Targeting Pod Market Size, Share & Industry Analysis, By ype (FLIR & Laser Designator Pods, Laser Designator Pods, FLIR Pods, and Laser Spot Tracker Pods), By Component (FLIR Sensor, Charge Coupled Device (CCD) Camera, Environmental Control Unit (ECU), Moving Map System (MMS), Digital Data Recorder, Video Data Link, and Processor), By Platform (Combat Aircraft, Unmanned Aerial Vehicles (UAVs), Attack Helicopters, and Bombers), By Fit (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

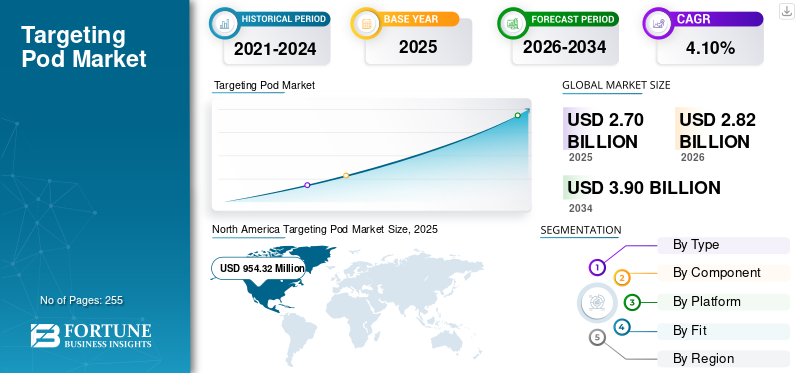

The global targeting pod market size was valued at USD 2709.6 million in 2025. The market is projected to grow from USD 2826 million in 2026 to USD 3,907.80 million by 2034, exhibiting a CAGR of 4.10% over the forecast period. North America dominated the targeting pod market with a market share of 35.20% in 2025.

The targeting pod market is expected to witness significant growth during the forecast period, driven by modernization programs and advancements in targeting systems. These systems enhance precision and situational awareness for combat aircraft, UAVs, and helicopters, reflecting a global shift toward improved defense capabilities.

For Instance, in January 2019, the U.S. Air Force awarded Northrop Grumman Corporation a contract worth USD 1.3 billion to supply an indefinite quantity of Litening advanced targeting system and provide the services such as sustainment, production, software, and upgrades.

Additionally, increasing geopolitical tension and ongoing conflicts between nations are propelling market growth. The Russia-Ukraine war has allowed the countries to focus on modernizing their aircraft fleets with advanced equipment, such as modern targeting systems, which can work in harsh environmental conditions.

Key players, such as Lockheed Martin, Northrop Grumman, and Raytheon Technologies, are continuously on research and development of innovative solutions to improve targeting system technologies and actively innovating solutions to address challenges such as limitations of terrestrial sensors, data quality, and bias in artificial intelligence (AI) systems, and the unpredictability of AI decision-making processes. These efforts aim to enhance system efficiency and expand their global presence.

Thus, the market is expected to grow over the forecast period due to the increasing defense budget, investments by key players to develop technologically advanced targeting systems, and increasing geopolitical tensions.

For Instance, in November 2021, Aselsan signed an agreement with Motor-Sich and Ukroboronprom. Under this agreement, EO equipment is supplied under the Mi-8 Helicopter Modernization program.

Download Free sample to learn more about this report.

Targeting Pod Market Key Takeaways

- 2025 Market Size: USD 2,709.6 million

- 2026 Market Size: USD 2,826 million

- 2034 Forecast Market Size: USD 3,907.80 million

- CAGR: 4.10% (2026–2034)

- North America dominated the market with a 35.20% share in 2025.

- The FLIR & laser designator pods segment is projected to lead the market with a 42.39% share in 2026.

- The combat aircraft segment is expected to dominate the market, accounting for 61.56% of the global market in 2026.

Asia Pacific

Asia Pacific held USD 596.11 million in 2025 and is projected to reach USD 625.67 million in 2026.

North America

North America generated USD 954.32 million in 2025 and is projected to reach USD 996.72 million in 2026.

Europe

Europe accounted for USD 783.62 million in 2025 and is expected to grow to USD 811.62 million in 2026.

U.S.

U.S. market is projected to reach USD 814.02 million by 2026.

Japan

Japan market is projected to reach USD 101.42 million by 2026.

