Ballistic Missiles Market Size, Share & Industry Analysis, By Missile Type (Land-Attack (LABM), Anti-Ship (AShBM), and Air-Launched (ALBM)), By Component (Guidance Systems, Propulsion Systems, Warheads, Missile Airframes, Sensors & Seekers, and Communication Systems), By Missile Speed (Subsonic ,Supersonic and Hypersonic (Above Mach 5)), By Launch Platform, By Missile Range, Short Range, Medium Range ,Intermediate Range (3,500 - 5,500 km), and Intercontinental Range (Above 5,500 km)), By Propulsion System (Solid Propellant and Liquid Propellant), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

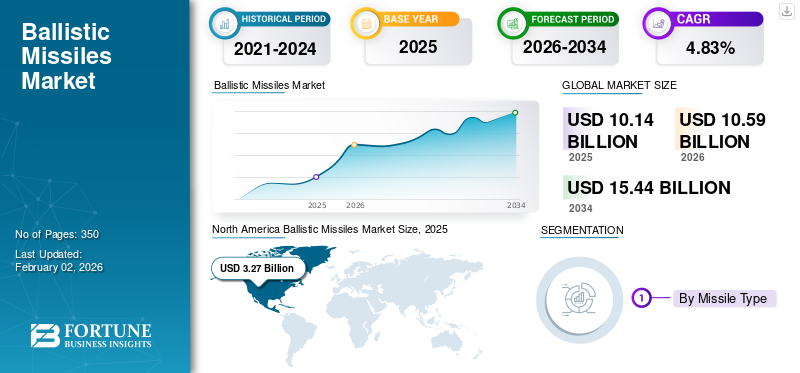

The global ballistic missiles market size was valued at USD 10.14 billion in 2025. It is projected to grow from USD 10.59 billion in 2026 to USD 15.44 billion by 2034, exhibiting a CAGR of 4.83% over the forecast period. North America dominated the ballistic missiles market with a market share of 32.28% in 2025.

A ballistic missile is a guided, rocket-propelled weapon system designed to deliver conventional, nuclear, chemical, biological, or other warheads to a predetermined target by following a primarily ballistic (free-fall) trajectory. This is governed by the laws of orbital mechanics and gravity after an initial powered boost phase. The ballistic missiles market includes RDT&E (Research, Development, Testing and Evaluation), production, procurement, and modernization (PPM), operation, maintenance, and associated support services for ballistic missile programs.

The global ballistic missiles market share is set for sustained and technology-driven growth over the next two decades, shaped by geopolitical competition and declining arms control frameworks. Demand for this product is higher among major powers (the U.S., Russia, China and others) that are modernizing strategically and regional powers (India, Pakistan, North Korea, Iran, and selective Middle Eastern and Northeast Asian states) which are seeking credible deterrence against perceived threats.

This market expansion is further fueled by tensions arising from Russia's invasion of Ukraine, China's assertive stance in the Indo-Pacific situation, instability in the Middle East, and the nuclear ambitions of North Korea and Iran. Investments in the market are focused on survivable second-strike capabilities (such as SSBNs and mobile launchers), enhanced counterforce accuracy, and extended range for global or regional power projection. Increased spending on missile defense systems, such as the U.S. Ground-based Midcourse Defense (GMD), Aegis Ballistic Missile Defense (BMD), Terminal High Altitude Area Defense (THAAD), and Patriot PAC-3/4, along with Russian, Chinese, Indian, and Israeli counterparts, creates a dynamic offense-defense spiral.

Technological advancements are catalyzing the market evolution. Hypersonic glide vehicles (HGVs) and cruise missiles are shifting from development to deployment, particularly by the U.S., Russia, and China, driving R&D and procurement budgets. Miniaturization of warheads, improved propulsion efficiency, sophisticated penetration aids (such as decoys and jammers), and Multiple Independently Targetable Reentry Vehicles (MIRVs) are also improving the lethality and survivability.

Artificial intelligence and advanced command and control integration are vital for rapid decision-making, targeting, and battle management. The market will continue as an oligopoly featuring state-owned giants such as Russia's Roscosmos/Makeyev and China's CASIC/CALT, alongside major Western firms such as Lockheed Martin, Northrop Grumman, and Raytheon in the U.S.; MBDA in Europe is predicted to consolidate tier-2/3 suppliers for critical subsystems. While niche players may emerge in specific technologies, complete systems face high entry barriers due to complexity and cost.

The long-term trajectory indicates a complex and volatile strategic landscape, featuring advanced ballistic and hypersonic capabilities that integrate conventional and nuclear strike options. This situation is particularly risky for China's DF-26 IRBM and Russia's Iskander systems, which may lead to lower decision-making thresholds and increased crisis instability. Arms control agreements are unlikely to restrain development or deployment, resulting in ongoing arms races.

Furthermore, the market’s growth is expected to be geographically uneven, with Asia Pacific taking the lead due to the China-U.S. strategic competition and regional issues involving India, Pakistan, and North Korea, followed by the Middle East as well as notable investments on modernization in North America and Europe. Ultimately, the ballistic missiles market will continue to serve as a critical barometer of geopolitical tension, influencing defense budgets and the strategic calculations of nations in future.

Major companies operating in this market include Lockheed Martin, Boeing, Northrop Grumman, and Raytheon in the U.S., which are developing advanced missile systems and related technologies. Internationally, organizations such as China Aerospace Science and Technology Corporation (CASC) and India’s Defence Research and Development Organisation (DRDO) also play a significant role in these missile development. The evolution of the market reflects ongoing global security concerns, innovative advancements, and strategic military modernization efforts, making ballistic missiles a fundamental component of national defense resources globally.

Download Free sample to learn more about this report.

Ballistic Missiles Market Key Takeaways

- 2025 Market Size: USD 10.14 billion

- 2026 Market Size: USD 10.59 billion

- 2034 Forecast Market Size: USD 15.44 billion

- CAGR: 4.83% from 2026–2034

- North America dominated the ballistic missiles market with a 32.28% share in 2025.

- Land-Attack (LABM) segment is expected to hold a 66.33% market share in 2026.

- Ground-based systems segment is expected to lead with a 71.03% market share in 2026.

