Medical Camera Market Size, Share & Industry Analysis, By Product Type (Endoscopy Cameras, Surgical Microscopy Cameras, Ophthalmology Cameras, Dermatology Cameras, Dental Cameras, and Others), By Sensor Type (CMOS Sensors and CCD Sensors), By Resolution (Standard Definition and High Definition), By Application (Surgical and Diagnostics), By End-user (Hospitals & Specialty Clinics, Diagnostic Centers, and Others), and Regional Forecast, 2026-2034

Medical Camera Market Size and Future Outlook

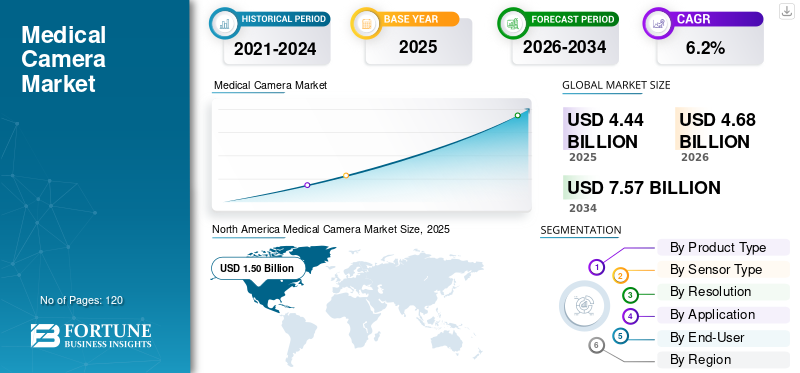

The global medical camera market size was valued at USD 4.44 billion in 2025. The market is projected to grow from USD 4.68 billion in 2026 to USD 7.57 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the medical camera market with a market share of 33.78% in 2025.

Medical cameras are imaging devices used by clinicians to visualize and record events inside or on the surface of the body during procedures. In this market, endoscopy cameras are a major part because they help doctors work through small openings with a clear view on a monitor. The market growth is attributed to a growing number of surgical & diagnostic procedures, technological advancements in image-capturing functionalities, and a focus on improved safety and consistency in the operating room. In addition, rising demand for cutting-edge surgical equipment due to better precision is also projected to have a positive impact on the growth.

- For instance, in January 2023, PENTAX Medical announced the launch of its new advanced and premium video processor, compatible with endoscopes.

Furthermore, many key industry players, such as Stryker Corporation, Olympus Corporation, KARL STORZ SE & Co. KG, Sony Group Corporation, and Carl Zeiss Meditec AG, operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

Medical Camera Market Key Takeaways

- 2025 Market Size: USD 4.44 billion

- 2026 Market Size: USD 4.68 billion

- 2034 Forecast Market Size: USD 7.57 billion

- CAGR: 6.2% from 2026–2034

- North America dominated the medical camera market with a 33.78% share in 2025.

- Endoscopy cameras accounted for the leading product type segment share in 2025.

- CMOS sensors dominated the global medical camera market by sensor type in 2025.

North America

North America was valued at USD 1.50 Billion in 2025, supported by the growing number of minimally invasive surgical procedures and advancements in imaging technologies.

Europe

Europe is projected to reach USD 1.21 Billion in 2026, driven by increasing investments in product innovation and rising surgical procedure volumes.

Asia Pacific

Asia Pacific is projected to reach USD 1.39 Billion in 2026, supported by expanding healthcare infrastructure and rising adoption of advanced imaging systems.

U.S.

The U.S. market is projected to reach USD 1.35 Billion in 2026, owing to strong demand for medical imaging systems across surgical and diagnostic applications.

Japan

The Japan market is projected to reach USD 0.24 Billion in 2026, driven by increasing adoption of advanced medical imaging technologies and growing healthcare investments.

Read More

MEDICAL CAMERA MARKET TRENDS

Faster Upgrades Through Modular Platforms is One of the Important Trends Observed in the Market

Recently, healthcare facilities and institutions have been focusing on the adoption of modern and compact equipment that can offer a wide range of functionalities in the same space. Moreover, hospitals are preferring systems that allow step-by-step improvements, adding features or compatibility through software and modular components. This reduces disruption, supports standardization, and lowers the risk of investing in equipment that quickly becomes outdated. Companies also highlight futuristic designs in their launches, reflecting strong buyer preference for flexible upgrade paths.

