Marine Interior Market Size, Share & Industry Analysis, By Ship Type (Commercial Vessels and Defense Vessels), By Commercial Vessels (Passenger Vessels, Cargo Vessels, and Others), By Passenger Vessels (Ferries, Cruises, and Yacht), By Cargo Vessels (Container Vessels, Tankers, Bulk Carriers, and Others), By Defense Vessels (Aircraft Carriers, Amphibious Ships, Destroyers, Frigates, Submarines, and Others), By Material (Aluminum, Steel, Composites, Joinery, and Others), By Installation (Line Fit, and Retrofit), By Product Type, By Application, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

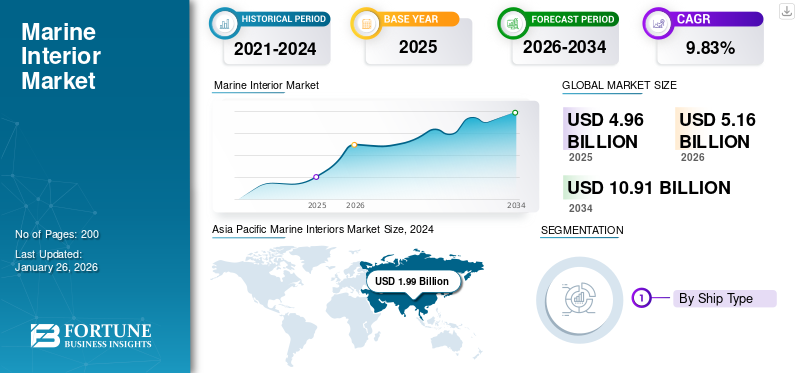

The global marine interior market size was valued at USD 4.96 billion in 2025. The market is projected to grow from USD 5.16 billion in 2026 to 10.91 billion by 2034, exhibiting a CAGR of 9.83% during the forecast period. Asia Pacific dominated the global market with a share of 45.43% in 2025.

Marine interior encompass the design, engineering, manufacturing, and installation of all interior spaces aboard vessels ranging from public areas, cabins, crew quarters, galleys and pantries, and wet units to ceilings and wall panels, lighting, furniture, floorings, and integrated services for HVAC, insulation, fire protection, hygiene, and acoustics. It covers both newbuilds and refurbishments across cruise ships, ferries, luxury yachts, naval/defense vessels, offshore units, and commercial ships.

The marine interiors industry is expanding steadily on the back of cruise tourism recovery, luxury yacht demand, vessel refurbishments, and stricter safety/sustainability standards. Firms that can deliver turnkey, compliant, modular, and sustainable fit‑outs at scale are best positioned to win.

Marine Interiors S.p.A. (Fincantieri Group), R&M Group, ALMACO Group, KAEFER, Aros Marine, Trimline, Mivan Marine, NORAC (panels/partitions), Bolidt (deck/floor systems), Forbo (flooring), and others key vendors across globally direct and indirectky involved in the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Ship Interior Refurbishment Projects to Boost Market Growth

Composite internal solutions are becoming increasingly popular as they improve vessel stability, reduce weight, and improve efficiency. The growing demand for composite solutions is increasing the replacement of existing inland marine solutions with composite solutions. In addition, the ever-increasing number of aging ships is leading to an increase in refurbishment projects globally. In October 2018, INS Vikramaditya, India’s only aircraft carrier, had undergone refurbishment. The refit had taken place at the Cochin Shipyard for five months, and the required cost is of USD 94.7. During the refit, the carrier’s hull got treated and painted.

Moreover, a large number of tanks and spaces got cleaned and painted too. Also, 16 shaft bearings were changed as part of the refit. In November 2021, the 68-meter Nobiskrug motor yacht Triple Seven will undergo a six-month refit at the Amels and Damen Yachting facilities in Vlissingen. The yacht will mainly undergo for a modifications and full respray to the stabilizers, shaft lines and interior galley, and its general interior works as per part of 15-year survey.