North America

North America accounted for USD 3.27 billion in 2025, representing 32.28% of the global market.

Europe

Europe reached USD 3.05 billion in 2025, capturing 30.08% of the global market share.

Asia Pacific

Asia Pacific recorded USD 1.96 billion in 2025, contributing 19.36% of global revenue.

U.S.

The U.S. ballistic missiles market is projected to reach USD 3.15 billion in 2026, driven by strategic deterrence and modernization programs.

Japan

Japan’s ballistic missiles market is projected to reach USD 0.05 billion in 2026, supported by regional security investments and defense modernization.

Read More

Market Dynamics

Market Drivers

Escalating Arms Rivalry, Regional Instability, and Security Threats to Drive Market Growth

The escalating arms conflict, regional instability, and security threats are directly fueling global demand for advanced ballistic missiles and defense systems. Countries perceive growing risks from competitors, such as China's hypersonic missiles, Russia's ICBM (Intercontinental Ballistic Missile) deployments, and regional conflicts including Houthi attacks and the Ukraine war, which expose capability gaps. This drives ongoing investments in credible deterrence through next-generation missiles, hypersonics, and integrated air/missile defense (IAMD) systems to counter emerging such threats.

The market is responding with a surge in contracts, collaborations, and technological breakthroughs. Major developments for 2023–2024 include Germany’s USD 4.3 billion Arrow-3 purchase in November 2023, Northrop Grumman’s USD 3.9 billion Sentinel ICBM contract in January 2024, and Lockheed-Rocket Lab hypersonic partnerships in May 2024. Testing milestones, such as India’s MIRV-capable Agni-V in March 2024 and France’s M51.3 SLBM in November 2023, further accelerated modernization. Alliances including AUKUS (hypersonic R&D in April 2024) and NATO initiatives pool funds to address shared threats.

This growth cycle is self-perpetuating due to three dynamics: technological breakthroughs, such as hypersonics and MIRVs, by one country trigger rival investments; alliance frameworks including NATO, AUKUS, and QUAD institutionalize shared spending; and defense contractors reinvest profits into R&D, which reduces costs and allows for broader adoption. With no diplomatic off-ramps in sight, evidenced by North Korea’s solid-fuel ICBM tests (2023–2024) and the global defense budget surge, the ballistic missile market will continue to expand as deterrence becomes inseparable from geopolitical survival.

Advancing Adversary Missile & Missile Defense Capabilities to Compel Investment in Countermeasures and Enhanced Lethality

Russia, China, North Korea, and Iran are aggressively developing missile capabilities to overcome existing defenses and project power. Key advancements include hypersonic glide vehicles including Russia's Kinzhal and China's DF-17, maneuverable re-entry vehicles, MIRVs, solid-fuel ICBMs such as North Korea's Hwasong-18, and advanced penetration aids, including decoys and jamming systems. These developments, demonstrated through extensive testing and combat use in Ukraine and against shipping, aim to overpower or bypass missile defenses, creating a pressing perception of vulnerability among threatened states. This situation directly prompts counter-investment by Western bloc countries and NATO member states.

Western bloc countries responded by significantly scaling and enhancing missile defense systems. Recent developments include a USD 4.2 billion THAAD interceptor contract awarded to Lockheed Martin in March 2024, a potential USD 2.2 billion Patriot PAC-3 MSE sale to Germany in April 2024, USD 419 million SM-3 production award to RTX (Raytheon Technologies Corporation) in May 2024, and critical design approval for the USD 100+ billion Sentinel ICBM program in January 2024. Next-generation systems including the Glide Phase Interceptor (GPI) targeting hypersonics received USD 75 million in development awards in February 2024. Furthermore, adversaries observe these enhancements and invest in countermeasures, such as advanced decoys, FOBS, and swarming drones, restarting the cycle. These developments drive exponential ballistic missiles market growth.

- Massive Production: Significant investments in contracts for interceptors (THAAD, Patriot, SM-3) and offensive missiles, including USD 756 million for Lockheed's LRHW hypersonic in February 2024.

- Technological Innovation: R&D surges for next-gen capabilities, such as GPI (Glide Phase Interceptor) and directed energy systems such as the RTX-Rafael Iron Beam laser Joint Venture announced in May 2024.

- Industrial Consolidation and Collaboration: Vertical integration, exemplified by Raytheon Technologies Corporation's USD 5.2 billion acquisition of Aerojet Rocketdyne in April 2024, multinational partnerships including the 21-nation European Sky Shield Initiative, which has been expanding since May 2024, and AUKUS Pillar II hypersonic cooperation, group resources, and expertise.

Geopolitical tensions and the inherent security dilemma ensure this cycle remains the primary engine for sustained market expansion across offensive and defensive domains.

Market Restraints

Stringent International Arms Control Regimes and Export Restrictions to Hinder Technology Transfer and Market Access

Stringent international regimes including the MTCR, Wassenaar Arrangement, and country-specific sanctions deliberately suppress ballistic missile market growth by restricting technology transfer and market access. This is achieved through comprehensive control lists targeting dual-use technologies, such as advanced materials, propulsion, and guidance systems, along with "catch-all" clauses, which block the flow of critical expertise and components essential for missile development or upgrades. Consequently, complex licensing requirements, restrictions on Iran, North Korea, and Russia, and burdensome end-use monitoring fragments the addressable market, largely confining legal trade to established military alliances including NATO and key U.S. allies while isolating other potential buyers.

These restrictions impose substantial compliance costs and operational burdens, driving industry consolidation and restructuring supply chains. Recent developments include MBDA's acquisition of HTS Group in June 2024 secured sensitive microelectronics within an EU supply chain for programs such as FC/ASW, while Lockheed Martin's reshoring initiatives (August 2023-February 2024) relocated rocket motor production to the U.S. and allies to mitigate sanctions risk. Sanctions on Russian titanium since April 2024 have disrupted global aerospace supply chains, necessitating costly requalification of alternative sources. Significant collaborations, such as Northrop Grumman-Raytheon's GBSD integration in April 2024 and MBDA/Eurosam's SAMP/T NG contract in March 2024, are partially driven by the need to navigate complex controlled supply chains within trusted regulatory blocs.

