Medical Packaging Films Market Size, Share & Industry Analysis, By Material (Polyethylene (PE), Polypropylene (PP), Polyvinyl chloride (PVC), Polyester (PET), and Others), By Type (Thermoformable films, Barrier films, Forming & Non-forming films, and Others), By Application (Blister Packs, Bags, Sachets & Pouches, Tubes, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

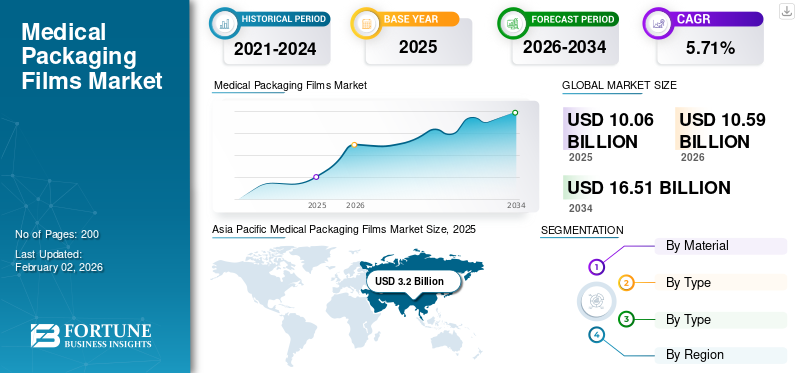

The global medical packaging films market size was valued at USD 10.06 billion in 2025 and is projected to grow from USD 10.59 billion in 2026 to USD 16.51 billion by 2034, exhibiting a CAGR of 5.71% during the forecast period. Asia Pacific dominated the medical packaging films market with a market share of 31.76% in 2025.

The medical packaging films market is an expanding and divided sector consisting of a high-value, technically demanding segment, and a high-volume, price-sensitive segment. Recent forecasts indicate that the overall films market is expected to grow rapidly over the coming decade, fueled by increasing healthcare expenditure, focus on sustainability, a rise in disposable medical devices, and heightened production of biologics.

The market encompasses several major players Amcor, Klöckner Pentaplast, and Wipak Group at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Medical Packaging Films Market Takeaways

- 2025 Market Size: USD 10.06 Billion

- 2026 Market Size: USD 10.59 Billion

- 2034 Forecast Market Size: USD 16.51 Billion

- CAGR: 5.71% from 2026–2034

- Asia Pacific dominated the medical packaging films market with a 31.76% share in 2025.

- The polyethylene (PE) segment is anticipated to lead the market with a 41.57% share in 2026.

- Thermoformable films are projected to dominate the market with a 46.86% share in 2026.

North America

North America accounted for USD 2.48 billion in 2025 and is expected to grow to USD 2.6 billion in 2026.

Europe

Europe held a market value of USD 2.02 billion in 2025 and is projected to reach USD 2.13 billion in 2026.

Asia Pacific

Asia Pacific generated USD 3.2 billion in 2025 and is projected to reach USD 3.4 billion in 2026.

U.S.

The medical packaging films market is estimated to reach USD 2.05 billion by 2026.

Japan

The market is projected to reach USD 0.64 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Healthcare Expenses and Chronic Diseases Drives Market Growth

The increasing expenses in the healthcare and medical sectors, along with the rising prevalence of chronic illnesses, are fueling the demand for medical packaging film industry. The growing number of pharmaceutical companies has spurred innovations in this area, prompting the packaging sector to advance, which will improve the protection of medications. The expanding aging population has escalated the need for pharmaceutical products, and the increased access to healthcare services is impacting the demand for medical product packaging. Stringent regulations in the pharmaceutical industry have elevated the standards of the packaging sector, established by EMA and FDA, to ensure high quality packaging materials. This is necessary to meet the efficiency and safety requirements needed for medications to preserve their integrity. Henceforth, the growing healthcare expenses and rise of chronic diseases is driving the global medical packaging films market growth.

