Micromachining Equipment Market Size, Share & Industry Analysis, By Machine Type (Micro-Milling & Micro-Turning, Laser Micromachining, Electrical Discharge Machining (EDM), Electrochemical Machining (ECM), Water Jet Micromachining, Hybrid Micromachining, and Others), By Application (Drilling, Cutting, Surface Structuring, Micro-Welding / Joining, and Marking & Engraving), By End-Use Industry (Semiconductor & Electronics, Medical Devices, Automotive, Aerospace & Defense, Optics & Photonics, Energy & Power, General Manufacturing, and Others), and Regional Forecast, 2026 – 2034

Micromachining Equipment Market Size and Future Outlook

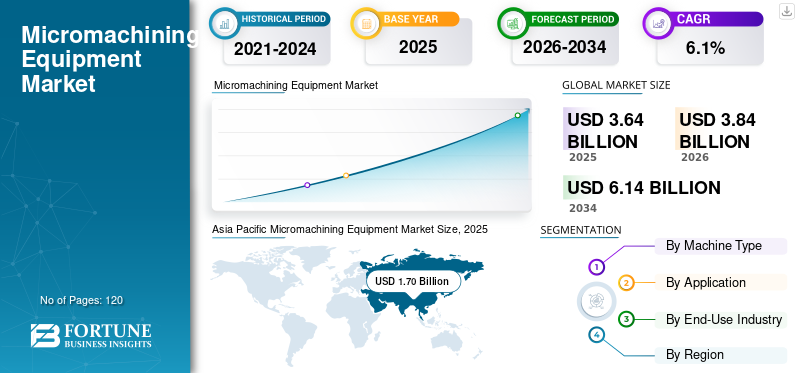

The global micromachining equipment market size was valued at USD 3.64 billion in 2025. The market is projected to grow from USD 3.84 billion in 2026 to USD 6.14 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. Asia Pacific dominated the micromachining equipment market with a market share of 46.70% in 2025.

Micromachining equipment is increasingly being adopted in advanced semiconductor and electronics manufacturing to enable ultra precise material processing with minimal defects and high repeatability. These systems are designed to operate in controlled environments, leveraging ultrafast laser technologies, precision motion systems, and advanced process control to perform micro-drilling, cutting, and surface structuring across critical production stages such as wafer dicing, PCB fabrication, and advanced packaging. The growing complexity of semiconductor architectures, including 3D ICs and heterogeneous integration, is intensifying growing demands and drive the need for highly precise micromachining solutions. The expansion of applications across medical devices and electronics, along with increasing requirements for aerospace components in aerospace and defense, is further accelerating adoption. The expansion of semiconductor fabrication capacity and rising demand for high-density interconnects are supporting precise manufacturing processes that maintain stringent quality and yield standards. Increasing investments in next-generation fabs and the shift toward smart manufacturing are further driving the growth of the market across Asia Pacific, North America, and Europe, where manufacturers are prioritizing high accuracy, scalability, and process optimization.

- For instance, in February 2026, LPKF Laser & Electronics AG introduced advanced laser micromachining systems for PCB and semiconductor applications, featuring enhanced precision and high-speed processing capabilities to support next-generation electronics manufacturing.

TRUMPF Group, Coherent Corp., GF Machining Solutions, LPKF Laser & Electronics AG, and Han’s Laser Technology Industry Group Co., Ltd. are among the key players holding a significant share of the market. Their competitive positioning is strengthened by strong expertise in precision manufacturing technologies, advanced laser and micro-machining capabilities, continuous innovation in high-accuracy processing systems, and strategic collaborations with semiconductor and electronics manufacturers to address evolving miniaturization and performance requirements.

Download Free sample to learn more about this report.

MICROMACHINING EQUIPMENT MARKET TRENDS

Rising Adoption of Ultrafast Lasers and AI-Driven Process Control is Transforming Micromachining Equipment Capabilities

Demand for micromachining equipment is increasingly being shaped by the need for higher precision, reduced thermal impact, and the ability to process complex and advanced materials across semiconductor, medical, and electronics industries. Manufacturers are focusing on deploying ultrafast laser technologies such as femtosecond and picosecond systems combined with AI-driven process control to enhance machining accuracy and surface quality. This shift is enabling the precise structuring of brittle and sensitive materials such as glass, ceramics, and silicon without inducing microcracks or heat-affected zones. Additionally, increasing pressure to achieve higher yields and minimize material waste is driving investments in intelligent micromachining solutions capable of real-time monitoring, adaptive parameter control, and predictive maintenance. Industries are also prioritizing flexible and automated systems that can be seamlessly integrated into high-throughput production lines while supporting scalability for evolving manufacturing requirements. These advancements are reshaping market dynamics as companies transition toward smart manufacturing ecosystems that enhance process efficiency, reduce defects, and improve overall productivity. Equipment manufacturers are responding by developing next-generation micromachining platforms with enhanced precision, faster processing speeds, and advanced digital integration capabilities.

