Situational Awareness Market Size, Share & Industry Analysis, By Product Type (Command & Control (C2), Surveillance & Tracking Systems, Detection, Identification & Classification Systems, and Others), By Technology (Radio Frequency (RF), Electro-Optical / Infrared (EO/IR), and Others), By Platform (Ground (Fixed, Mobile/Deployable, and Portable/Man-portable), Airborne, Naval, and Space), By Component (Sensors, Navigation & Positioning Systems (PNT/GNSS), Cameras, Software, and Others), By End-User (Army, Navy, Air Force, Aviation Authorities, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

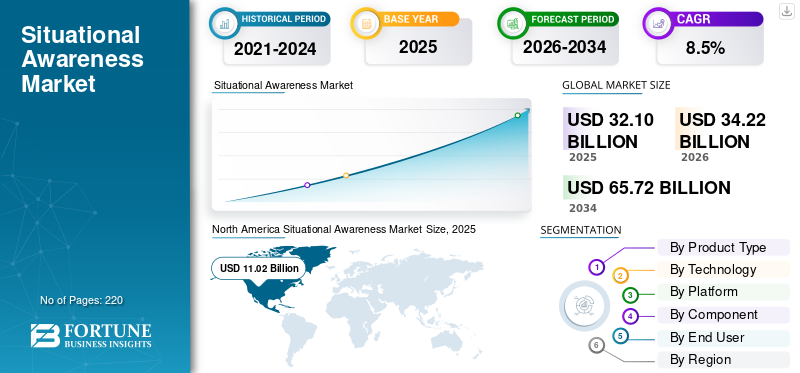

The global situational awareness market size was valued at USD 32.10 billion in 2025. The market is projected to grow from USD 34.22 billion in 2026 to USD 65.72 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period. North America dominated the situational awareness market with a market share of 34.33% in 2025.

The situational awareness market is witnessing strong growth, driven by increasing geopolitical tensions, surging investments in border and maritime security, and the rapid integration of unmanned systems across aerospace, defense, homeland security, and maritime domains. These systems leverage AI-driven sensor fusion, advanced radar/EO/IR networks, IoT-enabled command-and-control platforms, and real-time analytics to provide comprehensive battlefield pictures, enhancing threat detection and decision-making.

- For instance, in April 2025, Thales was selected by NATO for phase 3 of the NCOP (NATO Common Operational Picture) program, dubbed “NCOP-BMD,” valued at hundreds of millions to equip command centers with unified real-time threat landscapes for joint forces.

Prominent players such as Thales Group, Raytheon Technologies, Lockheed Martin, L3Harris Technologies, and Northrop Grumman are advancing innovations such as multi-spectral sensor fusion for contested environments, quantum-secure data links for space/maritime domains.

Download Free sample to learn more about this report.

Situational Awareness Market Key Takeaways

- 2025 Market Size: USD 32.10 billion

- 2026 Market Size: USD 34.22 billion

- 2034 Forecast Market Size: USD 65.72 billion

- CAGR: 8.5% from 2026–2034

- North America dominated the situational awareness market with a 34.33% share in 2025.

- The surveillance & tracking systems segment held the largest market share.

- The ground platform segment accounted for the largest market share.

North America

North America generated USD 11.05 billion in 2025 and is projected to reach USD 11.70 billion in 2026.

Europe

Europe is projected to grow at a CAGR of 8.9% during the forecast period.

Asia Pacific

Asia Pacific emerged as the second-largest regional market in 2025.

U.S

The U.S. situational awareness market was valued at USD 9.77 billion in 2025.

Japan

The Japan situational awareness market was valued at USD 1.09 billion in 2025.

