Automated Drilling and Riveting Systems Market Size, Share & Industry Analysis, By Operation Type (Drilling Systems, Riveting Systems, and Integrated Drilling & Riveting Systems), By Automation Level (Fully Automated Systems and Semi-Automated Systems), By End-Use Industry (Aerospace, Space & Launch Vehicles, Defense Ground Systems, Rail Transportation, Automotive, and Heavy Industrial Equipment), and Regional Forecast, 2026–2034

Automated Drilling and Riveting Systems Market Size and Future Outlook

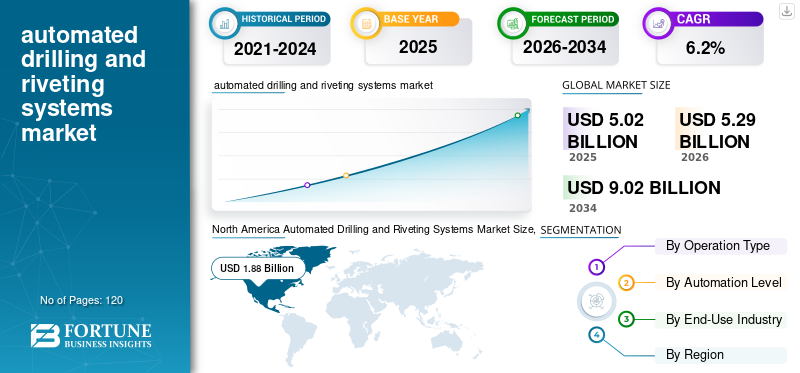

The global automated drilling and riveting systems market size was valued at USD 5.02 billion in 2025. The market is projected to grow from USD 5.29 billion in 2026 to USD 9.02 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the automated drilling and riveting systems market with a market share of 37.45% in 2025.

Automated drilling and riveting systems are advanced aerospace manufacturing solutions used to perform high-precision drilling, fastening, and structural joining of metallic and composite components within aircraft and defense assemblies. These systems integrate multi-axis gantry platforms or robotic cells with CNC-controlled drilling units, automatic fastener insertion modules, and closed-loop force control systems to deliver consistent hole quality, fastening accuracy, and repeatable structural integrity across large airframe sections. The industry is witnessing strong growth in the market, supported by increasing adoption of automation, evolving market trends, and continuous industry developments focused on digital traceability and predictive maintenance integration to enhance operational reliability. Growing demand for composite-intensive airframes and lightweight aluminum-lithium fuselage sections is accelerating the deployment of fully integrated drilling and riveting platforms across North America, Asia Pacific, and the Middle East and Africa, where they play a crucial role in improving production scalability and long-term operational efficiencies within aerospace manufacturing environments.

- For instance, in September 2024, Broetje-Automation has deployed large flexible drilling and riveting gantry systems to support Airbus A320 family production rate increases. In June 2024, Electroimpact supplied automated drilling and fastening equipment for Boeing 737 fuselage panel assembly lines to enable higher monthly output while maintaining structural tolerance compliance and repeatability requirements.

Broetje-Automation, Electroimpact, Ascent Aerospace, MTorres, and Fives are among the key players holding a significant share of the market. Their competitive positioning is supported by integrated gantry-based fastening platforms, robotic drilling cells for composite structures, proprietary force-control and hole-quality verification technologies, and the capability to deliver turnkey, certification-ready assembly automation solutions for commercial aerospace, defense, and space manufacturing applications.

Download Free sample to learn more about this report.

AUTOMATED DRILLING AND RIVETING SYSTEMS MARKET TRENDS

Shift toward Closed-Loop Fastening Verification and Digital Traceability is Transforming Automated Drilling and Riveting Systems Architecture

Demand for automated drilling and riveting systems is increasingly shaped by OEM requirements for certified fastening integrity, real-time process validation, and full digital traceability across high-rate aerospace and defense production programs with long lifecycle compliance obligations. These evolving requirements are significantly influencing overall market dynamics, as manufacturers prioritize the adoption of automation and data-driven quality assurance to enhance structural reliability and long-term operational performance. Rather than focusing solely on cycle-time acceleration, leading suppliers are investing in closed-loop force control, automated hole-quality inspection, advanced control systems, and sensor-integrated riveting heads. These capabilities support frequent production rate variability and parallel assembly of aluminum, titanium, and composite airframe structures while maintaining strict positional tolerances and repeatability.

