Cruise Missiles Market Size, Share & Industry & Analysis, By Missile Type (Land-Attack Cruise Missiles (LACM), Anti-Ship Cruise Missiles (ASCM), and Air-Launched Cruise Missiles (ALCM)), By Component (Guidance & Propulsion Systems, Warheads, Missile Airframe, Sensors & Seekers, & Communication Systems), By Missile Speed (Subsonic, Supersonic & Hypersonic), By Launch Platform (Airborne, Ground-Launched, & Naval), By Missile Range (Short, Medium, & Long Range), By Guidance Technologies (Autonomous, Real-Time Tracking, & Swarm Intelligence), By Operational Mode, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

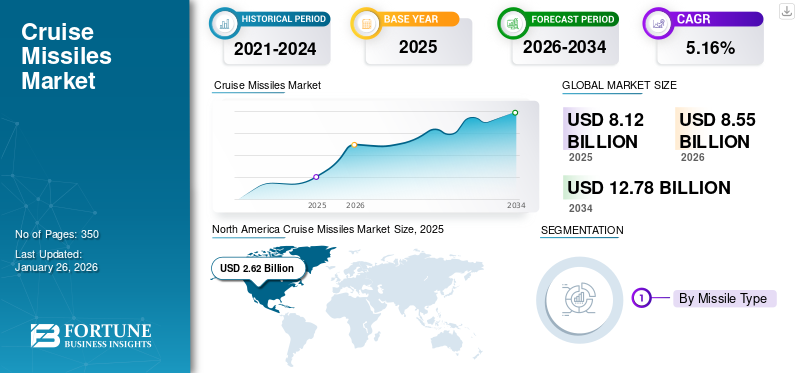

The global cruise missiles market size was valued at USD 8.12 billion in 2025 and is projected to grow from USD 8.55 billion in 2026 to USD 12.78 billion by 2034, exhibiting a CAGR of 5.16% during the forecast period. North America dominated the cruise missiles market with a market share of 32.20% in 2025.

Cruise missiles are guided missiles flying at a moderately low elevation within Earth's atmosphere, fueled by jet engines, and designed for precision strikes. They take a modified way toward their target and can be propelled from various platforms including aircraft, ships, and ground-based launchers. The need for long-range accuracy strike capabilities, which are fundamental for modern warfare, has led to an increase in funding for missiles. Additionally, the rising geopolitical pressures due to countries prioritization toward improving defense capabilities drives market growth. Cruise missiles fly at low altitudes regularly following terrain to avoid detection by radar. They are profoundly maneuverable and can alter their direction mid-flight to hit the target accurately.

With the growth in improved guidance systems such as GPS, inertial navigation, and advanced radar seekers, and demand for greater accuracy in targeted strikes, the market is expected to grow at a high rate in the forthcoming years. Raytheon Technologies Corporation, Lockheed Martin Corporation, and Northrop Grumman Corporation are some of the key players in the market.

Download Free sample to learn more about this report.

Cruise Missiles Market Takeaways

- 2025 Market Size: USD 8.12 billion

- 2026 Market Size: USD 8.55 billion

- 2034 Forecast Market Size: USD 12.78 billion

- CAGR: 5.16% from 2026–2034

- North America dominated the cruise missiles market with a 32.20% share in 2025.

- Air-Launched Cruise Missiles (ALCM) held the dominant market position and are expected to grow at the fastest CAGR.

- Hypersonic missiles dominated the market and are projected to register the highest growth rate during the forecast period.

North America

North America led the global market with USD 2.62 billion in 2025 and is projected to reach USD 2.74 billion in 2026.

Europe

Europe accounted for USD 2.47 billion in 2025 and is expected to grow to USD 2.62 billion in 2026.

Asia Pacific

Asia Pacific generated USD 1.55 billion in 2025 and is projected to reach USD 1.63 billion in 2026.

U.S.

Strong defense modernization programs and investments in advanced missile technologies continue to drive market growth.

Japan

Rising regional security concerns and increasing defense capabilities are supporting demand for advanced cruise missile systems.

Read More

Market Dynamics

Market Drivers

Military Modernization and Increased Defense Spending to Fuel Demand for Cruise Missiles

Increased global military investments and rising geopolitical pressures are altogether boosting the demand for missiles. This surge in demand is fueled by countries seeking to modernize their militaries and enhance defense capabilities, leading to increased investment in advanced missile technology.

