Matting Agents Market Size, Share & Industry Analysis, By Type (Silica-based, Wax-based, Organic Polymer-based, and Others), By Application (Architectural & Decorative, Industrial, Printing Inks, Wood & Furniture, and Others), and Regional Forecast, 2026-2034

Matting Agents Market Size and Future Outlook

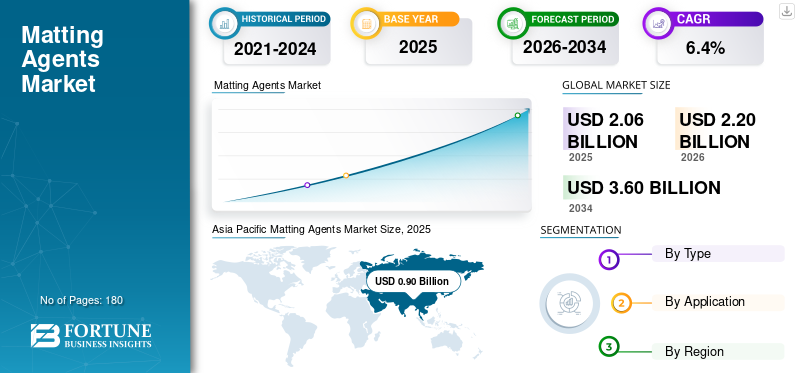

The matting agents market size was valued at USD 2.06 billion in 2025. The market is projected to grow from USD 2.20 billion in 2026 to USD 3.60 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. Asia Pacific dominated the matting agents market with a market share of 43.68% in 2025.

Matting agents are specialized additives employed primarily to diminish gloss and produce controlled matte, dead-matte, silky, textured, or soft-touch finishes in coatings and inks. Depending on their chemical composition and formulation design, they can also enhance properties such as scratch resistance, mar resistance, anti-blocking, slip, transparency, and tactile performance. These agents are predominantly supplied as silica-based, wax-based, and organic polymer-based systems, with additional niche demand for hybrid and specialized inorganic technologies.

Furthermore, the market is predominantly led by different major suppliers possessing profound expertise in coatings and extensive formulation support capabilities. Esteemed companies such as Evonik Industries AG, BYK Additives & Instruments, Lubrizol Corporation, allnex, Deuteron GmbH, and Münzing Chemie GmbH maintain robust positions through comprehensive product portfolios, technical services, and innovation tailored to specific applications across decorative, wood, industrial, powder, and specialty coatings applications. Their publicly available portfolios indicate that competition is driven by factors such as compatibility, matting efficiency, transparency, tactile qualities, durability, and regulatory compliance.

Download Free sample to learn more about this report.

Matting Agents Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.06 billion

- 2026 Market Size: USD 2.20 billion

- 2034 Forecast Market Size: USD 3.60 billion

- CAGR: 6.4% from 2026–2034

- Asia Pacific dominated the matting agents market with a 43.68% share in 2025.

- The industrial segment accounted for the largest market share in 2025.

- The wax-based segment held the second-largest market share in 2025.

Asia Pacific

Asia Pacific led the global market in 2025, reaching a valuation of USD 0.90 billion, supported by strong industrial and coatings demand.

Europe

Europe is expected to witness steady growth, reaching a market value of USD 0.45 billion by 2026 with a CAGR of 4.9%.

North America

North America continues to benefit from rising demand for premium decorative paints, wood coatings, and industrial finishes.

U.S.

U.S. The matting agents market is estimated to reach approximately USD 0.37 billion in 2026, driven by growth in coatings and industrial applications.

Japan

Japan The market is projected to reach around USD 0.10 billion in 2026, supported by demand from automotive, industrial, and specialty coating sectors.

Read More

MATTING AGENTS MARKET TRENDS

Shift Toward Premium Matte-Surface Engineering is Prominent Market Trend

A major trend in the market is the shift from single-purpose gloss suppression toward multifunctional matte-surface design. In current coatings development, formulators increasingly expect matting agents to contribute not only to low gloss but also to a smooth feel, soft-touch effects, anti-blocking, transparency, burnish resistance, mar resistance, and better overall surface quality. Public product and technical materials from Evonik Industries AG, BYK Additives & Instruments, Lubrizol Corporation, and Deuteron GmbH consistently position matting agents as tools for both visual and tactile optimization, especially in premium coatings systems.