- For instance, in May 2024, MTorres delivered flexible robotic drilling and riveting cells for composite aerostructure assembly programs incorporating automated fastener feeding and digital process monitoring. Similarly, in November 2023, Ascent Aerospace has advanced its fastening system platforms with programmable force-control and integrated inspection modules to support qualification requirements in commercial and defense aircraft manufacturing environments.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Commercial Aircraft Production Targets to Drive Market Growth

The automated drilling and riveting systems market is experiencing accelerated growth as increasing commercial aircraft production targets and sustained defense platform modernization programs drive OEMs and Tier-1 aerostructure suppliers to expand qualified assembly capacity and invest in next-generation fastening automation technologies. Narrowbody aircraft programs continue to ramp output, while military aircraft production and upgrade cycles are reinforcing long-term demand for structurally certified drilling and fastening systems. Production activity across fuselage panel assembly, wing box integration, and composite structural sections intensified in 2024, prompting leading automation providers to prioritize system upgrades, digital integration, and scalable gantry deployments capable of meeting tighter takt times and repeatability requirements.

- For instance, in March 2024, Ascent Aerospace continued to advance its automated fastening system platforms for commercial aircraft fuselage assembly programs, while in July 2024, MTorres delivered robotic drilling and riveting solutions for composite aerostructure manufacturing. These deployments support higher production-rate environments across major aerospace programs in Europe and North America.

MARKET RESTRAINTS

Variability in Material Behavior to Constraint Industry Expansion

Unlike conventional industrial fastening applications, automated drilling and riveting systems in aerospace environments must accommodate diverse material stacks, including aluminum alloys, titanium components, and carbon fiber reinforced composites, each requiring distinct drilling parameters, force-control settings, and fastening sequences. Variability in material behavior, structural tolerances, and OEM-specific qualification protocols limits the standardization of fully modular, high-throughput drilling and riveting platforms. Differences in fastener types, hole preparation requirements, and surface protection standards often necessitate program-specific tooling, calibration procedures, and validation cycles, increasing integration complexity and deployment timelines. For suppliers serving commercial and defense aircraft manufacturers, where structural non-conformance can directly impact certification and delivery schedules, this technical variability can delay large-scale automation rollouts and constrain rapid capacity scaling, even amid strong end-market demand.

MARKET OPPORTUNITIES

Defense Localization Policies and ITAR-Driven Sourcing to Create New Market Opportunities

An emerging opportunity in the market is being created by defense localization policies and stricter ITAR and export-control requirements, which are reshaping capital equipment sourcing strategies across military aerospace and advanced defense manufacturing programs. Defense OEMs are increasingly prioritizing regionally certified automation integrators capable of delivering ITAR-compliant drilling and fastening systems, secure data architectures, and in-country installation and lifecycle support to reduce geopolitical and supply-chain risk. This shift is expanding demand for automated drilling and riveting systems suppliers that can meet defense qualification standards, support low-to-medium volume aircraft and unmanned system programs, and provide long-term technical servicing for structurally critical assembly lines.

- For instance, in October 2024, PaR Systems supported defense-focused automation deployments in North America by delivering customized, secure drilling and fastening platforms designed to meet program-specific qualification requirements, while in February 2024, KUKA Systems advanced aerospace drilling and riveting automation solutions in Europe to comply with export-control and controlled military manufacturing standards.

MARKET CHALLENGES

Fragmented Aerospace and Defense Qualification Standards to Add Certification Burden

Automated drilling and riveting systems suppliers face significant challenges arising from fragmented qualification, compliance, and documentation requirements across commercial aerospace and defense manufacturing programs. Fastening systems must often comply with program-specific structural validation standards, OEM production specifications, ITAR controls, AS9100 quality management systems, and customer-defined process approval protocols, requiring tailored system configurations, software documentation, and verification procedures. Differences in airframe architecture, material stack-ups, fastener types, and inspection standards limit full standardization of drilling and riveting platforms and increase integration complexity during new program industrialization. For automation providers serving multiple OEMs across regions, repeated validation cycles, plant-level audits, and requalification testing can extend deployment timelines and elevate engineering costs, hindering automated drilling and riveting systems market growth. This regulatory and procedural fragmentation constrains scalability, even as end-market demand supports higher aircraft production rates.

Segmentation Analysis

By Operation Type

Integrated Drilling & Riveting Systems Segment Led as it Serves as the Structural Backbone of High-Throughput Aerospace Assembly Lines

By operation type, the market is segmented into drilling systems, riveting systems, and integrated drilling & riveting systems.

