Marine Scrubber Market Size, Share & Industry Analysis by Type (Wet Scrubber and Dry Scrubber), By Technology (Closed-Loop Scrubber, Open-Loop Scrubber, and Hybrid Scrubber), By Installation (New Build and Retrofit), By Vessels Type (Bulk Carriers, Container Ship, Oil/Chemical/Product Tankers, Passenger Vessels, Ro-Ro Vessels, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

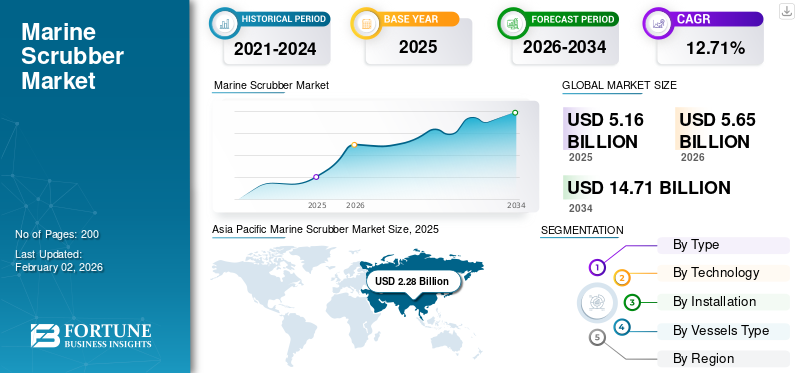

The global marine scrubber market size was valued at USD 5.16 billion in 2025. The market is projected to grow from USD 5.65 billion in 2026 to USD 14.71 billion by 2034, exhibiting a CAGR of 12.71% during the forecast period. Asia Pacific dominated the marine scrubber market with a market share of 44.16% in 2025.

A marine scrubber is a cleaning system that eliminates particulate matter and toxic substances, including sulfur oxides (SOx) and nitrogen oxides (NOx), from exhaust gas streams produced by ships. Prior to the advent of exhaust gas cleaning systems in the shipping sector, everything that was emitted from the exhaust went straight into the air, causing tremendous damage caused to the planet and mankind. However, using scrubbers, up to 98% of the SOx emissions are removed; hence, the demand for marine scrubbers is growing rapidly.

While the International Maritime Organization (IMO) imposed a worldwide cap on sulfur in ships' exhaust emissions on January 1, 2020, marine exhaust gas cleaning systems (EGCS) or scrubbers have played an increasingly important role to remain compliant. As the current emphasis is on sustainability, further rules are likely to come into effect to ensure a cleaner shipping sector and an improved environment.

Furthermore, the market encompasses several major market players. Broad portfolio with innovative products and strong regional presence expansion have supported the dominance of these companies in the market. Major players are MITSUBISHI HEAVY INDUSTRIES, LTD., Pacific Green Marine Technologies, Valmet, Wärtsilä, and others.

Download Free sample to learn more about this report.

Marine Scrubber Market Takeaways

- 2025 Market Size: USD 5.16 Billion

- 2026 Market Size: USD 5.65 Billion

- 2034 Forecast Market Size: USD 14.71 Billion

- CAGR: 12.71% from 2026–2034

- Asia Pacific dominated the marine scrubber market with a 44.16% share in 2025.

- The wet scrubber segment is expected to account for 85.76% of the market in 2026 and grow at a CAGR of 12.9%.

- The open-loop scrubber segment is expected to hold 82.96% of the market share in 2026 and grow at a CAGR of 12.3%.

North America

North America generated USD 1.02 billion in 2025 and is expected to reach USD 1.10 billion in 2026, supported by growing adoption of emission control technologies in maritime operations.

Europe

Europe accounted for USD 1.38 billion in 2025, representing 26.79% of the global market, and is projected to reach USD 1.52 billion in 2026.

Asia Pacific

Asia Pacific led the global market with USD 2.28 billion in 2025 and is projected to reach USD 2.52 billion in 2026, driven by extensive shipbuilding activities and fleet modernization.

U.S.

The U.S. market remains a key contributor to North American growth, supported by increasing compliance with marine emission regulations and vessel retrofit activities.

Japan

The Japan marine scrubber market is projected to reach USD 0.58 billion by 2026, driven by strong commercial shipping activity and investments in sustainable maritime technologies.

