Marine Fuel Optimization Market Size, Share & Industry Analysis, By Solution Type (Voyage Optimization, Performance Monitoring & Analytics, Fleet Management & Decision Support Systems, Advisory & Optimization Services, and Others), By Deployment Mode (Onboard Systems, Cloud-Based Solutions, and Hybrid) , By Vessel Type (Commercial Shipping, Offshore Vessels, Passenger Vessels, Naval & Defense Vessels, and Others) By End-User (Fleet Operators / Shipping Companies, Charterers, Ship Management Companies, Naval & Defense Authorities, and Others) and Regional Forecast, 2026-2034

Marine Fuel Optimization Market Size and Future Outlook

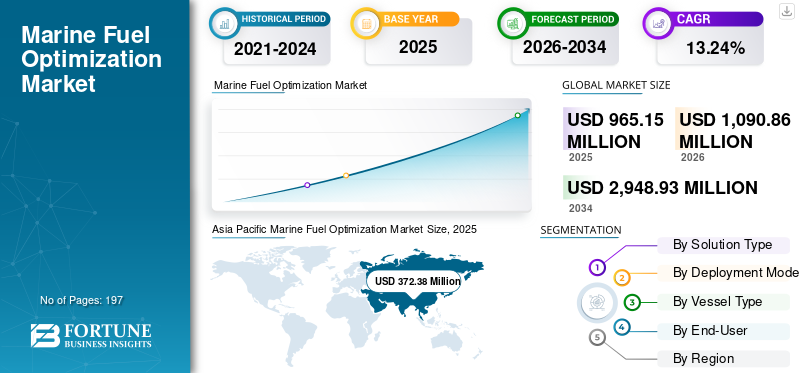

The global marine fuel optimization market size was valued at USD 965.15 million in 2025. The market is projected to grow from USD 1,090.86 million in 2026 to USD 2,948.93 million by 2034, exhibiting a CAGR of 13.24% during the forecast period. Asia Pacific dominated the marine fuel optimization market with a market share of 38.58% in 2025.

Marine fuel optimization systems are critical solutions used in modern maritime operations to enhance fuel efficiency, reduce emissions, and improve overall vessel performance. These systems enable ship operators to monitor, analyze, and optimize fuel consumption through advanced technologies such as real-time data analytics, voyage optimization tools, engine performance monitoring, and weather routing. Unlike traditional fuel management practices, MFO solutions leverage digital platforms, onboard sensors, and cloud-based analytics to deliver precise insights into operational efficiency, enabling informed decision-making. Widely deployed across commercial shipping, offshore vessels, passenger fleets, and naval operations, these systems support stable and efficient vessel operations while addressing stringent performance and environmental requirements, making them an essential component of modern maritime digitalization.

The demand for MFO solutions is witnessing steady growth, driven by rising fuel costs, increasing global shipping activity, and the need to comply with stringent environmental regulations aimed at reducing greenhouse gas emissions. The expansion of international trade, coupled with the growing adoption of digital and smart shipping technologies, is accelerating the integration of optimization systems across fleets. Additionally, advancements in data analytics, artificial intelligence, and connectivity are enabling more accurate and predictive fuel management capabilities. Trends such as fleet digitalization, autonomous shipping initiatives, and increased focus on operational efficiency are further supporting market growth. Moreover, regulatory frameworks emphasizing sustainability and emission reduction are encouraging shipowners and operators to invest in advanced fuel optimization technologies, thereby driving the adoption of efficient and intelligent marine fuel management solutions.

