Megawatt Charging System Market Size, Share & Industry Analysis, By Component (Charging Hardware, Software & Energy Management Systems, and Installation, & Others), By Vehicle Type (Heavy-Duty Trucks, Medium-Duty Trucks, Electric Buses & Coaches, and Off-Highway & Industrial Vehicles), By End User (Fleet Operators & Logistics Companies, Public Transport Authorities, & Others), By Charging Configuration (Single-Output MCS Chargers, Multi-Output/Dispenser-Based MCS Systems, & Others), By Charger Power Output (1.0-1.5 MW, 1.5-2.0 MW, and Above 2.0 MW), and Regional Forecast, 2026-2034

Megawatt Charging System Market Size and Future Outlook

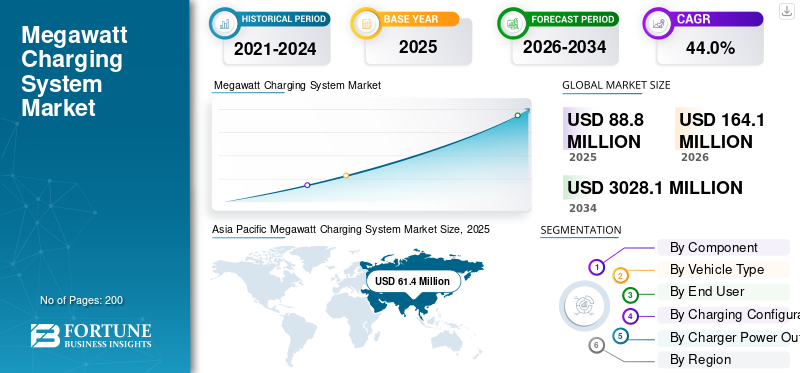

The global megawatt charging system market size was valued at USD 88.8 million in 2025. The market is projected to grow from USD 164.1 million in 2026 to USD 3,028.1 million by 2034, exhibiting a CAGR of 44.0% during the forecast period. Asia Pacific dominated the megawatt charging system market with a market share of 69.14% in 2025.

The megawatt charging system is a high-power electric vehicle charging standard enabling ultra-fast charging for heavy-duty electric trucks, buses, and commercial vehicles using megawatt-level direct current power. Market drivers include rising electric commercial vehicle adoption, demand for fast charging infrastructure, stricter emission regulations, fleet electrification initiatives, and advancements in high-power charging technologies supporting long-haul operations.

Major players in the megawatt charging system market include ABB, Siemens, Schneider Electric, Bosch Rexroth, Phoenix Contact, Alpitronic, and Tritium, competing through ultra-high-power charging solutions, grid integration, standardization, and reliability-focused designs.

Download Free sample to learn more about this report.

MEGAWATT CHARGING SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 88.8 million

- 2026 Market Size: USD 164.1 million

- 2034 Forecast Market Size: USD 3,028.1 million

- CAGR: 44.00% from 2026–2034

- Asia Pacific dominated the market with a 69.14% share in 2025.

- The Charging Hardware segment is projected to account for the largest market share in 2026.

- The Heavy-Duty Trucks segment is expected to hold the largest market share in 2026.

Asia Pacific

Dominated the market, driven by rapid heavy-duty EV adoption and charging infrastructure expansion.

Europe

Growing due to stringent emission regulations and freight corridor electrification.

North America

Driven by commercial fleet electrification and charging infrastructure investments.

U.S.

Witnessing strong growth with increasing megawatt charging deployments for electric freight fleets.

Japan

Growing with OEM-led innovation and early adoption of megawatt charging technology.

Read More

MEGAWATT CHARGING SYSTEM MARKET TRENDS

Standardization and Interoperability Boost High-Power Charging Adoption

One of the key megawatt charging system market trends includes standardization and interoperability across chargers, vehicles, and grid interfaces. Industry collaboration through global standards bodies enables cross-OEM compatibility, reducing infrastructure risk. Unified protocols simplify deployment for fleet operators, encourage multi-vendor ecosystems, and support international corridor charging. This trend improves scalability, lowers total ownership costs, and accelerates the adoption of megawatt-level charging for heavy-duty electric trucks, buses, and industrial vehicles.