This trend is especially evident in waterborne wood coatings, premium architectural paints, leather-like coatings, industrial finishes, and dead-matte powder coatings. Evonik Industries AG has explicitly highlighted the development of new visual-property tuning in waterborne leather coatings using various silica morphologies and particle sizes. Concurrently, BYK’s sustainable CERAFLOUR line and Lubrizol’s LiquiMatt products exemplify the mounting demand for additives that combine matting properties with a soft tactile sensation, transparency, and simplified formulation handling. The trend indicates that matting agents are transitioning from a limited additive category to a higher-value formulation tool.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth in Coatings Output and Premium Low-gloss Formulations is Accelerating the Adoption of Matting Agents

A significant matting agents market growth driver is the extensive and growing global coatings sector. Decorative paints, wood coatings, industrial coatings, powder coatings, and related specialty finishes collectively constitute the principal demand sources for these additives. As the product is used as a performance additive in these downstream systems, their growth is essentially linked to the expansion of coatings manufacturing and the demand for premium formulations.

Simultaneously, the intensity of additives per coating system is increasing within premium formulations. Matting agents are no longer employed solely to reduce shine as they are also selected to enhance clarity, tactile sensation, anti-blocking properties, scratch resistance, and visual depth. Evonik’s ACEMATT portfolio, Lubrizol’s silica/wax-based solutions, and BYK’s CERAFLOUR technologies exemplify this transition toward higher functional loading in premium decorative, wood, industrial, and specialty systems. As matte and ultra-matte finishes continue to expand their market share in architectural interiors, furniture, cabinetry, industrial metal surfaces, and consumer-facing applications, demand for advanced matting systems is growing faster than the volume of simple coatings alone.

MARKET RESTRAINTS

Formulation Trade-offs and Compatibility Constraints can Slow Replacement and Limit Cost-Down Opportunities

A significant limitation within the market is that matting agents are highly sensitive to formulation specifics. Enhanced matting efficiency may compromise transparency, viscosity, surface smoothness, sedimentation behavior, burnish resistance, and film clarity. Public literature from suppliers such as Evonik Industries AG and Deuteron GmbH indicates that various grades are designed with precise consideration of morphology, surface treatment, and compatibility requirements, owing to substantial performance variability across waterborne, solventborne, UV-curing, and powder coating systems. Consequently, substituting these agents is more complex than with typical commodity additives.

Another constraint is the pressure to reformulate products to meet evolving regulatory standards and customer demand while maintaining optimal performance. Notably, transitioning away from PFAS-associated or legacy surface-modification techniques can compel formulators to simultaneously recalibrate gloss, slip, anti-blocking properties, and durability. BYK’s ECS 2025 initiative concerning PFAS-free solutions, alongside Deuteron’s promotion of PTFE-free polymethylurea alternatives, exemplify the commercial significance of this transition. Consequently, changes in suppliers and chemical compositions may necessitate prolonged validation processes and extensive technical retesting, especially in high-performance industrial and specialty coating applications.

MARKET OPPORTUNITIES

Sustainable, Bio-based, PFAS-alternative, and Easier-to-process Products are Creating New Market Opportunties

A significant market opportunity in the market is sustainability-driven portfolio renewal. BYK has expanded its CERAFLOUR line with bio-based grades, such as CERAFLOUR 1003 and 1004, designed to achieve favorable matting and soft-feel effects with high transparency. Additionally, Deuteron has highlighted PTFE-free polymethylurea technologies that offer enhanced friction and tactile properties. These advancements indicate that bio-based and PFAS-alternative matting solutions are transitioning from experimental options to commercially viable products. Consequently, this development offers new prospects in decorative, industrial, wood, and specialty coatings, where sustainability assertions increasingly influence raw material selection.

A secondary opportunity is to transition toward more user-friendly formats that reduce processing complexity. Lubrizol’s Lanco LiquiMatt 5730 is marketed as a liquid matting agent suitable for wood coatings, capable of replacing multiple powder surface modifiers and thereby reducing dust generation and incorporation issues. This exemplifies a broader commercial trend where additives that facilitate handling, dispersion, and shop-floor processing, despite not possessing entirely novel chemistry, can capture increased market share. In a sectors where application support and formulation efficiency are highly valued, such user-friendly formats enable manufacturers to command premium prices and foster stronger supplier loyalty.

MARKET CHALLENGES

Cost Pressure and Multi-property Optimization Continue to Create Margin and Adoption Pressure

One of the primary challenges in the market is balancing premium performance with cost expectations. Decorative paints and coatings represent a substantial demand segment, however, they are also sensitive to price, which constrains formulators from extensively utilizing expensive specialty additives unless the performance enhancements are both perceptible and justifiable. Concurrently, higher-value segments such as wood, industrial, and specialty coatings require greater clarity, tactile qualities, scratch resistance, and process stability, thereby exerting ongoing pressure on suppliers to substantiate the value of premium formulations. In light of the moderate growth environment across the broader coatings industry, maintaining profit margins remains an ongoing commercial challenge.