The regimes fundamentally redirect R&D investment and collaboration into narrow, alliance-based silos, restricting broader market innovation and globalization. Hypersonic development exemplifies this, with sensitive R&D confined to trusted groups such as the U.S.-Australia SCIFiRE program since November 2023 and the U.K./Italy/Japan GCAP, as open international collaboration is unfeasible under current controls.

Consequently, the market grows within heavily regulated segments among established players, while overall expansion is stifled. Investment is diverted from pure market growth toward compliance and secure supply chains, and consolidation increases barriers to entry, leaving non-alliance states with underdeveloped indigenous programs or a reliance on illicit networks. These adaptations confirm the regimes' success in deliberately constraining the organic growth and globalization of the ballistic missile market.

Highly Prohibitive Development & Lifecycle Costs to Limit Procurement Scale and Market Growth

The high upfront R&D investment required for modern ballistic missiles, encompassing advanced propulsion, materials, guidance, and rigorous testing, creates an extremely high barrier to entry and scale. Major powers, such as the U.S., Russia, China, France, U.K., and India can sustain indigenous programs, as evidenced by the extreme cost overruns in projects including the U.S. GBSD (LGM-35A Sentinel), which triggered a Nunn-McCurdy breach in January 2024, with total lifecycle estimates exceeding USD 130-160 billion. These massive R&D costs must be recouped over production runs, driving per-unit prices excessively high and forcing nations to procure minimal quantities, transforming programs into economically constrained capabilities rather than scalable resources.

Lifecycle costs comprise decades of maintenance, specialized infrastructure such as silos and SSBNs, regular multi-million-dollar flight tests, continuous upgrades, and highly skilled personnel that dwarf initial procurement outlays and impose severe long-term fiscal burdens. This is starkly demonstrated by the U.K.'s Dreadnought SSBN program in the 2023 MoD report (approximately GBP 31 billion for 4 subs, excluding missiles and warheads) and the GBSD's 50-year cost profile.

These recurring expenses compel nations to make tough trade-offs: prioritizing the maintenance of existing systems over new procurement, restricting fleet sizes to minimal credible deterrent levels, such as India's modest Agni-V orders from 2023 to 2024, and postponing modernization. The outcome is a procurement landscape where lifecycle affordability determines scale, rather than capability need.

It serves primarily as strategic deterrents, where small, survivable arsenals serve, contradicting Cold War-scale expansion. Simultaneously, their immense costs create unsustainable opportunity expenditures, diverting resources from conventional forces and competing priorities, exacerbated by budget pressures and the availability of cheaper precision-strike alternatives, such as BrahMos JV expansion in March 2023, US PrSM production during 2023-2024. Market developments showcase the market consolidation, such as L3Harris acquiring Aerojet Rocketdyne in July 2023, which focuses on efficiency in a niche sector, while new entrants remain rare and partnerships, such as Franco-German MGCS between 2023-2024, avoid ballistic systems. Consequently, the market is capped to a handful of countries pursuing nuclear deterrence, with growth fundamentally limited by this prohibitive cost ceiling.

Market Opportunities

Integration of AI and Advanced C5ISR to Create Demand for Next-Generation Battlefield Management and Decision Support Systems

Integrating artificial intelligence (AI) with C5ISR networks revolutionizes military decision-making by enabling real-time data fusion, predictive threat analysis, and automated resource allocation. This has created an urgent need for next-generation Battlefield Management Systems (BMS) and Decision Support Systems (DSS) capable of processing AI-accelerated sensor data into actionable insights. Recent developments underscore this shift: the US Army’s USD 450 million award to BAE Systems in May 2024 for the AI-powered TITAN targeting system, Lockheed Martin’s USD 4.5 billion JADC2 contract in March 2024 for all-domain command infrastructure, and Anduril’s acquisition of Blue Force Technologies in January 2024 to enhance autonomous BMS capabilities. These investments aim to compress the "sensor-to-shooter" timeline to near-instantaneous response, a capability critical for modern multi-domain warfare.

Rising ballistic missiles system capabilities are fueling growth of the global market, as advanced C5ISR architectures reveal gaps in countering next-generation threats, particularly hypersonic and maneuverable missiles. Countries are simultaneously investing in offensive missiles for restriction and integrated defense systems for protection, creating a self-reinforcing cycle. Key developments include Lockheed Martin’s USD 2.3 billion hypersonic LRHW award in March 2024, Northrop Grumman’s USD 3.9 billion Next-Gen Interceptor contract in October 2023, and AUKUS Pillar II collaborations in April 2024 on hypersonic countermeasures. Strategic consolidation, such as L3Harris’ USD 4.7 billion acquisition of Aerojet Rocketdyne in January 2024, further integrates propulsion and guidance technologies vital for missile innovation.

The AI-C5ISR-BMS triad and evolving missile threats are interdependent sectors projected for robust growth. It is accelerated by real-world validation in Ukraine (drone/C5ISR warfare), Gaza (ballistic missile intercepts), and Indo-Pacific tensions (China’s DF-17, India’s Agni-V). Commercial technologies, including edge computing, such as the RTX-Red 6 AR training partnership established in April 2024 and AI-hardened systems, are reducing costs and enhancing performance. This resulted in a global rearmament cycle that prioritizes integrated deterrence, where AI-driven battlefield awareness necessitates faster, smarter missiles and vice versa, ensuring sustained defense expenditure by 2032.

Development of Hypersonics and Counter-Hypersonic Systems to Stimulate Investment in Next-Generation RDT&E and Procurement Opportunities

The operational deployment of hypersonic weapons by opponents such as Russia's Kinzhal and China's DF-17 has triggered a global arms race, creating a capability gap for the U.S. and its allies (NATO, AUKUS, Japan). This imperative drives massive, sustained investment in next-generation RDT&E to overcome profound technological challenges. Hypersonic systems demand breakthroughs in materials science for thermal management at 2000°C and above, propulsion systems such as scramjets, advanced boost-glide, and AI-driven guidance for maneuverable flight in challenging environments. Simultaneously, counter-hypersonic systems require entirely new sensor architectures, including space-based HBTSS, resilient OTH radars, high-velocity interceptors including GPI, and AI-enabled battle management. The U.S. budget request exceeding USD 11 billion for hypersonics, demonstrates RDT&E surge, mirrored by allied nations including Japan (Hyplex testing) and Australia (SCIFiRE program).