Military consumption has been on the rise globally, with the U.S., China, and India heavily expanding their defense budgets. This increment is driven by a need to modernize armed forces and upgrade capabilities, including missile systems.

Countries are contributing heavily to the R&D of missile technology to improve system effectiveness and remain competitive in modern warfare. This includes developing faster, more precise, and versatile missile systems. Increasing geopolitical tensions in various regions, such as the Middle East, South China Sea, and Eastern Europe, are advancing, driving the demand for precision strike capabilities and making missiles a key component of modern defense methodologies. The Indian government, for instance, has designated a significant budget for the Ministry of Defense in FY 2025-26. Additionally, the U.S. government allocated USD 2.53 billion to the Ground-based Midcourse Defense (GMD) Program, showcasing the growing focus on missile defense systems.

Advancements in Multi-Domain Warfare Systems and Growing Emphasis on Indigenous Development to Propel Market Growth

The cruise missile market is anticipated to develop due to advancements in multi-domain warfare systems and a growing emphasis on indigenous advancement. This is often pertinent in India, where the "Atmanirbhar Bharat" program promotes self-reliance in defense and aerospace, leading to the advancement of indigenous missile technologies. Modern warfare includes integrating various domains (air, land, ocean, cyber, space) to attain strategic targets. Missiles play a crucial part in this, giving long-range precision strike capabilities. The trend toward self-reliance in defense is driving demand for indigenously created missiles. Nations are investing in research and development, leading to the creation of advanced missile technologies similar to the BrahMos and Nirbhay.

BrahMos: A long-range supersonic missile created through a joint venture between India and Russia, exhibiting a successful case of international collaboration.

Nirbhay: An indigenously created long-range subsonic missile, highlighting the advancement in domestic missile technology development.

The improvement in new technologies and a focus on self-reliance are anticipated to increase the demand for missiles within the coming years.

Market Restraints

Arms Control Agreements and Trade Restrictions to Delay Adoption and Limit Market Growth

Arms control agreements and trade restrictions aim to restrain the expansion and use of weapons, often hindering their adoption and growth in the market. These measures can include treaties limiting weapon types and quantities, global agreements restricting transfers, and national regulations administering exports and imports. The impact of these measures can range from slowing down the development and sending new technologies to preventing the rise of arms markets in specific regions.

The Arms Trade Treaty (ATT): This global treaty aims to control the international exchange of conventional arms, with the goal of diminishing human suffering and promoting transparency. While the ATT has been in force for several years, some major arms exporters have not ratified it, and concerns remain about its effectiveness in controlling the global arms trade.

The Non-Proliferation Treaty (NPT): This treaty aims to prevent the spread of nuclear weapons and promotes serene uses of nuclear technology. The NPT has been a major factor in limiting the number of nuclear-weapon states, but concerns remain about the potential for proliferation.

National Regulations: Many countries have regulations overseeing the export of military technology and weapons designed to anticipate their misuse or redirection to unintended recipients. These controls can impact the global market by limiting the accessibility of certain weapons.

Market Opportunities

Geopolitical Tensions and Regional Security Needs Provides Lucrative Opportunity

Geopolitical tensions and territorial security needs are driving the global demand for advanced defense systems, especially missiles, as countries seek to bolster deterrence in the midst of escalating conflicts. Rising defense budgets, such as China's 7.2% increase in 2025 to defend national security, reflect a broader drift of military modernization due to regional instabilities.

Tensions within the Asia Pacific, the Middle East, and Eastern Europe, exemplified by the India-Pakistan conflict in May 2025, where airstrikes and drone attacks intensified along the Kashmir border, emphasize the need for precision-guided, long-range capabilities. This clash, involving high-tech weaponry and civilian casualties, highlights how geopolitical rivalries fuel arms races, with India deploying 15 BrahMos missiles to debase Pakistan's capabilities.

Similarly, maritime security concerns within the South China Sea, a hotspot for geopolitical control struggles, have incited Malaysia to advocate for stronger regional cooperation to guarantee freedom of navigation. These improvements make way for defense contractors to supply advanced missile systems as nations prioritize strategic deterrence and rapid-response capabilities to address advancing threats while navigating export controls and international arms control systems.

Cruise Missiles Market Trends

Download Free sample to learn more about this report.

