Micro-Mobility Market Size, Share & Industry Analysis, By Propulsion Type (Electric and Manual /Human-Powered), By Vehicle Type (E-Scooters, E-Bikes, Bicycles and Light Electric Mopeds), By Speed Category (Low-Speed (<25 km/h), Mid-Speed (25–45 km/h), and Ultra-Low-Speed (<10 km/h)), By End-User (Individual Consumers and Enterprises), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

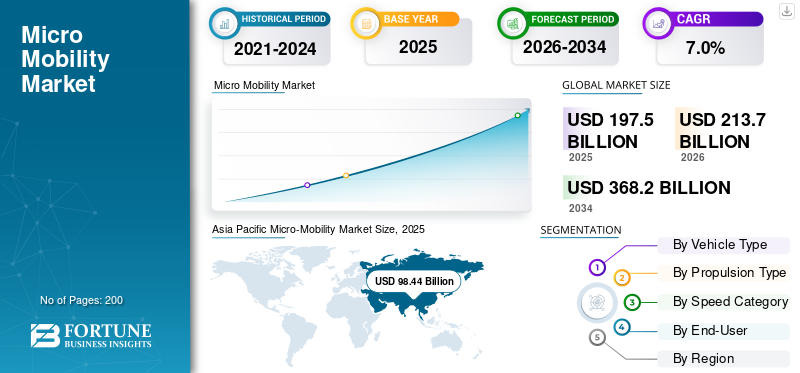

Micro-Mobility Market Size and Future Outlook

The global micro-mobility market size was valued at USD 197.50 billion in 2025. The market is projected to grow from USD 213.70 billion in 2026 to USD 368.20 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. Asia Pacific dominated the global micro-mobility market with a market share of 49.8% in 2025.

The micro-mobility market refers to the ecosystem of lightweight, low-speed transportation solutions designed for short-distance travel, urban, and suburban travel. This includes electric scooters (two-wheeled battery-powered vehicles), e-bikes (pedal-assisted or fully electric bicycles), electric mopeds (small electric-powered motorcycles), and compact pedal bicycles suitable for trips generally under 10 kilometers. The market encompasses shared mobility platforms, personal-use ownership models, hardware manufacturing, battery systems, charging infrastructure, and supporting digital applications such as fleet management (tools for overseeing vehicle operations) and mobility-as-a-service (MaaS) platforms. Micro-mobility is positioned as an efficient, sustainable, and cost-effective transportation alternative for addressing last-mile connectivity challenges, reducing urban area congestion, and lowering emissions.

The growth of the micro-mobility market is driven by rapid urbanization, increasing traffic congestion, and the rising adoption of eco-friendly transportation modes. Governments worldwide are encouraging low-carbon transit solutions, leading to supportive regulations, dedicated cycling lanes, and infrastructure investments. Consumer preference for affordable and convenient commuting options, especially for last-mile travel, is accelerating demand for shared e-scooter and e-bike services. This development drives the micro-mobility market growth during the forecast period.

The micro-mobility market is characterized by strong competition among global shared mobility operators, vehicle manufacturers, and technology providers. Key market players such as Lime, Bird, Tier Mobility, and Spin dominate the shared e-scooter space through extensive fleets and advanced fleet management systems. Companies such as Giant Bicycles, Yadea, Xiaomi, Segway-Ninebot, and VanMoof contribute significantly through innovative e-bike and scooter manufacturing.

Download Free sample to learn more about this report.

Micro-Mobility MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 197.50 billion

- 2026 Market Size: USD 213.70 billion

- 2034 Forecast Market Size: USD 368.20 billion

- CAGR: 7.0% from 2026–2034

- Asia Pacific dominated the micro-mobility market with a 49.8% share in 2025.

- The e-bikes segment accounted for 11.2% of the market share in 2025.

- Mid-speed (25–45 km/h) segment held the largest share owing to optimal urban commuting efficiency.

North American

North America shows steady growth supported by shared mobility platforms and cycling infrastructure expansion.

Europe

Europe remains a mature market with strong regulatory push for sustainable urban transport.

Asia Pacific

Asia Pacific leads the market, driven by high urban density and strong e-mobility adoption.

U.S.

Growth driven by e-scooter sharing systems and expanding last-mile connectivity demand.