Market Restraints

Long Material Lead Times to Hinder Market Growth

Various materials are used to develop the ship's internal components, including aluminum, steel, composites, and carpentry. The limited availability of these and other raw materials can increase shipbuilding time. In addition, the situation has worsened since COVID-19 due to the increase in cargo ships. However, long lead times, limited availability, and high raw material costs of materials may result in delivery delays or order cancellations. This factor directly limits the global marine interior market growth.

Market Opportunities

Growing Adoption of Luxury Passenger Vessels for Personal and Entertainment Purpose across Emerging Countries Catalyze Market Growth

The marine interior industry is positioned for exceptional growth across multiple expanding segments, creating substantial opportunities for manufacturers, designers, and technology providers. The cruise tourism recovery represents the most significant opportunity, with major operators planning 44 new ships between 2023 and 2028, requiring comprehensive interior outfitting that emphasizes luxury, sustainability, and passenger experience.

The luxury yacht market continues its upward trajectory, driven by increasing high-net-worth individuals seeking bespoke, personalized interior experiences that incorporate cutting-edge technology and premium materials. Expedition cruising and specialty vessels represent emerging niches with high-value opportunities, as operators differentiate through unique interior concepts that enhance guest engagement and justify premium pricing.

- For instance, in November 2023, Daikin MR Engineering launched the 'Cabin Partner' marine air conditioning system, featuring eco-friendly R32 refrigerant and sensor-based environmental control. Trimline introduced an AI-powered 'Concept Box' in June 2023 for enhanced client engagement and design visualization, allowing text-based design inputs to generate immediate visual renderings.

Global Marine Interior Market Trends

Development of Composite Interior Solutions to Improve Vessel Efficiency and Stability is Prominent Market Trend

Over the last few years, the efficient design and development of commercial and navy ships have increased. To further modify vessel structure and reduce overall ship weight, the adoption of new material to design interior solutions is surging across the globe. The composite material is one of them. The demand for the composite material is increased to offer lightweight and highly efficient interior systems and components for cruise ships and navy vessels to enhance travel experience, efficiency, and stability. PE Composites and its partners, including Innovate UK, Carnival, and Trimline Ltd., have designed a lightweight composite cruise cabin called ‘LiteCab.’

- For instance, in May 2024, IGL Coatings launched their second wave of marine solutions, featuring eight new sustainable products including fabric guard, teak guard, leather protection, and PFAS-free formulations for comprehensive marine interior care. Esmarin Composites developed a fireproof composite material with 100-year durability that is fully recyclable and offers superior design flexibility compared to traditional metals and gypsum.

Market Challenges

Shortage of Skilled Labor and High Investment Can Hamper Market Growth

The marine interior industry faces significant operational and regulatory challenges that can substantially impact project timelines, costs, and market entry. Stringent safety regulations, particularly IMO fire safety codes (FTP Code), SOLAS compliance, and evolving environmental standards create complex compliance requirements that demand specialized engineering expertise and certified materials, increasing development costs and time-to-market.

Supply chain disruptions continue to plague the industry, with material shortages, extended lead times, and cost inflation affecting project delivery schedules and profitability margins. Skilled labor shortages in shipbuilding and interior fit-out sectors constrain capacity and increase labor costs, particularly for specialized installation and craftsmanship roles required for luxury and complex projects.

Download Free sample to learn more about this report.

Segmentation Analysis

By Ship Type

Commercial Segment Dominated Market in 2024 as Growing Seaborne Trade Drive Market Growth

By ship type, the market is classified into commercial vessels and defense vessels.

The commercial vessels dominated the market in 2026 year with holding 81.27% of global marine interior market share across the globe. In addition, the segment also estimated fastest-growing and most substantial segment, driven by comprehensive regulatory requirements and expanding global maritime trade. Commercial vessel interior requirements encompass public areas, crew accommodation, mess spaces, recreational facilities, and specialized areas including engine room access spaces, creating diverse market opportunities across vessel types from cargo ships to passenger ferries.