Read More

Market Dynamics

Market Drivers

Increasing Defense Budgets and Modernization of Military Operations Programs to Propel Targeting Pod Market Growth

The targeting pod market is showing significant growth. This is due to their versatile role in aircraft systems, which add extra capabilities to modern and old aircraft fleets by identifying targets and guiding precision-guided munitions (PGM) to hit them with laser-guided bombs. As these pods can be mounted on any platform, ranging from fighter aircraft to unmanned aerial systems, they serve wide applications in modern warfare.

In September 2024, the Pentagon awarded Lockheed Martin a contract valued at $5.1 billion for Block 4-related upgrades of the F-35 Lightning II fighter jet. These upgrades are part of ongoing efforts to enhance the aircraft's capabilities, including advanced hardware and software improvements. Additionally, Lockheed Martin's facility in Orlando, Florida, is responsible for manufacturing the Electro-Optical Targeting System (EOTS), a critical component of the F-35 that provides precision targeting and situational awareness.

Additionally, increasing geopolitical tension has resulted in Nations focusing on the Military modernization program. The targeting system's capability to integrate with the targeting systems and platforms and technological advancements makes it an important part of such a program. Innovation in material science to make pods lighter weight with increased payload capacity further propels the market growth. Innovation in materials, such as carbon alloy, composite material, and resigns has increased material payload capacity without affecting strength or payload capabilities. This advancement fuels the adoption of targeting systems designed specifically for unmanned aircraft systems, which have comparatively low payload capacity.

Market Restraints

High Development and Procurement Costs Restrain Market Growth

Developing advanced targeting systems requires high investment in innovative technologies, such as thermal imaging, laser designation, and data link capabilities. The high initial cost limits their adoption, especially in nations with restricted defense budgets. Moreover, the expense involved in integrating these pods with old or existing platforms, such as fighter jets or drones, is an additional challenge faced by several defense forces globally. Maintenance costs and the need for frequent upgrades or repairs to match improving technology standards further add to the budgets, making it more challenging for new players to enter the market.

Additionally, stringent export regulations and geopolitical concerns associated with targeting systems are obstacles to targeting pod market growth. Targeting systems are crucial and sensitive defense equipment, and the transfer or sale of these systems or related components is subject to International in Arms Regulations (ITAR). Nations that are dependent on imports of military equipment may face challenges or denial of adopting this technology due to political tensions or compliance requirements, further hampering market growth.

For instance, in July 2019, the U.S. removed Turkey from the F-35 program due to political tensions, blocking its access to associated targeting systems and causing delays in the country's defense modernization plans.

Market Opportunities

Modernization Program of Military Aircraft to Present New Opportunity

Countries across the globe are focusing on modernizing their military aircraft programs, which presents a significant market opportunity for the market. They are upgrading their defense capabilities to counter emerging threats, such as MANPADs and laser-guided missiles, leading to increased demand for advanced targeting systems.

Targeting pods that include technologies, such as laser designators, infrared sensors, and GPS are becoming highly significant for precise strikes in modern warfare. Asia Pacific and the Middle East are contributing to the market, where defense spending is rising due to territorial conflicts and the need for advanced military equipment. Additionally, the demand for multi-role aircraft necessitating modern targeting systems is further driving the demand for targeting systems.

For Instance, in October 2024, the U.S., through Foreign Military Sale, awarded Lockheed Martin a contract worth USD 90.68 million to deliver sniper advanced targeting systems to Poland. The contract involves Sniper Advanced Targeting systems with two-way datalinks, system support, and spare parts.

Moreover, the integration of targeting systems with unmanned aerial vehicles will fuel market growth further. The development of drones for surveillance and combat operations is growing, and countries are significantly adopting this trend with advanced targeting systems. Targeting systems improve situational awareness and accuracy in strikes and support real-time data transfer, making them an important component for UAVs.

Targeting Pod Market Trends

The Shift toward Lightweight and Compact Systems is an Emerging Trend in the Market

Manufacturers are focusing on developing smaller and more efficient targeting systems that can be easily integrated into a wide range of platforms, including smaller fighter jets and UAVs. This innovation is driven by advancements in material and small-scale components, such as sensors and processors, which reduce the system's overall size and weight without disturbing or compromising its capabilities. The European region drives the demand for such systems, which focus on solutions that are multipurpose and multi-adaptable over traditional systems.