The global market is moderately fragmented, characterized by the presence of established maritime technology providers alongside a wide range of regional and specialized solution vendors operating across international shipping markets. Key participants such as Wärtsilä Corporation, Kongsberg Gruppen, ABB Ltd., DNV, and Siemens Energy maintain a strong market presence through comprehensive portfolios that include voyage optimization, performance monitoring, and digital fleet management solutions. At the same time, numerous small and mid-sized companies offer application-specific, cost-effective, and customized solutions, intensifying competition within the market. Market players are increasingly focusing on advancements in data analytics, artificial intelligence, real-time monitoring systems, and integration with onboard and cloud-based platforms to meet evolving operational and regulatory requirements. Strategic initiatives such as collaborations with shipping companies, expansion of digital capabilities, and penetration into emerging maritime markets are shaping the competitive landscape and supporting long-term growth of the market.

Download Free sample to learn more about this report.

Marine Fuel Optimization Market KEY TAKEAWAYS

- 2025 Market Size: USD 965.15 million

- 2026 Market Size: USD 1,090.86 million

- 2034 Forecast Market Size: USD 2,948.93 million

- CAGR: 13.24% from 2026–2034

- Asia Pacific dominated the marine fuel optimization market with a 38.58% share in 2025.

- The voyage optimization segment held the largest solution type share at 27.99% in 2025.

- The onboard systems segment led the deployment mode with a 50.69% share in 2025.

Asia Pacific

Asia Pacific dominated the market with a value of USD 372.38 million and a 38.58% market share in 2025.

Europe

Europe accounted for USD 277.32 million of the global marine fuel optimization market in 2025.

North America

North America reached a market size of USD 177.71 million in 2025, supported by strong digital maritime adoption.

U.S.

The U.S. marine fuel optimization market was valued at USD 143.96 million in 2025.

Japan

The market reached USD 105.23 million in 2025, driven by advanced maritime technologies and fuel efficiency initiatives.

Read More

Marine Fuel Optimization Market Trends

Increasing Adoption of Digitalization and Data-Driven Solutions is Driving Market Growth

The growing adoption of digital technologies and data-driven decision-making in the maritime industry is significantly accelerating the market. Ship operators and fleet managers are increasingly integrating advanced solutions such as real-time monitoring systems, AI-based analytics, and cloud-enabled platforms to enhance fuel efficiency and operational performance. These systems provide actionable insights into vessel operations, including voyage planning, engine performance, and fuel consumption patterns, enabling operators to make informed decisions that reduce fuel costs and improve overall efficiency. As global shipping companies strive to optimize fleet performance while maintaining cost competitiveness, the demand for intelligent fuel optimization solutions continues to rise.

Furthermore, the maritime industry’s transition toward smart shipping and connected vessels is reinforcing the adoption of digital optimization tools. The integration of Internet of Things (IoT) sensors, predictive analytics, and automated decision-support systems is enabling continuous monitoring and optimization of vessel performance under varying operational and environmental conditions. Additionally, increasing pressure from regulatory bodies to reduce emissions and improve energy efficiency is compelling shipping companies to adopt advanced digital solutions. These systems not only help in compliance with environmental standards but also contribute to reduced fuel consumption and lower operational risks.

For instance, in 2025, Maersk and Hapag-Lloyd continued expanding the use of digital fleet optimization platforms and real-time performance monitoring tools to improve fuel efficiency and reduce carbon emissions. Similarly, CMA CGM advanced its fleet efficiency programs through the integration of data-driven operational optimization systems. In parallel, technology providers including Wärtsilä, Kongsberg Digital, ABB, and DNV strengthened collaborations with shipping companies to deploy AI-enabled voyage optimization, weather routing, and performance analytics solutions. Further, supporting enhanced operational efficiency and regulatory compliance across global fleets.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Fuel Cost Pressures and Need for Operational Efficiency are Driving Market Growth

The increasing pressure on shipping companies to reduce fuel consumption and optimize operational costs is a major driver of the marine fuel optimization market growth. Fuel expenses account for a significant portion of overall vessel operating costs, prompting shipowners and operators to adopt advanced solutions focused on optimizing fuel usage and improving overall efficiency. MFO systems enable real-time monitoring, data analytics, and performance tracking, allowing operators to make informed decisions related to voyage planning, speed optimization, and engine performance. These capabilities help reduce fuel wastage, improve fleet management efficiency, and enhance profitability in a highly competitive shipping environment.