- For instance, in July 2024, the International Maritime Organization introduced new SOLAS Chapter XV establishing safety measures for ships carrying industrial personnel, creating new interior design requirements for offshore support vessels and energy sector vessels.

Defense vessels represent the second fastest-growing segment in global marine interior markets, characterized by highly specialized requirements, advanced materials, and stringent security protocols that drive premium pricing and technological innovation. The Indian Ministry of Defense's shipbuilding procedures under the Defense Procurement Policy require comprehensive interior design for naval vessels including weapons integration spaces, command centers, crew accommodation, and specialized compartments that must meet both operational and habitability standards. U.S. Navy habitability standards under OPNAVINST 9640.1A establish detailed interior specifications for ships over 150 feet or manned by 100+ personnel, including berthing clearances, lighting levels, materials standards, and space allocations that significantly exceed commercial requirements.

By Commercial Vessels

Increasing Adoption of Passenger Vessels for Recreational Purpose in Emerging Countries Catalyze Segmental Growth

By commercial vessels, the market is classified into passenger vessels, cargo vessels, and others.

The passenger vessels estimated to be the fastest growing during the forecast period with highest CAGR of 10.2% during the 2025-2032 forecast year. The growth is driven by International Convention for the Safety of Life at Sea (SOLAS) Chapter II-2 prescribes rigorous fire safety and subdivision requirements for passenger spaces, driving demand for advanced fire-retardant panels, automated detection systems, and compliant cabin modules. Passenger ship interiors must adhere to the International Ship and Port Facility Security (ISPS) Code, necessitating secure access control, CCTV integration, and hardened bulkhead installations that exceed commercial vessel standards. The Maritime Labour Convention (MLC) 2006 mandates enhanced accommodation for passenger vessel crews, including minimum berthing space, recreational facilities, and sanitary provisions, which indirectly raises interior fit-out requirements across the vessel.

- In October, 2025 Southampton Marine Services Ltd (SMS Group), recognized as the largest independent ship repairer in the UK, has landed a significant contract worth USD 3.94 million with the German cruise line AIDA to carry out a refit on the first of three vessels in Marseilles.

The cargo vessels sub-segment dominate the market share with holding the 46.52% in 2024 year. The growth is driven by sheer fleet size and ongoing global trade growth. SOLAS Chapter II-1 outlines structural fire protection and material standards for all merchant ships, creating baseline demand for fire-resistant linings, insulation, and segregated accommodation units on cargo vessels. In June 2025 developed next-generation acoustic insulation solutions to reduce crew fatigue on long-haul cargo voyages.

By Passenger Vessels

Stringent Safety Regulations and Evolving Passenger Expectations Catalyze Segmental Growth

By passenger vessels, the market is classified into ferries, cruises, and yacht.

The cruise sub-segment is estimated to be the fastest growing with a CAGR of 10.7% during forecast period. In addition, sub-segment accounted for the largest market share with 48.19% share in 2024. Increasing demand for cruise ships command the largest share and growth rate within the passenger vessel interior market, driven by stringent safety regulations, evolving passenger expectations, and robust order books. Cruise Lines International Association (CLIA) guidelines issued in 2024 emphasize antimicrobial surfaces, touch less fixtures, and improved passenger flow, accelerating adoption of self-sanitizing forbo flooring systems and smart cabin controls.

- For instance, in August 2025, The EU Clean Shipping Partnership’s grant program supports low-GWP HVAC systems and recycled-content laminates for newbuild, reinforcing sustainability credentials.