Multi-Platform Integration and Advancements in Hyperspectral Technologies to Amplify Product Demand

Artificial Intelligence (AI) and autonomous frameworks, alongside stealth and evasion innovations, are transformative trends within the market, improving precision, survivability, and versatility. AI enables missiles to process real-time information, optimize flight paths, and recognize targets with negligible human intervention. Autonomous systems use AI for autonomous navigation and decision-making, reducing dependence on external guidance and improving response times in dynamic combat scenarios.

For instance, India's Indigenous Technology Cruise Missile (ITCM), tested in April 2024, showcases AI-driven guidance for precision targeting and versatility to countermeasures, displaying enhanced autonomy. These frameworks utilize advanced calculations to analyze sensor inputs, enabling rockets to adjust directions mid-flight and evade threats. Stealth and evasion technologies center on making missiles undetectable and resilient against advanced defense frameworks. Stealth designs consolidate radar-absorbing materials, low-altitude flight paths, and aerodynamic shaping to diminish radar cross-sections.

Evasion technologies incorporate electronic countermeasures and angular thrusters for quick maneuvers, permitting missiles to avoid detection. A prominent case is Russia's Kalibr missile, which utilizes stealth technology and low-altitude flight to avoid radar discovery, coupled with onboard frameworks to counter missile resistance. Together, these technologies upgrade mission success rates by guaranteeing missiles reach targets undetected and unhindered. The integration of AI with stealth capabilities makes highly successful, versatile systems, driving demand in present-day warfare for precise, survivable, and autonomous missiles, especially among driving defense powers such as the U.S., China, and Russia.

War Impact Analysis

Ongoing War Conditions and Geopolitical Tensions, Drive Demand for Indigenous and Advanced Warfare Technologies

The Russia-Ukraine, Israel-Palestine, and India-Pakistan clashes, alongside past war-like situations, have essentially formed the development, arrangement, and strategic utilization of missiles, driving advancements in technology, strategies, and proliferation.

In the Russia-Ukraine war (2022–present), Russia's extensive use of Kalibr missiles, propelled from maritime platforms, illustrated their precision and long-range capabilities, targeting the Ukrainian framework with devastating impact. These subsonic, low-flying missiles evaded early detection, inciting Ukraine to upgrade its air defense frameworks, similar to when the U.S.-supplied Patriot, to intercept them. This conflict highlighted the need for cost-effective countermeasures, as each Patriot missile costs millions compared to cheaper missiles.

Additionally, within the Israel-Palestine conflict, precision-guided missiles have been less noticeable due to the conflict's deviated nature. Still, Israel's use of advanced rocket systems, air-launched variants, against Hamas targets underscores their part in urban warfare. The 2006 Lebanon War observed Israel deploy Delilah missiles, competent in loitering and precise strikes, exhibiting their versatility in targeting versatile threats.

Furthermore, in India-Pakistan tensions, both countries developed indigenous cruise missiles in the midst of ongoing tensions, especially post-1999 Kargil War and the 2019 Balakot airstrike. India's BrahMos, a supersonic missile created with Russia, offers a 290–800 km range and flexibility across land, ocean, and air launched platforms, pointed at deterring Pakistan's tactical nuclear threats. Pakistan's Babur missile, with a 700 km range, serves as a counter, improving its deterrence against India's conventional predominance. These missiles reflect a territorial arms race, with missiles favored for their accuracy and capacity to bypass ballistic missile resistance.

Past wars, such as the 1991 Gulf War, marked a turning point for missiles, with the U.S. Tomahawk missiles making a big impact, exhibiting their capacity to strike deep, hardened targets with minimal collateral damage. This success impelled worldwide interest for these missiles, leading to expansion among state and non-state actors. Modern conflicts proceed to drive developments, such as stealth features, hypersonic speeds, and AI-guided targeting while raising concerns around escalation and arms control challenges in unstable regions.

SEGMENTATION ANALYSIS

By Missile Type

Air Launched Cruise Missiles Dominated the Market Propelled by Technological Advancements

By missile type, the market is divided into Land-Attack Cruise Missiles (LACM), Anti-Ship Cruise Missiles (ASCM), and Air-Launched Cruise Missiles (ALCM).