In addition, the growing global trade volumes and expansion of maritime transportation are increasing the demand for advanced fleet management systems capable of handling large and complex operations. As shipping companies operate diverse fleets, the need for centralized monitoring, cross-fleet optimization, and cross-fleet standardization is becoming critical. These platforms enable operators to benchmark vessel performance, standardize operational practices, and ensure consistent fuel efficiency across fleets. The integration of digital technologies such as artificial intelligence, IoT, and predictive analytics is further enhancing the effectiveness of these systems, supporting improved decision-making and large-scale fuel optimization strategies.

For instance, in 2025, shipping companies such as Maersk and Hapag-Lloyd expanded the use of digital fleet optimization platforms and real-time performance monitoring systems to improve fuel efficiency and reduce operational costs. Further, highlighting the increasing importance of fuel optimization technologies in modern maritime operations.

MARKET RESTRAINTS

High Implementation Costs and Integration Complexity are Restraining Market Growth

The high initial investment and complexity associated with the deployment of marine fuel optimization systems act as key restraints for market growth. Implementing these solutions requires the integration of advanced hardware components such as sensors and onboard systems, along with sophisticated software platforms for data analytics and monitoring. This can lead to significant upfront costs, particularly for small and mid-sized shipping companies, limiting widespread adoption.

Moreover, integrating fuel optimization solutions with existing fleet management infrastructure can be technically challenging. Variations in vessel types, legacy systems, and operational conditions make it difficult to achieve seamless integration and effective cross-fleet standardization. These challenges hinder the ability of operators to implement uniform fuel consumption monitoring and optimization strategies across fleets, reducing the overall efficiency of deployed systems. Data accuracy, system compatibility, and crew training also present challenges, as effective utilization of these systems depends on proper configuration and user expertise.

For instance, in 2024, maritime technology providers such as Wärtsilä, Kongsberg Digital, ABB Marine & Ports, and DNV highlighted challenges related to integrating digital optimization platforms with legacy vessel systems. Further, emphasizing the technical and financial barriers associated with large-scale deployment.

MARKET OPPORTUNITIES

Stringent Emission Regulations and Decarbonization Initiatives are Creating Growth Opportunities

The increasing focus on reducing greenhouse gas emissions in the maritime sector is creating significant growth opportunities for the market. Regulatory bodies such as the International Maritime Organization (IMO) are implementing stringent measures, including Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII), compelling shipowners to adopt fuel-efficient technologies. MFO systems play a crucial role in helping operators comply with these regulations by improving fuel efficiency and reducing emissions.

Furthermore, the transition toward sustainable shipping practices and alternative fuels is increasing the complexity of vessel operations, thereby driving the need for advanced optimization solutions. These systems help manage multi-fuel operations, optimize energy usage, and support decarbonization strategies. The growing adoption of digital twins, predictive maintenance, and AI-driven analytics is also creating new opportunities for solution providers to offer advanced, value-added services.

For instance, in 2025, companies such as Wartsila and Kongsberg Digital expanded their digital maritime solutions to support emission reduction and regulatory compliance, reflecting the growing demand for advanced fuel optimization technologies.

MARKET CHALLENGES

Data Reliability and Lack of Standardization are Challenging Market Expansion

Ensuring data accuracy and standardization across diverse vessel systems remains a significant challenge for the market. These systems rely heavily on data collected from onboard sensors, engine systems, and external environmental inputs. Inconsistent data quality, sensor inaccuracies, and variations in measurement standards can impact the effectiveness of optimization algorithms and lead to suboptimal decision-making.