MARKET RESTRAINTS

High Cost of Advanced Packaging Films Hamper Market Growth

Advanced medical packaging films, which include multi-layer laminates, high-barrier films, and anti-counterfeit features, tend to be more expensive than conventional materials. In budget-conscious markets such as LATAM, Africa, and certain regions of Asia, hospitals and pharmaceutical businesses frequently opt for more affordable, less sophisticated packaging alternatives to reduce expenses. Consequently, the adoption of premium films remains sluggish, even though they offer superior safety and compliance benefits. It thus hinders the global medical packaging films market expansion. Henceforth, the high cost of advanced packaging films hinders the market growth.

MARKET OPPORTUNITIES

Increase in Demand for Sustainable and Biodegradable Films Create Lucrative Growth Opportunities

Sustainable and biodegradable films serve as sustainable alternatives to conventional plastics. They are crafted from renewable resources such as cornstarch or sugarcane and are designed to naturally break down into harmless substances such as water and carbon dioxide. Films created from PLA, starch, PHA, and chitosan are commonly utilized for various food packaging needs, encompassing snacks, fresh produce, and beverages. Biodegradable films provide ecological advantages, including less waste and reduced damage to ecosystems, which complements the growing consumer preference for sustainable packaging options. Thus, there is a growing demand for biodegradable and sustainable films, which in turn, offers potential growth opportunities.

MARKET CHALLENGES

Strict Regulatory Compliance and Certification Challenges Market Growth

Medical packaging is subject to strict regulations due to its direct influence on patient safety. Packaging films are required to adhere to the standards set by the US FDA (21 CFR), EU EMA, ISO 11607, USP guidelines, and local health authorities. These films must complete rigorous stability, sterilization, and migration testing prior to being approved. Adhering to these regulations increases research and development costs, extends certification timelines, and adds complexity to operations, particularly for smaller manufacturers. Henceforth, stringent regulatory compliances and certifications thus poses a challenge to the market development.

MEDICAL PACKAGING FILMS MARKET TRENDS

Growing Innovations in Packaging Films Booms as a Market Trend

Innovation in technology has spurred innovation in medical packaging films and improved the market's potential. Developments such as child-resistant films, ultra-high barrier films, anti-counterfeiting features, and senior-friendly packaging are some examples. Manufacturers are increasingly opting for polyolefin materials over glass for product packaging. Leading companies in the market are dedicated to safeguarding both patients and the environment concurrently. The majority of pharmaceutical firms are adopting vacuum packaging to maintain the drugs' integrity and prevent contamination.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Remarkable Benefits Offered by Polyethylene Material Boosts Segment Growth

In terms of material, the market is categorized into polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polyester (PET), and others.

The polyethylene (PE) segment captured the largest share of the market in 2024. In 2026, the segment is anticipated to dominate with 41.57% share. Polyethylene (PE) is a preferred choice for medical packaging films due to its outstanding barrier properties, safeguarding against moisture, oxygen, and impurities, essential for preserving the sterility and effectiveness of medical products. Its adaptable nature and flexibility enable it to fit various shapes and sizes for blister packs, sterile wraps, and device packaging. Furthermore, PE provides durability, chemical resistance, and biocompatibility, ensuring the safety of products, evidence against tampering, and compliance with cleanroom standards without endangering the patient's health.

Polypropylene (PP) material segment is expected to grow at a CAGR of 5.62% over the forecast period.

By Type

Thermoformable Films’ High Usage in Medical Sector Propels Segment Growth

In terms of type, the market is categorized into thermoformable films, barrier films, forming & non-forming films, and others. The thermoformable films segment captured the largest medical packaging films market share in 2024. In 2026, the segment is anticipated to dominate with a 46.86% share.

Thermoformable films offer advantages such as outstanding barrier properties, high resistance to punctures and wear, effective sealing, and the ability to create customized shapes for medical devices. These films can be shaped into trays and other structures through heating and pressure application, enabling secure packaging of sterile medical items such as syringes and catheters. Major benefits for medical packaging include preserving product sterility, high performance, compatibility with sterilization techniques, and providing tamper-evidence to improve patient safety.