Read More

Market Dynamics

MARKET DRIVERS

Need for Regulatory Compliance and Cost-Saving Advantage to Push Product Demand

The sea scrubber market witnesses strong growth mainly based on strict regulatory compliance needs and strong economic incentives for ship operators. The 2020 sulfur cap imposed by the International Maritime Organization (IMO) lowered permissible sulfur levels in marine fuels from 3.5% to 0.5%, triggering the pressing need for emission control technologies immediately. This regulatory structure, compounded by current Emission Control Area (ECA) requirements specifying 0.1% sulfur content in specified areas, has made scrubbers a key compliance mechanism for the shipping fleet across the globe, creating a significant demand for new advanced marine scrubbers.

The economic benefit of scrubber technology arises from the large difference in fuel cost between high-sulfur fuel oil (HSFO) and compliant low-sulfur variants, with cost savings of around USD 200 per ton propelling adoption levels.

The Baltic and International Maritime Council (BIMCO) and the International Chamber of Shipping (ICS) have acknowledged scrubbers to offer considerable economic advantage, with the ICS commenting that capital expenditures of up to USD 3-5 million per vessel can be recovered in two to three years in terms of fuel cost savings. These advantages are anticipated to drive the global marine scrubber market growth.

- For instance, in May 2024, MIT, Georgia Tech, and other researchers published evidence which demonstrates that heavy fuel oil can match or better the use of low-sulfur fuels in terms of overall environmental considerations, offering scientific evidence to support ongoing scrubber use.

MARKET RESTRAINTS

Outcomes of Washwater Discharge with Hazardous Substance from Scrubber Systems May Hamper Market Growth

The marine scrubber business is subject to powerful environmental and regulatory restrictions that progressively reduce operational freedom and market growth opportunities. Increasing concern over scrubber washwater discharge has led many jurisdictions to introduce prohibitions or bans on scrubber use, leading to operational risk for shipowners.

The International Council on Clean Transportation (ICCT) has recorded that scrubber washwater has polycyclic aromatic hydrocarbons, heavy metals such as nickel, lead, copper, and mercury and acidic substances that lead to ocean acidification. These effects have triggered 93 recorded bans and regulations in 45 states up to February 2023, 86% of which are total prohibitions compared to modest limitations.

Maritime organizations such as BIMCO have confirmed increasing complexity in scrubber discharge legislation, keeping port restrictions and sea area prohibitions on open-loop scrubber discharges in databases to assist shipowners in understanding regulatory needs. The Danish Shipping association has noted new prohibitions, comprising Denmark’s ban on scrubber discharge from July 1, 2025, for open-loop systems, with closed-loop systems to be restricted from July 1, 2029.

- For instance, in January 2025, imports at the IMO demanded a complete prohibition on scrubbers, in reference to a Pacific Environment study indicating scrubber wastewater toxicity and higher particulate matter emissions, driving increasing regulatory pressure in the sector.

MARKET OPPORTUNITY

Rise of New Opportunities amid Geographical Expansion and Technological Innovation

The shipboard scrubber business offers significant growth opportunities in terms of technological innovation and geographical expansion, in hybrid and next-generation scrubber systems that meet regulatory heterogeneity across jurisdictions.

The development of hybrid scrubber technology has picked pace dramatically, with manufacturers designing systems comprising both open- and closed-loop to offer operational flexibility in various regulatory regimes. These state-of-the-art systems integrate artificial intelligence and automated control features that allow real-time optimization based on vessel position, regulatory demand, and operating conditions, which is the state of the art in adaptive emission control technology.

Furthermore, there is an increased environmental awareness among leisure boaters and stricter emissions regulations for pleasure craft. Government subsidies and green shipping programs offer other market opportunities, with some jurisdictions providing subsidies and economic incentives for emission-reducing technology, offering positive conditions for scrubber uptake by environmentally aware operators.

The opportunities for integration with carbon capture technology and alternative fuel systems make scrubbers complementary technologies in total emissions reduction strategy. They also exhibit the potential to increase their operating relevance beyond existing regulatory requirements.

- For instance, in June 2024, Spectra Fuels announced that scrubber technology has a beneficial effect on the efficisncy of fuel consumption by allowing ships to burn high-sulfur fuels profitably while conforming to regulation, noting the ongoing economic potential of the industry.