This RDT&E wave directly stimulates next-generation procurement cycles for offensive hypersonic systems, including the U.S. Army's LRHW, USAF's HACM - Raytheon USD 985 million contract in September 2023, and integrated counter-hypersonic architectures. The technological spillover benefits the broader ballistic missile market including advances in propulsion, lightweight materials, and sensors enhance conventional ballistic and cruise missiles. Counter-hypersonic efforts also require upgrades and new procurement avenues for existing BMD systems such as Aegis, THAAD, and Patriot, as demonstrated by the integration of PAC-3 MSE with LRHW defense in the February 2024 test. Furthermore, the threat compels nations without hypersonic ambitions to invest heavily in advanced BMD, thus expanding that market globally. Hypersonics represent a new high-value niche within the strategic missile market, attracting new entrants and partnerships, such as India's HSTDV/BrahMos-II and EU efforts through MBDA.

Recent developments underscore the collaboration, fueling this growth. Major contracts center on essential RDT&E, such as MDA's Glide Phase Interceptor downselect to RTX and Northrop Grumman in April 2024, and L3Harris's USD 209 million HBTSS award in January 2024. Strategic alliances are crucial; for example, AUKUS Pillar II explicitly prioritizes hypersonics/counter-hypersonics co-development, while NATO's USD 1.17 billion Innovation Fund in June 2023 targets significant technological advancements in hypersonics. The industry consolidates capabilities through M&A, such as Thales acquiring RUAG for composites in January 2024, and Leidos acquiring Gibbs & Cox for naval integration in March 2021, while venture capital invests in startups such as Hermeus and Venus Aerospace. This global industrial and governmental mobilization, driven by competition and technological need, ensures ongoing RDT&E investment and procurement growth across hypersonics and the interconnected ballistic missile market in future.

Ballistic Missiles Market Trends

Shift toward Mobile and Survivable Launch Platforms has Emerged as a Market Trend

The fundamental driver accelerating demand for Transporter Erector Launchers (TELs) and Nuclear Ballistic Missile Submarines (SSBNs) is the critical need for enhanced survivability against modern precision-strike capabilities. Fixed silos are increasingly vulnerable to advanced Intelligence, Surveillance, and Reconnaissance (ISR) systems, hypersonic missiles, and MIRV-ed warheads, making them potentially susceptible to a disabling first strike. In contrast, mobile TELs utilize camouflage, dispersal, and constant movement ("hide and shoot") to evade detection. SSBNs operate undetected in the vast ocean, providing a nearly invulnerable second-strike capability for assured retaliation. This survivability is crucial for credible nuclear deterrence in an era of escalating great power competition (US-China, Russia-NATO) and deteriorating arms control treaties (INF collapse, New START uncertainty), compelling nations to prioritize these resilient platforms.

Technological advancements underpin this shift, including missile miniaturization, such as solid-fueled ICBMs/SLBMs, improved platform mobility, such as advanced TEL off-road capability, rapid launch sequences, SSBN pump-jet propulsion, quieting, and enhanced command and control. Massive as well as long-term investments in next-generation SSBNs demonstrate this commitment. The U.S. investments in Columbia-class into General Dynamics Electric Boat were worth USD 9.47 billion in December 2022 and USD 5.1 billion in Nov 2023; BAE Systems USD 4.2 billion for propulsion in August 2023. The U.K. investments in Dreadnought-class into BAE Systems USD 5.33 billion in September 2022, Rolls-Royce USD 2.65 billion for the reactor in June 2023. The French procurement agency invested in SNLE 3G (Naval Group design in 2021), and the landmark AUKUS pact in March 2023, facilitating nuclear submarine tech transfer to Australia.

Simultaneously, new mobile ICBM programs are surging, such as the US GBSD/Sentinel TEL-based system through Northrop Grumman USD 13.3 billion in EMD 2020, Oshkosh TELs, CDR in Sep 2023, Russian Yars/Sarmat deployments in September 2023, Chinese DF-41/DF-31AG deployments, North Korean Hwasong-17/18 tests in July 2023, and India's Agni-V MIRV test from TEL in March 2024.

This focus on survivability is reshaping the global ballistic missile market, driving accelerated demand for TELs, especially in Asia Pacific - China, India, Pakistan, North Korea, and Russia. In addition, sustaining multi-decade SSBN/SLBM replacement cycles among major powers (the U.S., U.K., France, Russia, China, and India). While fixed silos are being modernized, such as the U.S. Sentinel silos for cost-effectiveness and as part of diversified arsenals, relative market growth is overwhelmingly concentrated in mobile/survivable segments and their aiding technologies, such as stealth, C4ISR, and advanced propulsion. Geopolitical instability and regional proliferation concerns further reinforce this trend, as North Korea, India, and Pakistan rely heavily on TELs for credible deterrence without extensive SSBN fleets. Consequently, the forecast period will see sustained market growth fueled by the strategic necessity of mobile and concealed launch platforms to ensure nuclear deterrence viability against evolving threats.

Blurring Lines between Conventional and Nuclear Strike Options to Influence Development of Dual-Use Systems

The intentional blurring of conventional and nuclear boundaries is a strategy employed by major powers to enhance deterrence through ambiguity. The U.S., Russia, and China are developing dual-capable systems, such as the U.S. Conventional Prompt Strike, Russia's Kinzhal, and China's DF-26, to complicate adversaries' decision-making, using uncertainty as a deterrent. This drives research and development into delivery platforms that serve both conventional precision-strike and nuclear roles, undermining traditional distinctions. Programs including the U.S. Sentinel ICBM (USD 13.3 billion development) and AUKUS hypersonic collaborations (2023) exemplify technological convergence, where conventional missiles achieve strategic range and nuclear-alike accuracy while nuclear systems adopt advanced guidance, fueling a self-reinforcing cycle of innovation and proliferation. This results in increased crisis instability, as shown by Russia's 2024 threats linking Kinzhal to nuclear escalation and China's DF-26 brigade expansions.