Another challenge is that formulators increasingly desire multiple properties simultaneously such as low gloss, high transparency, a smooth feel, anti-blocking qualities, scratch resistance, low sedimentation, and ease of incorporation. Deuteron’s technical positioning regarding PMU-based matting agents and Evonik’s application guidance concerning various silica structures illustrate that suppliers are still addressing a multi-variable performance puzzle rather than a straightforward gloss issue. Consequently, the market continues to value formulation depth and technical service, although this also escalates commercialization complexity.

Segmentation Analysis

By Type

High Demand for Silica-based Systems Contributed to Segmental Growth

Based on type, the market is segmented into silica-based, wax-based, organic polymer-based, and others.

The silica-based segment dominated the market in 2025, driven by its extensive use in architectural, wood, and industrial coatings, plastics, and certain ink products. Silica-based agents are preferred for their high matting efficiency, adaptable gloss control, and the ability to modify clarity, transparency, and surface texture through variations in particle size, morphology, porosity, and surface treatment. Evonik’s ACEMATT portfolio, along with the broader scientific literature concerning matting silicas, underscores the importance of silica-based systems across major coating technologies.

The wax-based segment held the second-largest share in 2025, driven by applications that require gloss reduction, surface protection, slip, anti-blocking, and soft-touch qualities. Public BYK and Lubrizol materials demonstrate that wax-like and wax-based matting additives are particularly important in wood coatings, industrial coatings, inks, and specialty surface-finish systems. This segment is also benefiting from sustainable product development, with bio-based CERAFLOUR additives showing how wax-like matting technologies are advancing toward renewable raw-material platforms. Additionally, this segment is projected to grow at a CAGR of 6.4% over the study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Growing Demand for Higher Durability and Chemical Resistance by Industrial Sector Leads to Segment’s Dominance

In terms of application, the market is categorized into architectural & decorative, industrial, printing inks, wood & furniture, and others.

The industrial segment commanded the largest matting agents market share in 2025, notably in metal finishes, plastic coatings, coil coatings, engineered surfaces, and other performance-oriented systems. Industrial formulators typically prioritize low gloss alongside durability, anti-blocking, chemical resistance, and a smooth finish. Consequently, both silica- and wax-based systems are significant within this sector. Guidance from public suppliers indicates consistent utilization of matting technologies in such applications, especially where non-reflective finishes and high-quality aesthetic appeal are imperative. Additionally, this segment is forecasted to grow at a CAGR of 6.7% over the study period.

The wood & furniture segment is a high-value application sector and is among the most significant premium applications. Publicly available materials from Evonik and Lubrizol explicitly target matting products for wood coatings, where attributes such as matte appearance, silky texture, smoothness, and scratch resistance are critical performance parameters. This segment benefits from robust demand across cabinetry, furniture, flooring, interior joinery, and clear coats, where dead-matte or natural-look finishes are preferred. Although this segment is smaller in volume compared to decorative coatings, wood coatings typically support higher-value additive consumption per unit of coating.

The architectural & decorative segment constitutes a significant market share, supported by its position as the largest downstream category within the coatings industry worldwide. As matte finishes and low-sheen appearances gain popularity in interior walls, trims, premium emulsions, and design-oriented decorative systems, the demand for silica-based and hybrid matting technologies remains robust. This segment is particularly vital in the Asia Pacific, European, and North American regions, where high-end matte aesthetics are increasingly becoming mainstream in residential and commercial interiors.

Matting Agents Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Matting Agents Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region accounted for the largest share, valued at USD 0.82 billion, and continued to lead in 2025, with a valuation of USD 0.90 billion. This predominance is primarily attributable to the region’s focus of production in decorative coatings, industrial finishing, furniture manufacturing, plastics processing, and export-oriented coatings supply chains. China alone reported coatings output of 35.341 million tons in 2024, establishing it as the primary structural demand basis for matting-agent consumption. Japan also maintains its significance owing to its established coatings manufacturing sector and the detailed industry statistics published by the Japan Paint Manufacturers Association.

China Matting Agents Market

By 2026, the China market is projected to reach USD 0.54 billion. China is the largest demand center in the Asia Pacific region, driven by extensive use in architectural paints, industrial coatings, furniture finishes, plastic coatings, and engineered surfaces. The ongoing trend toward premiumization in decorative coatings, coupled with growth in industrial finishing, fosters increased consumption of silica- and wax-based matting systems. Concurrently, the expansion of specialty applications is progressively creating opportunities for polymer-based grades.

