Mild Hybrid Vehicle Market Size, Share & Industry Analysis, By Vehicle Type (Sedan/Hatchback, SUV, Light Commercial Vehicle, and Heavy Commercial Vehicle), By Architecture (12V Mild Hybrid Systems, 24V Mild Hybrid Systems, and 48V Mild Hybrid Systems), By Component (Starter Generator/Electric Motor, Battery Pack, DC-DC Converter, Power Electronics/Inverter, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

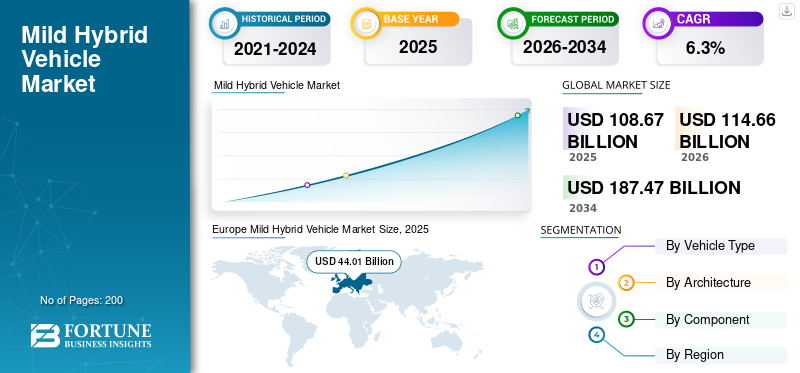

The global mild hybrid vehicle market size was valued at USD 108.67 billion in 2025. The market is projected to grow from USD 114.66 billion in 2026 to USD 187.47 billion by 2034, growing at a CAGR of 6.3% during the forecast period. Europe dominated the global market with a market share of 40.49% in 2025.

The Mild Hybrid Vehicle (MHEV) market refers to the global industry for vehicles equipped with mild hybrid technology, which combines a traditional internal combustion engine (ICE) with a small electric motor and battery to assist the engine rather than power the car independently. This auxiliary electric system improves overall fuel efficiency and reduces emissions by providing extra torque during acceleration, enabling start-stop functions, and recovering energy through regenerative braking, but cannot drive the vehicle on electric power alone similar to full hybrids or plug-in hybrids.

The growth of the market is primarily driven by stringent emission regulations, fuel-efficiency mandates, cost advantages over full electrification, and rising global vehicle production. The governments across major automotive markets have tightened CO₂ and fuel-economy standards. For instance, the European Union requires average fleet emissions to remain below 95 g CO₂/km, while China’s Corporate Average Fuel Consumption (CAFC) targets and India’s CAFE II norms (effective from 2023) have pushed automakers to adopt electrification at scale. Mild hybrid systems typically deliver 10–20% fuel-efficiency improvement compared to conventional ICE vehicles at a significantly lower cost than full hybrids or BEVs, making them an attractive compliance solution for OEMs.

Key manufacturers in the market play a critical role in accelerating adoption by integrating cost-effective electrification and mild hybrid technologies across high-volume vehicle platforms and regions. Toyota Motor Corporation and Honda Motor Co. leverage their long-standing hybrid expertise to optimize 12V and 48V mild hybrid systems, particularly in compact and mid-size passenger cars, helping reduce fleet emissions at scale. Volkswagen Group, Stellantis, and Renault Group have been instrumental in expanding 48V MHEV architectures across mass-market models in Europe, where regulatory pressure is the highest, making mild hybrids a core compliance strategy for CO₂ targets.

Download Free sample to learn more about this report.

MILD HYBRID VEHICLE MARKET TRENDS

Rapid Shift toward 48V Mild Hybrid Architectures across Vehicle Segments

A key trend shaping the market is the accelerating transition from conventional 12V systems to 48V mild hybrid architectures, driven by the need for higher efficiency gains and compatibility with advanced vehicle functions. Compared to 12V systems, 48V MHEVs enable stronger regenerative braking, higher torque assist, and support for energy-intensive features such as electric turbochargers, advanced start-stop, and electrified auxiliaries. This trend is particularly evident in passenger cars, SUVs, and light commercial vehicles, where OEMs are standardizing 48V systems across multiple platforms to balance between cost and performance, compliance, and cost.

