Medical Suction Devices Market Size, Share & Industry Analysis, By Product (Manual Suction Devices, Electric Suction Devices, and Venturi Suction Systems), By Flow Rate (< 20 L/min, 20–40 L/min, 40–60 L/min, and > 60 L/min), By Application (Respiratory Care, Surgical Procedures, Dental Care, Wound Care, and Other), By End-User (Hospitals, Home Care Settings, Dental Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

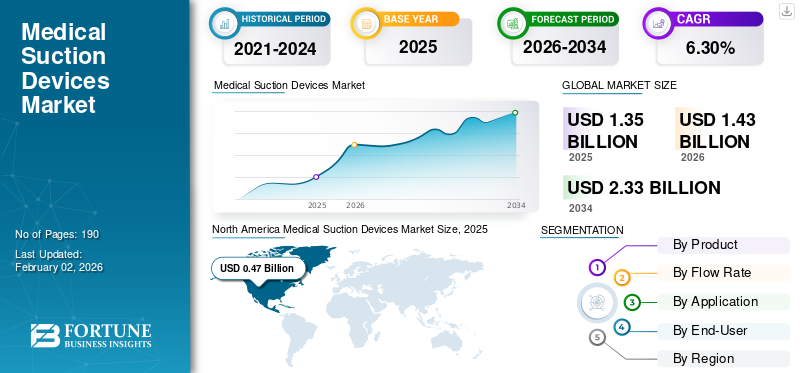

The global medical suction devices market size was valued at USD 1.35 billion in 2025. The market is projected to grow from USD 1.43 billion in 2026 to USD 2.33 billion by 2034, exhibiting a CAGR of 6.30% during the forecast period. North America dominated the medical suction devices market, with a 34.52% share in 2025.

Medical suction devices are used to remove mucus, blood, saliva, and other fluids from a patient’s airway or surgical site, thereby maintaining breathing and ensuring a clear operating field. These devices play a vital role in emergency care, surgical procedures, and home care applications. Market growth is primarily driven by the increasing number of surgical procedures, rising prevalence of chronic respiratory diseases, and growing demand for portable and battery-operated suction systems. Additionally, the adoption of suction devices in home healthcare settings is further boosting market expansion.

Furthermore, the market comprises several major players, including Allied Healthcare Products, Inc., Medela AG, Drive DeVilbiss Healthcare, Precision Medical, and Olympus Corporation, at the forefront. Continuous innovation, coupled with a strong focus on research and development, is helping these companies maintain their strong presence in the global market.

Download Free sample to learn more about this report.

Medical Suction Devices Market Key Takeaways

- 2025 Market Size: USD 1.35 billion

- 2026 Market Size: USD 1.43 billion

- 2034 Forecast Market Size: USD 2.33 billion

- CAGR: 6.30% from 2026–2034

- North America dominated the medical suction devices market with a market share of 34.52% in 2025.

- The electric suction devices segment is projected to dominate the market with a share of 73.64% in 2026.

- The 20–40 L/min segment is projected to dominate the market with a share of 35.01% in 2026.

North America

North America accounted for USD 0.47 billion in 2025 and is projected to reach USD 0.49 billion in 2026, supported by high surgical volumes and continued technological advancements.

Europe

Europe generated USD 0.38 billion in 2025 and is expected to witness steady growth due to standardized procurement practices and increasing focus on infection prevention.

Asia Pacific

Asia Pacific held a 28.40% market share in 2025 and is anticipated to record the fastest growth during the forecast period, driven by expanding healthcare infrastructure and rising medical procedure volumes.

U.S.

The market is estimated to reach USD 0.46 billion in 2026, supported by advanced healthcare facilities, stringent clinical standards, and strong regulatory oversight.

Japan

The market is expected to experience stable growth, supported by increasing adoption of advanced medical devices, a growing elderly population, and demand for high-quality healthcare services.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Surgical Volume and Emergency Care Demand to Propel Market Growth

The growing global burden of surgeries and trauma cases is one of the key factors driving demand for medical suction devices. These systems are widely used in operating rooms, ICUs, and ambulances to ensure airway clearance and patient safety. Moreover, the rising geriatric population, which is prone to respiratory and cardiac conditions, is contributing to the increasing need for suctioning in chronic care management, thereby boosting the global medical suction devices market growth. The availability of portable and wall-mounted suction systems with advanced flow control and low noise further enhances usability across multiple healthcare settings.