The yacht sub-segment is estimated to be the second fastest growing during the forecast period with 10.1% CAGR. Luxury and super yachts represent the characterized by custom craftsmanship, innovative materials, and technology integration. ISPA (International Super yacht Interior Designers Association) standards published in 2025 define lightweight composite requirements, fire-retardant upholstery, and bespoke joinery tolerances unique to yachts under 500 gt. MLC 2006 applies for commercial yachts carrying paying guests, requiring 6 m² minimum cabin area, private ensuite facilities, and dedicated crew mess spaces, driving premium interior package demand.

By Cargo Vessels

Existing Fleet of Container Vessels are Dominating the Cargo Vessels thus Create a Lucrative Opportunity for Interior Adoptions in New Build and Retrofit

By cargo vessels, the market is classified into container vessels, tankers, bulk carriers, and others.

The container vessels sub-segment is estimated to be the fastest growing with CAGR of 10.7%. In addition, the segment also accounted for the largest market share valued at 0.73 USD million in 2024. The growth is driven stringent safety, environmental, and habitability mandates. Container vessels represent the largest segment in cargo interior markets, leveraging economies of scale and standardized accommodation protocols to maintain dominance.

The International Association of Classification Societies (IACS) Common Structural Rules for bulk carriers and container ships established unified fire-resistant bulkhead specifications, driving consistent interior material requirements across global fleets. The U.S. Maritime Administration awarded grants in 2025 for pilot VR-based safety drills in container ship accommodation modules, reducing evacuation times by 28%.

- For instance, in July 2025, IMO’s Energy Efficiency Design Index (EEDI) Phase 3 came into force, indirectly increasing demand for lightweight interior materials to meet EEDI weight-reduction targets. DNV’s 2024 “Guide for Crew Habitability on Workboats” introduced noise and vibration limits, stimulating insulation upgrades in container ship accommodations.

Others sub-segment constitute the second-fastest growing, driven by enhanced safety protocols following major maritime incidents and specialized cargo-handling requirements. The International Maritime Solid Bulk Cargoes (IMSBC) Code requires specialized crew training areas and cargo monitoring stations with enhanced ventilation and emergency egress capabilities.

By Defense Vessels

Growing Need of Modernization Program of Defense Fleet by Emerging Countries Drives Segmental Growth

By defense vessels, the market is classified into aircraft carriers, amphibious ships, destroyers, frigates, submarines, and others.

The frigates sub-segment is expanding rapidly with a highest compound annual growth rate of 7.2% due to enhanced multi-mission requirements and accelerated fleet modernizations. The U.S. Navy’s NAVSTDS habitability standards (OPNAVINST 9640.1A) updated in 2024 require dedicated mission-planning centers, secure communications rooms, and mixed-use berthing arrangements supporting 150% surge capacity, driving demand for flexible modular cabins and integrated systems. NATO’s AEP-75 Allied Engineering Publication mandates advanced shock-resistant paneling and vibration-dampening solutions for crew accommodation and operations centers aboard frigates to ensure survivability in littoral zones.

- For instance, in 2025, the U.K. Ministry of Defence issued a tender for bio-based acoustic insulation panels to reduce vessel noise signature and improve crew rest quality under IMO G7 guidelines.

Submarines hold the largest share of defense interior specialist markets due to unique habitability and mission-critical system integration demands. U.S. Navy SUBSAFE program requirements impose rigorous watertight integrity and fire-resistant interior divisions, necessitating “A-60” bulkheads and certified low-smoke cables for all submersible compartments. A 2025 DTIC study on submarine habitability highlighted augmented reality-based maintenance interfaces for rapid system diagnostics within confined compartments, generating new retrofit markets.

By Material

Rapid Adoption of Composite Material Driven by Weight Reduction and Innovation Drives Market Growth

By material, the market is classified into aluminum, steel, composites, joinery, and others

The composites segment estimated to be the fastest growing during forecast period with a highest CAGR of 10.7%. The global marine interior market is embracing advanced composites at an unprecedented rate, driven by stringent weight-optimization mandates and evolving design freedoms. IACS Common Structural Rules now recognize fiber-reinforced polymer (FRP) panels for non-structural partitions, allowing up to 30% weight savings over steel equivalents while maintaining fire integrity under FSS Code MSC.98(73).