Additionally, the lack of standardized frameworks for data integration across different vessel types and systems creates challenges in implementing uniform optimization solutions. Shipping companies often operate mixed fleets with varying technologies, making it difficult to achieve seamless integration and consistent performance monitoring. This complexity can limit scalability and hinder the full potential of fuel optimization systems.

For instance, in 2025, maritime solution providers such as DNV emphasized the importance of data standardization and digital integration frameworks. Further, to improve the accuracy and effectiveness of vessel performance and fuel optimization systems, highlighting ongoing challenges in the market.

Segmentation Analysis

By Solution Type

Voyage Optimization Gains Prominence with Increasing Focus on Route Efficiency and Cost Reduction

Based on solution type, the global market is segmented into voyage optimization, performance monitoring & analytics, fleet management & decision support systems, advisory & optimization services, and others.

The voyage optimization segment dominated the market, accounting for 27.99% share in 2025, driven by its critical role in reducing fuel consumption through efficient route planning, weather routing, and speed optimization. Voyage optimization solutions are widely adopted across commercial shipping fleets, including container ships, bulk carriers, and tankers, as they enable operators to minimize fuel usage while maintaining schedule reliability. The increasing volatility in fuel prices and the need to improve operational efficiency are further encouraging shipowners to deploy advanced voyage planning tools integrated with real-time weather and sea condition data.

The performance monitoring & analytics segment is emerging as the fastest-growing segment, accounting for a CAGR of 15.59% during the forecast period. This growth is driven by the increasing adoption of data-driven decision-making and digital fleet management practices. These solutions provide real-time insights into engine performance, fuel consumption patterns, and vessel efficiency, enabling predictive maintenance and continuous optimization.

By Deployment Mode

Onboard Systems Maintain Market Leadership Owing to Reliability and Real-Time Operational Control

Based on deployment mode, the global market is segmented into onboard systems, cloud-based solutions, and hybrid.

The onboard systems segment dominated the market, accounting for 50.69% of marine fuel optimization market share in 2025, driven by its widespread installation across existing vessel fleets and its ability to provide real-time monitoring and control without reliance on external connectivity. These systems are highly preferred by ship operators for their reliability, data security, and direct integration with vessel equipment such as engines and navigation systems. Onboard solutions enable continuous tracking of fuel consumption, engine performance, and operational parameters, making them essential for immediate decision-making during voyages.

The cloud-based solutions segment is emerging as the fastest-growing segment, accounting for a CAGR of 16.68% during the forecast period. This growth is driven by the increasing digitalization of the maritime industry and the need for centralized fleet management.

By Vessel Type

Commercial Shipping Segment Dominates Due to High Fuel Consumption and Extensive Fleet Operations

Based on vessel type, the global market is segmented into commercial shipping, offshore vessels, passenger vessels, naval & defense vessels, and others.

The commercial shipping segment dominated the market, accounting for 45.75% share in 2025, driven by the large number of vessels operating in global trade and their high fuel consumption levels. Container ships, bulk carriers, and tankers rely heavily on fuel optimization solutions to reduce operational costs and improve efficiency across long-haul routes. The increasing volume of international trade and pressure to maintain profitability amid fluctuating fuel prices are key factors supporting the dominance of this segment.

The offshore vessels segment is emerging as the fastest-growing segment, accounting for a CAGR of 14.96% during the forecast period. This growth is driven by rising offshore oil & gas exploration activities and increasing demand for support vessels such as OSVs and drill ships. These vessels operate under complex and variable conditions, requiring advanced fuel optimization and performance monitoring solutions to enhance efficiency and reduce operational risks.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Fleet Operators/Shipping Companies Drive Market Demand Through Continuous Emphasis on Fuel Cost Management

Based on end-user, the global market is segmented into fleet operators/shipping companies, charterers, ship management companies, naval & defense authorities, and others.