The Air-Launched Cruise Missiles (ALCM) segment accounted for a dominating market share and is expected to grow at the fastest CAGR in the forthcoming years. The development of ALCMs is impelled by their adaptability, long-range capabilities, and integration with modern air forces. Propelled from aircraft, ALCMs amplify the reach of air power, allowing strikes deep into the enemy domain without exposing platforms to air resistance.

Technological progressions, counting stealth features, improved propulsion, and precise route systems improve their survivability and adequacy. ALCMs are progressively favored for their capacity to carry conventional or nuclear warheads, offering vital and strategic alternatives. Demand is driven by advancing threats, territorial conflicts, and the need for rapid-response, standoff weapons, making ALCMs critical to advanced military doctrines.

The Land-Attack Cruise Missiles (LACM) segment is expected to grow at a significant CAGR in the forecast period. The development of LACMs is driven by their accuracy, flexibility, and strategic value in modern warfare. These low-flying, guided missiles can strike removed targets with high accuracy, minimizing collateral harm and enabling strikes from secure distances. Advances in guidance systems, such as GPS and terrain contour matching, improve their adequacy against hardened or mobile targets. The expansion of LACMs among countries is fueled by their capacity to project power without risking manned aircraft, coupled with moderately low costs compared to ballistic missiles. Rising geopolitical pressures and the need for non-nuclear deterrence encourage their development and deployment globally.

By Component

Advancements in Propulsion System Leads to their Dominance

By component, the market is divided into guidance systems, propulsion systems, warheads, missile airframes, sensors & seekers, and communication systems.

The propulsion systems segment accounted for a dominating market share in 2024. The growth within the industry is driven by advancements in propulsion systems, which enhance rocket performance, extend, and speed. Developments such as scramjet engines, solid rocket motors, and hybrid propulsion systems empower missiles to attain hypersonic speeds and longer ranges, meeting cutting-edge warfare demands. For instance, hypersonic missiles, fueled by advanced air-breathing engines, offer fast strike capabilities, making them harder to intercept. Also, the selection of electric propulsion systems improves fuel proficiency and maneuverability, adjusting to sustainability objectives. Rising defense budgets and geopolitical pressures advance fuel investments in these advanced propulsion innovations, driving market demand.

The guidance systems segment is expected to grow at the highest CAGR in the forecast period.

The market is propelled by progressions in guidance systems, which improve accuracy and viability. Innovations such as GPS, inertial navigation, radar, and infrared homing ensure exact targeting, minimizing collateral damage. The integration of AI improves situational awareness and target recognition, whereas miniaturization decreases system size and weight, empowering more agile missiles. Increasing geopolitical conflicts and the need for precision-guided weapons drive demand for these systems. For instance, the U.S. Department of Defense detailed in 2022 that over 90% of combat weapons were precision-guided, highlighting their basic part in advanced fighting and fueling development.

By Missile Speed

High Investments by Defense Departments Drive Hypersonic Missiles Top Position

By missile speed, the market is divided into Subsonic (Below Mach 1), Supersonic (Mach 1 - 5), and Hypersonic (Above Mach 5).

The hypersonic segment dominated the market in 2024 and is expected to grow at the highest CAGR in the forthcoming years. The development of hypersonic missiles, capable of surpassing Mach 5, is fueled by their unmatched speed, maneuverability, and key advantages. These missiles travel at low elevations with eccentric trajectories, making them difficult to identify and intercept by regular defense systems. The U.S., China, and Russia are making heavy investments due to their potential to enter advanced missile defenses, guaranteeing deterrence and power projection. Technological advancements in propulsion, such as scramjet engines, and materials science empower sustained high-speed flight. Geopolitical pressures and the need for fast, precise strike capabilities further fuel their development, reshaping advanced warfare dynamics.

The supersonic segment is expected to grow at a significant CAGR in the forecast period. Supersonic missiles, traveling between Mach 1 and Mach 5, are experiencing growth due to their balance of speed, cost, and viability. They offer speedier response times than subsonic systems, upgrading tactical advantages in time-sensitive operations. Advances in drive technologies, such as ramjets, and moved forward guidance systems increment their accuracy and lethality. Countries are modernizing arsenals to counter rising threats, with supersonic missiles giving a cost-effective choice to hypersonic missiles. Their ability to overpower older air defenses and bolster fast deployment in regional conflicts drives demand. Moreover, export markets and collaborative defense programs accelerate their expansion.