Read More

SITUATIONAL AWARENESS MARKET TRENDS

Shift Toward AI-Enhanced Sensor Fusion and Edge AI Processing is a Prominent Market Trend

The shift toward AI-enhanced sensor fusion and edge AI processing is accelerating in situational awareness systems for aerospace, defense, aviation, and maritime security, propelled by needs for real-time multi-domain integration, reduced latency, and resilient operations in contested environments. Public safety drives market demand as cities deploy fused sensor networks for real-time incident response, like counter-drone tech along borders. These technologies combine data from radar, EO/IR, hyperspectral sensors, and IoT networks using AI algorithms for automated threat classification, predictive analytics, and fused common operational pictures (COP). Moreover, military forces are focused on the evolution of sensor fusion technology for improving accuracy in low-visibility scenarios, countering jamming/stealth threats, and supporting swarming UAVs, naval patrols, and air traffic management during rising multi-domain warfare demands.

- For instance, in February 2025, QinetiQ US received a USD 42 million, four-year task order from the US Army Combat Capabilities Development Command C5ISR Center to develop embedded intelligent sensor processing and advanced imaging technologies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rise in Defense Budgets and C4ISR Modernization is Expected to Drive Market Growth

A primary driver for the situational awareness market is the global surge in defense budgets, coupled with accelerated investments in C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) modernization across aerospace, defense, aviation, and maritime security sectors.

- For instance, according to the Stockholm International Peace Research Institute (SIPRI), worldwide military expenditure hit USD 2.44 trillion in 2024, up 6.8% from 2023. Moreover, the U.S. Department of Defense awarded Thales USD 150 million in 2025 under a multi-year initiative to upgrade NATO's NCOP-BMD system, enhancing real-time fused sensor data for joint operations in air, sea, and space domains. This bolsters resilient supply chains for advanced processors and multi-spectral arrays.

Such defense spending and investment propel demand for AI-driven situational awareness systems featuring sensor fusion platforms, edge analytics, and secure data links for contested environments. Access control systems integrate with situational awareness platforms to manage secure entry in defense facilities. As forces pursue multi-domain superiority, deploying networked UAV swarms, maritime patrol vessels, and air defense grids, there's a rise in the need for low-latency, resilient solutions to deliver persistent monitoring.

MARKET RESTRAINTS

High Development and Integration Costs to Limit the Market Expansion

High development and integration costs pose a significant restraint for situational awareness systems, as advanced AI-driven sensor fusion, quantum-secure networks, and multi-domain platforms demand substantial R&D investments. Cybersecurity vulnerabilities further hamper adoption, with rising threats of jamming, spoofing, and hacking targeting networked C4ISR systems in contested environments, necessitating continuous and expensive countermeasures. Ongoing maintenance, cybersecurity upgrades, and lifecycle sustainment further burden budgets. These high costs deter smaller defense budgets or emerging players, which is anticipated to slow market penetration and hamper the situational awareness market growth.

MARKET OPPORTUNITIES

Expansion of Unmanned Systems and Swarm Operations Presents Market Growth Opportunities

The expansion of unmanned systems and swarm operations is creating demand for advanced situational awareness solutions that enable coordinated control, collision avoidance, and real-time threat assessment across distributed assets.

- For instance, in June 2025, Northrop Grumman announced flight testing of its latest MQ-4C Triton unmanned ISR aircraft at Palmdale, CA, for U.S. Navy calibration ahead of operational transfer, bolstering maritime surveillance.

Swarm-capable systems incorporate decentralized edge computing, low-latency mesh networks, and multi-spectral sensor arrays compatible with UGVs, USVs, and high-altitude drones. Such advancements accelerate the adoption of resilient, scalable awareness platforms, presenting lucrative opportunities for market growth.

- For instance, in June 2025, Kongsberg Geospatial and FireSwarm Solutions signed an MOU to integrate IRIS Terminal situational awareness software with autonomous drone swarms, enhancing real-time wildfire detection, suppression, and disaster response capabilities.

MARKET CHALLENGES

Interoperability Challenges Across Legacy and Modern Platforms Act as a Market Challenge

An important market challenge is the lack of seamless interoperability between legacy systems and next-generation multi-domain platforms in aerospace, defense, aviation, and maritime security. Many forces rely on disparate sensors, protocols, and data formats from legacy systems. This issue delays unified common operational pictures (COP), increases integration costs, and exposes vulnerabilities in coalition environments. These factors are expected to create challenges for the growth of the market.