To know how our report can help streamline your business, Speak to Analyst

Japan Matting Agents Market

The Japan market in 2026 is estimated to be around USD 0.10 billion, accounting for roughly 4.7% of the global revenues.

India Matting Agents Market

The India market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 4.9% of global revenues.

Europe

Europe is anticipated to experience substantial growth in the market in the forthcoming years. Over the forecast period, the region is projected to grow at an annual rate of 4.9%, reaching a market valuation of USD 0.45 billion by 2026. This region is characterized by considerable demand across various sectors, including premium architectural coatings, industrial coatings, wood coatings, coil coatings, and powder coatings. Furthermore, Europe significantly contributes to the shift toward PFAS-free, bio-based, and more regulatorily compliant additive systems. The communication from BYK regarding ECS 2025 and sustainability initiatives, particularly regarding PFAS-free solutions, underscores the region’s leadership in modernizing formulations.

U.K. Matting Agents Market

The U.K. market in 2026 is estimated at around USD 0.05 billion, accounting for roughly 2.1% of global revenues.

Germany Matting Agents Market

Germany’s market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 3.6% of global revenues.

North America

North America represents a mature yet appealing market, characterized by premium decorative paints, wood coatings, industrial coatings, and specialized niche systems. Demand remains robust due to the continued acceptance of matte aesthetics, soft-touch surfaces, and high-performance industrial finishes across residential, commercial, and engineered sectors. Publicly available portfolios from Lubrizol and Evonik highlight sustained strength in silica- and wax-based solutions catering to both mainstream and premium coatings sector.

U.S. Matting Agents Market

Given North America’s strong contribution the U.S. market can be estimated at around USD 0.37 billion in 2026, accounting for roughly 16.8% of global sales.

Latin America and the Middle East & Africa

Over the forecast period, Latin America and the Middle East & Africa are anticipated to experience moderate growth. Latin America's expansion is driven by increasing demand for matting agents in the decorative and automotive sectors. In contrast, the Middle East & Africa region is gradually developing through the consumption of construction coatings, industrial coatings, and distribution-driven specialty additives. The Latin America market is projected to reach USD 0.12 billion by 2026.

GCC Matting Agents Market

The GCC market in 2026 is estimated at USD 0.06 billion, accounting for approximately 2.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Breadth, Technical Support, and Regulatory Alignment Leads to Market Competition

The market remains moderately fragmented, characterized by significant specialty-additives suppliers operating alongside specialized formulation experts. Competitive advantage is primarily derived from application engineering, compatibility across various coating systems, matting efficiency, clarity retention, surface feel optimization, and regulatory compliance support. The publicly available portfolios of Evonik Industries AG, BYK Additives & Instruments, Lubrizol Corporation, allnex, and Deuteron GmbH demonstrate a growing customer preference for suppliers capable of addressing integrated appearance and performance challenges rather than solely providing standard gloss-reduction additives.

Large incumbents also benefit from extensive cross-category offerings, including silica agents, wax additives, polymeric surface modifiers, powder-coating additives, and specialty sustainability-aligned solutions. This enables them to address a broader spectrum of formulation challenges across decorative, wood, industrial, and specialty sectors. Public evidence indicates that suppliers with robust technical service and localized formulation support are better positioned to secure premium market share, particularly as customers navigate PFAS-free requirements, bio-based content objectives, and multifunctional surface-property targets.

LIST OF KEY MATTING AGENTS COMPANIES PROFILED

- Evonik Industries AG (Germany)

- BYK Additives & Instruments (Germany)

- Lubrizol Corporation (U.S.)

- allnex (Germany)

- Deuteron GmbH (Germany)

- Münzing Chemie GmbH (Germany)

- R. Grace (U.S.)

- PQ Corporation (U.S.)

- Huber Advanced Materials (U.S.)

- Imerys (France)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Deuteron introduced the Deuteron MK-F7, a superior polymethylurea-based matting agent engineered to deliver enhanced tactile sensation, improved sliding, and friction performance, all achieved without the use of PTFE.

- March 2023: BYK has broadened its portfolio of sustainable additives by introducing CERAFLOUR 1003 and CERAFLOUR 1004, which are bio-based products derived from corn starch polymers, possessing wax-like characteristics suitable for matting and soft-feel effects.

REPORT COVERAGE

The global matting agents market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.06 billion in 2025 and is projected to reach USD 3.60 billion by 2034.

The market is projected to growth at a CAGR of 6.4% during the forecast period of 2026-2034.

Industrial application segment leads the market.

Asia Pacific held the highest market share.

Growth in coatings output and premium low-gloss formulations is accelerating the adoption of matting agents.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us