Medical Display Market Size, Share & Industry Analysis, By Device Type (Diagnostic Displays, Surgical Displays, Dental Displays, and Others), By Panel Size (Up to 22 Inches, 23–26 Inches, and Above 41 Inches), By Resolution (Up to 2MP, 2.1–4MP, 4.1–8MP, and Above 8MP), By End-user (Hospitals & ASCs, Diagnostic Imaging Centers, Dental Clinics, and Others), and Regional Forecast, 2026-2034

Medical Display Market Size and Future Outlook

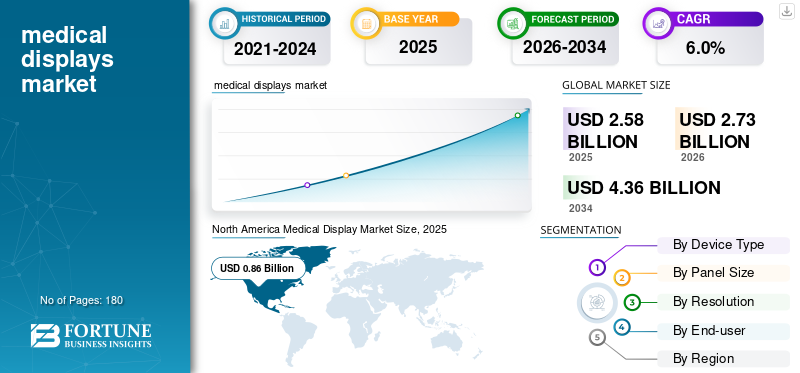

The global medical display market size was valued at USD 2.58 billion in 2025. The market is projected to grow from USD 2.73 billion in 2026 to USD 4.36 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. North America dominated the medical display market with a market share of 33.33% in 2025.

Medical displays are specialized monitors designed for diagnosis, clinical image viewing, surgery, and patient review, with performance features such as high brightness, grayscale accuracy, DICOM calibration, stable luminance, and long-term image consistency. The global market is growing rapidly, fueled mainly by the transition to digital image management systems that require large, high-brightness monitors in hospitals. As a result, healthcare facilities are upgrading from outdated CCFL and non-compliant screens to DICOM-calibrated LED or OLED displays to meet stringent image quality and regulatory requirements.

Furthermore, Barco, EIZO Inc., and Sony held the highest market share in 2025 due to their diversified portfolio and strong brand reputation.

Download Free sample to learn more about this report.

MEDICAL DISPLAY MARKET Key Takeaways

- 2025 Market Size: USD 2.58 billion

- 2026 Market Size: USD 2.73 billion

- 2034 Forecast Market Size: USD 4.36 billion

- CAGR: 6.0% from 2026–2034

- North America dominated the medical display market with a market share of 33.33% in 2025.

- The 23–26 inches segment accounted for the largest market share and is expected to hold 45.1% in 2026.

- The hospitals & ASCs segment led the market and is projected to account for 59.9% of the market in 2026.

North America

North America accounted for the largest share of revenues in 2024, valued at USD 0.82 billion, and also dominated in 2025 with a value of USD 0.86 billion. Robust infrastructure in the region is leading to high volumes of diagnostic and surgical procedures.

Europe

Europe is projected to record a growth rate of 5.4% during the forecast period, reaching USD 0.77 billion by 2026 due to established radiology workflows and the widespread use of CT, MRI, and PET across advanced healthcare systems.

Asia Pacific

Asia Pacific is projected to attain USD 0.61 billion by 2026, supported by expanding healthcare infrastructure and increasing investments in digital healthcare.

U.S.

The market is anticipated to reach USD 0.78 billion in 2026, representing approximately 28.5% of the global market, supported by favorable reimbursement policies and rising procedure volumes.

Japan

The market is projected to generate USD 0.17 billion in revenue by 2026, accounting for nearly 6.2% of the global market, driven by continued healthcare technology adoption.

Read More

MEDICAL DISPLAY MARKET TRENDS

Shift toward High-Resolution, Workflow-Centric, and AI-Ready Displays to Emerge as a Key Trend

Currently, key players are emphasizing higher resolution, wider panels, and breast imaging optimization, multiview viewing, and AI-enabled surgical visualization. They are positioning displays as part of a larger clinical workflow that includes integration with PACS and image management systems, as well as future-ready operating room platforms.

- For instance, in January 2021, Barco released the Nio Fusion 12MP diagnostic display, a versatile 12MP system for PACS and breast imaging that supports multiple modalities with KVM switching and DICOM calibration.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Adoption of Advanced Medical Imaging Modalities to Fuel the Market Expansion

Over the past few years, there has been a significant surge in diagnostic imaging procedures, including MRI, mammography, CT, ultrasound, and endoscopy, driving strong demand for DICOM-compliant, high-resolution medical displays for accurate image review and diagnosis. In response, major manufacturers are developing new products and entering partnerships with imaging system manufacturers to expand their reach worldwide. These factors are expected to drive the global medical display market growth.

