Fire Control System Market Size, Share & Industry Analysis, By Platform (Land, Air, Naval, and Stationery/fixed), By System Type (Integrated Fire Control Systems, Target acquisition & Tracking Systems, Ballistic Computers & Weapon Control Units, & Others), By Weapon Type (Artillery guns & Howitzers, Tank guns, CIWS, Air Defense Guns & Missile Launchers, & Others), By Component (Sensors, Computing & Control, Display and Interface, & Others), By Range (Short-range & Medium-Range Fire Control Systems, and Beyond-Visual-Range), By End-User, and Regional Forecast, 2026-2034

Fire Control System Market Size and Future Outlook

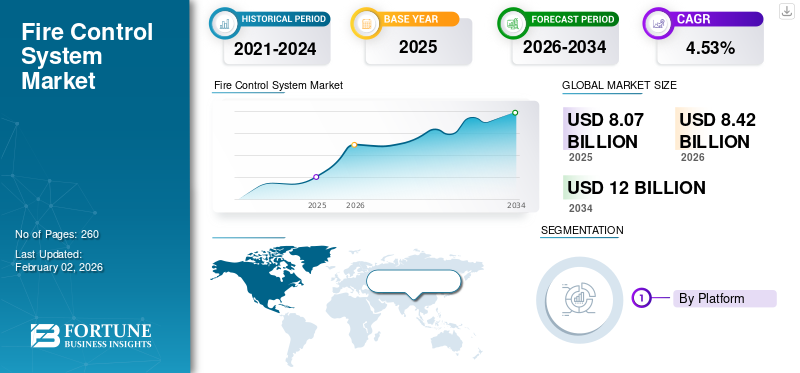

The global fire control system market size was valued at USD 8.07 Billion in 2025. The market is projected to grow from USD 8.42 Billion in 2026 to USD 12.0 Billion by 2034, exhibiting a compound annual growth rate CAGR of 4.53% during the forecast period. North America dominated the global fire control system market with a market share of 39.40% in 2025.

The fire control system (FCS) market encompasses sensors, computers, software, and actuators that convert raw targeting data into precise, time-critical weapon engagement across land, naval, and airborne platforms. Modern FCS suites integrate inputs from fire-control radars, electro-optical/infrared sights, and laser rangefinders with ballistic and kinematic calculations to deliver a high first-round hit probability for tank guns, artillery, CIWS, naval guns, and air-defense launchers, often while the platform and target are both in motion. Three converging trends are pulling demand.

The competitive landscape is concentrated but globally distributed; key players include BAE Systems, Rheinmetall, Leonardo, Thales, Saab, Elbit Systems, Lockheed Martin, RTX, Northrop Grumman, General Dynamics, Hanwha Aerospace, and Aselsan, which embed FCS as part of broader land systems, naval weapons, or integrated air- and missile-defense portfolios.

Download Free sample to learn more about this report.

Fire Control System Market Key Takeaways

- 2025 Market Size: USD 8.07 billion

- 2026 Market Size: USD 8.42 billion

- 2034 Forecast Market Size: USD 12.0 billion

- CAGR: 4.53% from 2026–2034

- North America dominated the fire control system market with a 39.40% share in 2025.

- The land platform segment accounted for the largest market share due to rising military modernization programs.

- The integrated fire control systems segment dominated the market driven by increasing adoption of sensor fusion and network integration.

North America

North America held a 39.40% share in 2025, valued at USD 3.18 billion.

Asia Pacific

Asia Pacific is expected to grow significantly due to expanding armored fleets and naval procurement activities.

Europe

Europe is projected to witness the fastest growth driven by rising NATO defense spending and tank modernization programs.

U.S.

The U.S. market is projected to witness strong growth supported by Abrams M1E3, IBCS, and LTAMDS modernization programs.