The fleet operators/shipping companies segment dominated the market, and accounted for 41.21% share in 2025, driven by their direct responsibility for fuel costs and operational efficiency. These companies are the primary adopters of fuel optimization systems as they seek to reduce fuel expenses, improve voyage efficiency, and enhance overall fleet performance. The growing need to comply with emission regulations and maintain competitive advantage is further driving adoption among fleet operators.

The ship management companies segment is emerging as the fastest-growing segment, accounting for a CAGR of 14.43% during the forecast period. This growth is driven by the increasing outsourcing of vessel operations to third-party management firms.

Marine Fuel Optimization Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Marine Fuel Optimization Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market, accounting for approximately USD 372.38 million in 2025. The market in Asia Pacific is growing due to the region’s strong maritime trade activity, large commercial shipping fleet, and increasing adoption of digital maritime solutions across countries such as China, Japan, South Korea, and Southeast Asia. The region benefits from high vessel density, expanding shipbuilding activities, and rising fuel cost pressures, which are encouraging shipowners to adopt advanced optimization technologies. Additionally, growing regulatory focus on emission reduction and increasing investments in smart shipping and port digitalization are further supporting market growth.

China Marine Fuel Optimization Market

In 2025, the China market reached approximately USD 105.18 million. The market is growing due to China’s dominance in global shipping, large fleet operations, and rapid adoption of digital fleet management and performance monitoring systems. Increasing investments in smart ports and maritime digitalization are further accelerating demand.

Japan Marine Fuel Optimization Market

The Japan market in 2025 was valued at around USD 105.23 million. Growth is driven by strong ship ownership, advanced maritime technologies, and increasing focus on operational efficiency and emission compliance. Japanese shipping companies are actively integrating fuel optimization systems to improve fleet performance.

North America

North America was valued at approximately USD 177.71 million in 2025. The market in North America is growing due to the presence of large fleet operators, increasing adoption of digital shipping technologies, and strong regulatory emphasis on emission reduction. The region is witnessing rising investments in fleet optimization platforms, data analytics, and connected vessel technologies to improve operational efficiency and sustainability.

U.S. Marine Fuel Optimization Market

The U.S. market was analytically approximated at USD 143.96 million in 2025. Growth is driven by the expansion of maritime logistics, increasing adoption of AI-based optimization tools, and strong focus on reducing fuel consumption across commercial and defense fleets.

Europe

The Europe region accounted for approximately USD 277.32 million in 2025. The market in Europe is growing due to stringent environmental regulations, including IMO and EU emission standards, and strong adoption of advanced digital maritime solutions. The region is at the forefront of maritime decarbonization, driving the adoption of fuel optimization technologies across commercial and offshore fleets.

Norway Marine Fuel Optimization Market

The Norway market was valued at around USD 58.52 million in 2025. The market is supported by advanced maritime technologies, offshore activities, and early adoption of digital optimization solutions.

Germany Marine Fuel Optimization Market

The German market in 2025 was valued at around USD 44.97 million. The growth is driven by strong shipping industry presence, increasing digitalization, and adoption of fleet optimization systems.

Latin America

Latin America accounted for approximately USD 91.35 million in 2025. The market is growing due to increasing maritime trade, rising fuel costs, and gradual adoption of digital optimization solutions. Countries such as Brazil and Mexico are witnessing increased demand driven by offshore oil & gas activities and growing shipping operations.

Brazil Marine Fuel Optimization Market

The Brazil market in 2025 was valued at around USD 37.07 million. The growth is driven by strong offshore operations and increasing focus on fuel efficiency in tanker and support vessels.

Middle East & Africa

The Middle East & Africa region accounted for approximately USD 46.39 million in 2025. The market is growing due to expanding oil & gas shipping activities, increasing investments in maritime infrastructure, and rising adoption of fuel optimization technologies to reduce operational costs and emissions.