- For instance, in June 2024, OMNIVISION introduced the smallest dental-scanning camera module. The cameras are specially made for intraoral 3D scanners.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Minimally Invasive Procedures to Accelerate Market Growth

Minimally invasive procedures are becoming more common as they often involve smaller cuts, less pain, and a faster recovery for patients. Moreover, these procedures rely heavily on medical cameras to give surgeons a clear internal view. As hospitals expand laparoscopic, endoscopic, and robotic-assisted surgeries, the need for reliable imaging systems continues to increase. Surgeons also prefer high-quality visualization to improve precision and reduce complications. Due to this strong link between minimally invasive surgery and visualization, the growth in such procedures is directly pushing demand for medical camera systems across hospitals and specialty clinics. Thus, these factors lead to the medical camera market growth.

- For instance, according to data published by the NCBI in August 2024, Germany witnessed a rise in the proportion of colorectal minimally invasive surgeries from 26.2% in 2019 to 43.7% in 2023.

MARKET RESTRAINTS

High Upfront Spend and Slower Buying Cycles to Deter Market Expansion

Medical camera systems can be expensive once hospitals consider the full setup, including camera heads, control units, monitors, accessories, and installation. Even when a facility wants to upgrade, budgets may be released slowly, and approvals can take time. In addition, many hospitals also try to extend the life of current equipment through repairs and partial upgrades rather than full replacements. This delays purchasing and can create uneven demand across regions and hospital types.

MARKET OPPORTUNITIES

Expansion in Emerging Healthcare Infrastructure to Offer Lucrative Market Opportunities

Healthcare infrastructure is expanding in many emerging countries across Asia, Latin America, and the Middle East. Governments and private hospital groups are investing in new operating rooms and endoscopy suites. As these facilities come online, they require modern visualization equipment, including medical camera systems. Many of these markets are still under-penetrated, which creates room for new installations rather than just replacement sales. Moreover, manufacturers that offer cost-effective and easy-to-use camera platforms have strong growth potential in these regions. This geographic expansion is expected to create steady long-term opportunities for the medical camera market.

MARKET CHALLENGES

Integration and Training Across Busy Clinical Teams to Pose a Critical Market Challenge

Even when a hospital buys new camera systems, implementation can be challenging. Teams need training, workflows may need adjustment, and compatibility with existing equipment can create delays. Hospitals also run tight schedules, so switching systems room by room can be difficult without affecting procedure throughput. In addition, IT and security checks are becoming more common for connected systems, adding another layer of review before deployment.

Segmentation Analysis

By Product Type

Substantial Number of Endoscopic Procedures Globally Are Driving the Endoscopy Cameras Segment Growth

Based on the product type, the market is segmented into endoscopy cameras, surgical microscopy cameras, ophthalmology cameras, dermatology cameras, dental cameras, and others.

The endoscopy cameras segment accounted for the largest medical camera market share in 2025. Endoscopy cameras hold a high share as they are used across many specialties, and procedure volumes are large. In addition, they support both routine diagnostics and surgical work, so hospitals prioritize dependable camera stacks with consistent performance. Furthermore, new launches and upgrades from large manufacturers are also projected to boost segment growth.

The dental cameras segment is anticipated to rise with a CAGR of 7.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sensor Type

Superior and Modern Digital Imaging Needs in Clinical Environments Boosts CMOs Segment’s Growth

Based on sensor type, the market is bifurcated into CMOS sensors and CCD sensors.

In 2025, the CMOS sensors segment dominated the global market. CMOS sensors are widely used since they are well-suited for modern digital imaging needs in clinical environments. In addition, the sensors also offer benefits such as stable output, efficient performance, and compatibility with current camera platforms.

The CCD sensors segment is anticipated to rise with a CAGR of 5.4% over the forecast period.

By Resolution

Strong Balance of Image Clarity and Cost is Accelerating High Definition Segment’s Growth

Based on resolution, the market is divided into standard definition and high definition.

In 2025, the high definition segment dominated the global market. High-definition systems represent a large share as they offer a strong balance of clarity and cost. Moreover, many hospitals still standardize around HD in several rooms, even while premium rooms move toward higher resolutions. In addition, HD also supports training and documentation needs without forcing major infrastructure changes.

- For instance, in October 2025, Ikegami Tsushinki Co., Ltd. and NHK Foundation announced the development of MKC-820NP, a medical 8K Super high-vision camera.

The standard definition segment is anticipated to rise with a CAGR of 5.1% over the forecast period.

By Application

Considerable Number of Surgical Procedures to Boost Surgical Application Segment Growth

Based on application, the market is bifurcated into surgical and diagnostics.

In 2025, the surgical segment dominated the global market. Surgical use drives high demand since camera systems are essential in minimally invasive procedures, and many operating rooms rely on video as the primary view. Moreover, hospitals also invest in surgical visualization to improve workflow consistency and to support multiple specialties using the same rooms.

The diagnostics segment is anticipated to rise with a CAGR of 7.0% over the forecast period.