For Instance, in October 2023, Northrop Grumman partnered with South Korea’s LIG Nex1 to develop advanced targeting systems and airborne electronic warfare solutions for the Republic of Korea. This collaboration underscores the trend of nations investing in modernizing their defense capabilities through international partnerships.

- North America witnessed targeting pod market growth from USD 1003.86 Million in 2023 to USD 913.97 Million in 2024.

Additionally, the emerging adoption of artificial intelligence (AI) and machine learning (ML) technologies in targeting systems has also evolved as a trend in the market. AI-powered targeting systems can process and analyze battlefield data in real time, resulting in faster and more accurate target identification. Moreover, these systems improve threat detection by identifying patterns and analyses that traditional methods may not notice. The integration of AI and ML is expected to change the targeting systems, making them more effective in hard situations. In the coming years, this trend will probably grow as nations focus on modernizing and automating solutions to improve their operational completeness.

Download Free sample to learn more about this report.

Impact of the Russia-Ukraine War

Geopolitical Tensions Affecting Operations have Influenced the Market Amid the Russia-Ukraine War

The conflict between Russia and Ukraine has significantly influenced the market. This impact can be analyzed through various parameters related to both countries and their implications on global military procurement and modernization programs.

Increased Defense Spending and Demand for Advanced Targeting Systems

The conflict has shown the importance of targeting systems in identifying and neutralizing the target with precise aiming capabilities. Targeting systems play an important role in identifying threats and guiding the weaponry so that they can hit the target with precision, improving mission efficiency. Additionally, their mounting capabilities to exit the fleet and modernize the fleet with advanced targeting systems further drive product demand. For Instance, in May 2021, the Russian Aerospace Forces received SU-34 Bombers equipped with advanced multipurpose targeting systems under the Synch program. Moreover, according to the TASS Russian news agency, in the coming years, several aircraft will be equipped with reconnaissance pods to enhance the ability of the Su-34 to detect ground targets of all types.

Integration with Modern Warfare Technologies: -

The war has increased the pace of integrating targeting systems with advanced technologies, such as AI, UAVs, and electronic warfare systems. For Instance, in December 2024, Thales worked to integrate AI into the TALIOS laser designation pod for the French Air and Space Force. This improvement will expand the Rafale's combat capabilities, allowing pilots to operate in complex combat environments by using deep learning technologies.

Challenges in Urban and Hybrid Warfare and Disturb the Supply Chain: -

The Russia-Ukraine conflict involved both conventional and hybrid warfare, where combat zones often were the civilian areas. This makes targeting systems more important. These systems need to work according to complex situations, such as identifying UAS, distinguishing combatants from non-combatants, and operating in an electronic warfare environment.

Due to sanctions on Russia and geopolitical tensions, the conflict has disrupted the global supply chain for defense equipment, including targeting system components. This has resulted in disruption in production and increased spare part costs. To tackle this situation, manufacturers took various proactive measures to reduce dependence on disrupted supply chains. For Instance, in September 2024, Saab announced plans to establish production facilities in Ukraine as part of efforts to bolster the country's independent defense capabilities. The Swedish defense company aims to collaborate with Ukrainian defense contractors to manufacture drone technologies, ammunition components, and sensor technology. This initiative reflects Saab's commitment to helping Ukraine develop sovereign capacity while transitioning the Western arms industry from donation-based aid to direct partnerships.

SEGMENTATION ANALYSIS

By Type

FLIR and Laser Designator Pods Dominated the Market, Fueled by their Enhanced Situational Awareness Capability

The market is classified by type into FLIR & laser designator pods, laser designator pods, FLIR pods, and laser spot tracker pods.

FLIR & laser designator pods is estimated to dominate the market with the largest share of 42.39% in 2026 due to their important role in precision strikes and enhanced situational awareness. These systems are used for wide applications ranging from air-to-ground and air-to-air operations, providing high-resolution imagery and real-time target designation in diverse weather conditions. Defense forces are widely adopting these pods for modernized fighter jets, UAVs, and other combat platforms.

For Instance, in April 2024, Sweden awarded Saab a contract worth USD 37 million to supply litening 5 target designator pods. The pods will be integrated with the country’s Gripen multi-role fighter aircraft. Delivery for the pods and maintenance support will take place in 2026.