For instance, according to European Automobile Manufacturers’ Association (ACEA) data, electrified vehicles (including mild hybrids) accounted for over 50% of new passenger car registrations in the EU in 2024, with mild hybrids representing the largest single electrified powertrain category. Similarly, statistics from the International Energy Agency (IEA) indicate that 48V mild hybrid systems contribute to average fuel consumption reductions of 10-15%, making them a preferred compliance technology for automakers in Europe and Asia. Additionally, the China Association of Automobile Manufacturers (CAAM) reports that vehicles equipped with mild hybrid or hybrid-assisted systems accounted for over 35% of new energy-related vehicle launches in China’s passenger car segment in 2023, underscoring the growing institutional and industry-level support for mild hybrid architectures globally.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations and Cost-Effective Electrification to Drive Vehicle Adoption

The tightening of global emission and fuel-efficiency regulations is a major factor driving the mild hybrid vehicle market growth, as automakers seek scalable and cost-effective electrification solutions. Mild hybrid systems, especially 48V architectures, enable OEMs to achieve significant CO₂ and fuel-consumption reductions without the high costs and infrastructure requirements associated with full hybrids or battery electric vehicles. These systems improve fuel efficiency by 10-20% and support start-stop and regenerative braking. Furthermore, these are increasingly deployed across high-volume passenger cars, SUVs, and light commercial vehicles to meet regulatory targets while maintaining affordability.

For instance, in Europe, automakers must comply with an average fleet emission target of 95 g CO₂/km, and industry data indicates that vehicles equipped with 48V mild hybrid systems can reduce emissions by up to 15 g CO₂/km compared to conventional ICE models. As a result, more than 60% of newly electrified vehicles launched in Europe between 2022 and 2024 incorporated mild hybrid technology. Similarly, in China, mild hybrids contribute to meeting CAFC fuel-consumption targets, while in India, CAFE II norms have accelerated adoption, with mild hybrid systems being present in over 25-30% of new passenger vehicle models offered by leading OEMs. These regulatory and economic advantages continue to position mild hybrids as a key transitional technology, driving sustained market growth globally.

MARKET RESTRAINTS

Limited Policy Incentives and Shift toward Zero-Emission Targets May Restrain Mild Hybrid Adoption

A key restraint impacting the market is the growing policy emphasis on zero-emission vehicles, which reduces long-term regulatory and financial support for mild hybrids. While MHEVs offer measurable fuel and emission benefits, their inability to operate in pure electric mode limits the eligibility for incentives, low-emission zone (LEZ) access, and long-term compliance pathways in several regions. As governments accelerate timelines for ICE phase-outs, mild hybrids are increasingly positioned as an interim solution rather than a future-proof technology.

For instance, according to the European Automobile Manufacturers’ Association (ACEA), battery electric vehicles accounted for approximately 15% of new EU passenger car registrations in 2024, supported by strong purchase incentives, while mild hybrids received minimal or no direct subsidies across most EU member states. Data from the International Energy Agency (IEA) further indicates that over 30 countries have announced targets to phase out new ICE vehicle sales between 2030 and 2040, with policy frameworks primarily favoring BEVs and PHEVs. In addition, statistics from the U.K. Department for Transport (DfT) show that vehicles without zero-emission capability face increasing restrictions in more than 20 urban low-emission zones, limiting the long-term attractiveness of mild hybrids for both consumers and fleet operators. These policy and regulatory trends collectively restrain the growth potential of the market over the medium to long term.

MARKET OPPORTUNITIES

Rising Demand for Affordable Electrification in Emerging Markets Creates Strong Growth Opportunities

The market presents a significant opportunity in emerging economies, where rapid motorization, rising fuel prices, and tightening emission norms are increasing the demand for fuel-efficient yet affordable vehicles. In these regions, limited charging infrastructure, higher upfront costs of BEVs, and range anxiety continue to constrain full electrification, positioning mild hybrids as a practical transitional solution. MHEVs offer significant fuel savings and emission reductions without requiring major changes to consumer behavior or supporting infrastructure, making them well-suited for high-volume passenger cars and commercial vehicles.