- For instance, in June 2025, TRUMPF Group introduced ultrafast laser micromachining solutions with integrated real-time process monitoring, designed to improve precision and throughput in semiconductor and medical device manufacturing applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Advanced Material Processing and Next-Generation Manufacturing to Drive Market Growth

The micromachining equipment market growth is gaining strong momentum as industries increasingly require precise processing of advanced and difficult-to-machine materials such as silicon carbide, sapphire, ceramics, and composite substrates. The rapid evolution of semiconductor technologies, including advanced packaging, chiplet architectures, and high-density interconnects, is driving the need for ultra-precise micro-scale fabrication processes. Additionally, the expansion of applications in photonics, MEMS, and micro-optics is accelerating demand for high-accuracy surface structuring and micro-patterning solutions. Manufacturers are also focusing on improving process repeatability and reducing defects, leading to increased adoption of systems with integrated monitoring and adaptive control capabilities. The growing shift toward electric vehicles and advanced sensors is further supporting demand for micromachining in battery components and electronic modules. As production environments become more complex and quality-driven, industries are investing in high-performance equipment that enables consistent precision, scalability, and efficient material utilization across high-value manufacturing applications.

- For instance, in April 2025, Coherent Corp. expanded its portfolio of ultrafast laser systems designed for precision micromachining of advanced materials, supporting applications in semiconductor packaging and microelectronics

MARKET RESTRAINTS

Process Sensitivity and Material-Specific Limitations to Challenge Market Adoption

The adoption of micromachining equipment is constrained by the high sensitivity of processes to material properties, environmental conditions, and parameter settings, which can significantly impact output quality and consistency. Variations in material composition, thickness, and thermal behavior often require precise calibration and process optimization, increasing setup time and operational complexity. In applications involving brittle or multi-layered materials, challenges such as microcracks, burr formation, and heat-affected zones can limit process efficiency and yield. Additionally, maintaining consistent performance across different production batches requires advanced control systems and skilled expertise, which may not be readily available in all manufacturing environments. The dependence on highly controlled operating conditions and specialized process knowledge can create barriers for widespread adoption, particularly among smaller manufacturers. These challenges are further amplified in high-volume production settings where even minor deviations can lead to significant quality losses, making process stability and repeatability critical concerns for end users.

MARKET OPPORTUNITIES

Expanding Applications in Advanced Electronics and Medical Microfabrication Creating New Growth Avenues

An emerging opportunity in the market is the increasing demand for advanced semiconductor packaging and high-density interconnect technologies, which require ultra-precise material processing capabilities. As chip architectures evolve toward chiplets, 3D stacking, and heterogeneous integration, manufacturers are relying on micromachining solutions for micro-drilling, via formation, and fine pattern structuring with minimal thermal impact. Additionally, the rapid growth of microelectronics, including sensors, MEMS devices, and compact consumer electronics, is driving the need for high-accuracy and repeatable fabrication processes. The expansion of glass and advanced substrate usage in electronics is further creating demand for non-contact and high-precision laser micromachining systems. Manufacturers are also focusing on developing equipment capable of handling complex geometries and multi-material processing while maintaining throughput and yield. These trends are enabling end users to enhance production capabilities, reduce defects, and support next-generation product development, creating significant growth opportunities across semiconductor and electronics manufacturing ecosystems.

- For instance, in October 2025, LPKF Laser & Electronics AG highlighted 25 years of ProtoLaser innovation, emphasizing continuous development from infrared to picosecond laser systems for precision electronics manufacturing applications.