The barrier films segment is expected to grow at a CAGR of 5.51% over the forecast period.

By Application

Rising Utilization of Bags in Medical Sector Drives Segment’s Growth

Based on application, the market is segmented into blister packs, bags, sachets & pouches, tubes, and others. In 2026, the global market was dominated by bags in terms of application with a market share of 43.46%. Medical packaging bags preserve sterile conditions, shield products from contamination and harm, simplify storage and transportation, and guarantee patient safety with tamper-evident seals. They also protect fragile items such as electronic medical devices from electrostatic discharge (ESD) and safeguard pharmaceuticals from moisture and oxygen, maintaining their potency and effectiveness. Bags are used to transport potentially hazardous biological specimens from hospitals to laboratories, protecting handlers and the environment from contamination.

To know how our report can help streamline your business, Speak to Analyst

In addition, blister packs application is projected to grow at a CAGR of 5.71% during the study period.

Medical Packaging Films Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific Medical Packaging Films Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, Asia Pacific generated USD 3.2 billion, contributing 31.76% to global market revenue, and is projected to grow to USD 3.4 billion in 2026. The region is emerging as a central hub for generic medications and biosimilars, with India and China at the forefront of exports. Pharmaceutical firms depend on multi-layer barrier films to maintain drug stability, extend shelf life, and meet export regulations. There is a growing demand for cold chain packaging films for biologics, vaccines, and drugs that require temperature control. The Japan market is projected to reach USD 0.64 billion by 2026, the China market is projected to reach USD 1.11 billion by 2026, and the India market is projected to reach USD 0.92 billion by 2026.

North America

The North America region captured 24.65% of the global market in 2025, generating USD 2.48 billion in revenue, and is projected to reach USD 2.6 billion in 2026. North America and Europe are anticipated to witness a notable growth in the coming years. During the forecast period, North America is projected to record the growth rate of 5.29%, which is the second highest amongst all the regions and touch the valuation of USD 2.48 billion in 2025. The U.S. holds the position of being the largest pharmaceutical market globally; the segments for biologics, biosimilars, and specialty medications are experiencing significant growth. Films used in medical packaging are essential for maintaining drug stability, prolonging shelf life, and adhering to FDA regulations. There is a strong demand for cold chain packaging films, driven by the expansion in biologics, cell therapies, and mRNA vaccines. In 2026, the U.S. market is estimated to reach USD 2.05 billion.

Europe

Europe maintained a strong presence in the global market, reaching USD 2.02 billion in 2025, accounting for 20.11% share, and is expected to reach USD 2.13 billion in 2026. Europe is home to one of the oldest populations in the world; the growing incidence of cardiovascular diseases, diabetes, cancer, and neurological disorders leads to increased long-term use of medications. The need for secure medication packaging, IV bags, diagnostic tools, and single-use medical devices directly supports the demand for packaging films.

Backed by these factors, the UK is anticipated to record a market valuation of USD 0.41 billion in 2026, while Germany is expected to reach USD 0.47 billion in the same year, and France to record USD 0.30 billion in 2025.

Latin America

The Latin America market generated USD 1.46 billion in 2025, representing 14.56% of the global market landscape, and is expected to reach USD 1.53 billion in 2026. Brazil, Mexico, and Argentina are focusing on updating their hospitals and enhancing healthcare accessibility. This increased investment leads to a higher demand for sterile medical packaging films utilized in intravenous bags, syringes, surgical kits, and diagnostic equipment, driving market expansion.

Middle East & Africa

Middle East & Africa recorded a market size of USD 0.9 billion in 2025, capturing 8.92% of the global market share, and is projected to reach USD 0.93 billion in 2026. Moreover, global pharmaceutical corporations in the Middle East & Africa are establishing local packaging and distribution facilities, which is driving a significant demand for multi-layer barrier films that comply with international standards.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings coupled with Strong Distribution Network of Key Companies Supported their Leading Position

The global medical packaging films market showcases a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Amcor, Klöckner Pentaplast, Wipak Group are some of the dominating players in the market. A comprehensive range of medical packaging films products, global presence through a strong distribution network, and collaborations with research and academic institutes are few characteristics of these key players which support their dominance.