- For instance, according to data published in the International Journal of Obesity, in 2021, an estimated 0.6 million bariatric and metabolic surgical procedures were performed globally.

MARKET RESTRAINTS

Significant Cost of Sensors Along with Stringent Reimbursement Policies to Hamper Market Growth

Despite growing demand, the market faces challenges due to high maintenance and calibration costs associated with suction systems. Frequent replacement of filters, tubes, and canisters adds to operational expenses. Moreover, limited reimbursement coverage for suction devices used in homecare settings discourages their adoption, particularly in developing economies. The lack of awareness and training among caregivers regarding device handling and infection control also hinders broader usage.

MARKET OPPORTUNITIES

Technological Integration and Homecare Expansion to Offer Growth Opportunities

The integration of digital monitoring and pressure regulation systems presents new growth opportunities for manufacturers. Advanced models featuring automatic pressure adjustment, overflow protection, and smart battery indicators are improving device efficiency and patient safety. The growing preference for home healthcare and post-surgical rehabilitation is also opening new market opportunities for lightweight and rechargeable suction systems. Companies focusing on user-friendly interfaces and telemonitoring compatibility are expected to gain a competitive edge.

MEDICAL SUCTION DEVICES MARKET TRENDS

Shift Toward Lightweight and Portable Designs for Enhanced Mobility is One of the Prominent Trends

A major trend shaping the market is the increasing preference for lightweight, portable suction devices that deliver reliable vacuum performance in diverse healthcare settings. Manufacturers are emphasizing compact form factors, quiet operation, and multi-power compatibility for improved convenience. Portable suction devices are gaining popularity in homecare, ambulatory services, and field emergency care due to their ease of operation and battery efficiency. Furthermore, there is an ongoing trend toward integrating infection prevention features such as closed-circuit canisters and disposable liners to minimize cross-contamination.

- For instance, in October 2022, Drive DeVilbiss Healthcare Ltd. announced the launch of its new product VacuAide 7325 portable suction unit. The product features a longer battery, specifically designed for use in homecare and hospital settings.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Risk of Cross-Contamination and Device Malfunction to Pose Challenges

One of the major challenges in the market is ensuring device hygiene and reliability during prolonged use. Improper cleaning and reuse of suction tubing or canisters can lead to infection risks. Additionally, inconsistent suction pressure or device malfunction during emergency care can impact treatment outcomes. Manufacturers are focusing on introducing single-use accessories and incorporating safety valves to prevent backflow, but maintaining compliance with international safety standards remains a challenge, particularly in low-resource healthcare systems.

Segmentation Analysis

By Product

Consistent Suction Output and Better Ergonomics Boosted Demand for Electric Suction Devices

On the basis of product, the market is classified into manual suction devices,

electric suction devices, and venturi suction systems.

The electric suction devices segment held the highest global medical suction devices market share in 2024. These systems deliver stable and controllable negative pressure, which is essential in surgical procedures, emergency response, and ICU airway management. They are widely preferred in hospitals as they provide consistent suction output, compared to manual/hand-operated units, which are mainly used as backups. Moreover, other factors, such as the availability of portable and battery-powered models, are also projected to have a positive impact on segment growth. The electric suction devices segment is projected to dominate the market with a share of 73.64% in 2026.

- For instance, in May 2020, Medela LLC announced the opening of a new manufacturing facility in the U.S.

The venturi suction systems segment is expected to rise at a CAGR of 5.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Flow Rate

Wide Range Applications of 20–40 L/min Flow Rate Accelerated Segment Growth

In terms of flow rate, the market is categorized into < 20 L/min, 20–40 L/min, 40–60 L/min, and > 60 L/min.

The 20–40 L/min segment captured the largest market share in 2024. In 2025, the segment dominates with a 35.1% share. This range is widely considered the practical balance between effective fluid evacuation and controlled suction force that does not damage surrounding tissue. Moreover, devices in this range are commonly used in general surgery, airway clearance, wound drainage, and emergency care, making them suitable for most routine hospital procedures. Furthermore, high-flow systems above this range are typically limited to specific high-bleed settings, whereas very low-flow devices are more specialized. The 20–40 L/min segment is projected to dominate the market with a share of 35.01% in 2026.