This strategic ambiguity directly accelerates the global ballistic missiles market, which is projected to grow with hypersonics as the fastest-growing segment. The following three interconnected factors drive demand:

- Great Power competition (AUKUS hypersonics, U.S.-Japan ship-killer missiles)

- Regional arms races (India’s Agni-V tests, Pakistan’s responses)

- Alliance security needs (NATO’s Tyrfing missile, European Sky Shield).

Contracts including Lockheed Martin’s USD 756 million LRHW award in January 2024 and Kongsberg’s USD 1.2 billion Tyrfing contract in July 2024 highlight market momentum. The influx of private capital, exemplified by BlackRock’s USD 12 billion aerospace acquisition in December 2024, along with vertical integration witnessed in the L3Harris-Aerojet merger in July 2023, enhances R&D and production resilience, enabling rapid scaling of dual-use technologies.

The dual-use surge creates dangerous escalation pathways. Entanglement risks arise when conventional and nuclear assets share platforms, such as DF-26 brigades or C2 networks, increasing the likelihood that conventional strikes could be misinterpreted as nuclear attacks, particularly with the hypersonic compression of decision windows, such as DF-17’s 5-minute flight time to Taiwan. This fuels arms racing, as evidenced by Russia’s "mirror responses" to NATO deployments and India-Pakistan missile developments. According to NIST 2025 guidelines, AI integration further blurs fire-control distinctions, while arms control erosion, exemplified by Russia’s New START suspension, eliminates stabilizing frameworks. Ultimately, the cycle of ambiguity-driven procurement and escalating threats — demonstrated by global missile defense investments, such as the USD 345 million SM-3 contract in December 2023 — lowers nuclear thresholds and increases miscalculation risks, with market growth and strategic instability becoming mutually stronger.

Download Free sample to learn more about this report.

War Impact Analysis

Demand Surge & Strategic Reassessment, Supply Chain Strain, Technological Acceleration, Proliferation Risks, and Long-Term Instability Drive Market Expansion

Global war and conflict act as the primary accelerant for the ballistic missile market, triggering an immediate and profound surge in demand. Acute conflicts, such as the Russo-Ukrainian War, demonstrate the critical role of the product in long-range strike, strategic deterrence (including nuclear signaling), and countering integrated air defenses. This visibility compels nations, particularly those perceiving direct threats or operating in volatile regions (e.g., East Asia, Middle East, Eastern Europe), to accelerate procurement, store refill, and force modernization programs.

Beyond immediate conflict zones, latent geopolitical tensions drive a global strategic reassessment. The erosion of arms control frameworks (e.g., INF Treaty collapse), heightened major power competition (US-China-Russia), and proliferation concerns foster an environment where ballistic missiles, especially those with greater range, accuracy (conventional or nuclear), and survivability features (maneuverable re-entry vehicles - MaRVs, hypersonic glide vehicles - HGVs), are viewed as indispensable instruments of national security and power projection. This fuels sustained, long-term investment across established and developing missile powers.

Conflict disrupts and reshapes the global supply chain for missile production. High-intensity warfare rapidly reduces existing stockpiles of missiles and critical components (guidance systems, solid propellant, specialized alloys, semiconductors), exposing vulnerabilities and creating acute shortages. This drives intense competition for scarce resources, inflates costs, and incentivizes states to aggressively pursue import diversification, black/gray market procurement, or forced domestic industrial expansion – often at the cost of efficiency or price control.

Simultaneously, the operational demands of modern conflict act as a potent catalyst for technological acceleration. Lessons learned drive rapid iteration in areas such as counter-electronic warfare resilience, terminal guidance precision for conventional strikes, penetration aids against advanced missile defenses (BMD), and hypersonic technologies. This R&D surge, heavily funded by defense budgets swollen by perceived threat, further fragments the market. Distinct technological ecosystems develop, aligned with major powers (US/NATO, Russia, China), leading to incompatible systems, specialized regional niches, such as short-range missiles (SRBMs) for regional powers, and a widening gap between the capabilities of leading and developing missile states.

SEGMENTATION ANALYSIS

By Missile Type

Demand for Strategic Deterrence and Long-Range Strike Capabilities Drive Land-Attack Segment’s Growth

By missile type, the market is divided into Land-Attack (LABM), Anti-Ship (AShBM), and Air-Launched (ALBM).

Land-Attack (LABM) is the dominant segment and will hold a significant market with a share of 66.33% in 2026. This growth is attributed to its crucial role as the basis for strategic deterrence and long-range conventional strike capabilities. Massive nuclear modernization programs, active deployments, and the demand for precision conventional strikes against fixed targets drive sustained investment in the segment. Its versatility across ranges, from tactical to intercontinental systems, along with its essential function in major power deterrence postures, ensures continued procurement and technological upgrades. For instance, in March 2024, Northrop Grumman Corporation secured multi-billion-dollar production contracts for the U.S. Ground Based Strategic Deterrent (GBSD) to develop and provide Next-Generation ICBMs to the Missile Defense Agency (MDA). Additionally, in September 2023, Russia deployed the Sarmat ICBM through its first operational regiment, marking a shift in strategic investment. In April 2024, Poland signed a contract with Hanwha Aerospace to deliver Chunmoo MRLS capable of firing Homar-K missiles with a range of over 600 km.

Anti-Ship (AShBM) is anticipated to be the fastest-growing segment during the forecast period. The growth is attributed to the urgent need to counter naval power, particularly in the Indo-Pacific. China’s DF-21D/DF-26 programs demonstrated their game-changing potential, triggering rapid development of hypersonic-enabled systems. For instance, in March 2024, under the Conventional Prompt Strike (CPS) program, the U.S. Navy had completed comprehensive testing between 2023 and 2024. It is planning an initial operational capability (IOC) on its Zumwalt-class destroyers by late 2025 through contracts with Lockheed Martin and Dynetics. These developments of strategic necessity, hypersonic technology integration, and regional threat proliferation drive explosive market expansion.

By Component

Emphasis on Precision Strike, Resilience Against Jamming and Spoofing Stimulate Guidance Systems Growth

The market is divided by component into guidance systems, propulsion systems, warheads, missile airframes, sensors & seekers, and communication systems.