MARINE SCRUBBER MARKET TRENDS

Adoption of New Emerging Technologies within System to Streamline Operations

The maritime scrubber market witnesses significant trends with major inclination toward technological advancements, regulatory compliance, and operational optimization that characterize the industry's development. Digitalization and integration of artificial intelligence are the biggest technology trends, as scrubber systems depict an increase in the inclusion of IoT sensors, real-time data analysis, and computerized controls for the ongoing monitoring of emission levels, system performance, and predictive maintenance functions. These intelligent systems minimize human error and operating costs while offering data-driven information that optimizes efficiency and regulatory compliance, representing a considerable development toward more intelligent and dependable emission control technology.

The hybrid scrubber system uptake has become a prevalent trend, with producers placing emphasis on systems that merge open-loop and closed-loop characteristics to ensure operational flexibility within diverse regulatory conditions and water quality. This is a trend characterizing the response of the industry to regulatory fragmentation, which allows operators to maximize performance while upholding conformity in different jurisdictions.

Furthermore, more advanced material engineering is another major trend, with improved corrosion-resistant materials and specific coating systems intended to extend scrubber lifetime and minimize maintenance expenses in severe marine environments. These technological advancements are anticipated to influence global marine scrubber market trends over the forecast period.

- For instance, in February 2025, a study released on green investment during market uncertainty revealed that the decision to install scrubbers is influenced by freight premiums and fuel price differentials, where the scrubber-fitted ship freight premium was positively related to fuel price differentials.

MARKET CHALLENGES

Regulatory Uncertainty, Limitations, Operational Challenges Could Limit Market Growth

The scrubber marine industry faces complex challenges with regulatory complexity, technical limitations, and operational challenges that limit market development and operational efficiency. Regulatory uncertainty is the greatest challenge, with maritime associations reporting ever-increasingly complex and disparate regulations in different jurisdictions creating compliance challenges for international shipping operations.

The International Chamber of Shipping has observed that IMO standards contain baseline requirements for compliance. On the other hand, local authorities implement differing guidelines and requirements that can involve substantial penalties for non-compliance with regional regulations notwithstanding compliance with international standards.

Operational and technical issues pose ongoing concerns for scrubber-equipped ships, especially the issues of maintenance needs and system reliability in hostile marine environments. Scrubber systems produce highly acidic washwater with pH values as low as 3, posing serious corrosion issues for piping systems and equipment that need to be made from special materials and coated to protect against corrosion.

Claimed examinations have found poor protective coatings and workmanship as root causes of premature corrosion and system failures, from localized damage to catastrophic water inclusions in engine rooms, ballast tanks, and cargo holds. The sophistication of closed-loop systems demands high-level washwater treatment capabilities and specialized maintenance knowledge that might not be available in all ports and service points, causing disruptions in market demand.

- For instance, in June 2025, the UN Ocean Conference in Nice included a seminar on scrubber regulation when Swedish and Danish government representatives issued joint scrubber discharge bans, with Sweden enforcing restrictions from July 2025, evidencing growing government pressure on the sector.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Wet Scrubbers Segment Dominated in 2024 with Extensive Preference due to Technical and Economic Benefits

The market, by type, is divided into wet scrubber and dry scrubber.

The wet scrubber segment is expected to account for 85.76% of the market in 2026 and is estimated to be the fastest-growing segment with the highest CAGR of 12.9% during the forecast period of 2025-2032. Wet scrubbers record a majority of the total marine scrubber installations in the recreational marine and other sectors. The widespread preference for wet scrubber systems is a result of several operational, economic, and technical benefits compatible with maritime industry needs. Cost-effectiveness is another major reason for segmental growth.

- For instance, in August 2024, Lloyd's List quoted that shipowners keep fitting scrubbers mainly in new buildings and not via retrofits, with 36% of all crude and product tankers under order being fitted with scrubber systems, reflecting continued support for scrubber technology.

The dry scrubber segment has seen steady growth with an estimated growth rate of 10.3% over 2025 to 2032. The segment valuation stood at 0.73 USD billion in 2024. Dry scrubbers are not dependent on seawater availability and can, therefore, be used on inland waterway ships and in locations with low-quality water. Reduced operational costs in certain situations render dry scrubbers appealing, where they consume less in terms of resources compared to wet scrubbers and avoid elaborate wastewater treatment plants.