According to the Society of Indian Automobile Manufacturers (SIAM), passenger vehicles equipped with hybrid or hybrid-assist technologies (including mild hybrids) accounted for over 28% of new passenger vehicle model offerings in India in 2023, up from less than 15% in 2020, reflecting rapid OEM adoption. Similarly, data from the International Energy Agency (IEA) indicates that emerging economies outside China will account for nearly 45% of the global passenger car sales growth between 2025 and 2030, where charging infrastructure availability remains below 10 public chargers per 100,000 people in several markets. In Southeast Asia, statistics from the ASEAN Automotive Federation (AAF) highlight that improving fuel-efficiency standards and urban congestion policies are accelerating the demand for hybridized vehicles, positioning mild hybrids as a key growth opportunity in price-sensitive, high-volume automotive markets.

MARKET CHALLENGES

Cost Sensitivity and Limited Consumer Awareness to Create Adoption Challenges

A major challenge for the market is balancing system cost increases with clear consumer value perception, particularly in price-sensitive markets. Although mild hybrid systems are more affordable than full hybrids or BEVs, they still add incremental costs related to 48V batteries, integrated starter-generators, and power electronics, which can affect vehicle pricing in entry-level and mass-market segments. In addition, limited consumer awareness and understanding of mild hybrid benefits such as fuel savings, smoother start-stop operation, and emission reduction can reduce willingness to pay, slowing adoption despite regulatory and OEM push.

According to the International Energy Agency (IEA), mild hybrid systems typically add USD 800-1,500 to vehicle manufacturing costs, depending on system complexity. Data from the European Automobile Manufacturers’ Association (ACEA) indicates that while electrified vehicles accounted for over 50% of new passenger car registrations in the EU in 2024, consumer surveys show that nearly one-third of buyers could not clearly differentiate between mild hybrids, full hybrids, and plug-in hybrids. Similarly, statistics from the Society of Indian Automobile Manufacturers (SIAM) highlight that price sensitivity remains high, with over 70% of passenger vehicle buyers in India prioritizing upfront vehicle cost over long-term fuel savings, making it challenging for OEMs to fully pass on mild hybrid system costs. These factors collectively present a key challenge to faster and broader mild hybrid market adoption.

Segmentation Analysis

By Vehicle Type

SUV Segment Leads with High Demand and Suitability for Integrating Mild Hybrid Systems

On the basis of vehicle type, the market is segmented into sedans/hatchbacks, SUVs, light commercial vehicles, and heavy commercial vehicles.

Among these, the SUV segment dominates the mild hybrid vehicle market share due to its strong global demand, higher profit margins for OEMs, and suitability for integrating mild hybrid systems without significant cost or packaging constraints. SUVs benefit from mild hybrid technology through improved fuel efficiency and reduced emissions, enhanced low-speed torque, and smoother start-stop operation, which helps offset their higher weight and fuel consumption compared to smaller vehicles. The rising consumer preference for SUVs across both developed and emerging markets further supports their dominance, as automakers increasingly electrify SUV lineups to meet emission norms while maintaining performance and driving comfort.

According to ACEA, SUVs accounted for over 51% of new passenger car registrations in Europe in 2024 and a growing share of these models are now offered with 48V mild hybrid powertrains as standard or optional variants. Similarly, data from the International Energy Agency (IEA) indicates that SUVs contribute nearly 45% of global passenger vehicle sales, making them a primary focus for OEM electrification strategies. As a result, mild hybrid SUVs remain central to market revenue generation, while the sedan and hatchback segment is expected to grow at a moderate CAGR, driven mainly by cost-sensitive markets and entry-level hybridization.

The sedan/hatchback segment is expected to grow at a CAGR of 4.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Architecture

48V Mild Hybrid Systems Dominate Due to Higher Efficiency and Performance

On the basis of architecture, the market is segmented into 12V, 24V, and 48V mild hybrid systems.