- For instance, in January 2026, Keysight Technologies launched advanced high-power and megawatt charging test solutions, including the SL2600A Megawatt Charging Discovery System supporting up to 1,500 V/1,500 A and the scalable SL1047A, accelerating development and standards-compliant validation for next-generation EV and heavy-duty charging infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Fleet Electrification Policies to Accelerate Charging Infrastructure Adoption

Fleet electrification policies and emission reduction targets are a primary driver for the market. Governments and corporations are transitioning heavy-duty truck fleets to electric power to meet sustainability goals. This shift drives megawatt charging system market demand for ultra-fast charging that minimizes downtime and maximizes vehicle utilization. Large logistics hubs, ports, and transit operators increasingly invest in megawatt chargers to support continuous operations, long-haul routes, and scalable fleet expansion worldwide across emerging and developed economies.

- For instance, in February 2026, Xos launched its 2026 Electric Class 6 chassis starting at USD 99,000, featuring a 23,000 lb GVWR platform, up to 200 miles of range on extended variants, an LFP battery with more than 4,000 cycle durability, and advanced telematics with OTA updates for continuous performance optimization.

MARKET RESTRAINTS

High Infrastructure Investment and Grid Upgrade Requirements to Restrict Product Adoption

High upfront infrastructure investment is a major factor restraining the megawatt charging system market growth. Deploying megawatt chargers requires grid upgrades, substations, advanced cooling, and energy management systems. These capital-intensive requirements increase project complexity and lengthen payback periods. As a result, smaller fleet operators and players in developing regions may delay adoption due to financing constraints. As a result, market growth is likely to be uneven across regions despite strong long-term electrification and decarbonization objectives, limiting short-term growth visibility for stakeholders during the study period.

MARKET OPPORTUNITIES

Renewable Energy and Storage Integration to Create Long-Term Growth Opportunities

Integration of renewable energy and on-site storage presents a strong opportunity in the market. Combining megawatt chargers with solar, wind, and battery systems reduces grid dependence and energy costs. This integrated approach also enhances charging reliability and sustainability for fleet depots and logistics centers. It also supports smarter energy optimization, enabling operators to manage peak loads efficiently while improving long-term return on infrastructure investments across diverse applications during the forecast period, supporting the sustainable megawatt charging system market globally.

- For instance, in January 2025, the U.S. Department of Energy (DOE) committed USD 68 million to the SuperTruck Charge initiative, funding high-power EV charging sites near ports, hubs, and corridors. Projects include MCS chargers with up to 10+ MW power, 3 MW battery energy storage, and 9 MW concurrent charging designs, enhancing grid resiliency and scalable heavy-duty charging infrastructure for long-haul electric fleets.

MARKET CHALLENGES

Grid Stability Management to Hinder Market Growth

Managing grid stability is a critical challenge as market deployment scales. Simultaneous charging of multiple heavy-duty vehicles creates high peak loads and power quality risks. Utilities and operators must coordinate closely to implement smart charging, load balancing, and energy storage solutions. These technical requirements add operational complexity and require advanced planning to ensure reliable charging without disrupting local electricity networks as demand rises and market adoption accelerates across regions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Installed Base Expansion and Infrastructure Rollouts Drive Charging Hardware Segment Growth

By component, the market is segmented into charging hardware, software & energy management systems, and installation, commissioning & services.

The charging hardware segment dominates the market due to the critical need for physical ultra-high-power chargers across fleet depots, logistics hubs, highways, and ports. Large-scale deployment of heavy-duty electric trucks and buses requires reliable, standardized, and high-capacity charging equipment. Fleet operations prioritize robust hardware investments to ensure operational uptime, safety, and long-term performance. Ongoing public and private infrastructure rollouts, coupled with early-stage market penetration, sustain strong demand for hardware installations and replacement across regions.

- For instance, in January 2026, Wattev Energy doubled its charging network capacity by adding megawatt-class chargers capable of up to 1 MW output. The company expanded its footprint across key logistics corridors and enhanced fast charging access for heavy-duty electric fleets to reduce downtime.

The software and energy management systems segment is the fastest-growing, expanding at a CAGR of 48.9% over the forecast period. Rising focus on smart charging, load balancing, grid optimization, and energy cost management drives rapid adoption of digital platforms supporting megawatt-level charging infrastructure.