By Technology

Need for Less Capital-Intensive Solutions to Drive Open-Loop Scrubber Segment Growth

The market, by technology, is further sub-segmented into closed-loop scrubbers, open-loop scrubbers, and hybrid scrubbers.

The open-loop scrubber segment expected for the largest market share with 82.96% in 2026. The segment is estimated to depict a growth rate of 12.3% during the forecast period of 2026-2034. This extreme pattern of distribution illustrates the sea-faring sector's preference for straightforward, less capital-intensive solutions that reduce operating complexity and necessary capital investment. Open-loop systems' use of readily available seawater as the scrubbing medium to neutralize gases underscores the necessity for sophisticated chemical treatment systems and greatly lowers operating overhead.

- For instance, in August 2024, Lloyd's List cited that shipowners are still ordering scrubbers mainly through new buildings, with the highest number of all crude and product tankers ordered featuring scrubber systems, proving continued industry support for the technology.

The hybrid scrubber segment is estimated to be the fastest growing segment with the highest CAGR of 14.1% during the forecast period of 2026-2034. This accelerated growth is a result of industry acceptance of the operational flexibility and regulatory adaptability of hybrid systems, especially as discharge constraints become increasingly common in maritime jurisdictions. The high-growth pace of the hybrid segment stems from the need of ships to sail across various regulatory regimes wherein the option to alternate between open-loop and closed-loop modes offers operational flexibility that is not possible with pure open-loop systems.

By Installation

Growing Integration of Marine Scrubber System into New Build Ships for Economic and Environmental Growth to Push Segment Growth

The market, by installation, is further segmented into new build and retro fit.

The retro fit segment expected for the largest market share accounting for 57.08% market share in 2026 with a size of 2.89 USD billion. This dominance mirrors shipowner's desire to maximize the operational life of current vessels over the investment in wholly new tonnage, especially with the huge economic advantages of carrying on the use of high-sulfur fuel oil (HSFO) while meeting regulatory requirements. Retrofit installations allow fleet operators to preserve operating flexibility without adopting more costly low-sulfur variants, offering a cost-efficient route to compliance that does not involve the huge capital expense of new build vessels.

- For instance, in March 2023, BIMCO stated that 399 ships installed scrubbers in 2022, which is 24% down from the previous year's total installations. Although retrofits fell, scrubber installation in new builds continued to rise, added the company.

The new build segment is estimated to be the fastest growing segment with the highest CAGR of 14.2% during the forecast period of 2025-2032. The growth momentum of the new build sector is fueled by a number of factors such as enhanced economic feasibility, lower payback times, and reduced installation expenses. The cost benefit coupled with the fact that scrubber systems can be integrated in the initial design stage instead of intricate retrofitting makes newbuild installations ever more desirable for shipowners, anticipating long term fleet growth.

By Vessels Type

To know how our report can help streamline your business, Speak to Analyst

Bulk Carrier Segment Led the Market in 2024 Owing to High Fuel Usage

The market, by vessels type, is further sub-segmented into bulk carrier, container ship, oil/chemical/product tanker, passenger cruise, RO-RO vessels, and others.

The bulk carrier segment expected for the largest market share of 32.43% in 2026 with a size of 1.57 USD billion. This superiority can be credited to the operating nature of bulk carriers, which hugely gain from the installation of scrubbers owing to high fuel usage and long-distance routes.

The container ship segment is estimated to be the fastest growing segment with the highest CAGR of 12.7% during the forecast period of 2025-2032. Container ships offer strong growth prospects fueled by changing market forces and operational needs that support scrubber implementation. The development of global trade continues to spur the demand for container shipping capacity, with ships needing to comply in a way that supports operational effectiveness while adhering to emissions levels. Moreover, the fuel cost benefit is especially relevant to container lines running competitive routes where operating margins are essential in making profitability.

- For instance, in September 2024, Wartsila was engaged to provide its newest scrubber systems that are ready for carbon capture and storage termed CCS-Ready scrubbers for three container vessels owned by the German company Leonhardt & Blumberg. Implementing a CCS-Ready solution would ensure that Leonhardt & Blumberg remains compliant with current SOx emissions regulations and facilitates a seamless transition to a CCS system later on.

Marine Scrubber Market Regional Outlook

By geography, the market is classified into North America, Europe, Asia Pacific, and rest of the world.