- For instance, in February 2025, DTIC report revealed modular composite cabin modules reduce installation times by 35% during dry-dock refits, offering lifecycle cost advantages. The EU Horizon 2020 Green Yachting project validated flax-fiber-reinforced composites for yacht interiors, balancing performance and circularity metrics. IMO Sub-Committee on Ship Design & Construction (SDC 11) in January 2025 recommended composite staircases to optimize evacuation flow without compromising structural fire safety.

The Steel segment led the market accounting for 38.56% market share in 2026. Steel remains the dominant sub-segment of marine interior construction, offering unmatched cost efficiency, regulatory acceptance, and repairability across vessel classes. SOLAS Chapter II-1 mandates “A-0” class steel bulkheads for all accommodation divisions on cargo and passenger ships, ensuring proven fire resistance without extensive testing protocols required for new materials. USCG Commercial Vessel Compliance under 46 CFR Part 28 prescribes welded steel structures for berthing modules to guarantee hull-integrity under collision scenarios, reinforcing operator confidence in steel’s robustness.

To know how our report can help streamline your business, Speak to Analyst

By Installation

Rapid Adoption of Composite Material Driven by Weight Reduction and Innovation Drives the Market Growth

By installation, the market is classified into line fit and retrofit.

The Line fit segment led the market accounting for 58.20% market share in 2026. Line fit installations is projected to be the fastest-growing and most prevalent segment in global marine interior markets, distinguished by combined manufacturing schedules, compliant protocols, and fabrication workflow optimization. The IMO's Fire Safety Systems (FSS) Code mandates seamless integration of detection, suppression, and alarm systems into interior panels during construction stages, making line fit installations critical for compliance with MSC.98 (73) fire safety standards. Classification societies such as Lloyd's Register and DNV require marine interior materials to be factory tested for acceptance prior to shipyard delivery to ensure line fit components of IMO certification without delays in construction.

Retrofit installations are the second most rapidly expanding marine interior sector, fueled by regulatory compliance imperatives, operational efficiency needs, and fleet renewal strategies that lengthen vessel lifespans. Green Yard retrofit operations focus on regulatory compliance with international maritime practice, whereby interior alterations comply with flag state demands and classification society approvals. The Maritime Industry retrofit boom is a consequence of compressed compliance timelines, wherein shipowners face pressure to carry out interior upgrades in narrow drydock windows to reduce off-hire expenditures.

By Product Type

Rapid Adoption of Composite Material Driven by Weight Reduction and Innovation Drives Market Growth

By product type, the market is classified into ceiling & wall panels, lighting, furniture, galleys & pantries, and others.

The Ceiling & Wall Panels segment led the market accounting for 33.13% market share in 2026. The galley and pantries segment is experiencing rapid expansion with highest CAGR of 10.1% during the forecast period of 2025-2032. As operators prioritize crew welfare, food safety, and efficiency in confined maritime environments. The International Maritime Organization’s (IMO) 2023 amendments to the Fire Safety Systems (FSS) Code require wet chemical suppression in enclosed cooking areas, prompting adoption of UL-listed kitchen hood systems and fire-rated bulkheads in galleys. The U.S. Coast Guard’s Commercial Vessel Compliance guidelines under 46 CFR Part 28 specify sanitary fixtures and potable water outlets meeting NSF ANSI Standard 61, influencing pantry fixture design and material selection.

Ceiling and wall panels dominate marine interiors due to their critical role in safety compliance, acoustic control, and ease of maintenance. A Marine Technology Society white paper from 2024 endorsed self-healing resin panels that close minor surface cracks automatically, promising lifecycle cost savings. The International Chamber of Shipping’s 2025 safety bulletin advised routine panel integrity audits as part of enhanced survey programmers, ensuring cyclic replacement and consistent aftermarket demand.