The FLIR pods segment is expected to experience the fastest growth at the highest CAGR during the forecast period. FLIR pods are capable of operating in low-visibility conditions, such as nighttime and tough weather. The increasing demand for advanced surveillance and reconnaissance capabilities, especially for UAVs and rotary-wing aircraft, is driving this growth. Additionally, with advancements in material and components, FLIR pods are becoming compact and lightweight, allowing integration with a wide range of platforms.

By Component

FLIR Sensors Dominated the Market due to their Rapid Adoption in Military and Defense Applications

The market is segmented by component into FLIR Sensor, Charge Coupled Device (CCD) Camera, Environmental Control Unit (ECU), Moving Map System (MMS), digital data recorder, video data link, and processor.

The FLIR (Forward Looking Infrared) sensor segment is projected to dominate the market with the largest share of 23.52% in 2026. FLIR sensors provide advanced thermal imaging capabilities that are important for a wide range of military and defense applications. Additionally, FLIR sensors provide extra advantages in low-light and worse weather conditions by providing clear, detailed imagery that can give a better understanding of the current situation and help in target identification. As military operations increasingly focus on precision and efficiency, the demand for FLIR sensor technology continues to grow.

For Instance, in July 2023, the U.S. Army awarded Raytheon a contract worth USD 117.5 million to supply low-rate initial production of 3rd Generation Forward Looking Infrared (3GEN FLIR) B-Kit Sensors. Under the contract, RTX will deliver 3GEN FLIR B-Kit sensors for the U.S. Army platform.

The Moving Map System (MMS) segment is expected to witness the fastest growth during the forecast period. This growth is attributed to the increasing demand for integrated navigation and situational awareness systems with modern aircraft and UAVs. These systems can offer real-time geographic data, improve pilots' decision-making, and increase the overall effectiveness and success rate of the mission. As advancements in technology give birth to innovative and reliable mapping solutions, with increasing importance on digital warfare and network-centric operations, the moving map system segment is quickly gaining attention, driving the demand in the market.

For instance, in May 2024, the U.S. State Department agreed to the sale of 34 Sniper Advanced Targeting Pods (ATPs) for the FA-50 Fighters, which Poland is buying from South Korea

By Platform

Combat Aircraft Segment Dominated the Market due to Increasing Focus on Precision Strikes

The market is segmented by platform into combat aircraft, unmanned aerial vehicles (UAVs), attack helicopters, and bombers.

Among platforms, the combat aircraft segment will dominate the market, accounting for the largest market share of 61.56% in 2026 and is also expected to dominate the market during the forecast period. This is attributed to the widespread and long-time use of manned fighter jets in military operations. These aircraft play an important role in combat missions, which require highly advanced targeting systems to improve their effectiveness in both air-to-air and air-to-ground operations. The increasing defense budgets, ongoing modernization efforts, and increasing focus on precision strikes further increase the demand for combat aircraft in the market.

The unmanned aerial vehicles segment is expected to notice the fastest growth due to the highest CAGR during the forecast period. This is attributed to their versatility in targeting system missions, cost-effectiveness, and ability to conduct missions in high-risk environments without putting human pilots' lives at risk. The Russia-Ukraine war has demonstrated the importance of UAVs on the battlefield. Nations are increasingly adopting drone technology for surveillance, reconnaissance, and strike operations, and the need for advanced targeting systems tailored for UAVs is rapidly expanding. The shift toward unmanned systems show the broader trends in defense strategies, driving accelerated growth of the segment in the market.

- The attack helicopters segment is expected to hold a 16.89% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Fit

OEM Segment Dominates the Market, Fueled by Growing Integration of Advanced Targeting Systems into New Aircraft Platforms

The market is segmented into OEM and aftermarket, based on fit.

OEM is estimated to dominates the market in the fit segment with share of 67.64% in 2026, fueled by the growing development and integration of advanced targeting systems into new aircraft platforms. OEMs have made strong relationships with defense contractors and military organizations, which allows them to provide tailored solutions that meet specific operational requirements. The high demand for new and modernized programs for aircraft, with the need for innovative and advanced cutting-edge technology to improve mission effectiveness, reinforces the OEM segment, fueling the segment’s growth.