Segmentation Analysis

By Product Type

Real-Time Threat Detection Demand to Propel Surveillance & Tracking Systems Segmental Growth

Based on the product type, the market is divided into command & control (C2) / common operating picture (COP) systems, surveillance & tracking systems, detection, identification & classification systems, decision support & threat assessment systems, counter-UAS situational awareness systems, and others.

The surveillance & tracking systems segment is anticipated to account for the largest situational awareness market share. Growing demand for real-time threat detection is driving the market segment. These systems integrate sensors such as radar, EO/IR cameras, and acoustic detectors with AI analytics to fuse multi-domain data. Moreover, military and naval forces are procuring situational awareness systems for real-time tracking and command capabilities & boost situational awareness and rapid threat response for logistics operations.

- For instance, in February 2026, Raytheon secured a DARPA contract to develop an advanced EO/IR sensor and targeting system under the Pulling Guard program, enhancing protection for commercial and naval vessels against unmanned surface vehicles.

The counter-UAS situational awareness systems segment is anticipated to rise with a steady growth rate, with a CAGR of 10.3% over the forecast period.

By Technology

Radar and Communication Advancements Enabling Persistent Monitoring to Propel Radio Frequency (RF) Segmental Growth

By technology, the market is segmented into radio frequency (RF), electro-optical / infrared (EO/IR), acoustic / sonar, GNSS / PNT, and others.

The radio frequency (RF) based segment is anticipated to account for the largest market share. The segment in the situational awareness industry grows due to its critical role in radar and communication technologies that enable real-time threat detection and tracking. Advancements in software-defined radios enhance flexibility, allowing dynamic frequency adaptation for diverse environments such as defense and aerospace operations.

- For instance, in July 2025, Spire Global launched new radio frequency geospatial intelligence products for its Space Reconnaissance portfolio, providing persistent monitoring, real-time geolocation, and enhanced situational awareness across VHF, UHF, and L bands. Such developments provide persistent maritime and terrestrial monitoring, enabling threat tracking and driving segment growth.

The electro-optical / infrared (EO/IR) based segment is projected to grow at a steady annual growth rate (CAGR) of 9.5% over the forecast period.

By Platform

Multi-Layered Sensor Fusion into C5ISR Pushes the Ground Segment’s Growth

Based on the platform, the market is categorized into ground, airborne, naval, and space.

Ground accounted for the largest market share of the industry due to its central role in processing and distributing real-time data from aerial, naval, and space-based sensors. Key players are developing systems for ground platforms that fuse inputs from radars, cameras, and IoT devices into unified operational views for defense forces. Moreover, an increase in the integration of multi-layered situational awareness systems with existing C5ISR platforms is expected to drive the segment growth during the forecast period.

The space segment is expected to grow at the fastest rate of CAGR of 10.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Miniaturization and Multi-Spectral Fusion Support Sensors Segment Growth

Based on component, the market is segmented into sensors, navigation & positioning systems (PNT/GNSS), cameras, software, and others.

The sensors segment held the largest share of the market in 2025. The sensors segment grows through its foundational role in capturing real-time environmental data across defense and security applications. Miniaturization and multispectral fusion are allowing sensors seamless integration of surveillance systems into drones, vehicles, and wearables for enhanced threat identification. In addition, there is a surge in the demand for sensors for passive detection during stealth threats and EW dominance.

- For instance, in February 2026, Lockheed Martin secured a U.S. Foreign Military Sales contract to supply IRST21 Legion-ES infrared search-and-track sensors for Taiwan's F-16 fighters. The long-wave infrared systems enable passive detection and extended-range tracking of airborne threats, enhancing aircrew situational awareness in contested environments.

The software segment is projected to emerge as the fastest-growing at a CAGR of 9.7% over the forecast period.

By End User

Rising Budgets and Dismounted Soldier Modernization Fuel Army Segment Growth

Based on end user, the market is segmented into army, navy, air force/space force, aviation authorities, port/ maritime authorities, and others.