By Application

Rapid Adoption of Composite Material Driven by Weight Reduction and Innovation Drives Market Growth

By application, the market is classified into passenger area, public area, and crew area.

The public area sub-segment is estimated to be the fastest growing during the forecast period with holding the highest CAGR of 10.0%. The growth is driven by developing entertainment expectations, regulatory requirements of safety, and revenue maximization programs. Bureau Veritas classification observations point out that contemporary cruise vessels are "essentially designed as hotel accommodation installed within a ship, where public areas and recreational areas require more space," mirroring the industry growth trend.

- For instance, in October 2025, AB Yachts launched the new AB 95 yacht with 6,000 horsepower and cutting-edge interior design created in collaboration with Archea Associati, as a premiere at the 2025 Cannes Yachting Festival.

Passenger area are the second fastest growing in interior category, driven by privacy expectations, accessibility needs, and upgraded comfort standards that set premium cruise experiences apart. Passenger cabin materials must comply with classification societies' fire-resistance requirements as well as offering acoustic protection less than 60 dB to support rest quality on long voyages.

Global Marine Interior Market Regional Outlook

By geographic, the market is categorized into North America, Europe, Asia Pacific, and Rest of World

ASIA PACIFIC

Asia Pacific Marine Interiors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 45.43% of the global market in 2025, generating USD 2.25 billion in revenue, and is projected to reach USD 2.35 billion in 2026, with the support of sheer shipbuilding capability, cost-efficient manufacturing, and fast-growing maritime infrastructure in key economies. China's maritime ship market commands considerable market share, with state-owned entities CSSC and CSIC heavily investing in green propulsion, smart shipping, and autonomous ship technologies while controlling commercial ship exports such as bulk carriers, tankers, and container vessels. Japan's maritime ship industry is growing fast with its classic shipbuilding heritage and technological capabilities, with shipyards concentrating on high-value ships such as LNG carriers, advanced cargo vessels, and autonomous ships.

The Japan market is projected to reach USD 0.5 billion by 2026, the China market is projected to reach USD 1.02 billion by 2026, and the India market is projected to reach USD 0.15 billion by 2026.

South Korea's leading shipbuilders such as HD Hyundai Heavy Industries, Hanwha Ocean, and Samsung Heavy Industries keep increasing the production capacity while adopting latest interior technologies and environmental design methods.

EUROPE

In 2025, the Europe market stood at USD 1.89 billion, representing 38.07% of global demand, and is projected to grow to USD 1.98 billion in 2026. Europe is estimated to be the fastest growing with highest CAGR of 10.1%, fueled by established ship-building infrastructure, high-end vessel production, and ongoing innovation in luxury cruise building. The European region led with a 37.74% share worth USD 1.65 billion in 2024 due to the presence of prominent shipbuilders such as Meyer Werft, Fincantieri S.p.A., STX Europe AS, and interior specialists including Trimline Ltd., Kaefer GmbH, and Marine Interiors S.p.A. The demand is fueled by rising demand for luxury travel experience and eco-friendly shipbuilding technology. Europe has the world's biggest fleet of motorboats, yachts, and super yachts, with France's pleasure boating sector alone consisting of 5,435 firms employing 40,510 staff and generating nearly one-third of European sales. Cruise tourism added more than USD 52.36 billion to the regional economy in 2024, with 7.3 million Europeans going on cruise holidays, according to the European Cruise Council, fueling ongoing ship interior refinements and new shipbuilding projects.

The UK market is projected to reach USD 0.14 billion by 2026, while the Germany market is projected to reach USD 0.19 billion by 2026.