Japan

Strong adoption supported by compact cities and preference for efficient short-distance mobility.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Growth of Shared Mobility Ecosystems Drives Market Growth

The rapid expansion of shared mobility ecosystems is a major catalyst for the micro-mobility market, as cities increasingly integrate e-scooters, e-bikes, and other lightweight vehicles into urban transportation networks. Shared mobility providers are scaling their fleets, improving operational efficiency, and forming strategic partnerships with municipalities to ensure regulatory compliance and expand service coverage. The rise of Mobility-as-a-Service (MaaS) platforms, which unify public transit, micro-mobility, and ride-hailing into a single app-based interface, further enhances accessibility and user convenience. Additionally, advancements in IoT-based fleet tracking, predictive maintenance, and digital payment systems streamline operations and reduce downtime. The increasing consumer shift toward on-demand, flexible transportation options strengthens the adoption of shared micro-mobility solutions across both mature and emerging markets, driving market growth during the forecast period.

MARKET RESTRAINTS

Regulatory Restrictions and Permitting Limits May Hamper Market Growth

Regulatory restrictions and permitting limits represent a major barrier to the expansion of the micro-mobility market. Many cities enforce strict guidelines on fleet size, operational zones, and parking regulations to control congestion, safety risks, and public space misuse. Governments often require operators to obtain costly and highly competitive permits, creating entry barriers and limiting the number of service providers in a region. Additionally, frequent changes in local policies, pilot program uncertainties, and short-term operating licenses create instability for companies planning long-term investments. Restrictions on sidewalk riding, night-time operations, and speed limits further reduce service flexibility and user convenience. Consequently, these regulatory hurdles slow market penetration, complicate scalability, and increase compliance costs for shared micro-mobility operators.

MARKET OPPORTUNITIES

Expansion of Smart City Initiatives to Create Lucrative Growth Opportunities

The expansion of smart city initiatives presents a significant opportunity for the micro-mobility market as governments increasingly prioritize sustainable, data-driven urban private/public transport systems. Cities are investing in digital infrastructure, intelligent traffic management, and multimodal mobility platforms that seamlessly integrate micro-mobility with public transit. These initiatives aim to reduce congestion, lower emissions, and improve last-mile access. For instance, in 2024, cities such as Paris, Singapore, and Los Angeles expanded their Smart Mobility Programs to include sensor-enabled bike lanes, geo-fenced parking zones, and unified Mobility-as-a-Service (MaaS) apps that incorporate e-scooters and e-bikes. Such advancements create a favorable environment for micro-mobility operators by improving safety, operational efficiency, and user convenience, ultimately accelerating adoption across urban transportation networks.

Micro-Mobility MARKET TRENDS

Swappable Battery Technology is One of the Significant Micro-Mobility Market Trends

Swappable battery technology is emerging as a transformative trend in the micro-mobility market, significantly enhancing operational efficiency, fleet uptime, and user convenience. Instead of waiting for vehicles to charge, operators can replace depleted batteries with fully charged units within minutes, reducing downtime and improving service availability. This model also lowers infrastructure costs by minimizing the need for extensive charging stations.

Leading companies are increasingly adopting this approach. For instance, in 2024, Gogoro Inc. and Cycle & Carriage announced they would launch Gogoro battery swapping and Smartscooters in Singapore. The Gogoro Network is a new generation of smart, safe, and dynamic swappable battery refueling for riders, businesses, and communities. In Taiwan, Gogoro has more battery swapping stations than gas stations and supports over 610,000 riders with 1.4 million smart batteries across 12,500 GoStation racks at more than 2,500 locations.

MARKET CHALLENGES

Safety Risks and Accident Concerns are a Challenging Factor for Market Expansion

Safety risks and accident concerns continue to challenge the micro-mobility market. These issues strongly influence regulation and user trust. Many micro-mobility vehicles, especially e-scooters, lack sturdy protective features. Riders are left vulnerable in heavy traffic. Poor rider training, sporadic helmet use, and limited awareness of local rules add to rising accident rates. Road hazards such as potholes, uneven surfaces, and weak lighting make falls and collisions more likely. For example, in 2024, Paris and New York saw a rise in micro-mobility injuries. Authorities responded with tighter speed limits and stricter rules. These safety issues often trigger regulatory scrutiny, restrictions, and lower consumer adoption.

Download Free sample to learn more about this report.

Segmentation Analysis

By Propulsion Type

Growing Adoption of Lithium-Ion Technologies Reinforces Electric Segment Growth

Based on propulsion type, the market is classified into electric and manual/human-powered.