By Launch Platform

Stealth Innovation in Aircrafts and Bombers Led to Airborne Segment’s Dominance

By launch platform, the market is divided into airborne, ground-launched, and naval.

The airborne segment dominated the global market in 2025 and is expected to grow at the highest CAGR in the forecast period. The development of airborne launch platforms for missiles is driven by their vital flexibility, amplified range, and improved survivability. Aircraft such as bombers and stealth fighters can dispatch missiles from thousands of miles away, bypassing enemy air defenses. Progressed avionics, precision-guided systems, and stealth innovation improve precision and diminish detection risks. This allows quick, adaptable strikes in diverse scenarios, making air-launched missiles a basic resource for modern air forces seeking global control.

The naval segment is estimated to grow at the second-highest rate during the forecast period. Maritime launch platforms, including submarines and warships, fuel missile growth due to their stealth, mobility, and global reach. Submarines empower covert dispatches, minimizing detection, whereas surface ships can unleash large missile salvos for overpowering strikes. Their capacity to operate in challenging sea environments, coupled with advanced targeting systems, guarantees precise, long-range attacks. This flexibility and vital positioning make maritime platforms irreplaceable for modern maritime warfare.

By Missile Range

Short-Range Missiles Hold Leading Share Owing to their Cost-Effectiveness and Flexibility in Warfare

Based on missile range, the market is sub-segmented into Short Range (Below 1000 km), Medium Range (1000-3000 km), and Long Range (Above 3000 km).

The short-range segment accounted for a dominating market share in 2025 and is expected to grow at a significant CAGR in the forthcoming years. Short range missiles are increasingly being produced due to their flexibility in tactical warfare, offering quick response and high precision for front-line targets. Advances in compact electronics and direction systems empower cost-effective, agile missiles deployable from different platforms, including ships and aircraft. Regional conflicts and deviated threats drive their adoption by smaller countries. Improved maneuverability and low-altitude flight capabilities allow these missiles to avoid radar, expanding their effectiveness in advanced combat scenarios.

The long-range is expected to grow at the highest CAGR in the forthcoming years. The development of long-range missiles is driven by advancements in precision guidance, stealth innovation, and propulsion systems, empowering strikes over thousands of kilometers with pinpoint accuracy—geopolitical tensions, especially in contested regions such as the Indo-Pacific, fuel demand for vital deterrence. Countries invest in these missiles to project control, counter anti-access/area-denial strategies, and bypass advanced air defenses. Hypersonic and autonomous technologies enhance their range, speed, and lethality, impelling global proliferation.

To know how our report can help streamline your business, Speak to Analyst

By Guidance Technology

Real-Time Tracking is the Preferred Guidance Technology Owing to its Quick Response and Improved Connectivity

By guidance technology, the market is divided into autonomous, real-time tracking, and swarm intelligence.

The real-time tracking segment dominated the global cruise missiles market share in 2025. Advanced sensors, satellite communication, and AI integration drive the growth of real-time tracking. These advances enable precise target tracking and mid-flight course adjustments, improving accuracy and viability—global defense demands for quick response to dynamic threats fuel investment. Improved connectivity, such as 5G and secure information links, ensures real-time data transmission. Also, geopolitical rivalries and the need for precision strikes in complex situations accelerate advancement and deployment.

The autonomous segment is estimated to grow at the highest rate during the forecast period. Autonomous missiles are developing due to breakthroughs in AI, machine learning, and sensor fusion. These systems permit independent navigation, deterrent avoidance, and real-time decision-making, reducing human intervention. Rising geopolitical tensions and defense modernization push countries to create precise, low-collateral weapons. Progresses in compact electronics and computing power enhance autonomy. Moreover, cost-effective production and worldwide arms competition drive quick innovation and adoption of these modern, self-guided missile systems.

By Operational Mode

Pre-Programmed Targets is the Leading Operational Mode with Proliferation of Missile Innovation and Request for Cost-Effective, Precise Weaponry

By operational mode, the market is divided into pre-programmed targets, dynamic targeting/in-flight retargeting, and loitering /patrolling.

The pre-programmed targets segment dominated the global market in 2025. The growth of pre-programmed target missiles is driven by advancements in precision direction technologies, such as GPS, TERCOM, and DSMAC, empowering accurate strikes over long distances. Their low-altitude flight paths and stealth highlights evade radar detection, making them perfect for targeting high-value resources such as command bunkers or ships. Rising global tensions, the proliferation of missile innovation, and the request for cost-effective, precise weaponry further fuel their advancement and deployment.