GCC Marine Fuel Optimization Market

The GCC market in 2025 was valued at around USD 20.23 million. Growth is driven by high tanker traffic, strong maritime trade routes, and increasing adoption of digital optimization systems across major shipping hubs such as the UAE and Saudi Arabia.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players in the Global Market are Focusing on High-Efficiency Designs and Advanced Power Conversion Technologies

The marine fuel optimization market is moderately fragmented, characterized by the presence of established maritime technology companies alongside specialized digital solution providers and regional vessel performance analytics firms. Leading participants such as Wärtsilä, ABB, Kongsberg Maritime/Kongsberg Digital, and DNV maintain strong positions through portfolios spanning voyage optimization, fleet performance management, fuel and emissions monitoring, and compliance-focused digital tools. Wärtsilä positions fleet optimization around cloud analytics, AI, intelligent automation, route planning, vessel performance tracking, and CII management, while Kongsberg highlights fuel and emissions performance tools, voyage optimization, and real-time vessel dashboards aimed at lowering fuel costs and emissions. ABB is active in voyage optimization and routing services, including speed-routing capabilities, and DNV remains influential through voyage optimization training, ship energy-efficiency guidance, and decarbonization-oriented advisory offerings.

In 2025, Wartsila continued emphasizing AI-powered vessel efficiency, digital twins, and fleet optimization, while also supplying efficiency-focused propulsion and control solutions for new Dutch vessels equipped with EcoControl. Meanwhile, DNV published new guidance in 2025 to help shipowners select energy-efficiency measures and technologies, reinforcing its role in the broader vessel efficiency and fuel optimization ecosystem.

LIST OF KEY MARINE FUEL OPTIMIZATION COMPANIES PROFILED

- Wartsila (Finland)

- ABB (Switzerland)

- Kongsberg Maritime (Norway)

- DNV / StormGeo (Norway)

- Siemens Energy (Germany)

- NAVTOR (Norway)

- NAPA (Finland)

- ZeroNorth (Denmark)

- Veson Nautical (U.S.)

- Marorka (Iceland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Wartsila continued expanding its AI-driven fleet optimization and voyage performance solutions, focusing on improving fuel efficiency and supporting compliance with carbon intensity regulations (CII). The company emphasized the integration of real-time analytics, digital twins, and predictive modeling to enhance vessel operational efficiency across global fleets.

- February 2026: Kongsberg Digital strengthened its Vessel Insight and performance analytics platform, enabling ship operators to leverage cloud-based data for real-time fuel optimization and emissions monitoring. The platform enhancements are aimed at improving decision-making and supporting digital transformation across maritime operations.

- November 2025: DNV (through StormGeo) expanded its weather routing and voyage optimization services, offering advanced decision-support tools to improve route planning and minimize fuel usage under varying environmental conditions. This expansion highlights the growing importance of data-driven operational optimization.

- September 2025: ABB Marine & Ports advanced its Advisory and Voyage Optimization solutions, incorporating enhanced weather routing, speed optimization, and energy efficiency modules to help vessels reduce fuel consumption and meet sustainability targets. The development reflects increasing demand for integrated digital optimization systems.

- May 2025: ZeroNorth enhanced its AI-powered optimization platform to support multi-vessel fleet performance tracking, emissions reduction, and fuel consumption optimization. The company continues to focus on enabling decarbonization through digital maritime solutions and advanced analytics.

REPORT COVERAGE

The global marine fuel optimization market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.24% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Solution Type, Deployment Mode, Vessel Type, End-User, and Region |

| By Solution Type |

|

| By Deployment Mode |

|

| By Vessel Type |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 965.15 million in 2025 and is projected to reach USD 2,948.93 million by 2034.

The market is expected to exhibit a CAGR of 13.24% during the forecast period.

The fleet operators/shipping companies segment led the market in terms of end-user.

The rising fuel cost pressures and need for operational efficiency are driving market growth.

Wartsila, ABB, Siemens Energy, and NAVTOR are among the prominent players in the market.

Asia Pacific dominated the market with the highest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us