Japan

The Japan market is projected to witness growth driven by increasing investments in naval defense systems and regional security upgrades.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Modernization of Armored, Naval, and Air-Defense Fleets Leading to Market Growth

The strongest fire control system market growth driver is the global acceleration of defense modernization programs. Militaries are replacing analogue and first-generation digital fire-control units with multisensory, software-defined systems capable of fusing radar, EO/IR, laser ranging, and external battlefield data. This shift is no longer optional, platform survivability now hinges on rapid target engagement, stabilization accuracy, and interoperability with wider command-and-control networks. Countries in Europe and Asia are prioritizing upgrades for tanks, artillery, frigates, destroyers, and integrated air-defense batteries, largely driven by renewed geopolitical tensions and the need to counter drones, cruise missiles, and high-maneuvering threats. The broader transition toward networked, modular combat systems directly increases the FCS content per platform, expanding both new-build and retrofit demand.

- In November 2024, the U.K. Ministry of Defense announced a USD 330 million modernization contract for Challenger 3 MBTs, with upgraded digital fire-control and multisensory sights forming a core deliverable.

MARKET RESTRAINTS:

High Integration Complexity and Long Procurement Cycles To Act As A Market Restraint

A major restraint for the market is the inherent complexity of integrating sensors, computing modules, actuators, and stabilized weapon systems across platforms with very different architectures and legacy electronics. Additionally, defense procurement cycles remain slow, heavily regulated, and prone to delays caused by budget reviews, shifting political priorities, and supply chain constraints. These structural frictions limit year-on-year market acceleration even when defense budgets rise.

- In June 2024, Germany’s Federal Audit Office reported delays in the Leopard 2A8 upgrade program, citing extended integration testing for the new digital fire-control and sensor suite as a key bottleneck.

MARKET OPPORTUNITIES:

Expansion of Autonomous and AI-Enabled Targeting Systems Posing As a Major Market Opportunity

The clearest opportunity lies in the transition toward AI-assisted and autonomous fire-control capabilities. Militaries increasingly require systems that can classify threats, track multiple incoming objects, predict trajectories, and support decision-making with minimal crew workload. This creates meaningful whitespace for OEMs offering modular FCS architectures with onboard processing, predictive algorithms, adaptive stabilization, and machine vision enhancements. The rise of drone swarms, loitering munitions, and long-range precision weapons further amplifies the need for such next-generation engagement solutions. Countries investing in integrated air-defense grids and new-age armored formations are actively seeking AI-driven fire-control upgrades, creating a rich pipeline across NATO, Indo-Pacific, and Middle Eastern programs.

- In Sept 2024, South Korea’s Defense Acquisition Program Administration revealed a new AI-enabled targeting module for its Redback IFV program, enhancing automatic target recognition and integrating machine-vision capabilities into the fire-control suite.

FIRE CONTROL SYSTEM MARKET TRENDS:

Shift Toward Open-Architecture, Multi-Sensor Fusion FCS Posing As Major Market Trends

Download Free sample to learn more about this report.

A defining technological trend is the movement toward open-architecture fire-control systems that can integrate multiple sensors, effectors, and software modules from different suppliers. Defense ministries increasingly demand plug-and-play frameworks to avoid being locked into single-vendor ecosystems. This trend is driven by the need to incorporate domestic sensors, sovereign encryption, drone detection modules, and new weapon types without requiring a redesign of the entire fire-control unit. Multi-sensor fusion is becoming standard practice, with systems blending radar, EO/IR, LIDAR, and third-party cueing to improve situational awareness and engagement accuracy. Software-centric architectures allow updates through patches rather than hardware replacement, fundamentally reshaping lifecycle value.

- In April 2024, the U.S. Navy confirmed the deployment of an open-architecture combat system upgrade across select destroyers, enabling the integration of new EO/IR fire-control modules and third-party missile-tracking sensors.