Asia Pacific

Asia Pacific Marine Scrubber Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 2.28 billion in 2025, capturing 44.16% of global revenue, and is estimated to reach USD 2.52 billion in 2026. The dominance is based on scrubber installations, given that the region is the world's busiest maritime trade corridor and hub to the largest shipbuilding centers. The Chinese, South Korean, and Japanese shipowners hold the largest proportion of the world's scrubber-fitted fleet, both retrofitting and new build integration as well as large retrofitting campaigns. Key Asian shipyards such as Samsung Heavy Industries and Mitsubishi Heavy Industries already provide scrubber‐ready vessel designs, which allow easy integration at construction and decrease installation lead times. The Japan market is projected to reach USD 0.58 billion by 2026, the China market is projected to reach USD 0.76 billion by 2026, and the India market is projected to reach USD 0.26 billion by 2026.

Regional governments such as China's Ministry of Transport have also issued policy incentives such as accelerated depreciation plans and port fee rebates to promote rapid scrubber adoption and maintain compliance with IMO 2020 sulfur limits. China’s domestic shipyards handle 75% of worldwide scrubber retrofit work and 150 out of the 200 global scrubber installation projects are centered in domestic yards. This leadership position of China in the Asia Pacific market is a result of its complete maritime industrial chain, rigorous environmental compliance system, and technological innovation strength in congruence with global emission reduction regulations.

In addition, Chinese producers exhibit a high level of technological progress in designing and producing scrubber systems. Qingdao Sunrui Marine Environment Engineering designs independent SOxFREE exhaust gas cleaning systems with original U-type and I-type tower structures.

Furthermore, while countries such as Japan accounted for the second largest country in the market with a share of 22.67%, South Korea accounted for 18.94%. The market in India is estimated to grow at a CAGR of 12.9% during the forecast period. The U.S. market is projected to reach USD 0.86 billion by 2026.

- For instance, in December 2023, Performance Shipping Inc., a shipping company specializing in the ownership of tanker vessels, signed two shipbuilding contracts with Shanghai Waigaoqiao Shipbuilding Co. Ltd. and China Shipbuilding Trading Co. Ltd. for building two 114,000 DWT LNG-ready LR2 Aframax product/crude oil tanker vessels. The vessels would be upgraded with ballast water treatment systems (BWTS), exhaust gas cleaning systems (EGCS – commonly referred to as scrubbers) for Tier II (NOx Emissions) compliance, and electronic main engines with high-pressure selective catalytic reactors (HPSCR) for Tier III (NOx Emissions) compliance.

Europe

Europe accounted for USD 1.38 billion in 2025, representing 26.79% of the global market share, and is projected to reach USD 1.52 billion in 2026. The expansion is driven by a surge in European operators' closed‐loop and hybrid system retrofits. According to European Community Shipowners' Associations (ECSA), almost 70% of European‐flagged ships scheduled for scrubber retrofits in 2024 chose closed‐loop or hybrid design to preserve operational flexibility in Baltic and North Sea waters. The UK market is projected to reach USD 0.11 billion by 2026, while the Germany market is projected to reach USD 0.15 billion by 2026.

North America

North America contributed 19.76% to the global market in 2025, with a valuation of USD 1.02 billion, and is projected to reach USD 1.1 billion in 2026.

Rest of the World

The Rest of the World region captured 9.29% of the global market in 2025, generating USD 0.48 billion in revenue, and is projected to reach USD 0.5 billion in 2026.

Competitive Landscape

Key Market Players

Growing Environmental Regulations Lead Major Key Players to Introduce Innovative Products

The market for marine scrubbers is highly competitive with high growth fueled by OEMs, who are emphatically pushing new build integration to benefit from long term service income. Key players are competing to future-proof EGCS by integrating SOx abatement with carbon-capture and tighter wash-water controls. Additionally, OEMs are coordinating R&D activities with advancing government association guidelines to future-proof technologies.

- In 2021, Yara Marine's completed the acquisition of Lean Marine, adding its FuelOpt and Fleet Analytics to the scrubber portfolio. Further, in 2024, the then-Yara Marine changed name to Manta Marine Technologies under new ownership (Okapi), retaining decarbonization hardware plus digital optimization under one roof, an integrated strategy replicated by others through partnerships instead of outright acquisitions.

- In January 2025, the OSPAR Commission endorsed a decision to phase out scrubber discharges in internal waters and ports in the North-East Atlantic, hastening the transition to hybrid/zero-discharge configurations and establishing a premium for OEMs with strong closed-loop chemistries and after-treatment.