The patrolling segment is expected to grow at a significant CAGR in the forthcoming years. Patrolling missiles, akin to loitering munitions, have developed due to their capacity to provide persistent reconnaissance and quick response capabilities. Prepared with AI and advanced sensors, they can autonomously patrol, identify, and lock in moving targets with high accuracy. Their adaptability, combined with advancements in propulsion and miniaturization, allows for amplified ranges and reduced detectability, meeting modern warfare's requirement for versatile, real-time strike alternatives.

Supply Chain Analysis

Key Components

- Guidance Systems: GPS, inertial navigation, terrain mapping.

- Propulsion: Jet engines (subsonic, supersonic, hypersonic).

- Payloads: Conventional or nuclear warheads.

- Materials: Titanium, composites, semiconductors.

Supply Chain Dynamics

- Sourcing: Global, with risks from trade restrictions and geopolitical tensions. Missiles require specialized components such as guidance systems (e.g., GPS, inertial navigation), propulsion (jet engines), and materials (titanium, composites, semiconductors). These are sourced from a limited number of trusted suppliers, often concentrated in the U.S., Europe, or Asia. Geopolitical tensions, such as the U.S.-China trade disputes or sanctions on Russia, can disrupt access to critical materials such as rare earth metals or chips.

- Manufacturing: Precision engineering in secure facilities. Production involves precision engineering in secure, specialized facilities to meet strict defense standards. Only a few contractors (e.g., Raytheon Technologies and Lockheed Martin) have the expertise and clearance to assemble these systems, creating bottlenecks.

- Disruptions: COVID-19 pandemic caused material shortages; semiconductor scarcity persists. External shocks, such as the COVID-19 pandemic, exposed vulnerabilities, causing delays due to factory shutdowns or semiconductor shortages. Single-source suppliers amplify risks—if one fails, production halts.

- Regulations: ITAR and export controls limit international collaboration. Strict export controls (e.g., ITAR) limit international collaboration, forcing reliance on domestic or allied suppliers, which can increase costs and lead times.

Challenges

- Single-Source Risks: Reliance on specialized suppliers.

- R&D Costs: High for advanced technologies such as stealth and hypersonic.

- Labor: There is a need for skilled engineers and technicians.

Mitigation Strategies

- Diversification: Expanding supplier networks.

- Local Production: Reducing dependency on foreign components.

- Innovation: Investing in 3D printing and AI for efficiency.

Cruise Missile Market Regional Outlook

By region, the market is studied into North America, Europe, Asia Pacific, Middle East, and the rest of the world.

North America

North America Cruise Missiles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 2.62 billion in 2025, representing 32.20% of the global industry, and is expected to reach USD 2.74 billion in 2026. North America, particularly the U.S., is growing rapidly due to the rise in defense modernization and geopolitical tensions around the world. The region invests heavily in advancing technologies and modernization programs such as AGM-158 JASSM and Tomahawk Block V. There is an emphasis on precision strikes and a rising preference for hypersonic systems and A2/AD countermeasures that subtly drive demand for the same. The interoperability of NATO enhances procurement initiatives, thus driving market growth.

Europe

Europe recorded a market size of USD 2.47 billion in 2025, capturing 30.42% of the global market share, and is projected to reach USD 2.62 billion in 2026. The growth in this region is attributed to increased NATO defense spending and increasing threats and geopolitical uncertainties in the Eastern-Europe region. European Union-backed projects such as FC/ASW aim at new and advanced missile systems. High emphasis on stealth enabled high range munition support propels market growth in the region.

Asia Pacific

In 2025, Asia Pacific represented USD 1.55 billion, accounting for 19.12% of the worldwide market, and is projected to grow to USD 1.63 billion in 2026. Rising military expenditures and rising tensions in the South China sea, Indo-Pak rivalries significantly propel market growth. Countries are heavily investing in creating indigenous missiles due to ongoing tension. China and India and advancing BrahMos and CJ-10 missiles as indigenous production; this, in turn, is expected to lead to significant regional market growth.