MARKET CHALLENGES:

Supply-Chain Constraints and Skilled Workforce Shortage Pose a Threat to Market Growth

The market faces persistent challenges related to component supply and the availability of skilled manpower. High-precision sensors, advanced processors, thermal imaging modules, and stabilization actuators rely on specialized manufacturing chains that remain vulnerable to semiconductor bottlenecks and geopolitical export controls. Restrictions on imaging sensors and laser components have slowed deliveries across Europe and Asia. At the same time, the defense electronics sector is experiencing a shortage of experienced systems engineers, embedded-software specialists, and integration teams capable of handling modern FCS architectures. These constraints increase delivery timelines and reduce production scalability even for well-funded programs.

Segmentation Analysis

By Platforms

Land segment is growing due to High Military Demand

Based on platforms, the market is classified into land, air, naval, and stationery/fixed.

Land platforms account for the largest fire control system market share, driven by the sheer volume of main battle tanks, IFVs, and self-propelled artillery in service globally. Armies are prioritizing digital FCS upgrades, such as thermal sights, laser rangefinders, ballistic computers, and stabilized turrets, to keep legacy fleets relevant against drones, ATGMs, and precision artillery. Upgrades are cheaper and faster than buying new hulls, so land-based programs create steady retrofit revenue, plus new-build demand increases in Europe and Asia.

- In September 2023, the U.S. Army canceled the Abrams SEPv4 upgrade and launched the M1E3 program, keeping advanced fire control at the core of its future tank.

By System Type

Integrated Fire Control Systems Drive High-Value Spend Leading To Segmental Growth

In terms of system type, the market is categorized into integrated fire control systems, target acquisition & tracking systems, ballistic computers & weapon control units, gun directors & turret drives, electro-optical fire control systems, and radar-based fire control systems.

Integrated fire control systems, complete suites combining sensors, computers, software, and actuators, form the largest system-type segment. Customers increasingly want a single, platform-level solution that fuses radar, EO/IR, laser, and external cues, rather than buying stand-alone components. This supports higher ASPs and recurring software revenue as new modes, counter-UAS functions, and networking features are fielded. The trend is reinforced by integrated air and missile defense concepts that tie multiple launchers and sensors into a single fire-control network.

- In July 2024, the U.S. Army’s Integrated Air and Missile Defense program advanced testing of IBCS, which links Sentinel and Patriot sensors into a common fire-control architecture.

By Component

Sensors Segment Growing Due To High Value And Frequent Upgradation

Based on the component, the market is segmented into sensors, computing and control, display and interface, actuation and stabilization, and auxiliary.

Sensors, fire-control radars, EO/IR cameras, and laser rangefinders represent the largest component share as they are high-value, upgraded frequently, and central to performance. Modern FCS roadmaps prioritize the enhanced detection and tracking of low-observable drones, cruise missiles, and fast-moving ground targets, which necessitates the adoption of new AESA radars, higher-resolution thermal imagers, and multispectral optics. Even when platforms keep their computers and actuators, they often receive new sensors during mid-life upgrades, creating repeat business for OEMs.

- In Dec 2023, the U.S. DoD awarded Raytheon a USD 48.1 million contract to enhance AN/MPQ-64 Sentinel A3 radars, improving air-surveillance and fire-control capabilities for ground-based air defense.

By Weapon Type

Tanks Segment Growing Due To High Demand From Heavy Armor

Based on the weapon type, the market is segmented into artillery guns & howitzers, tank guns, close-in weapon systems (CIWS), air defense guns & missile launchers, naval guns, and rockets and guided missile launchers.

Among weapon types, tank guns generate the largest FCS spend thanks to the global installed base of MBTs and IFVs and the high value of their turret and sighting systems. Modern doctrines still rely on heavy armor for deterrence and breakthrough operations, so armies are investing in digital gun control, hunter-killer sights, and stabilized day/night optics. Each vehicle carries multiple FCS elements, making per-platform content substantial compared with many artillery or rocket systems.

- In October 2024, Taiwan and several Asia-Pacific armies continued upgrading their legacy M60 and other tanks with enhanced fire-control systems and thermal sights, while also inducting new M1A2-series vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Range

Medium Range Segment Is Growing Due To High Demand For Military Applications

Based on the Range, the market is segmented into Short-range fire control systems, medium-range fire control systems, and beyond-visual-range (BVR) fire control systems.