Among these, the 48V mild hybrid systems segment dominates the market due to its ability to deliver significantly higher fuel-efficiency gains, improved torque assistance, and compatibility with advanced vehicle functions compared to lower-voltage systems. The 48V architecture supports stronger regenerative braking, electric boost during acceleration, and the integration of energy-intensive features such as electric superchargers and advanced thermal management systems. These advantages make 48V systems particularly suitable for SUVs, premium vehicles, and high-volume passenger cars, where performance and emission compliance are equally critical.

According to the European Automobile Manufacturers’ Association (ACEA), over 65% of newly launched electrified ICE-based passenger vehicles in Europe in 2024 were equipped with 48V mild hybrid systems, reflecting OEM preference for higher-efficiency architectures to meet stringent CO₂ targets. Similarly, data from the International Energy Agency (IEA) indicates that 48V mild hybrid systems achieve fuel-consumption reductions of up to 15-20%, compared to 5-8% for 12V systems. As a result, global OEMs such as Volkswagen Group, Stellantis, BMW, and Mercedes-Benz continue to standardize 48V architectures across multiple platforms, reinforcing the segment’s dominance over the forecast period.

The 24V mild hybrid system segment is expected to grow at a CAGR of 5.6% over the forecast period.

By Component

Starter Generator/Electric Motor Segment Leads as it Forms the Core of Mild Hybrid Systems

On the basis of component, the market is segmented into starter generator/electric motor, battery pack, DC-DC converter, power electronics/inverter, and others.

Among these, the starter generator / electric motor segment dominates the market, as it is the central component enabling key mild hybrid functionalities such as torque assist, regenerative braking, and advanced start-stop operation. Integrated starter generators (ISGs) and belt-driven starter generators (BSGs) directly influence system performance, fuel-efficiency gains, and driving refinement, making them indispensable across both 12V and 48V mild hybrid architectures.

For instance, according to the International Energy Agency (IEA), electric motor-based torque assistance in mild hybrid systems contributes to up to 70% of total fuel-efficiency gains achieved by MHEVs, highlighting its critical role in system effectiveness. Additionally, data from the European Automobile Manufacturers’ Association (ACEA) indicates that nearly all 48V mild hybrid vehicles sold in Europe in 2024 were equipped with integrated or belt-driven starter generators, underscoring near-universal adoption. As OEMs increasingly standardize mild hybrid systems across SUVs and high-volume passenger vehicles, the demand for starter generators and electric motors continues to outpace other components, reinforcing the segment’s dominant market position.

The battery pack segment is expected to grow at a CAGR of 7.2% over the forecast period.

Mild Hybrid Vehicle Market Regional Outlook

By geography, the global market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Mild Hybrid Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe’s dominance in the mild hybrid vehicle market is strongly supported by official automotive association data and regulatory-driven adoption trends. According to the European Automobile Manufacturers’ Association (ACEA), electrified vehicles accounted for over 50% of new passenger car registrations in the European Union in 2024, with mild hybrids representing the single largest powertrain category within electrified vehicles. ACEA data further shows that more than 40% of all new cars sold in the EU were mild hybrids, reflecting their critical role in helping OEMs meet the EU’s 95 g CO₂/km fleet emission target.

Additionally, the International Council on Clean Transportation (ICCT) reports that the widespread deployment of 48V mild hybrid systems has enabled average CO₂ reductions of 10–15% per vehicle, making them one of the most cost-effective compliance technologies in Europe. Major automotive markets such as Germany, France, Italy, and the U.K. collectively account for over 65% of Europe’s mild hybrid registrations, driven by strong OEM presence and rapid standardization of MHEV systems across passenger cars and SUVs. These association-backed statistics clearly reinforce Europe’s leading position in the global market.

Germany Mild Hybrid Vehicle Market

The Germany market reached a value of approximately USD 15.14 billion by 2025 and is set to expand at a CAGR of about 3.9% over the forecast period. Germany is a key contributor to Europe’s dominance in the market, supported by its strong automotive manufacturing base and early adoption of electrification technologies. Home to major OEMs such as Volkswagen Group, BMW, and Mercedes-Benz, Germany has rapidly integrated 48V mild hybrid systems across passenger cars and SUVs to meet EU CO₂ regulations. Mild hybrids are widely positioned as standard powertrains in both premium and mass-market models, making Germany one of the largest markets for MHEVs in Europe.