The army segment held the highest market share in 2025. The factors contributing to segment growth are a rise in defense budget and an increase in investment in robust situational awareness systems tailored for land-based operations in dynamic combat environments. Moreover, modernization programs drive the adoption of dismounted soldier systems with integrated sensors for enhanced threat detection and coordination, which propels the segment growth.

- For instance, in August 2025, the U.S. Army prototyped the Spectrum Situational Awareness System (S2AS) through PEO IEW&S and industry partners to detect, identify, and decode electromagnetic spectrum signals in contested battlefields. Soldiers are rigorously testing prototypes in exercises through FY2025-2026, with plans to field 10-15 initial units to Transformation in Contact forces by year-end.

The aviation authorities segment is projected to grow with a steady growth rate at a CAGR of 10.8% over the forecast period.

Situational Awareness Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Situational Awareness Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the situational awareness market in 2025 with a valuation of USD 11.05 billion, expected to hit USD 11.70 billion in 2026, driven by increasing defense investments in networked C4ISR systems, due to demands for multi-domain operations and real-time threat visualization.

U.S Situational Awareness Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 9.77 billion in 2025. High defense allocations support upgrades in sensor fusion and AI-driven analytics for radars, EO/IR systems, and command centers, enhancing decision-making in contested environments. The U.S. military advances awareness capabilities by adopting resilient platforms to overcome electronic warfare challenges and data overload. In addition, the defense sector in the U.S. constantly invests heavily in research and development of next-gen technologies, which drives market growth in the country.

- For instance, in December 2025, the U.S. Army adopted DroneArmor, Parsons Corporation's AI-driven C-UAS platform, featuring multi-sensor fusion to detect, track, and neutralize rogue drones along the southern border, delivering real-time situational awareness.

Europe

Europe is projected to record a growth rate of 8.9% during the forecast period, which is the second highest among all regions. The market in the region grows due to security demands from counter-terrorism, military modernization, and NATO interoperability missions. The market expands due to investments in advanced sensors, C4ISR platforms, and AI analytics for real-time threat detection across land, air, and maritime domains. Countries such as the UK, France, and Germany invest heavily in resilient situational awareness systems for networked soldier displays, UAV swarms, and command centers. In addition, defense forces, including the navy, are integrating a strategic situational awareness system for rapid threat response.

- For instance, in December 2025, BAE Systems secured a USD 36 million deal from Lockheed Martin to supply Multifunction Modular Mast (MMM) antennas for U.S. Navy Virginia-class submarines, enabling stealthy detection and direction-finding of adversary signals via integration with the AN/BLQ-10 EW system.

U.K Situational Awareness Market

The U.K. market in 2025 was valued at USD 1.51 billion, representing roughly 4.7% of global revenues.

Germany Situational Awareness Market

The Germany market reached approximately USD 2.05 billion in 2025, equivalent to around 6.4% of global sales.

Asia Pacific

The Asia Pacific market reached USD 0.58 billion in 2025 and secured the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 0.02 billion and USD 0.35 billion, respectively, in 2025. The Asia Pacific market grows rapidly due to heavy investments in advanced C4ISR systems, sensor fusion, and AI analytics for UAV swarms, naval surveillance, and soldier-portable displays during regional geopolitical challenges. Countries such as India, China, and South Korea prioritize resilient radar networks, EO/IR upgrades, and networked command platforms for extended-range drones.

Japan Situational Awareness Market

The Japanese market in 2025 hit USD 1.09 billion, accounting for roughly 3.4% of global revenues.

China Situational Awareness Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues at USD 2.94 billion, representing roughly 9.2% of global sales.

India Situational Awareness Market

The Indian market in 2025 was valued at USD 1.53 billion, accounting for roughly 4.8% of global revenues.