The aftermarket is experiencing rapid growth, propelled by the increasing focus on maintenance, upgrades, and support for existing systems. As nations' military budgets increase, they are focusing on increasing the operations life of current platforms rather than investing in new aircraft acquisitions. This has resulted in a rising demand for aftermarket services, such as retrofitting and software upgrades. Additionally, as technology evolves, the demand for retrofitting older aircraft fleet systems with updated capabilities becomes more important, which fuels the segment’s growth in the market.

For Instance, in January 2019, the U.S. Air Force awarded Northrop Grumman a contract worth USD 1.3 billion to upgrade and sustain its Litening advanced targeting system. The Litening pod is installed on a variety of USAF and U.S. Marine Corps aircraft, including the McDonnell Douglas AV-8B Harrier II, Fairchild Republic A-10 Thunderbolt II, Boeing B-52 Stratofortress, Lockheed Martin C-130 Hercules, Boeing F-15E Strike Eagle, Lockheed Martin F-16 Fighting Falcon, and Boeing F/A-18 Super Hornet.

Supply Chain Analysis

Raw Material Suppliers

- Key Suppliers:

- Lockheed Martin: Supplies materials for targeting systems and components.

- Raytheon Technologies: Provides advanced materials and electronics systems for Targeting solutions.

- Challenges:

- Price Fluctuations: Variations in material costs can affect overall system pricing.

- Supply Disruptions: Geopolitical tensions or natural disasters may lead to a shortage of raw materials.

- Regulatory Compliance: Suppliers must adhere to strict regulations, especially for dual-use materials.

Component Suppliers

- Key Suppliers:

- Elbit Systems: Offers various targeting solutions and technologies for defense applications.

- BAE Systems plc., and FLIR System: Supplies critical components for targeting systems, including transponders and receivers.

- Challenges:

- Technological Changes: Rapid advancements necessitate continuous innovation from suppliers.

- Quality Assurance: Consistency in quality is crucial for system reliability.

- Intellectual Property Protection: Safeguarding proprietary technologies is challenging.

Manufacturers

- Prime Contractors:

- Lockheed Martin Corporation: Integrates Targeting technologies into broader defense systems.

- Northrop Grumman Corporation: Develops advanced Targeting systems for military applications.

- Challenges:

- Supplier Coordination: Managing multiple suppliers for seamless integration is complex.

- Budget Management: Large projects often overrun budgets due to unforeseen issues.

- Regulatory Adherence: Compliance with international regulations, such as ITAR, complicates project management.

- Tier 1 / Tier 2 Suppliers:

- Lockheed Martin (Tier 1): Develop Targeting Systems.

- Northrop Grumman (Tier 2): Provides associated technologies for Targeting applications.

- Challenges:

- Specification Changes: Tier suppliers may struggle if prime contractors alter requirements.

- Competitive Pressure: Intense competition can squeeze margins.

- R&D Investment Needs: Continuous investment is necessary to address evolving threats.

Distributors

- Defense Procurement Agencies:

- U.S. Department of Defense (DoD): Oversees military procurement in the U.S.

- Bundesamt für Ausrüstung, Informationstechnik und Nutzung der Bundeswehr (BAAINBw): Manages German military procurement.

- Direction Générale de l'Armement (DGA): Handles French defense procurement.

- Challenges:

- Procurement Delays: Lengthy processes can affect operational readiness.

- Budget Fluctuations: Changes in defense budgets impact procurement plans.

- Regulatory Navigation: Agencies face complex regulations while acquiring advanced technologies.

- Contractors & System Integrators

- Key Companies:

- L3Harris Technologies, Inc.: Integrates communication and Targeting systems integration.

- Challenges:

- Technology Compatibility: Ensuring compatibility among Targeting system technologies and Targeting systems.

- Adaptability Requirements: Flexibility is required to meet changing military needs.

- Quality vs. Cost Balance: Meeting stringent military standards while controlling costs is essential.

- Key Companies:

End Users

- Army Aviation Forces

- Naval Aviation Forces

- Air Forces

Role of ITAR in Supply Chain

- The International Traffic in Arms Regulations (ITAR) significantly influences the supply chain for airborne countermeasures by regulating defense-related exports.

Impacts:

- Compliance Necessity: Companies must comply with ITAR to prevent unauthorized access to sensitive technologies.

- Collaboration Complications: ITAR compliance complicates international partnerships due to export licensing requirements.