Medium-range fire control systems supporting engagements out to tens of kilometers for artillery, air defense, and naval guns form the core range segment. They sit at the heart of layered defense architectures and long-range fires modernization, where militaries seek systems that can track, classify, and engage cruise missiles, drones, and aircraft at standoff distances. These FCS solutions often integrate multi-function radars and sophisticated tracking software, driving higher system value.

- In Aug 2024, the U.S. Army awarded Raytheon roughly USD 2 billion to begin production of the LTAMDS radar, a medium-range sensor for integrated air and missile defense batteries.

By End-User

Military Segment Growing Due To High Demand For Counter-UAS Applications

Based on the end-user, the market is segmented into civil and commercial, and military.

Military users account for almost all fire control system spending, with only a marginal slice coming from civil test ranges or specialized security applications. Land forces, navies, and air forces are all upgrading FCS to support multi-domain operations, counter-UAS missions, and precision fires. These programs are funded from core defense modernization budgets rather than discretionary technology projects. As geopolitical tensions rise, militaries are accelerating the procurement of tanks, artillery, ships, and air-defense systems, keeping the civilian share structurally small.

- In September 2024, Raytheon secured approximately USD 205 million U.S. Navy contract to continue production and upgrade the Phalanx CIWS, underscoring sustained military-driven demand.

Fire Control System Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Fire Control System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 3.07 billion, and also took the leading share in 2025 with USD 3.18 billion. North America is the largest regional market in value terms, driven by the U.S.'s modernization of armored brigades, integrated air and missile defense, and naval combatants. Programmes such as the Abrams M1E3, long-range precision fires, and Aegis/CIWS upgrades all incorporate advanced fire control, sensor fusion, and network integration. The U.S. also exports FCS-rich platforms and radars, spreading its technology base into allied fleets. Canada’s smaller but steady vehicle and naval projects add incremental demand.

- In 2024, the U.S. Army reoriented Abrams upgrades toward the M1E3 and advanced IBCS and LTAMDS, while the Navy funded additional Phalanx CIWS lots for surface combatants.

Europe

Europe has become the fastest-growing FCS region as NATO states react to the war in Ukraine and commit to higher defense spending. Demand is skewed toward upgrades, including new FCS for Leopard and Challenger tanks, artillery digitization, and modernized naval and ground-based air-defense fire-control systems. Eastern members are accelerating the purchase of radars and missile systems, creating additional demand for sensors and battle-management-linked FCS. Western Europe is also investing in cruise missiles and precision-strike capabilities, which rely on sophisticated guidance and targeting systems.

Asia Pacific

Asia Pacific is the most dynamic FCS market and is expected to grow at a significant CAGR, driven by large armored fleets, expanding air-defense networks, and active naval procurement. Countries such as China, India, South Korea, Japan, and Australia are purchasing or upgrading tanks, infantry vehicles, frigates, and destroyers, all equipped with modern multi-sensor fire control systems. Regional tensions in the Taiwan Strait, the Korean Peninsula, and the South China Sea support sustained spending on both land-based fire support and shipboard CIWS and gun systems.

Rest of the World

The rest of the world, comprising the Middle East & Africa and Latin America, has a smaller but strategically important FCS market, focused on air defense and select armored and naval projects. Gulf states prioritize integrated air- and missile-defense networks with sophisticated fire-control radars and command systems, while some Latin American countries pursue a gradual modernization of their aircraft and surface platforms. Budget volatility and procurement bureaucracy temper growth, but individual contracts are large when they materialize.