The guidance systems segment will be the leading segment, holding the largest market share of 34.64% in 2026. Due to its essential role as the missile brain, it remains as a primary component segment, requiring substantial investment to achieve precise strikes, ensure credible deterrence, and counter advanced Ballistic Missile Defense (BMD) systems. It is crucial for achieving extreme accuracy through Inertial Navigation Systems (INS)/ Global Positioning System (GPS), TERCOM (Terrain Contour Matching), DSMAC (Digital Scene Matching Area Correlator), resilience against jamming and spoofing, maneuvering capabilities (MaRVs), and the complex integration demands of hypersonic flight (HGVs), which drive sustained as well as high-value contracts and R&D.

For instance, in February 2024, Raytheon Technologies Corporation secured multiple contracts worth USD 345 million for Standard Missile guidance components and under the GEM-T program for Patriot missile guidance upgrades. In April 2024, DRDO had completed successful Advanced Guidance Tests of indigenously developed Long-Range Guidance Kit for conventional missiles, which showcases technological progress directly transferable to missile guidance systems. Additionally, in March 2024, U.S. Missile Defense Agency had awarded a contract worth USD 218 million to Lockheed Martin Corporation for THAAD interceptor guidance electronic assembly modernization, showcasing criticality and continuous investment in guidance technology.

Sensors and seekers segment is anticipated to be the fastest-growing segment with the highest CAGR during the forecast period. This growth is fueled primarily by the revolution in terminal-phase targeting needed for conventional missiles against moving or hardened targets and the extreme demand of hypersonic flight. The need for pinpoint accuracy requires Radar, IIR, Multi-Mode seekers, countering maneuvering targets, operating through plasma sheathing in hypersonics, and multi-sensor fusion, driving high investment in R&D and procurement.

For instance, in January 2024, BAE Systems and Elbit Systems announced a multi-mode seeker collaboration to develop and produce next-generation multi-mode seekers such as RF/IIR for precision-guided missiles and munitions. In March 2024, U.S. Missile Defense Agency had awarded a contract worth USD 96 million to L3Harris Technologies for the delivery of Hypersonic and Ballistic Tracking Space Sensor (HBTSS) satellites. This development fuels advancements in sensor technologies applicable to interceptor ballistic missile seekers demanding to operate in/against hypersonic threats.

By Missile Speed

Operational Readiness and Economic Viability Power Supersonic Ballistic Missiles Toward Dominance

By missile speed, the market is divided into subsonic (below Mach 1), supersonic (Mach 1 - 5), and hypersonic (above Mach 5).

Supersonic wiill dominate the segment with largest market with a share of 54.60% in 2026. Supersonic missiles maintain market dominance due to proven maturity, cost-effectiveness, immediate operational readiness, and widespread deployment. It fulfills critical strike and deterrence roles for nations without the extreme technical complexity and cost. Recent conflicts in Ukraine and the Middle East underscore their battlefield utility for precision strikes against high-value targets and overcoming layered air defenses. Continuous upgrades in accuracy (GPS/INS, terminal seekers), penetration aids (MaRVs, decoys), and range extensions ensures its relevance. Production scalability and established supply chains allow rapid replenishment and exports.

For instance, between 2023 and 2024, Raytheon Technologies Corporation received a production order amid high demand for SM-3 Block IIA supersonic hit-to-kill interceptors as to Japan deployments, the U.S. Navy contracts. This reflects the threat environment driven by offensive supersonic missiles and necessitates counter-capabilities. In March 2024, Russia announced that it is continuing the Iskander-M deployment for extensive use in Ukraine and confirming its effectiveness driving demand for similar capabilities globally. Observed upgrades focus on countering EW and improving accuracy.

The hypersonic segment is expected to be the fastest-growing segment with the highest CAGR during the forecast period. This growth is due to their unparalleled ability to penetrate advanced missile defenses (BMD). Their speed, maneuverability, and unpredictable flight profiles render existing BMD systems largely obsolete, offering a decisive strategic advantage. Intense major power competition (U.S. vs. China vs. Russia) is the primary driver, fueled by fears of falling behind. Russia's use of Kinzhal (air-launched HGV) in Ukraine, though limited, provided real-world proof-of-concept, accelerating urgency. Investment focuses on overcoming immense technical challenges including materials science (heat resistance), propulsion (scramjets), guidance (navigation at extreme speeds), and C4ISR integration. While unit costs are high, the perceived strategic necessity justifies massive R&D and procurement budgets.

For instance, in May 2024, the U.S. and Japan announced a partnership to co-develop Glide Sphere counter-hypersonic missile interceptors (Glide Phase Interceptor - GPI), indirectly validating the threat and driving offensive hypersonic R&D further.

By Launch Platform

Ground-based Platform Lead Due to Precision Missile Strikes from Fixed or Mobile Launchers

By launch platform, the market is sub-divided into airborne, ground-based, and naval segments.

Ground-based systems dominated the market and will hold the largest with a share of 71.03% in 2026. This growth is attributed to the high reliability of ground-based launchers for nuclear deterrence, bolstered by significant investments and national doctrines. The preference for ground-based launchers is also linked to their lower complexity, cost, and infrastructure requirements compared to sea or air launches. Hypersonic Glide Vehicles (HGVs) and advanced SRBMs/MRBMs, such as Iskander, PrSM, are ground-launched for tactical / theater-level precision strikes, observing high demand in regional conflicts, such as the Ukraine War and Taiwan Strait tensions. Established production lines, testing sites, and basing infrastructure create significant inertia and economies of scale. Mobile TELs offer survivability and operational flexibility incomparable by fixed silos or complex naval platforms. For instance, in June 2024, India had successfully tested Agni-P Prime, the new generation, canisterized MRBM, emphasizing ongoing modernization and expansion of its ground-based deterrent and regional strike force.