Integrated drilling & riveting systems held the largest automated drilling and riveting systems market share as they form the structural and operational backbone of high-rate, precision-critical aerospace assembly programs, particularly across commercial aircraft, defense platforms, and large aerostructure manufacturing environments. These systems combine automated hole drilling, fastener insertion, and closed-loop force control within unified gantry or robotic platforms, enabling synchronized operations, reduced cycle times, and enhanced structural repeatability across fuselage panels, wing sections, and composite assemblies. As OEMs increasingly prioritize takt-time compression, digital traceability, and minimized manual intervention, fully integrated drilling and fastening platforms are becoming a strategic investment focus for manufacturers seeking to scale production while maintaining certification compliance and structural integrity under demanding qualification standards.

- For instance, in April 2024, Fives delivered automated drilling and fastening systems for aerospace structural assembly applications through its aerospace division, while in September 2024, PaR Systems supplied customized automated fastening platforms for complex aerostructure integration programs. This supports digitally controlled drilling and riveting operations within North American aerospace manufacturing facilities.

Drilling systems play a critical role in supporting both standalone applications and modular automation upgrades across aerospace and industrial manufacturing environments, and are growing at a CAGR of 6.7%. While integrated systems dominate large-scale assembly lines, standalone drilling platforms offer greater deployment flexibility, lower initial capital intensity, and adaptability for mixed-material stack-ups and retrofit programs.

To know how our report can help streamline your business, Speak to Analyst

By Automation Level

Fully Automated Systems Segment Led due to theirWidespread Deployment Across Commercial A&D Aircraft Assembly Programs

By automation level, the automated drilling and riveting systems market is segmented into fully automated systems and semi-automated systems.

Fully automated systems held the largest share of the automated drilling and riveting systems market, driven by their widespread deployment across commercial aerospace and defense aircraft assembly programs where repeatability, throughput, and structural certification compliance are critical. These systems integrate CNC-controlled drilling units, automated fastener feeding modules, force-controlled riveting heads, and digital process monitoring within synchronized gantry or robotic architectures. Their ability to execute drilling, countersinking, fastener insertion, and quality validation in a single automated sequence significantly reduces cycle time, labor dependency, and rework rates. As aircraft production rates increase and OEMs prioritize takt-time compression and digital traceability, fully automated systems continue to serve as the core infrastructure of high-volume fuselage and wing assembly lines, reinforcing their dominance in overall market consumption.

Fully automated systems are also expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 6.2%, supported by rising investments in greenfield aerospace facilities and modernization of legacy assembly lines. Increasing emphasis on closed-loop fastening verification, predictive maintenance integration, and MES-connected data logging is driving OEMs and Tier-1 suppliers to transition from semi-automated workstations toward fully integrated, digitally enabled platforms.

By End-Use Industry

Extensive Deployment in High-Precision Airframe Assembly Led to Aerospace Segmental Dominance

Based on end-use industry, the market is segmented into aerospace, space & launch vehicles, defense ground systems, rail transportation, automotive, and heavy industrial equipment.

Aerospace accounts for the highest share of the market, driven by the extensive use of automated drilling and riveting systems across fuselage, wing, empennage, and structural airframe assembly operations within commercial aircraft programs. Aerospace production environments require tight positional tolerances, certified fastening integrity, and high repeatability across large structural assemblies, making integrated drilling and fastening automation a core infrastructure investment. Aircraft assembly programs are characterized by long qualification cycles, strict regulatory oversight, and sustained multi-year production runs, requiring system providers to deliver digitally traceable, force-controlled, and certification-ready fastening solutions. As commercial narrowbody aircraft production stabilizes at elevated rates and composite-intensive airframe structures expand, aerospace continues to represent the structural backbone of overall automated drilling and riveting systems demand.

The space & launch vehicles segment is expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 7.3%, supported by increasing investments in satellite deployment programs, reusable launch vehicle development, and national space initiatives. Structural assembly of launch vehicles and space-grade components requires precision drilling, lightweight material fastening, and high-integrity joining across aluminum-lithium alloys and composite structures under strict reliability standards.

Automated Drilling and Riveting Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America Automated Drilling and Riveting Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market accounted for over USD 1.88 billion in revenue in 2025, supported by a highly concentrated aerospace airframe assembly footprint across the U.S., Canada, and Mexico. Regional demand is structurally tied to high-rate narrowbody fuselage production, large-scale wing integration facilities, and defense aircraft structural assembly programs that rely heavily on automated drilling and fastening architectures. Commercial single-aisle assembly lines in the region utilize synchronized multi-spindle gantry systems to maintain takt-time discipline, while defense manufacturing facilities deploy adaptive drilling platforms for complex aluminum–titanium stack-ups and composite structures. The region also exhibits a significant installed base of legacy fastening systems undergoing digital upgrades, including sensor-enabled force monitoring and MES-connected traceability modules. Ongoing production rate normalization, structural assembly optimization, and long-cycle aerospace program backlogs continue to sustain consistent capital expenditure toward high-throughput, precision drilling and riveting automation platforms across the region.