MARKET CHALLENGES

Process Variability and Precision Sensitivity across Materials Impacting Operational Efficiency

A key challenge in the market is the high sensitivity of machining processes to variations in material properties and operating conditions, which can affect precision and consistency. Different materials such as metals, glass, ceramics, and composites respond differently to machining techniques, requiring precise parameter adjustments to avoid defects such as microcracks, recast layers, or thermal damage. Even minor deviations in process settings can lead to inconsistencies in feature size and surface quality, particularly in high-precision applications. Additionally, maintaining repeatability across large production volumes requires advanced monitoring and control systems, increasing operational complexity. The need for skilled expertise to optimize machining parameters and ensure stable performance further adds to implementation challenges. These factors can impact productivity and limit the ability of manufacturers to achieve consistent output, particularly in applications involving complex geometries and multi-material processing environments.

Segmentation Analysis

By Machine Type

Laser Micromachining Segment Led as it is Most Widely Adopted Technology across High-Precision Manufacturing Applications

By machine type, the market is segmented into micro-milling & micro-turning, laser micromachining, electrical discharge machining (EDM), electrochemical machining (ECM), water jet micromachining, hybrid micromachining, and others.

Laser micromachining held the largest micromachining equipment market share as it represents the most widely adopted and technologically advanced solution for high-precision material processing across industries such as semiconductors, electronics, and medical devices. Laser-based systems are extensively used due to their ability to deliver non-contact, high-speed, and highly accurate machining with minimal thermal impact, making them ideal for processing delicate and advanced materials such as silicon, glass, and ceramics. The demand is particularly strong in semiconductor manufacturing and advanced electronics, where micro-scale drilling, cutting, and structuring are critical for achieving high-density integration and superior product performance. Laser micromachining systems offer greater flexibility and automation capabilities compared to conventional techniques, further supporting their widespread adoption. As industries continue to focus on miniaturization and precision-driven manufacturing, there is increasing integration of laser systems with real-time monitoring and advanced control platforms, enabling improved process stability, higher throughput, and enhanced production efficiency.

- For instance, in July 2025, United Machining SA highlighted advancements in its laser texturing and micromachining capabilities for precision tooling and mold manufacturing applications, supporting high-accuracy surface structuring requirements.

Hybrid micromachining is the fastest-growing segment and is projected to expand at a CAGR of 6.7% over the forecast period. The growth of this segment is driven by the increasing need to combine multiple machining technologies, such as laser with mechanical or EDM processes, to achieve higher precision, improved surface quality, and enhanced processing efficiency.

To know how our report can help streamline your business, Speak to Analyst

By Application

Drilling Segment Led as It Enables High-Precision Micro-Hole Formation across Semiconductor and Electronics Applications

By application, the market is segmented into drilling, cutting, surface structuring, micro-welding / joining, and marking & engraving.

Drilling held the largest share of the market, driven by its critical role in enabling high-precision micro-hole formation across industries such as semiconductors, electronics, and medical devices. Micromachining drilling processes are widely used for applications such as PCB microvia formation, semiconductor wafer processing, and precision component manufacturing, where extremely small and accurate holes are required. These systems allow high-speed, repeatable, and non-contact drilling with minimal material deformation, making them ideal for processing advanced materials including silicon, glass, and composites. The demand is particularly strong in electronics and semiconductor manufacturing, where increasing device miniaturization and higher circuit density require precise and reliable drilling solutions.

Surface structuring is the fastest-growing segment and is projected to expand at a CAGR of 7.0% over the projected period. The growth of this segment is driven by increasing demand for functional surface modification in applications such as micro-optics, medical implants, and advanced electronics. Surface structuring enables precise patterning and texturing at micro scales, improving product performance, enhancing adhesion properties, and enabling advanced functionalities, making it a key area of innovation in micromachining applications.

By End-Use Industry

Semiconductor & Electronics Segment Led as It Represents Largest Demand for High-Precision Microfabrication Applications

By end-use industry, the market is segmented into semiconductor & electronics, medical devices, automotive, aerospace & defense, optics & photonics, energy & power, general manufacturing, and others.

Semiconductor & electronics held the largest share of the micromachining equipment market, driven by the increasing demand for high-precision fabrication processes required in advanced semiconductor devices and electronic components. Micromachining technologies are widely used for applications such as wafer dicing, microvia drilling, thin-film patterning, and precision cutting of substrates, enabling the production of compact and high-performance electronic devices. The demand is particularly strong in semiconductor manufacturing, where shrinking node sizes, increasing circuit density, and the adoption of advanced packaging technologies require extremely accurate and reliable material processing solutions. Additionally, the rapid growth of consumer electronics, communication devices, and high-performance computing systems is further driving the need for micromachining equipment capable of delivering consistent precision and high throughput.