By End-User

Higher Volume of Surgical Procedures in Hospitals & Specialty Clinics to Accelerate Segment Growth

Based on end-user, the market is segmented into hospitals & specialty clinics, diagnostic centers, and others.

In 2025, hospitals & specialty clinics companies held the largest market share. Hospitals and specialty clinics lead because they perform the highest procedure volumes and need multiple camera systems across departments. They also require standardization, service support, and dependable uptime. In addition, collaboration between hospitals and key players is also estimated to drive segment growth.

- For instance, in November 2022, Hospital for Special Surgery and Lazurite entered into a strategic collaboration for the ArthroFree wireless surgical camera system.

In addition, the diagnostic centers segment is projected to grow at a CAGR of 6.6% during the forecast period.

Medical Camera Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Camera Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.43 billion, and the leading share in 2025, with USD 1.50 billion. The market in North America is expected to increase due to the growing number of minimally invasive surgical procedures and technological advancements in image-capturing functionalities.

U.S Medical Camera Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is set to hit USD 1.35 billion in 2026, accounting for roughly 28.8% of global sales.

Europe

Europe is projected to record a growth rate of 5.6% in the coming years and reach a valuation of USD 1.21 billion by 2026. The region is estimated to witness considerable market growth due to rising investments in new product development and a growing number of surgical procedures.

U.K Medical Camera Market

The U.K. market in 2026 is estimated at around USD 0.20 billion, representing roughly 4.2% of global revenues.

Germany Medical Camera Market

Germany’s market is projected to reach approximately USD 0.27 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.39 billion in 2026 and secure the position of the third-largest region in the market.

Japan Medical Camera Market

The Japanese market in 2026 is estimated at around USD 0.24 billion, accounting for roughly 5.2% of global revenues.

China Medical Camera Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.46 billion, representing roughly 9.9% of global sales.

India Medical Camera Market

India’s market in 2026 is estimated at around USD 0.31 billion, accounting for roughly 6.6% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.30 billion in 2026. In the Middle East & Africa, the GCC is set to reach USD 0.07 billion in 2026.

South Africa Medical Camera Market

South Africa’s market is projected to reach around USD 0.03 billion in 2026, representing roughly 0.63% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Number of Product Launches and Technological Advancements by Key Players to Boost Market Progress

The global market holds a semi-consolidated market structure, constituting prominent players such as Stryker Corporation, Olympus Corporation, KARL STORZ SE & Co. KG, Sony Group Corporation, and Carl Zeiss Meditec AG. The significant global medical camera market share of these companies is due to the growing number of product launches and technological advancements.

- For instance, in May 2024, Optomed USA, Inc. introduced Optomed Aurora AEYE, a handheld AI-based fundus camera for diabetic retinopathy.

Other notable players in the global market include Topcon Corporation, Danaher, Haag-Streit Group, Richard Wolf GmbH, and ConMed Corporation. These companies are expected to prioritize collaborations to increase their global market share during the forecast period.

LIST OF KEY MEDICAL CAMERA COMPANIES PROFILED

- Stryker Corporation (U.S.)

- Olympus Corporation (Japan)

- KARL STORZ SE & Co. KG(Germany)

- Sony Group Corporation (Japan)

- Carl Zeiss Meditec AG (Germany)

- Topcon Corporation (Japan)

- Danaher (U.S.)

- Haag-Streit Group(Switzerland)

- Richard Wolf GmbH (Germany)

- ConMed Corporation (U.S.)

- ATMOS MedizinTechnik GmbH & Co. KG (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2025: EIZO Corporation announced the launch of its new CuratOR SC431 surgical camera. The new system provides high performance and image-capturing features.

- September 2024: Stryker announced the launch of its advanced surgical camera in India. The newly launched camera provides enhanced surgical visualization.

- September 2024: Olympus Corporation announced the launch of its new 4K camera head for endoscopic gynecology and urology procedures in Europe. The product is developed in collaboration with Sony Corporation.

- June 2023: Eyenuk received FDA approval for its Topcon NW400 retinal camera system. The camera is equipped with AI features.

- August 2022: AVer Information Inc. announced its entry into the medical camera field. The company also introduced medical-grade PTZ cameras, MD330U and MD330UI.

REPORT COVERAGE

The global medical camera market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Sensor Type, Resolution, Application, End-User, and Region |

| By Product Type |

|

| By Sensor Type |

|

| By Resolution |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.44 billion in 2025 and is projected to reach USD 7.57 billion by 2034.

In 2025, the market value stood at USD 1.50 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period.

By product type, the endoscopy cameras segment is expected to lead the market.

The rising number of minimally invasive procedures and technological advancements is driving market expansion.

Stryker Corporation, Olympus Corporation, KARL STORZ SE & Co. KG, Sony Group Corporation, and Carl Zeiss Meditec AG are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us