutions for boat manufacturing. Using Arkema’s Elium resin and recycled glass fibers, the collaboration supports closed-loop production models and reduces lifecycle emissions, directly aligning with the marine sector’s growing focus on sustainability.

- February 2025: Scott Bader introduced new Crestapol resin developments at JEC World 2025, including Crestapol 1240, designed to simplify bulkhead bonding and reduce surface preparation in boatyards. The improved processing efficiency and reduced dust generation offer clear benefits for marine builders seeking faster, cleaner, and more consistent composite fabrication.

REPORT COVERAGE

The global marine composites market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.3% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Fiber Type, Resin Type, Application, and Region |

|

By Fiber Type |

· Glass fiber (GFRP) · Carbon fiber (CFRP) · Others |

|

By Resin Type |

· Polyester · Vinyl Ester · Epoxy · Others |

|

By Application |

· Power Boats · Sailboats & Yachts · Commercial & Workboats · Cruise ships & Large Passenger Vessels · Offshore & Marine Structures · Others |

|

By Geography |

· North America (By Fiber Type, By Resin Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Fiber Type, By Resin Type, Application, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Fiber Type, By Resin Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Fiber Type, By Resin Type, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Fiber Type, By Resin Type, Application, and Country/Sub-region) o Saudi Arabia (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.86 billion in 2025 and is projected to reach USD 5.65 billion by 2034.

Recording a CAGR of 4.3%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The power boats segment led in 2025.

North America held the highest market share in 2025.

Increasing use of automation technologies are some of the factors that are expected to favor the product adoption.

Owens Corning, Toray Industries, Hexcel Corporation, Gurit Holding, and Mitsubishi Chemical Group are some of the prominent players in the market.

Increasing demand for lightweight and fuel-efficient vessel designs is the key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us