LIST OF KEY MARINE SCRUBBER COMPANIES PROFILED

- ALFA LAVAL (Sweden)

- ANDRITZ (Austria)

- Fuji Electric Co., Ltd. (Japan)

- MITSUBISHI HEAVY INDUSTRIES, LTD. (South Korea)

- Pacific Green Marine Technologies (U.K.)

- Valmet (Finland)

- Wartsila (Finland)

- Drizgas Tech (India)

- CR Ocean Engineering (U.S.)

- Clean Marine Pte. Ltd. (Norway)

KEY INDUSTRY DEVELOPMENTS

- January 2025 - COSCO, the Chinese container shipping company, enhanced its utilization of scrubber systems, also known as exhaust gas cleaning systems, in 2024. In that year, COSCO incorporated scrubber-equipped vessels with a total capacity of 417,827 TEU, along with 16 new scrubber-equipped container ships added to its fleet.

- July 2024 - Wartsila entered a six-year lifecycle agreement with Nautica Ship Management, based in Malaysia. This agreement pertains to two ships, the MTT Saisunee and MTT Senari, and aims to guarantee that the exhaust gas treatment systems of the vessels function at peak efficiency. The ships are feeder container vessels equipped with Wartsila hybrid scrubber systems.

- February 2023 - Dry bulk shipping company Golden Ocean Group announced that it reached an agreement to purchase six Newcastlemax vessels, each with a capacity of 208,000 deadweight tons (dwt), for a total price of USD 291 million. The acquired vessels, all featuring exhaust gas cleaning systems or scrubbers, will be leased back to their previous owner, an unrelated third party, for about 36 months at an average daily time charter equivalent rate of roughly USD 21,000 net.

- November 2022 - Greek shipowner Safe Bulkers equipped 20 of its bulk carriers with Alfa Laval PureSOx exhaust gas cleaning systems. The company also completed the installation of its 21st PureSOx scrubber and shared plans to carry out four additional retrofits in the first half of 2023.

- February 2022 - Wartsila, the technology company, finalized a new deal for its exhaust gas cleaning systems to be fitted on two new 218m roll-on/roll-off passenger vessels (RoPax) being constructed at Guangzhou Shipyard International (GSI) in China.

REPORT COVERAGE

The research market report provides a detailed analysis of the market insights and focuses on important aspects, such as key players, by type, by technology, by installation, and by vessels type depending on various regions and countries. Moreover, it offers insights into the market trends, competitive landscape, market competition, comparative analysis, and highlights key industry developments. Additionally, it encompasses several factors that have contributed to the expansion of the global market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Year |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.71% from 2026 - 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Wet Scrubber · Dry Scrubber By Technology · Closed-Loop Scrubber · Open-Loop Scrubber · Hybrid Scrubber By Installation · New Build · Retrofit By Vessels Type · Bulk Carrier · Container Ship · Oil/Chemical/ Product Tanker · Passenger Cruise · Ro-Ro Vessels · Others By Geographic North America (By Type, By Technology, By Installation, By Vessels Type and By Country) · U.S. (By Installation) · Canada (By Installation) Europe (By Type, By Technology, By Installation, By Vessels Type and By Country) · U.K. (By Installation) · Germany (By Installation) · Italy (By Installation) · France (By Installation) · Nordic Countries (By Installation) · Rest of Europe (By Installation) Asia Pacific (By Type, By Technology, By Installation, By Vessels Type and By Country) · China (By Installation) · Japan (By Installation) · South Korea (By Installation) · India (By Installation) · Southeast Asia (By Installation) · Rest of Asia Pacific (By Installation) Rest of the World (By Type, By Technology, By Installation, By Vessels Type and By Sub-Region) · Middle East & Africa (By Installation) · Latin America (By Installation) |

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size was valued at USD 5.16 billion in 2025 and is anticipated to reach USD 14.71 billion by 2034.

The market is likely to grow at a CAGR of 12.71% during the forecast period (2026-2034).

The top players in the industry are MITSUBISHI HEAVY INDUSTRIES, LTD. Pacific Green Marine Technologies, and Wartsila, among others.

Asia Pacific dominates the market.

The Asia Pacific region is estimated to be the fastest growing during the forecast period.

China is the dominant country in the Asia Pacific region.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us