U.S. Automated Drilling and Riveting Systems Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 1.62 billion in 2026, driven by its concentration of final aircraft assembly lines, Tier-1 aerostructure manufacturing hubs, and defense aircraft production facilities. Unlike sub-assembly-focused markets, U.S. facilities perform full structural integration activities requiring synchronized drilling, countersinking, and fastening operations across fuselage panels, wing sections, and empennage structures. High-speed gantry-based systems operating across moving production lines form the backbone of commercial aircraft assembly, while reconfigurable robotic drilling cells support classified defense manufacturing programs. Continuous investments in takt-time compression, automated hole-quality verification, and integrated fastening data capture are reinforcing the modernization of existing assembly infrastructure. The depth of OEM-supplier integration and large-scale production responsibility position the U.S. as the primary revenue contributor within the regional market.

Europe

The European market is supported by a distributed and program-driven aerospace manufacturing structure, particularly across Airbus-aligned airframe assembly, defense aircraft production, and high-value aerostructure fabrication hubs. Demand for Automated Drilling and Riveting Systems is closely tied to wing box integration in the U.K., fuselage and structural assembly operations in Germany and France, and composite aerostructure production in Spain and Italy. Unlike centralized manufacturing models, Europe’s cross-border aircraft production architecture requires modular and transportable drilling and fastening platforms capable of operating across segmented assembly facilities. Stringent structural validation standards, traceability mandates, and sustainability-focused factory modernization initiatives are accelerating investment in digitally integrated gantry systems and robotic fastening cells. Countries such as Germany, France, Spain, Italy, and the Netherlands lead regional adoption, supported by established aerospace clusters, advanced automation integration capabilities, and export-oriented airframe production programs.

U.K. Automated Drilling and Riveting Systems Market

The U.K. market in 2026 is estimated at around USD 0.35 billion, representing roughly 6.2% of global sales.

Germany Automated Drilling and Riveting Systems Market

Germany’s market is projected to reach approximately USD 0.41 billion in 2026, equivalent to around 7.4% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing Automated Drilling and Riveting Systems market, generating revenue of USD 1.38 billion in 2025 globally. Within the region, China and Japan are projected to reach approximately USD 0.51 billion and USD 0.16 billion, respectively, by 2026. Market expansion is primarily driven by increasing aerospace manufacturing localization, expansion of commercial aircraft structural assembly capacity, and rising defense platform industrialization across major economies. China’s growth is closely linked to domestic narrowbody aircraft production and aerostructure manufacturing investments, while Japan’s demand is supported by high-precision wing and composite component assembly programs integrated into global aerospace supply chains. South Korea, India, and ASEAN countries are emerging contributors as regional governments encourage aerospace capability development and Tier-1 supplier expansion.

China Automated Drilling and Riveting Systems Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with 2026 revenues estimated at around USD 0.51 billion, representing roughly 9.2% of global sales.

Japan Automated Drilling and Riveting Systems Market

The Japanese market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 2.9% of the global sales.

India Automated Drilling and Riveting Systems Market

The India market in 2026 is estimated at around USD 0.29 billion, accounting for roughly 5.2% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by defense localization initiatives, aerospace industrial development programs, and expanding advanced manufacturing activity, particularly across the GCC and select North African economies. Government-backed investments in domestic aircraft assembly, military platform integration, and aerospace capability development are supporting demand for automated drilling and riveting systems used in structural assembly and fastening operations. The GCC benefits from high-capex, specification-driven defense and aerospace projects requiring ITAR-compliant, digitally integrated drilling and fastening platforms, while North Africa is witnessing the gradual expansion of aerostructure manufacturing aligned with European aerospace supply chains. Across parts of Sub-Saharan Africa, limited but growing industrial capability is encouraging incremental adoption of semi-automated drilling and fastening solutions in defense and heavy equipment assembly.

GCC Automated Drilling and Riveting Systems Market

The GCC market is projected to reach around USD 0.08 billion in 2026, representing roughly 1.4% of the global sales.