- For instance, the National Center for Biotechnology Information (NCBI) data from August 2024 shows that around 6.4 million publicly funded CT scans occurred in the 2022–2023 fiscal year, equating to 160.2 scans per 1,000 people on average, up 9.0% from 2015.

MARKET RESTRAINTS

High Cost of Medical-Grade Displays to Restrict Market Growth

Despite strong demand for medical displays, the increased cost poses a major obstacle to broad adoption, especially in smaller hospitals and diagnostic centers. These displays must adhere to rigorous regulations and standards, which increases the overall production and calibration costs. Moreover, ongoing recalibration and maintenance needs increase total ownership costs, which is expected to hinder the market expansion in the forthcoming years.

- For instance, in December 2024, Carrot Medical introduced full large-display integration systems, priced between USD 100,000 and USD 200,000 for complete, turnkey installations.

MARKET OPPORTUNITIES

Expansion of Telemedicine to Offer Lucrative Opportunities

In recent years, the rise of telemedicine, digital pathology, and AI-powered diagnostic imaging has unlocked substantial growth opportunities for medical displays. The growing need for high-resolution, color-accurate, and remotely accessible visualization tools is also driving the demand for cutting-edge OLED, 4K/8K, and cloud-enabled medical monitors. This is expected to drive market expansion in the coming years.

- For instance, in April 2024, an analysis by Harvard Medical School indicated that expanded telemedicine services improved care quality and accessibility while causing only a slight rise in spending.

MARKET CHALLENGES

Technology Obsolescence, Integration Burden, and Price Pressure to Challenge Market Expansion

Rapid upgrades in panel technology, interface standards, and application-specific requirements may shorten the perceived relevance of products, forcing key companies to invest in R&D activities. Hospitals continuously must ensure compatibility among displays, graphics boards, PACS viewers, calibration software, and specialty workflows, further complicating deployment across large enterprises. Moreover, established brands and cost-focused domestic manufacturers are intensifying competition, which is expected to challenge market expansion.

Segmentation Analysis

By Device Type

Increasing Diagnostic Imaging Volumes to Boost the Diagnostic Displays Segment Growth

Based on device type, the market is segmented into diagnostic displays, surgical displays, dental displays, and others.

To know how our report can help streamline your business, Speak to Analyst

The diagnostic displays segment accounted for the largest global medical display market share in 2025. The segment’s growth is attributed to rising diagnostic imaging volumes and mandatory DICOM calibration requirements, which are expected to drive greater adoption of these displays in radiology departments.

- For instance, the Journal of the American College of Radiology (JACR) forecasted in February 2025 that imaging utilization in 2055 would be 16.9% to 26.9% higher than 2023 levels, assuming per-capita usage rates hold steady.

Additionally, the surgical displays segment is projected to grow at a CAGR of 6.5% during the forecast period.

By Panel Size

Increasing Number of Surgical Procedures to Drive the 23–26 Inches Segment Growth

By panel size, the market is segmented into up to 22 inches, 23–26 inches, and above 41 inches.

The 23–26 inches segment accounted for the largest market share in 2025. The segment’s growth is attributed to greater use of these displays in surgical procedures. Furthermore, the increasing number of surgical procedures is expected to drive the adoption of these displays. Moreover, the segment is estimated to hold a 45.1% share in 2026.

- For instance, Tomar Orthopaedics reported in November 2025 that the U.S. sees over 700,000 knee arthroscopies annually, compared to 150,000 in the U.K.

Additionally, the up to 22 inches segment is anticipated to grow at a CAGR of 5.0% over the forecast period.

By Resolution

High Usage of 2.1–4MP Displays in Radiology Departments to Boost the Segment’s Growth

By resolution, the market is classified into up to 2MP, 2.1–4MP, 4.1–8MP, and above 8MP.

The 2.1–4MP segment accounted for the largest market share in 2025. These resolutions fit general radiology, CT, MRI, and ultrasound applications well and are widely adopted in radiology departments. The adoption is due to their provision of sufficient pixel density for detailed image analysis at a lower cost than 5MP or 8MP alternatives. This affordability is expected to drive the segment’s expansion during the forecast period. Moreover, the segment is projected to hold a 36.2% share in 2026.

Additionally, the 4.1–8MP segment is expected to grow at a CAGR of 6.6% during the forecast period.

By End-user

Increasing Surgical Volume in Hospitals & ASCs to Propel the Segment’s Growth

On the basis of end-user, the market is segmented into diagnostic imaging centers, hospitals & ASCs, dental clinics, and others.

In 2025, the hospitals & ASCs segment led the market by end-user. There has been a rise in surgical volumes in ASCs and hospitals, boosting medical display usage in these settings and contributing to the segment’s growth in the coming years. Furthermore, the segment is set to hold 59.9% share in 2026.

In addition, the diagnostic imaging centers segment is estimated to surge at a CAGR of 6.4% during the analysis period.

Medical Display Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Display Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.82 billion, and also dominated in 2025 with a value of USD 0.86 billion. Robust infrastructure in the region is leading to high volumes of diagnostic and surgical procedures. Further, strong U.S. reimbursement policies are expected to boost display utilization by increasing procedure rates.