Latin America and the Middle East & Africa

Latin America exhibits steady market growth during the forecast period, supported by defense modernization efforts and peacekeeping operations across Brazil, Colombia, and Chile. The Latin America market reached a valuation of USD 3.17 billion in 2025. The market in Latin America grows rapidly due to investments in urban surveillance networks, counter-narcotics sensors, and mobile C4ISR for jungle and coastal operations. Countries such as Brazil, Mexico, and Colombia prioritize radar upgrades, EO/IR drones, and command integration to combat organized crime and enhance regional sovereignty. In addition, the Middle East & Africa market expands due to heavy investments in border surveillance radars, counter-drone systems, and AI analytics during geopolitical tensions.

Saudi Arabia Situational Awareness Market

The Saudi Arabian market reached around USD 0.40 billion in 2025, representing roughly 0.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on AI-Enhanced Sensors and C4ISR Platforms by Key Players to Propel Market Progress

The global situational awareness market remains consolidated, led by major players such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, Thales Group, BAE Systems, and L3Harris Technologies, which command significant shares through innovations in multi-spectral sensor fusion and resilient EMS processing systems. These firms advance market growth with strategic contracts from defense agencies and OEM partnerships, emphasizing development of AI-driven analytics, networked soldier displays, and software-defined radars for UAV swarms, command centers, and multi-domain operations across various platforms.

- For instance, in May 2025, Raytheon was selected by DARPA for the Pulling Guard program to develop EO/IR sensors on tethered drones for towed unmanned platforms, protecting commercial and naval vessels from USV threats with enhanced situational awareness.

Other prominent players such as Elbit Systems, Leonardo S.p.A., and General Dynamics focus on scalable production of edge-computing modules, counter-drone awareness networks, and extreme-environment sensor solutions.

LIST OF KEY SITUATIONAL AWARENESS COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Raytheon Technologies Corporation (U.S.)

- BAE Systems (U.K)

- L3Harris Technologies (U.S.)

- Thales (France)

- Saab (Sweden)

- Leonardo (Italy)

- Airbus (Netherlands)

- Indra Sistemas (Spain)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Qatar Civil Aviation Authority awarded Bayanat Engineering a contract for Frequentis' next-generation display system, unifying weather, runway, aerodrome, and support data into one real-time interface for controllers.

- October 2025: Thales launches Aurore, Europe's largest ground-based radar under France's ARES program, to track satellites and debris in Low-Earth orbit for enhanced space situational awareness.

- October 2025: Indian Air Force develops Unified Situational Awareness System (USAS) via indigenous VAYULINK tactical data-link, creating secure real-time networks linking aircraft, helicopters, UAVs, and ground units to boost battlefield intelligence.

- September 2025: V2X wins a USD 72 million deal to upgrade the Army's Gateway Mission Router, delivering cyber-hardened connectivity that fuses air-to-ground data for unified situational awareness and faster C4ISR decisions. The system supports DoD's multi-domain command initiative through 2030, building on prior USD 49M award with enhanced processing at reduced SWaP for aviation and ground platforms.

- September 2025: KBR secures three USD 175 million task orders from Air Force Research Laboratory under INCITE COPERS for multi-domain, space situational awareness, and trusted microelectronics technologies over five years.

- April 2025: Thales secured a contract for NATO's NCOP phase 3 (NCOP-BMD), delivering unified real-time operational pictures and ballistic missile defense awareness to enhance joint forces' decision superiority.

- January 2025: Northrop Grumman secures contract to equip Royal Australian Air Force C-130J fleet with AN/ALQ-251 advanced radio frequency countermeasures system for protection against sophisticated threats. The system delivers full situational awareness, radar warnings, and precise RF threat direction finding.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By Technology, By Platform, By Component, By End User, and Region |

| By Product Type |

|

| By Technology |

|

| By Platform |

|

| By Component |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 32.10 billion in 2025 and is projected to reach USD 65.72 billion by 2034.

In 2025, the market value stood at USD 11.02 billion.

The market is expected to exhibit a CAGR of 8.5% during the forecast period.

By platform, the ground segment is expected to lead the market.

The rise in defense budget and C4ISR modernization is driving market expansion.

Lockheed Martin (U.S.), Northrop Grumman (U.S.), Raytheon Technologies Corporation (U.S.), and BAE Systems (U.K), among others, are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us