NORTH AMERICA

North America contributed approximately USD 0.58 billion to the global market in 2025, accounting for 11.66% share, and is expected to reach USD 0.59 billion in 2026. The North American market achieved the second-largest global position in 2023, backed by the region's leading cruise line operators, well-established yacht production industry, and ongoing fleet growth programs. United States Coast Guard's comprehensive commercial vessel compliance specifications under 46 CFR rules generate steady demand for interior refitting, safety system integration, and accommodation enhancement in commercial fishing, cargo, and passenger ship fleets. North American cruise operators such as Royal Caribbean, Carnival Corporation, and Norwegian Cruise Line have ambitious newbuild programs involving 44 new vessels scheduled between 2023-2028 with an extensive interior fitting worth billions of dollars combined.

The U.S. market is projected to reach USD 0.49 billion by 2026.

REST OF THE WORLD

In 2025, Rest of the World represented USD 0.24 billion, accounting for 4.84% of the worldwide market, and is projected to grow to USD 0.24 billion in 2026. The Rest of World segment, including Middle East, Africa, Latin America, and other emerging economies, registers moderate but consistent growth in marine interior market as a result of rising maritime tourism investment, growing business opportunities, and changing passenger demands for contemporary amenities.

COMPETATIVE LANDSCAPE

Key Market Players

Growing Need of Modernization and Newbuild Requirement Drives Key Players Growth

The global marine interior market is undergoing robust consolidation as long-standing players resort to vertical integration and geographic expansion to take control of bigger value chains of projects. Top industry players such as R&M Group, ALMACO Group, Marine Interiors S.p.A. (Fincantieri), Kaefer GmbH, and Trimline Ltd. are using their scale benefits through strategic acquisitions, partnerships with new technologies, and overall turnkey service provision. Fincantieri's Marine Interiors business is a prime example of this trend, having positioned itself as a full shipbuilding integration platform by adding in-house cabin design, production capacity, and public area specialists since 2016, allowing for efficient project management from concept to delivery

Recent strategic mergers involve Zenko International's April 2025 merger with HF Interior to form a consolidated marine interior solutions provider with end-to-end capabilities from design and engineering to manufacturing and installation, illustrating the trend in the industry toward integrated service models. Influential players are seeking technological differentiation with AI-driven design software, where Trimline introduced their "Concept Box" in June 2023 to facilitate client interaction through text-based design inputs and real-time visual renderings.

Competition is characterized by moderate market concentration with various large players having considerable shares while a multitude of specialized companies cater to niche luxury yacht and expedition vessel segments, offering possibilities for scale players as well as boutique specialists. Geographic growth strategies are seen in cross-border collaborations, with Fincantieri inking a strategic MoU with Qatar's Milaha in May 2025 to promote maritime cooperation and technology integration in the Middle East. Players in the industry are adopting aggressive innovation strategies aimed at smart technology integration, sustainable materials development, and modular construction methods to distinguish their offerings and gain premium pricing.

Market leaders are heavily investing in digitalization efforts, with augmented reality and virtual reality design software becoming common offerings to speed up client approvals and lower project modification expenses. Material innovation is a key competitive front, with firms designing antimicrobial surfaces, lightweight composites, and fire-rated panels that surpass IMO regulations while lowering vessel weight and increasing fuel efficiency.

List of Key Global Marine Interior Market Company Profiles

- ALMACO Group Oy (Finland)

- De Wave S.r.l. (Italy)

- R&M Group (Germany)

- Trimline Ltd. (U.K.)

- MJM Marine Ltd. (U.K.)

- Maritime Montering AS (Norway)

- Marine Interiors S.p.A. (Italy)

- Aros Marine UAB (Lithuania)

- Vard Interiors AS (Norway)

- Norac AS (Norway)

- Panelfa S.L. (Spain)

- Metawell GmbH (Germany)

- STACO Co., Ltd. (South Korea)

- Ship Interior Systems, LLC (U.S.)