- For instance, Centers for Medicare & Medicaid Services data from March 2026 shows that Medicare reimburses most surgical procedures, covering the operation and post-op visits within a 10- or 90-day global period.

U.S. Medical Display Market

In 2026, the U.S. is anticipated to reach USD 0.78 billion, accounting for approximately 28.5% of the global market.

Europe

Europe is projected to record a growth rate of 5.4% during the forecast period, the third-highest globally, reaching USD 0.77 billion by 2026. The growth is attributed to established radiology workflows and the widespread use of CT, MRI, and PET across advanced healthcare systems in countries such as Germany, the U.K., and France.

U.K. Medical Display Market

The U.K. market is projected to reach USD 0.15 billion by 2026, representing approximately 5.4% of global revenues.

Germany Medical Display Market

The Germany market is expected to reach USD 0.17 billion by 2026, accounting for approximately 6.2% of global revenue.

Asia Pacific

By 2026, the Asia Pacific market is projected to reach approximately USD 0.61 billion, making it the second-largest market worldwide. The growth is attributed to expanding healthcare infrastructure and growing investment in digital healthcare across China, India, Japan, South Korea, Australia, and Southeast Asia.

Japan Medical Display Market

The Japan market is projected to generate approximately USD 0.17 billion in revenue by 2026, representing nearly 6.2% of the global market.

China Medical Display Market

The China market is anticipated to reach around USD 0.22 billion by 2026, accounting for nearly 7.9% of global revenues.

India Medical Display Market

The India market is expected to reach approximately USD 0.10 billion by 2026, accounting for around 3.7% of the global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 0.26 billion by 2026. The growth is supported by the gradual expansion of private hospitals, diagnostic centers, and specialty care infrastructure, especially in urban areas.

GCC Medical Display Market

By 2026, the GCC market is estimated to reach approximately USD 0.08 billion, representing around 2.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Product Portfolios Paired with Extensive Distribution to Solidify Leading Companies' Market Dominance

In 2025, Barco, EIZO Inc., and Sony held the largest global market share. This share is attributed to their established presence in radiology and surgical visualization, extensive product portfolios, and long-standing relationships with hospitals and imaging centers.

Moreover, other major players are expanding their geographical presence through signing strategic partnerships and acquisition agreements. Further, they are launching new products to expand their product portfolio and strengthen market share.

LIST OF KEY MEDICAL DISPLAY COMPANIES PROFILED

- Barco (Belgium)

- EIZO Inc. (Japan)

- Sony (Japan)

- Siemens Healthineers (Germany)

- BenQ Medical Technology Corp (Taiwan)

- LG Electronics (South Korea)

- NEC Corporation (Japan)

- Advantech Co., Ltd. (Taiwan)

- Double Black Imaging Inc. (U.S.)

- TRU-Vu Monitors, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: LG Electronics introduced the 31.5-inch 4K surgical monitor 32HS710S, equipped with smart features such as preset picture modes, failover input switching, and enhanced durability to optimize surgical workflows.

- August 2025: Sony launched the LMD-43M1MD, a 43-inch 4K 2D Mini LED surgical monitor for superior OR visibility. It boasts VESA DisplayHDR 1000 certification, 2,000 cd/m² peak brightness, 1,000,000:1 contrast, anti-reflective tech, and versatile connectivity.

- October 2024: Barco launched the Coronis OneLook flagship display solution for breast radiology on the first day of this year’s Breast Cancer Awareness Month.

- August 2024: EIZO Inc. launched the RadiForce RX670, a 30-inch 6MP radiology/teleradiology monitor with USB-C docking and comfort light.

- May 2024: Barco unveiled the AI-powered DL Precise tool for breast-imaging lesion segmentation across modalities, plus new Nio and Eonis 8MP displays with multimedia capabilities for seamless clinical collaboration at RSNA.

- April 2024: LG Electronics expanded its medical device push with the 21HQ613D 5MP diagnostic monitor, which was recently FDA-cleared in the U.S.

- April 2024: EIZO Inc. launched the CuratOR LX2420-T, a 23.8-inch Full HD touch monitor with 600 cd/m² brightness and DICOM compliance for ORs and interventional radiology.

REPORT COVERAGE

The report offers a comprehensive analysis of all market segments, examining key drivers, evolving trends, growth opportunities, restraints, and challenges influencing the market landscape. It further provides insights into technological developments, key procedure volumes, major industry developments, market share analysis, and detailed profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Device Type, Panel Size, Resolution, End-user, and Region |

| By Device Type |

|

| By Panel Size |

|

| By Resolution |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.58 billion in 2025 and is projected to reach USD 4.36 billion by 2034.

In 2025, the North America market value stood at USD 0.86 billion.

The market is expected to exhibit a CAGR of 6.0% during the forecast period of 2026-2034.

The diagnostic displays segment led the market by device type in 2025.

A key factor driving the market is the growing adoption of advanced medical imaging modalities.

Barco, EIZO Inc., and Sony are the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us