By Vehicle Type

Long-Haul Electrification and Logistic Operations Boost Heavy-Duty Trucks Segment Growth

Based on vehicle type, the market is segmented into heavy-duty trucks, medium-duty trucks, electric buses & coaches, and off-highway & industrial vehicles.

The heavy-duty trucks segment holds the largest megawatt charging system market share and remains the fastest-growing in the market due to the accelerating electrification of long-haul freight and logistics operations. These vehicles require ultra-fast, high-capacity charging to minimize downtime and maintain route efficiency. Strong regulatory pressure on emissions, growing fleet investments, and pilot-to-commercial scale transitions drive sustained adoption. Large depot-based charging installations and corridor charging networks further reinforce megawatt charging demand from heavy-duty truck operators globally.

- For instance, in October 2025, Orange EV delivered its 500th fully electric heavy-duty yard truck, marking a major milestone in commercial EV adoption; these Class-8 zero-emission trucks serve distribution centers and logistics operations, replacing diesel trucks while cutting emissions and operating costs.

The medium-duty trucks segment represents the second-largest market share, expanding at a CAGR of 41.4% during the forecast period. Growth is supported by urban distribution electrification, regional freight operations, and increasing deployment of scalable megawatt charging solutions.

To know how our report can help streamline your business, Speak to Analyst

By End User

Large-Scale Electrification of Freight Drive Fleet Operators & Logistics Companies Segment Dominance

By end user, the market is divided into fleet operators & logistics companies, public transport authorities, industrial operators, and commercial charging network operators.

Fleet operators and logistics companies dominate the market due to the large-scale electrification of freight, distribution, and long-haul transportation fleets. These end users require ultra-fast charging to maximize vehicle utilization and minimize operational downtime. Centralized depots, predictable routes, and high daily mileage make megawatt charging economically viable. Strong regulatory pressure, sustainability targets, and total cost optimization further reinforce consistent investments in high-capacity charging infrastructure across global logistics networks.

- For instance, in March 2024, Volvo Trucks North America announced the deployment of Volvo VNR Electric trucks for a Southern California drayage program, featuring up to 565 kWh battery capacity, 275-mile range, and DC fast-charging support. This enables small fleet operators to transition toward zero-emission port operations efficiently.

The industrial operators segment is the fastest-growing, expanding at a CAGR of 46.3% over the forecast period. Increasing electrification of mining, ports, construction, and industrial transport fleets is driving demand for high-power, site-specific megawatt charging solutions.

By Charging Configuration

Suitability for Early-Stage Infrastructure Rollouts Support Single-Output MCS Charger Dominance

By charging configuration, the market is categorized into single-output MCS chargers, multi-output/dispenser-based MCS systems, load-sharing/dynamic power MCS systems, and battery-buffered/hybrid MCS systems.

Single-output MCS chargers dominate the market due to their straightforward design, proven reliability, and suitability for early-stage infrastructure rollouts. Fleet operators and depot owners favor these systems for predictable charging patterns, easier installation, and lower system complexity. Single-output configurations efficiently support dedicated truck charging at logistics hubs and transit depots. Their compatibility with current grid capacities and standardized vehicle interfaces reinforces widespread adoption across initial megawatt charging deployments globally.

The load-sharing and dynamic power MCS systems segment is the fastest-growing, registering a CAGR of 48.2% during the forecast period. Rapid growth is driven by increasing demand for smart load management, optimized energy utilization, and simultaneous charging of multiple heavy-duty vehicles.

- For instance, in January 2025, Kempower began pilot deliveries of its megawatt charging system, supporting up to 1.2 MW power, 1,500 A current, and 1,000 V architecture. This enables ultra-fast charging for heavy-duty electric trucks at fleet depots and logistics hubs.

By Charger Power Output

Balanced Power Capacity and Near-Term Compatibility Anchor 1.0–1.5 MW Segment Leadership

By charger power output, the market is segmented into 1.0-1.5 MW, 1.5-2.0 MW, and above 2.0 MW.

The 1.0-1.5 MW segment holds the largest market share, supported by its balance between charging speed and grid compatibility. This power range aligns with current heavy-duty truck battery capacities and depot charging needs, enabling rapid turnaround without extensive grid upgrades. Fleet operators favor these systems for early electrification phases, predictable energy demand, and scalable infrastructure planning, sustaining widespread adoption across logistics hubs and transit depots globally.