U.K. Mild Hybrid Vehicle Market

The U.K. represents a growing market, driven by tightening emission norms, expanding low-emission zones, and rising fuel costs. Automakers are increasingly offering mild hybrid variants to help consumers reduce emissions while avoiding the higher upfront cost of full electrification. With strong demand for SUVs and crossovers, the U.K. market favors mild hybrid systems that improve fuel efficiency and urban drivability, supporting steady adoption as the country progresses toward its long-term zero-emission mobility targets.

North America

North America represents a steadily growing market for mild hybrid vehicles, supported by tightening fuel economy regulations, rising fuel prices, and increasing electrification of SUVs and pickup-based platforms. While BEVs are gaining traction, mild hybrids continue to play an important role as a transitional technology, particularly in large SUVs and light trucks where full electrification remains costly. Automakers such as Ford, General Motors, and Stellantis are increasingly integrating mild hybrid systems to improve fuel efficiency and meet Corporate Average Fuel Economy (CAFE) standards. The consumer preference for performance-oriented vehicles and larger vehicle formats supports the adoption of mild hybrid systems that enhance torque and drivability without compromising utility.

U.S. Mild Hybrid Vehicle Market

The U.S. market reached a value of USD 11.25 billion by 2025 and is expected to expand at a CAGR of about 5.8% over the forecast period. The U.S. is a steadily growing market, driven by tightening Corporate Average Fuel Economy (CAFE) standards, rising fuel prices, and strong consumer demand for mild hybrid vehicles (SUVs and light trucks). Automakers increasingly deploy mild hybrid systems in large vehicles to improve fuel efficiency and enhance performance without significantly increasing vehicle costs. While BEVs are gaining momentum, mild hybrids continue to play an important transitional role, particularly in segments where full electrification faces cost, range, or infrastructure challenges.

Asia Pacific

Asia Pacific is the fastest-growing regional market for mild hybrid vehicles, driven by high vehicle production volumes, rising urbanization, and tightening emission norms across major economies such as China, India, Japan, and South Korea. In China, mild hybrid systems support compliance with Corporate Average Fuel Consumption (CAFC) targets, while in India, CAFE II norms and limited charging infrastructure favor affordable hybridization over full electrification. Japanese and Korean OEMs leverage mild hybrid technology to enhance fuel efficiency in mass-market vehicles, while rapid SUV penetration further accelerates demand. Cost sensitivity and infrastructure constraints make mild hybrids an attractive bridge technology, positioning Asia Pacific as a key growth engine for the market.

China Mild Hybrid Vehicle Market

China dominates the Asia Pacific market, supported by its massive vehicle production base, stringent Corporate Average Fuel Consumption (CAFC) regulations, and strong OEM focus on powertrain efficiency. Mild hybrid systems are widely adopted across passenger cars and SUVs as a cost-effective solution to meet fuel-economy targets while maintaining affordability. With limited incentives for mild hybrids compared to BEVs, OEMs still rely heavily on MHEVs to achieve fleet-wide compliance, making China the largest market in the region in terms of volume. The China market touched a value of USD 16.42 billion by 2025, expanding at a CAGR of 7.1% over the forecast period.

India Mild Hybrid Vehicle Market

India is the fastest-growing market, driven by rising fuel prices, strict CAFE II emission norms, and limited public charging infrastructure. Mild hybrids offer a practical and affordable pathway to improved fuel efficiency in a highly price-sensitive market. Increasing adoption across compact cars and SUVs, combined with strong demand for fuel-efficient vehicles, is accelerating market growth at a faster pace than other Asia Pacific countries.

Japan Mild Hybrid Vehicle Market

Japan represents a mature and technologically advanced market, supported by strong domestic OEMs such as Toyota, Honda, and Suzuki. Mild hybrid systems are widely integrated into compact and mid-size vehicles to enhance fuel efficiency and reduce emissions, particularly in urban driving conditions. While full hybrids remain dominant, mild hybrids continue to play a complementary role, especially in entry-level and mass-market segments.