- Cost and Delay Increases: Adhering to ITAR can lead to higher administrative costs and potential delays in product delivery.

Targeting Pod Market Regional Analysis

The market is segmented by region into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America

North America Targeting Pod Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 35.22% of the global market in 2025, generating USD 954.32 Million in revenue, and is projected to reach USD 996.72 Million in 2026. This region's market is driven by advancements in defense technology and increasing defense budgets. The U.S. military operates several aerial platforms equipped with targeting systems, which are important for precision targeting in tight combat situations. U.S. is increasing its focus on upgrading old fleets with modern targeting systems and adopting UAV technology to enhance its military capabilities. Additionally, ongoing investments in modernization programs and the integration of next-generation targeting technologies are expected to propel the market growth further. The U.S. market is projected to reach USD 814.02 million by 2026.

For Instance, in May 2024, the Malaysian government awarded Lockheed Martin and Boeing contracts worth USD 80 million to acquire ten AN/AAQ-33 Sniper Advanced Targeting Systems. This system is equipped with high-definition sensors and a laser spot tracker, as well as improved targeting and reconnaissance capabilities for air-to-air and air-to-ground missions.

Europe

Europe maintained a strong presence in the global market, reaching USD 783.62 Million in 2025, accounting for 28.92% share, and is expected to reach USD 811.62 Million in 2026. This region's growth is attributed to government collaboration and the focus on modernization program measures amidst rising geopolitical tension and Russia-Ukraine conflicts. With geopolitical tensions in Eastern Europe, nations are continuously investing in upgrading their aerial systems. Countries such as the U.K., France, and Germany are key players in the development and procurement of advanced targeting systems. Moreover, collaborations between European defense contractors and technological advancements in sensors and imaging technologies further boost the market growth in this region. The UK market is projected to reach USD 121.91 million by 2026, while the Germany market is projected to reach USD 145.04 million by 2026.

For Instance, in February 2022, the French government announced that Indonesia had agreed to buy six Rafale fighter jet contracts worth USD 8.1 billion. Under this contract, the French manufacturer Dassault Aviation will deliver the 42 Rafale fighter jets to Indonesia.

Asia Pacific

In 2025, Asia Pacific generated USD 596.11 Million, contributing 22.00% to global market revenue, and is projected to grow to USD 625.67 Million in 2026. The Asia Pacific region is witnessing the fastest growth owing to the highest CAGR in the market during the forecast period. The market growth is driven by rising military expenditures, modernization programs, and increasing regional conflicts. Nations, such as China, India, and Japan are improving their air force capabilities and increasing investment in advanced military technologies, including precision-guided systems. The increasing focus on regional security issues, territorial arguments, and defense partnerships is propelling these nations to acquire and develop advanced targeting solutions. Moreover, the growing number of UAV developments in the region further boosts the demand for efficient targeting systems. The Japan market is projected to reach USD 101.42 million by 2026, the China market is projected to reach USD 218.55 million by 2026, and the India market is projected to reach USD 84.09 million by 2026.

For Instance, in September 2024, the U.S. Navy and the Royal Australian Air Force signed an agreement worth USD 74 million to enhance F/A-18F Super Hornets by acquiring 12 ASG-34A(V)1 Block II Infrared Search and Track systems.

Middle East & Africa

The Middle East & Africa region are anticipated to experience moderate growth during the forecast period. Middle East & Africa recorded a market size of USD 250.37 Million in 2025, capturing 9.24% of the global market share, and is projected to reach USD 262.82 Million in 2026. Countries, including Saudi Arabia and the UAE, are investing heavily in their military capabilities, including acquiring advanced aerial platforms equipped with targeting systems. Additionally, the rise of non-state actors and ongoing conflicts in regions, including North Africa, contribute to the need for advanced targeting solutions.

For Instance, in February 2020, the UAE Air Force and Air Defense awarded Lockheed Martin a contract to supply Sniper Advanced Targeting systems for the Mirage aircraft fleet. Additionally, under this contract, the company will deliver spares and upgrades.

Latin America

Latin America is experiencing significant growth but at a lower rate during the forecast period. The Latin America market generated USD 125.18 Million in 2025, representing 4.62% of the global market landscape, and is expected to reach USD 129.15 Million in 2026. Nations, such as Brazil, Argentina, and Colombia, are beginning to invest in advanced defense technologies to address internal security challenges and external threats. Increased defense budgets and partnerships with North American and European defense contractors will propel the market's growth. However, regional economic challenges and budget constraints could influence the pace of growth.