South America

The South American market is supported by the region’s developing aerospace and industrial manufacturing footprint, particularly in Brazil and Argentina, which serve as key hubs for aircraft assembly, aerostructure production, and defense-related manufacturing. Brazil’s commercial and defense aircraft programs represent the primary driver of demand for automated drilling and riveting systems, supported by structural assembly operations requiring precision hole-making and fastening automation. While overall production volumes remain lower compared to North America and Europe, export-oriented aerospace manufacturing and participation in global supply chains are encouraging investment in digitally integrated drilling and fastening platforms. Argentina and select regional facilities are gradually modernizing assembly infrastructure to improve structural repeatability, reduce manual dependency, and align with international aerospace quality standards.

Brazil Automated Drilling and Riveting Systems Market

The Brazilian market is projected to reach around USD 0.21 billion in 2026, representing roughly 3.7% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Program Integration Depth, System Reliability, and Long-Term OEM Alignment Rather than Portfolio Width

The automated drilling and riveting systems market is moderately consolidated, with competitive positioning shaped less by the breadth of automation portfolios and more by the depth of aerospace integration capability, program qualification history, and long-term participation in commercial and defense aircraft assembly programs. Leading players such as Broetje-Automation, Electroimpact, Ascent Aerospace, MTorres, and Fives maintain strong market positions by delivering high-precision gantry-based and robotic drilling and fastening platforms tailored to fuselage, wing, and composite aerostructure assembly environments. Their competitive strength is reinforced by proprietary force-control technologies, system integration expertise, aircraft-specific engineering customization, and the ability to sustain structural repeatability under high-rate production conditions across multi-year aircraft programs.

Competitive differentiation is increasingly driven by a supplier’s ability to support takt-time compression, integrate digital traceability into fastening operations, and manage complex multi-material stack drilling requirements rather than by equipment scale alone. As OEMs prioritize execution reliability, data-backed structural validation, and long-term lifecycle serviceability, Automated Drilling and Riveting Systems leaders are strengthening in-house engineering, software integration, and aftermarket support capabilities to protect installed-base positions and elevate switching barriers for new entrants.

- For instance, in June 2024, KUKA Systems supported aerospace structural assembly automation projects incorporating synchronized drilling and fastening integration within complex airframe production lines. Similarly, in January 2024, Coriolis Composites developed robotic drilling solutions tailored for composite aerostructure applications requiring high positional accuracy and adaptive process control.

LIST OF KEY AUTOMATED DRILLING AND RIVETING SYSTEMS COMPANIES PROFILED IN REPORT:

- Broetje-Automation (Germany)

- Electroimpact Inc. (U.S.)

- Ascent Aerospace (U.S.)

- MTorres (Spain)

- Fives Group (U.S.)

- KUKA Systems (Germany)

- PaR Systems LLC (U.S.)

- Coriolis Composites (France)

- FANUC Group (Japan)

- Asian Aerospace Automation Integrators (Thailand)

KEY INDUSTRY DEVELOPMENTS

- November 2025: KUKA Systems Aerospace expanded its automated drilling and fastening integration capabilities for large aerostructure assembly programs in North America, enhancing synchronized multi-axis gantry solutions designed for composite fuselage and wing section assembly under digitally traceable production environments.

- August 2025: MTorres advanced its robotic drilling and riveting platforms for composite-intensive airframe structures, integrating adaptive force-control and automated fastener feeding technologies to support higher-rate aerospace production programs across Europe.

- May 2025: Ascent Aerospace continued the modernization of its fastening system platforms derived from Gemcor technology, focusing on improved process monitoring, programmable fastening parameters, and enhanced system reconfigurability for next-generation aircraft assembly applications.

- March 2025: Broetje-Automation enhanced its flexible, rail-mounted drilling and riveting gantry systems for single-aisle aircraft assembly programs, integrating advanced hole-quality monitoring and real-time data capture modules to improve takt-time stability and structural traceability across high-rate fuselage production lines.

- October 2024: PaR Systems delivered customized automated drilling and fastening systems for defense-focused manufacturing facilities, incorporating secure control architectures and adaptive drilling functionality to meet program-specific qualification and compliance requirements.

REPORT COVERAGE

The global automated drilling and riveting systems market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATRRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Operation Type, Automation Level, End-Use Industry, and Region |

|

By Operation Type |

|

|

By Automation Level |

|

|

By End-Use Industry |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.29 billion in 2026 and is projected to reach USD 9.02 billion by 2034.

In 2025, North America’s market value stood at USD 1.88 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period (2026-2034).

By end-use industry, the aerospace segment leads the market.

Increasing aircraft production rates, tighter fastening tolerances, and composite airframe adoption lines are key factors driving the market.

J Broetje-Automation, Electroimpact, Ascent Aerospace, MTorres are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us