COMPETITIVE LANDSCAPE

Key Industry Players:

Wide Range of Product Offerings and Strong Distribution Network of Key Companies, supported their Leading Position

The market is semi-concentrated around a set of large defense primes, with intense competition at the program level rather than in terms of pure volume. Global leaders include BAE Systems, RTX (Raytheon), Lockheed Martin, Thales, Leonardo, Rheinmetall, Saab, Elbit Systems, Aselsan, Hanwha, and Northrop Grumman, all of which embed FCS within their wider land systems, naval combat systems, and integrated air- and missile-defense portfolios. Western primes typically dominate high-end naval and air-defense fire control. At the same time, European and Asian players have gained a share in armored vehicles and artillery FCS through aggressive export strategies and industrial partnerships. The landscape is shifting toward open architectures and modular sensors, which lower switching costs and allow local integrators to challenge incumbents on subsystems and software.

LIST OF KEY FIRE CONTROL SYSTEM COMPANIES PROFILED:

- Raytheon (RTX) (U.S.)

- Lockheed Martin (U.S.)

- BAE Systems (U.K.)

- Thales Group (France)

- Leonardo (Italy)

- Rheinmetall (Germany)

- Saab (Sweden)

- Elbit Systems (Israel)

- Northrop Grumman (U.S.)

- Hanwha Aerospace (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Fliant launched “FlightVue FDM”, a new full-lifecycle flight data monitoring and FOQA (Flight Operations Quality Assurance) platform designed for airlines and operators seeking modern safety and performance analytics capabilities. This product rollout signals a shift toward increasing software-led growth in the FDM market.

- October 2025: India’s DGCA (Directorate General of Civil Aviation) selected Tata Consultancy Services (TCS) to develop a centralized, real-time flight data capture software system that will link airlines and OEMs directly, enhancing national surveillance and oversight of aircraft operations.

- June 2025: Acron Aviation partnered with Air Cairo under a multi-year contract to provide a fully outsourced FDM service using Acron’s Flight Data Connect (FDC) platform covering the airline’s ATR, Embraer, and Airbus fleet. This arrangement accelerates fleet-level rollout of analytics and safety-event pipelines.

- June 2025: Textron Aviation announced a new FDM service option for its Cessna Citation and SkyCourier aircraft in partnership with GE Aerospace’s C-FOQA platform via Textron’s LinxUs data-reporting ecosystem. The move broadens the FDM-enabled business-jet and commuter-aircraft market segment.

- June 2025: A sharp rise in GPS jamming/spoofing incidents over conflict zones, 430,000 cases in 2024, up from 260,000 in 2023, underscores the need for enhanced flight-data-monitoring and situational-awareness systems on aircraft. This security environment drives demand for FDM solutions that focus on safety and resilience.

- April 2025: The FAA (U.S. Federal Aviation Administration) announced plans to deploy a modernized pilot-messaging/NOTAM database system by September 2025 to enhance data flow and operational transparency. Although not strictly an FDM contract, it highlights the broader aviation data infrastructure momentum that supports FDM adoption.

- June 2024: Broader aviation-safety regulatory developments highlighted the importance of FDM. Industry commentary noted that business aviation operators are now adopting FDM programs with strategic intent, rather than merely complying.

REPORT COVERAGE

The global fire control system market analysis provides an in-depth study of the market size & forecast by all the market segmentations included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The self-defense weapons market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.53% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Platform

By System Type

By Weapon Type

By Component

By Range

By End-User

By Region North America (By Platform, System Type, Weapon Type, Component, Range, End-User, and Country)

Europe (By Platform, System Type, Weapon Type, Component, Range, End-User, and Country)

Asia Pacific (By Platform, System Type, Weapon Type, Component, Range, End-User, and Country)

Rest of the World (By Platform, System Type, Weapon Type, Component, Range, End-User, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.07 billion in 2025 and is projected to reach USD 12.0 billion by 2034.

In 2025, the market value stood at USD 3.18 billion.

The market is expected to exhibit a CAGR of 4.53% during the forecast period.

The sensors segment led the market in terms of components.

The modernization of armored, naval, and air-defense fleets are key factors leading to market growth.

Raytheon (RTX) (U.S.), Lockheed Martin (U.S.), and BAE Systems (U.K.) are prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 260

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us