The market is poised for growth across all regions, driven by factors such as military modernization, geopolitical tensions, and technological advancements. Each region offers its opportunities and challenges, shaping investment strategies and influencing market growth.

Competitive Landscape

Key Market Players

Leading Players are Focusing on Integrating Advanced Technologies in Targeting Systems to Increase the Global Presence

The targeting pod market is characterized by a competitive landscape featuring key players such as Lockheed Martin, Northrop Grumman, and BAE Systems. These companies are leveraging advanced technologies, including AI and electronic warfare systems, to enhance the effectiveness of their identification solutions against evolving threats, such as drones and unmanned aerial vehicles. The increasing geopolitical tensions and military modernization programs are driving demand for sophisticated targeting systems across military platforms.

Regional dynamics play a significant role in shaping the competitive environment, with North America leading due to its substantial defense budgets and technological advancements, followed by Europe and the Asia Pacific region. The market is expected to grow robustly as key players continue to innovate and expand their product offerings to meet the increasing demand for effective identification solutions in military operations. Overall, the focus on technological integration and enhancing aircraft survivability against friendly and hostile fire will drive significant growth in the targeting system market over the coming years.

LIST OF KEY TARGETING POD COMPANIES PROFILED

- Lockheed Martin Corporation (the U.S.)

- Teledyne FLIR LLC (the U.S.)

- RTX Corporation (the U.S.)

- Northrop Grumman Corporation (the U.S.)

- ASELSAN A.S. (Turkey)

- Thales Group (France)

- Israel Aerospace Industries (IAI) (Israel)

- Rafael Advanced Defense Systems Ltd. (Israel)

- L3Harris Technologies (the U.S)

- MOOG Inc. (the U.S.)

- Ultra Electronics Holdings (U.K.)

- FLIR Systems (the U.S.)

- BAE Systems plc. (U.K)

- General Dynamics Corporation (the U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2024 – Lockheed Martin Corporation has been awarded a contract worth USD 90.68 million through U.S. Foreign Military Sale for Poland to receive Sniper Advanced Targeting systems (ATS), which will be integrated into FA-50 and Polish F-16 aircraft.

- May 2024 – Lockheed Martin Corporation and Boeing Company has been awarded a contract worth USD 80 million with Malaysian government to procure 10 AN/AAQ-33 Sniper Advanced Targeting systems for Malaysian F/A18D platforms.

- October 2020, the U.S. Navy awarded FLIR Systems contract worth 14.56 million to provide BRITE Star II electro-optical targeting avionics. The BRITE Star II multi-sensors provide intelligence, surveillance, reconnaissance, and target identification for manned and unmanned aircraft.

- May 2020, the U.S. Air Force awarded Lockheed Martin Corp. a contract worth USD 485 million for building new versions of legacy electro-optical combat jet target systems for U.S. allies under terms.

- December 2022, A Lockheed Martin was awarded a seven-year, USD 225.8 million contract to assist the U.S. Air Force in keeping an electro-optical targeting system employed by military aircraft in good working order. The Sniper Comprehensive Advanced Targeting Pod sustainment program includes support services to monitor system availability and reliability between maintenance cycles.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on important aspects, such as key players, products, applications, and platforms depending on various countries. Moreover, it offers deep insights into the market trends, competitive landscape, market competition, pricing of, and market status and highlights key industry developments. In addition, it encompasses several direct and indirect factors that have contributed to the expansion of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.10% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type

|

|

By Component

|

|

|

By Platform

|

|

|

By Fit

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 2709.6 million in 2025 and is anticipated to be USD 3,907.80 million by 2034.

The market will likely grow at a CAGR of 4.10% over the forecast period.

The top players in the industry are Lockheed Martin Corporation, Teledyne FLIR LLC, RTX Corporation, Northrop Grumman Corporation, ASELSAN A.S., Raytheon Technologies, Thales Group, Israel Aerospace Industries (IAI), Rafael Advanced Defense Systems Ltd., L3Harris Technologies.

North America dominated the global targeting pod market report in 2025, with USD 954.32 million, and is anticipated to dominate the market again, estimated to reach USD 1277.3 million by 2032.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us