Apart from this, other prominent players in the market include Sealed Air, Constantia Flexibles, and Honeywell International, Inc. These companies are undertaking various strategic initiatives such as investments in R&D and partnerships with pharmaceutical companies to enhance their market presence.

LIST OF KEY MEDICAL PACKAGING FILMS COMPANIES PROFILED

- Amcor (Netherlands)

- Klöckner Pentaplast (Netherlands)

- Wipak Group (Netherlands)

- Sealed Air (Netherlands)

- Constantia Flexibles (Netherlands)

- Honeywell International, Inc. (Netherlands)

- Spectrum Plastics Group (Netherlands)

- DuPont de Nemours, Inc. (Netherlands)

- Uflex Limited (Netherlands)

- Coveris Holdings (Netherlands)

- 3M Company (Netherlands)

- West Pharmaceutical Services (Netherlands)

- Perlen Packaging AG (Netherlands)

- ACG (Netherlands)

- Dunmore (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Coveris, a prominent manufacturer of medical packaging, introduced a new recyclable thermoforming film called Formpeel P at the COMPAMED exhibition in Düsseldorf. Formpeel P joins Coveris' range of sustainable materials, which already features Formpeel T, Flexopeel T, and Cleerpeel, and offers equivalent functionality and safety to conventional materials, all while reducing both flexible packaging and product waste.

- April 2025: Amcor announced the completion of its state-of-the-art coating facility for healthcare packaging located in Selangor, Malaysia. This new facility is a component of Amcor's larger strategy to enhance its healthcare offerings in the Asia Pacific area. Recent efforts include the purchase of healthcare packaging firm MDK in China, the creation of a grid lacquer paper unit in India, and the establishment of a co-extrusion blown film and printing facility in Singapore.

- October 2024: Klöckner Pentaplast (kp), a worldwide leader in environmentally friendly protective packaging, introduced kpNext MDR1, a novel medical device packaging film that broadens its kpNext line beyond pharmaceutical blister films and into the realm of medical devices. This innovative product aims to address the increasing need for sustainable packaging solutions in the healthcare sector.

- March 2024: TOPPAN Inc. and TOPPAN Speciality Films Private Limited (TSF) in India have created GL-SP, a barrier film that features biaxially oriented polypropylene (BOPP) as its substrate, with production and sales set to begin shortly. GL-SP expands the portfolio of sustainable packaging products in the TOPPAN Group’s GL BARRIER1 series of transparent vapor-deposited barrier films, which hold a significant share of the global market.

- January 2020: Aptar CSP Technologies, a pioneer in material science and active packaging solutions that guarantee product protection, prolong shelf life, and enhance user experiences, introduced a groundbreaking active packaging solution that combines oxygen scavenging and moisture absorption. This innovative technology leverages the company’s patented 3-phase Activ-Polymer™ platform incorporated into its Activ-Film™ product design.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.71% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Type, Application, and Region |

|

By Material |

|

|

By Type |

|

|

By Application |

|

|

By Geography |

North America (By Material, Type, Application, and Country)

Europe (By Material, Type, Application, and Country/Sub-region)

Asia Pacific (By Material, Type, Application, and Country/Sub-region)

Latin America (By Material, Type, Application, and Country/Sub-region)

Middle East & Africa (By Material, Type, Application, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 10.06 billion in 2025 and is projected to reach USD 16.51 billion by 2034.

In 2025, the market value stood at USD 3.2 billion.

The market is expected to exhibit a CAGR of 5.71% during the forecast period of 2026-2034.

The bags segment led the market by type.

The key factors driving the market growth is the increasing demand for sustainable packaging.

Amcor, Klockner Pentaplast, Wipak Group, Sealed Air, Constantia Flexibles, and Honeywell International, Inc., are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 in terms of share.

Increase in demand from the medical sectors are some of the factors that are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us