The electric propulsion segment dominates the micro-mobility market, accounting for the largest share due to rising demand for energy-efficient, convenient, and environmentally sustainable transportation solutions. Electric scooters and e-bikes have experienced rapid adoption as advancements in lithium-ion batteries, lightweight materials, and efficient motors improve performance and range. This segment benefits strongly from supportive government policies promoting low-emission transit, including subsidies, tax incentives, and expanding charging infrastructure. Growing consumer preference for effortless and faster commuting options further accelerates adoption. Additionally, shared mobility operators increasingly prioritize electric fleets to reduce operational costs and enhance user experience.

By Vehicle Type

High Utilization Rates Boosted the Bicycles Segment

In terms of vehicle type, the market is categorized into e-scooters, e-bikes, bicycles, and light electric mopeds.

The bicycle segment held the largest micro-mobility market share due to its widespread accessibility, low operational cost, and strong adoption in both emerging and developed regions. Traditional bicycles remain highly preferred for short-distance commuting, fitness activities, and recreational use, supported by expanding cycling infrastructure such as dedicated bike lanes and urban green mobility initiatives. Many cities promote bicycle usage as part of sustainability goals, offering rental programs, public bike sharing systems, and incentives that make bicycles the most widely accepted vehicle type. Their simple design, minimal maintenance requirements, and long lifespan make them cost-effective for operators and consumers. Additionally, the rise in health awareness and the integration of smart bicycle-sharing systems with GPS tracking and mobile apps continue to fuel strong growth in this segment.

To know how our report can help streamline your business, Speak to Analyst

By Speed Category

Superior Speed and Safety Provisions to Drive the Growth of the Mid-Speed Segment

Based on speed category, the market is segmented into Low-Speed (<25 km/h), Mid-Speed (25–45 km/h), and Ultra-Low-Speed (<10 km/h)

The Mid-Speed (25–45 km/h) segment dominates the micro-mobility market due to its optimal balance between speed, safety, and urban usability. Vehicles in this category, primarily e-bikes, e-scooters, and light electric mopeds, offer faster travel times than low-speed options while remaining compliant with most urban mobility regulations. Their ability to cover longer distances efficiently makes them appealing for daily commuters, delivery services, and shared mobility operators. Technological advancements, such as high-capacity lithium-ion batteries and enhanced motor efficiency, have improved performance reliability in this speed range. Additionally, many cities support mid-speed vehicles by expanding bike lanes and allowing regulated operation in dedicated zones. The rising demand for convenient, time-saving, and sustainable mobility solutions continues to strengthen the dominance of the segment.

By End-User

Rising Urban Commuting Requirements Bolster the Individual Consumers Segment Growth

Based on end-user, the market is segmented into individual consumers and enterprises.

The individual consumers segment dominates the micro-mobility market, driven by rising urban commuting requirements, affordability, and growing preference for flexible personal transportation. Consumers increasingly opt for e-bikes, e-scooters, and bicycles as efficient alternatives to cars, especially for short daily trips and last-mile travel. The segment benefits from expanding cycling infrastructure, government incentives for electric mobility, and heightened environmental awareness. Personal ownership models have gained momentum due to improved product reliability, longer battery life, and accessible financing or subscription plans. Additionally, remote work trends and health-conscious lifestyles have increased recreational and fitness-oriented usage. With continuous innovations such as lightweight frames, app-based diagnostics, and enhanced safety features.

Micro-Mobility Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific dominates the global micro-mobility market, supported by rapid urbanization, high population density, and a strong shift toward sustainable, affordable short-distance transportation. Countries such as China, India, Japan, and South Korea are experiencing significant growth due to government-backed initiatives promoting electric mobility, expansion of cycling infrastructure, and rising environmental awareness. China leads the region with large-scale bicycle sharing service programs, extensive e-scooter adoption, and technological leadership in battery manufacturing. India is also witnessing strong uptake driven by congested city environments, rising fuel prices, and increasing acceptance of e-bikes and bicycles for daily commuting. The presence of major manufacturers, favorable regulatory policies, and investments in smart city development further accelerate market expansion.

Asia Pacific Micro-Mobility Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America, Europe, and the Rest of the World (RoW) regions collectively contribute substantially to the global micro-mobility market. North America exhibits strong adoption due to rising demand for eco-friendly urban commuting, widespread deployment of shared e-scooter platforms, and expansion of cycling lanes in major cities such as Los Angeles, Austin, and Toronto. Government support for low-emission transport and a strong culture of recreational cycling further accelerate market growth.