Naval is anticipated to be the fastest-growing segment with the highest CAGR during the forecast period. Submarine-launched Missiles (SLBMs) are the cornerstone of a credible nuclear second-strike capability due to submarine stealth. This drives continuous modernization programs, such as the U.S. Columbia-class/Trident D5LE, U.K. Dreadnought/D5LE, French SNLE 3G/M51.3, and Chinese Type 096/JL-3. SSBNs provide global reach and a persistent deterrence posture, making them highly valued assets in higher power competition. Integration of hypersonic and advanced missiles (IRBMs) onto surface ships (destroyers and SSGNs) is a rapidly emerging trend, such as U.S. CPS, Chinese DF-21D/DF-26B ship variants, and Russian Zircon deployment plans, for long-range, non-nuclear strikes. Intense focus on naval power projection and A2/AD capabilities in the Pacific directly fuels investment in sea-based ballistic and hypersonic missiles. Advances in missile design (smaller size, solid fuel), navigation (GPS-independent), and submarine quieting technologies enable more capable and numerous sea-based systems.

For instance, in July 2023, the US Navy awarded USD 5.1 billion for Trident II (D5LE) contract modification to Lockheed Martin for continued D5LE production and support, ensuring SLBM capability for US/UK SSBNs into the 2040s. In February 2024, India had successfully tested a user trial of the K-4 SLBM from INS Arihant, its indigenous SSBN, marking significant progress in its sea-based deterrent.

To know how our report can help streamline your business, Speak to Analyst

By Missile Range

Nuclear Modernization Programs and Collapse of Arms Control Frameworks Drive Demand for Ballistic Missiles with Intercontinental Range

The market is segmented into tactical range (Below 300 km), short range (300 – 1,000 km), medium range (1,000 – 3,500 km), intermediate range (3,500 - 5,500 km), and intercontinental range (above 5,500 km), based on missile range.

Intercontinental range is anticipated to be the fastest-growing segment with the highest CAGR during the forecast period. The segment is experiencing the fastest growth, driven by massive, concurrent nuclear modernization programs in major powers and the collapse of arms control frameworks amid intense strategic competition. Colossal investments focus on replacing aging Cold War systems with new ICBMs featuring enhanced survivability, readiness, and advanced penetration technologies such as hypersonic glide vehicles (HGVs) to defeat missile defenses. Despite lower volume than tactical missiles, these ICBM programs' sheer scale and strategic priority fuel exceptional revenue growth.

Tactical range is a dominant segment and the held largest market share in 2024. This growth is attributed to their pervasive role in active regional conflicts, conventional deterrence, and precision strike requirements. Their lower cost, operational utility against tactical targets, and relative accessibility fuel constant demand for replenishment, upgrades, and force modernization, particularly for countering A2/AD strategies. This segment thrives on widespread operational need and a lower barrier to entry for regional actors. For instance, in February 2024, the U.S. Army awarded a contract worth USD 219 million for Early Operational Capability (EOC) production of the Precision Strike Missile (PrSM) Increment.

By Propulsion System

Rapid Deployment, Enhanced Survivability, and High Investment in Solid Propellant-based Missiles Stimulate Growth

By propulsion system, the market is divided into solid propellant and liquid propellant.

Solid propellant dominated with largest market share in 2024 and is anticipated to be the fastest-growing segment with the highest CAGR during the forecast period. This growth is due to its critical operational advantages including rapid deployment, enhanced survivability (such as safer storage, mobile launch compatibility), and reliability. These attributes are indispensable for modern "launch-on-warning" policies, mobile platforms (TELs, SLBMs), and hypersonic boost-glide vehicles. Stockpile replenishment, major power modernization programs, and proliferation among emerging missile states drive its growing demand.

Liquid propellant was the second-largest segment with a significant market share in 2024. This growth is due to legacy ICBM fleets in Russia (SS-18, RS-28 Sarmat) and China (DF-5), which rely on its higher efficiency for heavy payloads/extended range and throttling capability for advanced trajectories. While growth is slower than solid fuel, significant investment persists in modernizing silo-based deterrents and leveraging space launch vehicle (SLV) technology synergies. These efforts ensure liquid systems retain relevance for strategic heavy ICBMs despite operational drawbacks including lengthy fueling times and fixed infrastructure vulnerability.

Ballistic Missiles Market Regional Outlook

By region, the market is studied into North America, Europe, Asia Pacific, Middle East and rest of the world.

North America

North America Ballistic Missiles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 3.27 billion, accounting for 32.28% of the worldwide market, and is projected to grow to USD 3.41 billion in 2026. Strategic deterrence and defense requirements primarily drive missile development in the region. The U.S. upholds a significant resource of intercontinental missiles (ICBMs) and submarine-launched missiles (SLBMs) as part of its nuclear triad, ensuring a second-strike capability against potential rivals. These missiles serve as a deterrent against nuclear and conventional threats, assuring national security. Additionally, missile defense systems in the region aim to intercept and neutralize potential missile attacks, thereby enhancing regional stability. The evolving threat landscape, marked by advancing missile technology from adversaries, highlights the necessity of upholding advanced missile capabilities for defense and deterrence. The U.S. market is projected to reach USD 3.15 billion by 2026.

The U.S. develops and maintains missiles to sustain strategic deterrence, safeguard national security, and project global military power. ICBMs and SLBMs are essential components of its nuclear triad, ensuring a credible second-strike capability in the event of nuclear conflict. Additionally, the U.S. invests in missile defense systems such as THAAD and Aegis to counter potential threats from adversaries’ missile arsenals.

Europe

The Europe market generated USD 3.05 billion in 2025, representing 30.08% of the global market landscape, and is expected to reach USD 3.17 billion in 2026. Europe stood as the second-largest region regarding market share in 2025. NATO’s strategic posture and regional security concerns shape the missile landscape in Europe. Although most European nations lack independent ICBM capabilities, they depend on the U.S. nuclear deterrence and missile defense systems for safety. The deployment of missile interceptors and the development of advanced missile defense systems aim to counter potential threats from rogue states or emerging missile technologies. Europe emphasizes maintaining regional stability through alliances and deterrence, prioritizing missile defense over offensive missile proliferation. The threat of regional conflicts and concerns about proliferation drives the ongoing investments in missile technology and defense infrastructure. The UK market is projected to reach USD 0.18 billion by 2026, while the Germany market is projected to reach USD 0.14 billion by 2026.