- Novenco Marine & Offshore A/S (Denmark)

- Heinen & Hopman Engineering BV (Netherlands)

- Lonseal, Inc. (U.S.)

- Tarkett S.A. (France)

KEY INDUSTRY DEVELOPMENTS

- October 2025: - Maritime Montering has obtained a contract to provide comprehensive accommodation and HVAC systems for eight 6,300 DWT dry cargo ships being constructed for Wilson ASA at Udupi Cochin Shipyard Limited (UCSL). Each ship will feature approximately 450 square meters of living space for ten crew members, designed and equipped to adhere to high standards of comfort, safety, and efficiency. The project includes complete interior accommodation and HVAC installation as part of Maritime Montering’s comprehensive delivery model.

- September 2025: - Cochin Shipyard Limited (CSL) has entrusted the company with the turnkey accommodation and HVAC contract for a Service Operation Vessel (SOV) being constructed for North Star Shipping in Aberdeen, U.K. The new SOV will incorporate a walk-to-work gangway system (W2W) along with a compatible elevator to facilitate smooth, step-free access to the transition piece. Designed to function as both a logistics hub and floating living quarters, the vessel will accommodate up to 80 individuals in single cabins, which will include crew members and offshore wind professionals tasked with turbine maintenance.

- July 2025: - Maritime Montering has finished the upgrade of the habitability features on the INS Vikramaditya, supporting the “Make in India” initiative. Leveraging years of expertise in Europe and Asia, the company has collaborated in the construction of sophisticated naval ships at esteemed shipyards, where stringent standards are essential not just for performance but also for interior design solutions.

- June 2025: - The finishing of a comprehensive interior and accommodation project for the fishing ship M/S Heroyhav, constructed at Karstensens Skibsværft A/S. This signifies that this is the second Herøyhav that has been equipped. The first was delivered in 2014 and, after being sold to Chile in 2023, now operates under the name Centinela1.

- June 2025: - Maritime Montering has successfully finished the accommodation project for the crew quarters on the Amels 60 MEMORIES, the newest impressive addition from Damen Yachting. This project enhances the yacht-building legacy of the Amels LE 60 sister ships by providing exceptional comfort and well-being for the crew.

REPORT COVERAGE

The global marine interior market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the global market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.83% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Ship Type · Commercial Vessels · Defense Vessels By Commercial Vessels · Passenger Vessels · Cargo Vessels · Others By Passenger Vessels · Ferries · Cruises · Yacht By Cargo Vessels · Container Vessels · Tankers · Bulk Carriers · Others By Defense Vessels · Aircraft Carriers · Amphibious Ships · Destroyers · Frigates · Submarines · Others By Material · Aluminum · Steel · Composites · Joinery · Others By Installation · Line Fit · Retrofit By Product Type · Ceiling & Wall Panels · Lighting · Furniture · Galleys & Pantries · Others By Application · Passenger Area · Public Area · Crew Area By Region

· U.S. (By Installation) · Canada (By Installation)

· Italy (By Installation) · France (By Installation) · Nordic Countries (By Installation) · U.K. (By Installation) · Germany (By Installation) · Rest of Europe (By Installation)

· China (By Installation) · Japan (By Installation) · South Korea (By Installation) · India (By Installation) · Southeast Asia (By Installation) · Rest of Asia Pacific (By Installation)

· Middle East & Africa (By Installation) · Latin America (By Installation) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.16 billion in 2026 and is projected to reach USD 10.91 billion by 2034.

In 2025, the market value stood at USD 4.96 billion

The market is expected to exhibit a CAGR of 9.83% during the forecast period of 2026-2034.

The line fit segment is expected to hold the highest CAGR over the forecast period.

Increasing Ship Interior Refurbishment Projects to Boost Market Growth

ALMACO Group Oy (Finland), De Wave S.r.l. (Italy), R&M Group (Germany), Trimline Ltd. (U.K.), MJM Marine Ltd. (U.K.), and among others are top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us