Medical devices is the fastest-growing segment and is projected to expand at a CAGR of 6.3% during the forecast period. The growth of this segment is driven by increasing demand for minimally invasive surgical instruments, implantable devices, and micro-scale components that require extremely high precision and superior surface quality. Micromachining enables the fabrication of complex geometries and fine features in biocompatible materials, supporting innovation and performance improvements in advanced medical technologies.

Micromachining Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Micromachining Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific remains the fastest-growing micromachining equipment market, with revenue valued at USD 1.70 billion in 2025. Asia Pacific continues to dominate the market, driven by rapid industrialization, strong semiconductor manufacturing presence, and expanding electronics and precision engineering industries across key economies such as China, Japan, South Korea, and India. The region’s growth is primarily supported by rising investments in semiconductor fabrication, increasing demand for miniaturized electronic components, and the need for high-precision material processing solutions. China leads the regional market due to its large-scale manufacturing base and growing adoption of advanced micromachining technologies in electronics and semiconductor production, while Japan and South Korea are characterized by strong technological capabilities and high demand for precision manufacturing. Emerging markets such as India and Southeast Asia are witnessing increasing adoption of micromachining equipment as industries focus on enhancing production efficiency, improving product quality, and supporting the development of advanced manufacturing capabilities.

China Micromachining Equipment Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 0.70 billion, representing roughly 18.2% of global sales.

Japan Micromachining Equipment Market

The Japan market is estimated at around USD 0.21 billion in 2026, accounting for roughly 5.5% of the global sales.

India Micromachining Equipment Market

The Indian market is estimated at around USD 0.32 billion in 2026, accounting for roughly 8.4% of global sales.

North America

The North America market accounted for over USD 0.72 billion in revenue in 2025, supported by strong demand for high-precision manufacturing across semiconductor, medical device, and aerospace industries in the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in advanced manufacturing technologies, growing emphasis on miniaturization of electronic components, and the need for high-accuracy material processing solutions. Companies are increasingly adopting micromachining equipment to improve production precision, enhance product performance, and reduce material waste across critical applications. Additionally, government initiatives supporting semiconductor manufacturing and domestic production capabilities are encouraging the adoption of advanced microfabrication technologies. The presence of established aerospace, medical, and electronics industries further support the widespread deployment of high-performance micromachining systems across the region.

U.S. Micromachining Equipment Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 0.63 billion in 2026, driven by its strong semiconductor ecosystem, advanced aerospace manufacturing base, and growing demand for precision medical devices. Unlike many regions, U.S.-based manufacturers are focusing on deploying highly advanced micromachining systems capable of delivering ultra-high precision and supporting complex micro-scale fabrication processes. The country is witnessing significant investments in semiconductor fabrication facilities and advanced packaging technologies, increasing the need for precise drilling, cutting, and structuring solutions.

Europe

The European market is driven by a strong focus on precision engineering, advanced industrial infrastructure, and increasing adoption of high-accuracy manufacturing technologies across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for micromachining equipment is closely linked to the region’s well-established machine tool industry, strong presence in automotive and aerospace manufacturing, and growing emphasis on miniaturization and high-performance components. Organizations are increasingly investing in advanced micromachining solutions to improve production accuracy, enhance surface quality, and support complex component fabrication across industries.

U.K. Micromachining Equipment Market

The U.K. market is estimated at around USD 0.10 billion in 2026, representing roughly 2.6% of global sales.

Germany Micromachining Equipment Market

Germany’s market is projected to reach approximately USD 0.25 billion in 2026, equivalent to around 6.4% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in advanced manufacturing infrastructure, industrial diversification, and growing adoption of precision engineering technologies across key regions such as GCC countries, South Africa, Israel, and North Africa. Demand for micromachining equipment is closely linked to the region’s efforts to enhance local manufacturing capabilities, reduce import dependency, and support high-value industrial production across sectors such as aerospace, electronics, and medical devices. GCC countries are investing in advanced manufacturing and technology-driven industries as part of economic diversification initiatives, supporting the adoption of high-precision machining solutions. Israel represents a technologically advanced market within the region, with strong adoption of micromachining equipment across semiconductor, defense, and photonics applications. South Africa and North Africa are witnessing gradual adoption of precision manufacturing technologies as industries focus on improving production efficiency, enhancing product quality, and supporting industrial modernization efforts.