Asia Pacific

Asia Pacific contributed 19.36% to the global market in 2025, with a valuation of USD 1.96 billion, and is projected to reach USD 2.07 billion in 2026. This area is witnessing rapid missile development, driven by geopolitical tensions, territorial disputes, and regional rivalries. China, India, North Korea, and Russia are pursuing missile capabilities to enhance their strategic deterrence, assert regional dominance, and counter adversaries. North Korea’s missile program focuses on nuclear deterrence and coercion, while China and India are developing long-range missiles to protect their national interests. The proliferation of missile technology and ongoing modernization efforts demonstrate a desire for strategic stability and power projection. Regional instability and the potential for conflict escalation make missile capabilities a critical aspect of military defense strategies across this region. The Japan market is projected to reach USD 0.05 billion by 2026, the China market is projected to reach USD 0.53 billion by 2026, and the India market is projected to reach USD 0.42 billion by 2026.

Middle East

The Middle East & Africa market was valued at USD 1.43 billion in 2025, capturing 14.06% of global revenue, and is estimated to reach USD 1.49 billion in 2026. The Middle East is projected to experience moderate growth during the forecast period. This region plays a crucial role in security dynamics, often serving as a tool for power projection and deterrence. Iran possesses missile arsenals capable of targeting regional rivals and exerting influence throughout the broader Middle East. Iran’s development is intended to counter regional adversaries, deter foreign intervention, and bolster its strategic bargaining power.

Rest of the World

The rest of the world region is anticipated to observe significant growth during the forecast period. Ballistic missile development in Latin America remains limited, mainly influenced by geopolitical factors, defense modernization, and regional security concerns. The market in Latin America reached USD 0.43 billion in 2025, representing 4.23% of total market revenue, and is projected to reach USD 0.44 billion in 2026. Brazil and Argentina primarily utilize missile technology for defense and deterrence, focusing on regional stability. Some nations may pursue short-range missiles for tactical defense or to enhance their technological capabilities. Similarly, Africa is also expected to experience a rising demand due to various ongoing geo-political issues in the region.

Competitive Landscape

Key Market Players

Leading Players are Focusing on Integrating Advanced Technologies to Identify Objects in Low-Light

The market is fiercely competitive, primarily led by major defense contractors and state-sponsored missile programs. Key players include Lockheed Martin, Boeing, Northrop Grumman, Raytheon Technologies, and China Aerospace Corporation, which are investing heavily in advanced missile technology, precision, and range capabilities. The market is fueled by rising geopolitical tensions, regional conflicts, and the necessity for strategic deterrence, prompting nations to modernize and expand their missile resources.

Innovation emphasizes missile accuracy, stealth capabilities, and multi-stage propulsion systems, while governments prioritize the integration of missile defenses. Emerging nations such as India, Israel, and North Korea are also enhancing the competitive landscape by developing their own missile technologies. International arms control treaties and concerns about proliferation impact market dynamics, influencing research, development, and sales. Overall, the market is marked by technological innovation, strategic alliances, and government-led modernization efforts, creating a highly competitive sector with significant geopolitical implications.

LIST OF KEY BALLISTIC MISSILES COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- The Boeing Company (U.S.)

- MBDA (France)

- BAE Systems plc (U.K.)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- Makeyev Rocket Design Bureau (GRTs Makeyeva) (Russia)

- NPO Mashinostroyeniya (Russia)

- Bharat Dynamics Limited (India)

- China Aerospace Science Industry Corporation (CASIC) (China)

- Korea Aerospace Industries (KAI) (South Korea)

- Hanwha Aerospace (South Korea)

- Yuzmash (Ukraine)

- Roketsan (Turkey)

- Avibras (Brazil)

KEY INDUSTRY DEVELOPMENTS

- May 2024 - Raytheon Technologies entered into a strategic alliance with South Korea’s Agency for Defense Development (ADD). The partnership aims to co-develop next-generation missile defense systems capable of intercepting highly advanced ballistic missile threats, bolstering South Korea’s regional security posture.

- April 2024 - North Korea launched a new hypersonic missile, showcasing its continued advancements in missile technology. The government is now working with domestic defense manufacturers to accelerate indigenous development of hypersonic and intercontinental missile systems to counter regional threats.

- March 2024 - India’s Defense Research and Development Organisation (DRDO) announced the successful development and testing of the Agni-VI missile, featuring advanced stealth technology and a range exceeding 12,000 km. This missile is intended to enhance India’s nuclear deterrence and strategic reach across Asia and beyond.

- February 2024 - The China Aerospace Corporation (CASC) partnered with the China Academy of Launch Vehicle Technology to jointly develop a new solid-fuel intercontinental ballistic missile (ICBM). This collaboration aims to increase payload capacity and extend operational range, thereby enhancing China’s strategic missile arsenal.

- January 2024 - Lockheed Martin signed a USD 3 billion contract with the U.S. Air Force to modernize the Minuteman III Intercontinental Ballistic Missile (ICBM) system. This modernization aims to improve missile range, accuracy, and cybersecurity defenses, ensuring that strategic deterrence capabilities are maintained amid evolving threats.

REPORT COVERAGE

The report provides a thorough analysis of the market and emphasizes important aspects such as key players, products, applications, and platforms across various countries. Additionally, it offers in-depth insights into market trends, the competitive landscape, market competition, pricing, and overall market status while highlighting significant industry developments. Furthermore, it includes several direct and indirect factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.83% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Missile Type

|

|

By Component

|

|

|

By Missile Speed

|

|

|

By Launch Platform

|

|

|

By Missile Range

|

|

|

By Propulsion System

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 10.14 billion in 2025 and is anticipated to be USD 15.44 billion by 2034.

The market is likely to grow at a CAGR of 4.83% during the forecast period (2026-2034).

The top players in the industry are Lockheed Martin Corporation, Northrop Grumman Corporation, General Dynamics Corporation, The Boeing Company, MBDA, BAE Systems plc, Israel Aerospace Industries Ltd. (IAI), Makeyev Rocket Design Bureau (GRTs Makeyeva), and NPO Mashinostroyeniya.

In 2025, North America dominated the global market.

The expansion of intercontinental missiles (ICBMs) is largely driven by their role as a core component of nuclear deterrence strategies among major powers.

- 2021-2034

- 2025

- 2021-2024

- 350

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us