Europe

Europe remains a highly mature market, driven by strict environmental regulations, well-developed cycling infrastructure, and increased use of e-bikes for commuting. Countries such as Germany, the Netherlands, and France lead in both personal ownership and shared mobility usage.

Rest of the World

In the Rest of the World, including Latin America and the Middle East & Africa, growth is emerging gradually due to improving urban infrastructure and rising awareness of affordable mobility options. These regions hold long-term potential as investments in smart urban transport continue to expand.

COMPETITIVE LANDSCAPE

Key Players Focus on Service Portfolios to Improve User Experience

The market is led by established global rental operators and prominent vehicle manufacturers, including Lime, Bird Global, Tier Mobility, Dott, Segway-Ninebot, Giant Manufacturing, Yadea, and Xiaomi. These leaders are expanding their service portfolios through high-performance e-scooters, e-bikes, connected bicycles, and lightweight electric mopeds designed for urban commuting. Companies are increasingly integrating advanced lithium-ion battery systems, swappable battery technology, GPS-enabled tracking, and IoT-based fleet monitoring to improve vehicle uptime and user experience. Strategic partnerships with city authorities, mobility-as-a-service (MaaS) platforms, and battery-swapping network providers are enabling the creation of connected micro-mobility ecosystems that incorporate real-time location analytics, automated maintenance alerts, and remote diagnostics. Their offerings span shared micro-mobility services, personal-use vehicles, smart charging solutions, and digitally managed fleet operations.

Key industry players are adopting AI-driven telematics, cloud-based fleet dashboards, and predictive data analytics to enhance operational efficiency and optimize fleet utilization. Collaborations with technology providers such as AWS, Microsoft Azure, and Google Cloud enable scalable data management, real-time fleet insights, and advanced safety compliance features. Companies are also investing in regional expansions, localized manufacturing, carbon-neutral mobility initiatives, and subscription-based ownership models to strengthen their market position.

LIST OF KEY MICRO-MOBILITY MARKET COMPANIES PROFILED

- Lime (U.S.)

- Bird Global (U.S.)

- Dott (Germany)

- Spin (U.S.)

- Segway‑Ninebot (China)

- Yadea Technology Group (China)

- Giant Manufacturing Co., Ltd. (Taiwan)

- Xiaomi (China)

- Gogoro Inc. (Taiwan)

- VanMoof (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- April 2025- Voi Technology partnered with Wible in Spain to integrate Voi's e-scooters into the Wible multi-modal mobility app, allowing users to access both carsharing and e-scooter services through a single platform. This integration aims to provide a more seamless experience for urban transportation by combining different modes of transport in one app.

- April 2024: Tern launched its very first Bosch-powered e-bikes into the Taiwan market. The Tern Vektron and Tern Quick Haul will be available for sale at local bike shops around the island.

- March 2024: Merida announced the addition of three all-new Shimano EP801-powered bikes to their lineup: a new full carbon eOne-Sixty CF, bigger range alloy eOne-Sixty Lite & versatile aluminium eOne-Forty Lite.

- November 2023 - Giant Group introduced its first throttle-enabled electric bike, the Cito E+. The new model would be released under the company’s Momentum sub-brand of more affordable bikes designed for street, utility, and commuter use. The new Momentum Cito E+ comes with a glovebox.

- August 2022 - Pon Holdings and Porsche announced a joint venture for an e-bike. Porsche eBike Performance GmbH, based near Munich, would develop whole e-bike systems comprising motors, batteries, and software for connectivity. Stuttgart-based P2 eBike would then use these systems to launch a new generation of Porsche eBikes. However, the company also envisions selling third-party bikes.

REPORT COVERAGE

The global micro-mobility market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2025-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Propulsion Type, By Vehicle Type, By Speed Category, By End-User, and By Region |

| By Propulsion Type |

|

| By Vehicle Type |

|

| By Speed Category |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 197.50 billion in 2025 and is projected to reach USD 368.20 billion by 2034.

In 2025, the market value stood at USD 98.44 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period of (2026-2034).

The bicycle segment led the market by vehicle type.

The rising growth of shared mobility ecosystems is the key factor driving market growth.

Asia Pacific dominates the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us