GCC Micromachining Equipment Market

The GCC market is projected to reach around USD 0.08 billion in 2026, representing roughly 2.0% of the global sales.

South America

The South America market is driven by growing industrial activities, increasing focus on manufacturing efficiency, and gradual adoption of precision machining technologies across key economies such as Brazil, Argentina, and Chile. Demand for micromachining equipment is primarily supported by expanding automotive production, rising electronics assembly activities, and the need for high-precision component manufacturing across industrial sectors. Brazil is witnessing increased adoption of advanced machining systems in automotive and aerospace supply chains, where improving product quality and achieving tight tolerances are key priorities.

Brazil Micromachining Equipment Market

The Brazil market is projected to reach around USD 0.09 billion in 2026, representing roughly 2.4% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Precision Engineering Expertise, Advanced Laser Technologies, and High-Accuracy Processing Capabilities

The micromachining equipment market is moderately consolidated, with competitive positioning driven by technological capabilities, application-specific expertise, and the ability to deliver high-precision machining solutions across industries such as semiconductors, medical devices, electronics, and aerospace. Leading players such as TRUMPF Group, Coherent Corp., GF Machining Solutions, Han’s Laser Technology Industry Group Co., Ltd., and Mitsubishi Electric Corporation maintain strong market positions by offering advanced micromachining systems capable of high-speed, accurate material processing with minimal thermal impact. Their competitive strength is reinforced by continuous innovation in laser technologies, strong domain expertise in precision manufacturing, and the ability to integrate micromachining systems with automated and digital production environments.

Competitive differentiation is increasingly shaped by the ability to combine ultrafast laser technologies, precision motion systems, and intelligent control software to enhance machining accuracy, repeatability, and process efficiency. As industries focus on miniaturization, complex geometries, and advanced material processing, market players are investing in next-generation micromachining solutions with improved precision, higher throughput, and enhanced compatibility with diverse materials. Additionally, the ability to deliver customized solutions tailored to specific application requirements, material characteristics, and production workflows is becoming a key factor in maintaining competitive advantage and expanding global customer relationships. Companies are also strengthening their service capabilities, including real-time process monitoring, predictive maintenance, and digital optimization tools, to support long-term operational efficiency for end users.

- For instance, in March 2025, DMG MORI Co., Ltd. highlighted advancements in its LASERTEC series, focusing on integrated laser micromachining and precision manufacturing solutions for high-accuracy industrial applications.

LIST OF KEY MICROMACHINING EQUIPMENT COMPANIES PROFILED

- TRUMPF Group (Germany)

- Coherent Corp. (U.S.)

- United Machining SA (Switzerland)

- Han’s Laser Corporation (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Makino Milling Machine Co., Ltd. (Japan)

- 3D-Micromac AG (Germany)

- LPKF Laser & Electronics SE (Germany)

- Posalux SA (Switzerland)

- SYNOVA SA (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Makino Milling Machine Co., Ltd. highlighted its micro-milling and micro-EDM solutions designed for ultra-precision component manufacturing in aerospace and medical device applications.

- July 2025: 3D-Micromac AG focused on expanding its laser micromachining solutions for semiconductor and glass processing applications, supporting advanced packaging and microelectronics manufacturing.

- June 2025: LPKF Laser & Electronics AG highlighted advancements in its laser systems for glass and PCB micromachining, focusing on high-precision structuring for electronics and semiconductor applications.

- May 2025: Mitsubishi Electric Corporation emphasized its laser processing and EDM technologies for precision manufacturing, supporting micro-scale machining in electronics and industrial components.

- April 2025: Han’s Laser Technology Industry Group Co., Ltd. expanded its ultrafast laser portfolio for micromachining applications, targeting high-speed processing in semiconductor and consumer electronics manufacturing.

REPORT COVERAGE

The global micromachining equipment market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Machine Type, Application, End-Use Industry, and Region |

| By Machine Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value to stand at USD 3.84 billion in 2026 and is projected to reach USD 6.14 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 1.70 billion.

The market is expected to exhibit a CAGR of 6.1% during the forecast period (2026-2034).

By end use industry, the semiconductor & electronics segment leads the market.

Rising miniaturization demand, semiconductor growth, precision manufacturing needs, medical innovation, and ultrafast laser technology advancements drive market growth.

3D-Micromac AG, LPKF Laser & Electronics AG, Posalux SA, SYNOVA SA, and GF Machining Solutions are top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us