- The > 60 L/min segment is expected to rise at a CAGR of 7.0% over the forecast period.

By Application

Rise in Trauma Stabilization and Elective Interventions in Aging Patients Fostered Surgical Procedures Segment Growth

In terms of application, the market is categorized into respiratory care, surgical procedures, dental care, wound care, and other.

The surgical procedures segment captured the largest share of the market in 2024. In 2025, the dominates with a 38.6% share. Surgical procedures represent the leading application area for medical suction devices. Suction is required in almost every operating room to maintain a clear visual field by removing blood and fluids from the surgical site. This is critical in high-bleed specialties such as cardiovascular, orthopedic trauma, neurosurgery, and abdominal surgery. Also, a steady rise in global surgical volume, including trauma stabilization and elective interventions in aging patients, directly supports recurring demand for reliable suction systems in the OR. The surgical procedures segment is expected to lead the market, contributing 38.63% globally in 2026.

- For instance, in February 2023, NCBI published that the number of knee arthroplasty in the U.S. are expected to reach 3.48 million by 2030.

The wound care segment is expected to rise at a CAGR of 7.2% over the forecast period.

By End-User

High Volume of Surgical Procedures in Hospitals Boosted Segment Growth

Based on end-user, the market is segmented into hospitals, home care settings, dental clinics, and others.

In 2024, the hospitals segment dominated the global market. Hospitals require suction in operating rooms, ICUs, emergency departments, step-down units, and respiratory care wards, resulting in high unit density per facility. Hospitals also purchase both wall-mounted suction (central vacuum systems) and portable/battery-operated suction pumps for bedside and transport use. The hospitals segment is expected to account for 48.71% of the market in 2026.

In addition, the dental clinic segment is projected to rise at a CAGR of 5.5% during the study period.

Medical Suction Devices Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Suction Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 34.52% of the global market share, reaching a valuation of USD 0.47 billion, and is projected to grow to USD 0.49 billion in 2026. The factors fostering the dominance of the region include a considerable number of surgical procedures, technological advancements, and product approvals. The U.S. market is estimated to reach USD 0.46 billion in 2026. Certain factors such as high surgical volume, strict clinical and regulatory standards, and consolidated healthcare infrastructure, are expected to drive market growth in the U.S.

- For instance, in November 2022, EXSALTA received FDA approval for its new peristaltic pump.

Europe

The market in Europe reached USD 0.38 billion in 2025, representing 27.87% of total market revenue, and is projected to reach USD 0.39 billion in 2026. Europe is projected to witness notable growth in the coming years. During the forecast period, the Europe region is projected to record a growth rate of 5.2% and reach a valuation of USD 0.38 billion by 2025. This is primarily due to the standardization of procurement and a focus on infection prevention. Backed by these factors, countries including U.K., Germany are anticipated to record the valuation of USD 0.06 billion, USD 0.09 billion in 2026, and France market is estimated to reach USD 0.05 billion, respectively, in 2025.

Asia Pacific

Asia Pacific contributed approximately USD 0.38 billion to the global market in 2025, accounting for 28.40% share, and is expected to reach USD 0.41 billion in 2026. Asia Pacific is expected to exhibit the fastest CAGR during the forecast period. The market in Asia Pacific is estimated to reach USD 0.38 billion in 2026. In the region, India and China are estimated to reach USD 0.09 billion and USD 0.14 billion, respectively in 2026.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth over the forecast period. In 2025, Latin America generated USD 0.05 billion, contributing 3.58% to global market revenue, and is projected to grow to USD 0.05 billion in 2026. The consolidation of healthcare infrastructure, coupled with extensive investments in superior healthcare facilities, is further estimated to drive regional growth during the forecast period. In the Middle East & Africa, the GCC is set to reach a value of USD 0.02 billion in 2025. The Middle East & Africa region captured 5.64% of the global market in 2025, generating USD 0.08 billion in revenue, and is projected to reach USD 0.08 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Focus on Product Performance and Infection Control to Help Companies Maintain their Market Positions

The global medical suction devices market exhibits a semi-concentrated structure, comprising a mix of established manufacturers and several mid-sized companies that focus on specific settings, such as hospital OR/ICU use, EMS/transport, and homecare suction. Top producers of medical suction devices consistently focus on product performance, portability, infection control, and regulatory compliance to maintain or expand their market position.