The above 2.0 MW segment is the fastest-growing, expanding at a CAGR of 47.5% over the forecast period. Growth is driven by next-generation heavy-duty vehicles, ultra-fast turnaround requirements, and advancing grid and power electronics capabilities.

- For instance, in January 2026, BYD showcased its 1 MW megawatt fast-charging system, demonstrating the ability to add up to 400 km range in five minutes using high-voltage architecture and advanced thermal management, highlighting next-generation ultra-fast charging capabilities for heavy-duty electric vehicles.

Megawatt Charging System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Megawatt Charging System Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing market, driven by aggressive electrification of heavy-duty trucks, strong government support, and rapid infrastructure investments. China leads deployment through large-scale pilot corridors, port electrification, and state-backed grid expansion. Japan and South Korea support adoption via technology standardization and OEM-led initiatives. Rising logistics demand, manufacturing dominance, and favorable policies accelerate market growth, positioning the region as the primary contributor to global megawatt charging system market expansion.

- For instance, in January 2025, BYD unveiled its Super e-Platform with Megawatt Flash Charging, enabling up to 1 MW charging power, 1,000-volt architecture, and refueling speeds. This allows electric vehicles to achieve ultra-fast energy replenishment comparable to conventional fuel stops.

China Megawatt Charging System Market

The market in China in 2026 is estimated at around USD 106.1 million, accounting for roughly 64.7% of global revenues, driven by large-scale truck electrification, corridor pilots, and government-backed charging infrastructure expansion.

Japan Megawatt Charging System Market

The Japanese market in 2026 is estimated at around USD 3.4 million, accounting for roughly 2.1% of global revenues, supported by OEM-led standardization, technology innovation, and early deployment across logistics and industrial fleets.

India Megawatt Charging System Market

The Indian market in 2026 is estimated at around USD 2.2 million, accounting for roughly 1.3% of global revenues, fueled by rapid fleet electrification, logistics growth, policy incentives, and expanding pilot charging infrastructure.

Europe

Europe represents the second-largest megawatt charging system market, expanding at a CAGR of 43.0% during the forecast period. Stringent emission regulations, carbon neutrality targets, and strong public-private partnerships drive infrastructure rollout. The region focuses on highway freight corridors, depot charging, and cross-border interoperability. Leading truck OEMs and charging solution providers actively pilot megawatt systems. Well-developed grids, renewable integration, and regulatory clarity sustain steady market growth across Western and Northern European economies.

- For instance, in November 2025, a EUR 10 million (USD 11.8 million) European project was launched to support megawatt charging deployment, focusing on MCS-ready infrastructure, 1 to 3 MW charging capacity, grid integration, and cross-border freight corridors to accelerate heavy-duty electric vehicle adoption across the region.

Germany Megawatt Charging System Market

The German market in 2026 is estimated at around USD 3.4 million, accounting for roughly 2.1% of global revenues, driven by stringent emission regulations, freight corridor electrification, and strong OEM–utility collaborations.

U.K. Megawatt Charging System Market

The U.K. market in 2026 is estimated at around USD 2.1 million, accounting for roughly 1.3% of global revenues, supported by net-zero targets, depot charging investments, and commercial fleet electrification initiatives.

North America

North America holds the third-largest share of the market, supported by growing electrification of freight corridors and commercial fleets. The U.S. leads regional adoption through federal incentives, utility-backed charging programs, and private logistics investments. Fleet operators prioritize depot-based megawatt charging to reduce downtime. While grid upgrade timelines remain a consideration, strong technology innovation, OEM participation, and infrastructure funding support consistent market growth across logistics, ports, and industrial transport segments.

- For instance, in January 2026, Wattev doubled capacity at its San Bernardino electric truck charging depot, adding megawatt chargers delivering up to 1 MW, enabling simultaneous heavy-duty truck charging, reducing turnaround times, and scalable support for high-utilization electric freight operations.

U.S. Megawatt Charging System Market

The U.S. market in 2026 is estimated at around USD 9.7 million, accounting for roughly 5.9% of global revenues, driven by federal incentives, freight corridor pilots, utility partnerships, and large fleet electrification programs.

Rest of the World

The Rest of the World market shows gradual growth in the market, led by early adoption in the Middle East, Latin America, and select African regions. Growth is driven by port electrification, mining operations, and pilot freight projects. Infrastructure development remains selective due to grid limitations and capital constraints. However, rising sustainability commitments, renewable energy integration, and international partnerships create long-term growth potential across emerging logistics and industrial hubs.