Middle East

Middle East & Africa contributed 14.07% to the global market in 2025, with a valuation of USD 1.14 billion, and is projected to reach USD 1.21 billion in 2026. The Middle East is anticipated to witness moderate growth during the forecast period. Regional conflicts, threats, and active wars from neighboring countries have led countries in the Middle East to invest in missiles. Demand for advanced missile systems is rising in the region to boost the defense capabilities of Saudi Arabia and Turkey. Israel has an ongoing war with Palestine and, therefore, is readily investing in as much advanced propulsion and precision strikes as possible.

Rest of the World

The rest of the world is expected to experience significant growth during the forecast period. The Latin America market was valued at USD 0.34 billion in 2025, capturing 4.19% of global revenue, and is estimated to reach USD 0.35 billion in 2026. The market in Latin America and Africa is expected to grow with the focused modernization of naval and air forces. Increased border security, development and modernization programs, and transnational threats drive regional cruise missiles market growth.

Competitive Landscape

Key Market Players

Leading Players Focusing on Integrating Advanced Technologies for Precision Strikes

The market is highly competitive, featuring key players such as Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, Thales Group, and BAE Systems plc. These companies are highly focused on precision guidance, stealth, supersonic/hypersonic capabilities, and extended range.

AI-based targeting and vertical launch capabilities intensify competition in the market. Strategic alliances, defense export policies, and indigenous development are all key factors in the competitive landscape for the market.

LIST OF KEY CRUISE MISSILES MARKET PLAYERS PROFILED

- Raytheon Technologies Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- MBDA (France)

- Tactical Missile Corporation (KTRV) (Russia)

- Northrop Grumman Corporation (U.S.)

- BrahMos Aerospace (India)

- China Aerospace Science and Industry Corporation (CASIC) (China)

- Roketsan (Russia)

- NPO Mashinostroyeniya (Russia)

- Israel Aerospace Industries Ltd. (Israel)

- Korea Aerospace Industries Ltd. (South Korea)

- LIG Nex 1 (South Korea)

- Saab AB (Sweden)

- Aerojet Rocketdyne (U.S.)

- Denel Dynamics (South Africa)

KEY INDUSTRY DEVELOPMENTS

- June 2025: German defense company Rheinmetall and Anduril Industries, U.S.-based conglomerate unveiled a partnership to jointly develop cruise missiles, combat drones, and solid-fuel rocket motors for the European market including Anduril’s Barracuda family of low-cost cruise missiles and the YFQ-44 jet-powered combat drone.

- April 2025: A Hyderabad-based laboratory of Defence Research and Development Organisation (DRDO), Defence Research & Development Laboratory (DRDL), unveiled a milestone in the field of Hypersonic Weapon Technology. The organization conducted long-duration active cooled scramjet subscale combustor ground testing for over 1,000 seconds at the test facility at Hyderabad.

- January 2025: The Bundeswehr and TAURUS Systems GmbH, a joint venture between European missile house MBDA and Sweden's Saab, unveiled a contract for the support and modernization of the TAURUS KEPD 350 air-launched cruise missiles.

- November 2024: The U.S. has unveiled arming its submarines with nuclear-armed cruise missiles after a gap of about three decades. The US Naval force has issued a Request for Information (RFI) for a Sea-Launched Nuclear Cruise Missile (SLCM-N) in an offer to create a flexible cruise missile framework.

- November 2024: The Defence Research and Development Organisation (DRDO) conducted the maiden flight test of Long Range Land Attack Cruise Missile (LRLACM) from the Integrated Test Range (ITR), Chandipur, off the coast of Odisha on November 12, 2024, from a versatile enunciated launcher.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on important aspects, such as key players, products, applications, and platforms depending on various countries. Moreover, it offers deep insights into the market trends, competitive landscape, market competition, pricing of cruise missiles, and market status and highlights key industry developments. In addition, it encompasses several direct and indirect factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.16% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Missile Type

|

|

By Component

|

|

|

By Missile Speed

|

|

|

By Launch Platform

|

|

|

By Missile Range

|

|

|

By Guidance Technologies

|

|

|

By Operational Mode

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 8.55 billion in 2026 and is anticipated to be USD 12.78 billion by 2034.

The market is likely to grow at a CAGR of 5.16% during the forecast period.

The top players in the industry are Lockheed Martin Corporation, Raytheon Technologies Corporation, and Northrop Grumman Corporation.

In 2025, North America dominated the global market.

Advancements in propulsion system drives the components segment.

- 2021-2034

- 2025

- 2021-2024

- 350

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us