Medela AG, Drive DeVilbiss Healthcare, Precision Medical, and Olympus Corporation are among the leading players in the market. Key manufacturers of medical suction devices benefit from a broad suction product portfolio, strong hospital relationships, and ongoing product improvements, including quieter operation, controlled vacuum range, closed-canister fluid management, and battery-backed mobility.

In addition to these companies, other notable participants include Allied Healthcare Products, Inc., ATMOS MedizinTechnik, Laerdal Medical, Integra LifeSciences (with its Codman surgical suction/irrigation portfolios), and Teleflex Incorporated. These players are focusing on targeted strategies, such as expanding airway suction solutions for emergency response units, offering compact suction devices for home respiratory patients, and supplying specialty suction tools for neurosurgery and ENT procedures.

LIST OF KEY MEDICAL SUCTION DEVICE COMPANIES PROFILED

- Medela AG (Switzerland)

- Drive DeVilbiss Healthcare LLC (U.S.)

- Precision Medical, Inc. (U.S.)

- Allied Healthcare Products, Inc. (U.S.)

- Laerdal Medical AS (Norway)

- ATMOS MedizinTechnik GmbH & Co. KG (Germany)

- Welch Allyn, Inc. (U.S.)

- Olympus Corporation (Japan)

- ZOLL Medical Corporation (U.S.)

- Smiths Medical (U.K.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: SC Launch Inc. invested USD 200,000 in VayuClear, Inc. to scale the VORTEX Surgical Suction Clearing System nationally. The device rapidly clears clogged suction tips and suction lines in the OR in seconds, reducing delay, fluid exposure, and anesthesia time.

- June 2024: Medical University of South Carolina (MUSC) announced that the VORTEX Surgical Suction Clearing System by VayuClear is now ready for national rollout after pilot use in lumbar procedures.

- November 2021: Drive DeVilbiss Healthcare announced a partnership with BILT Intelligent Instructions to provide interactive 3D setup and service guidance for its home medical equipment line. The goal was to improve the correct assembly and safe use of portable respiratory/suction devices in post-acute and home settings.

- Aug 2020: Premier Inc. entered into a strategic collaboration with Medela AG for the supply of suction devices.

- May 2020: Medela AG announced the opening of a new production line in the U.S. The production is expected to increase by 10,000 units.

REPORT COVERAGE

The global medical suction devices market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.30% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Product · Manual Suction Devices · Electric Suction Devices · Venturi Suction Systems By Flow Rate · < 20 L/min · 20–40 L/min · 40–60 L/min · > 60 L/min By Application · Respiratory Care · Surgical Procedures · Dental Care · Wound Care · Other By End-User · Hospitals · Home Care Settings · Dental Clinics · Others By Region · North America (By Product, Flow Rate, Application, End-User, and Country) o U.S. § By Product o Canada § By Product · Europe (By Product, Flow Rate, Application, End-User, and Country/Sub-region) o Germany § By Product o U.K. § By Product o France § By Product o Spain § By Product o Italy § By Product o Scandinavia § By Product o Rest of Europe § By Product · Asia Pacific (By Product, Flow Rate, Application, End-User, and Country/Sub-region) o China § By Product o Japan § By Product o India § By Product o Australia § By Product o Southeast Asia § By Product o Rest of Asia Pacific § By Product · Latin America (By Product, Flow Rate, Application, End-User, and Country/Sub-region) o Brazil § By Product o Mexico § By Product o Rest of Latin America § By Product · Middle East & Africa (By Product, Flow Rate, Application, End-User, and Country/Sub-region) o GCC § By Product o South Africa § By Product o Rest of Middle East & Africa § By Product |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.35 billion in 2025 and is projected to reach USD 2.33 billion by 2034.

In 2025, the market value stood at USD 0.47 billion.

The market is expected to exhibit a CAGR of 6.30% during the forecast period of 2026-2034.

In 2025, the electric suction devices segment led the market by product type.

Rising surgical volume and emergency care demand to propel market growth.

Medela AG, Drive DeVilbiss Healthcare, Precision Medical, and Olympus Corporation are some of the prominent players in the market.

North America dominated the market with a share of 34.52% in 2025.

A rising number of surgical procedures, coupled with technological advancements in medical suction devices, is favoring product adoption.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us