- For instance, in February 2025, Al-Futtaim BYD UAE launched Megawatt Flash Charging technology in the region, supporting up to 1 MW charging power, 1,000-volt architecture, and ultra-fast energy replenishment, accelerating heavy-duty EV adoption and supporting the UAE’s net-zero transportation ambitions.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Partnership to Support Electrified Heavy Equipment Operations

The megawatt charging system market is moderately fragmented, with global power and charging specialists competing alongside emerging technology providers. Key players, including ABB, Siemens, Schneider Electric, Bosch Rexroth, Phoenix Contact, Alpitronic, and Tritium, compete through ultra-high-power charger efficiency, grid integration capabilities, and compliance with evolving MCS standards. Companies focus on modular hardware, intelligent energy management software, and utility partnerships. Strategic collaborations, pilot corridor projects, and localized manufacturing strengthen the market positioning of these companies. In October 2025, ABB launched a modular megawatt charger platform supporting dynamic load management and scalable depot deployments globally.

- For instance, in February 2026, Komatsu and Dimaag unveiled a mobile Megawatt Charging System for remote construction and mining sites. This delivers up to 1 MW charging power, a containerized design, and off-grid compatibility to support electrified heavy equipment operations.

LIST OF KEY MEGAWATT CHARGING SYSTEM COMPANIES PROFILED

- ABB (Switzerland)

- Siemens (Germany)

- Schneider Electric (France)

- Delta Electronics (Taiwan)

- Kempower (Finland)

- Alpitronic (Italy)

- Phoenix Contact (Germany)

- Stäubli (Switzerland)

- Tritium (Australia)

- Eaton (U.S.)

- Bosch Rexroth (Germany)

- ChargePoint (U.S.)

- Tesla (U.S.)

- Heliox (Netherlands)

- CharIN e.V. (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Tesla began pilot deployment of Semi Megachargers, designed for megawatt-class output, enabling rapid charging of Tesla Semi trucks to support long-haul freight electrification and high-utilization logistics operations.

- January 2026: ChargePoint introduced its Megawatt Charging System, supporting up to 1.2 MW, dynamic power allocation, and fleet-focused software integration. This targets depot and corridor charging for heavy-duty electric trucks and commercial fleets.

- January 2026: Kempower powered Plugit’s first public MCS charging stations in Kotka, Finland, delivering up to 1.2 MW output, 1,500 A current, and dynamic power distribution. This supports ultra-fast charging for heavy-duty electric trucks through a new sales and service partnership.

- October 2025: Siemens unveiled SICHARGE Flex, a next-generation EV charging system supporting up to 1 MW, modular power cabinets, dynamic load sharing, and grid-ready architecture, designed to scale megawatt charging across heavy-duty and mixed-use applications.

- June 2025: Scania demonstrated megawatt charging system technology at EVS38, validating MCS connector interfaces, high-current charging, and interoperability aligned with heavy-duty electric truck production roadmaps.

- April 2025: IONITY became the first network to procure Alpitronic’s HYC1000, a 1 MW megawatt charging system, supporting 1,000 V platforms, scalable modules, and future heavy-duty electric truck corridor deployment across Europe.

- February 2025: Alpitronic launched the HYC1000 megawatt charger, delivering up to 1 MW output, 1,000 V DC, liquid-cooled cables, and modular power stacks. This enables ultra-fast charging for next-generation heavy-duty electric vehicles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 44.0% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Component, By Vehicle Type, By End User, By Charging Configuration, By Charger Power Output, and By Region |

| By Component |

|

| By Vehicle Type |

|

| By End User |

|

| By Charging Configuration |

|

| By Charger Power Output |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 88.8 million in 2025 and is projected to reach USD 3,028.1 million by 2034.

In 2025, the Asia Pacific market value stood at USD 61.4 million.

The market is expected to exhibit a CAGR of 44.0% during the forecast period (2026-2034).

In terms of vehicle type, the heavy-duty trucks segment leads the market.

Fleet electrification policies are the key factor driving the market.

Key players in the market include ABB, Siemens, Schneider Electric, Bosch Rexroth, Phoenix Contact, Alpitronic, and Tritium.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us