Rest of the World

The rest of the world market is anticipated to grow at a significant pace, registering a CAGR of 4.2% over the forecast period. This region, including Latin America, the Middle East, and Africa, represents an emerging opportunity for the mild hybrid vehicle market. The adoption is primarily driven by rising fuel costs, gradual implementation of Euro-6–equivalent emission standards, and the growing demand for fuel-efficient passenger vehicles. While BEV penetration remains limited due to infrastructure and affordability challenges, mild hybrids offer a practical solution for improving efficiency without requiring charging ecosystems. OEMs are increasingly introducing mild hybrid variants in select models to cater to regulatory changes and evolving consumer preferences, supporting gradual market expansion across these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading OEMs Deploy Mild Hybrid Systems across Multiple High-Volume Platforms to Stay Ahead of Competition

The mild hybrid vehicle (MHEV) market is moderately consolidated, characterized by the strong presence of a limited number of global automotive OEMs with large-scale production capabilities, established electrification roadmaps, and deep integration with Tier-1 suppliers. While several regional and niche players offer mild hybrid variants, the market leadership is concentrated among major OEM groups that deploy mild hybrid systems across multiple high-volume platforms, especially in Europe and Asia Pacific. High R&D costs, regulatory complexity, and the need for supplier ecosystem integration act as entry barriers, preventing the market from becoming highly fragmented. At the same time, competition remains intense as OEMs race to standardize 48V mild hybrid architectures to meet emission norms and protect ICE-based portfolios during the transition to full electrification.

Volkswagen Group is one of the leading players in the global market, driven by its aggressive electrification strategy and broad vehicle portfolio spanning mass-market and premium brands such as Volkswagen, Audi, Skoda, and SEAT. The group has widely adopted 48V mild hybrid systems across gasoline and diesel platforms, particularly in Europe, to comply with stringent EU CO₂ regulations.

LIST OF KEY MILD HYBRID VEHICLE COMPANIES PROFILED

- Volkswagen Group (Germany)

- Toyota Motor Corporation (Japan)

- Hyundai Motor Group (South Korea)

- BMW Group (Germany)

- Honda Motor Co., Ltd. (Japan)

- Mercedes-Benz Group (Germany)

- Renault Group (France)

- Suzuki Motor Corporation (Japan)

- Ford Motor Company (U.S.)

- Stellantis (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- July 2025: EcoCar magazine honored the Fiat 600 Hybrid as the “Best Mild Hybrid Compact SUV” at the Electrified Top 50 Awards 2025. This recognition highlights the model’s strong blend of design, build quality, technological innovation, and affordability. Offered with both fully electric and hybrid powertrain options, the Fiat 600 stands out as a compelling value proposition for consumers looking for a versatile and cost-effective compact SUV.

- January 2025: Hyundai Motors Group announced platform-level optimization of 48V MHEVs to improve fuel efficiency and reduce system costs.

- March 2025: Stellantis confirmed increased production capacity for 48V MHEV-equipped vehicles across European plants.

- September 2024: Mercedes-Benz Group introduced upgraded ISG-based mild hybrid architecture to improve efficiency and NVH performance.

- April 2023: Renault Group introduced 12V and 48V mild hybrid powertrains across Clio and Captur lineups.

REPORT COVERAGE

The global mild hybrid vehicle market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Architecture, By Component, and Region |

|

By Vehicle Type |

· Sedan/ Hatch back · SUV · Light commercial Vehicle · Heavy Commercial Vehicle |

|

By Architecture |

· 12V Mild Hybrid Systems · 24V Mild Hybrid Systems · 48V Mild Hybrid Systems |

|

By Component |

· Starter Generator / Electric Motor · Battery Pack · DC-DC Converter · Power Electronics / Inverter · Others |

|

By Geography |

· North America (By Vehicle Type, By Lighting Position, By Lighting Type, By Functionality, By Sales Channel and Country) o U.S. (Vehicle Type) o Canada (Vehicle Type) o Mexico (Vehicle Type) · Europe (By Vehicle Type, By Lighting Position, By Lighting Type, By Functionality, By Sales Channel and Country) o Germany (Vehicle Type) o U.K. (Vehicle Type) o France (Vehicle Type) o Rest of Europe (Vehicle Type) · Asia Pacific (By Vehicle Type, By Lighting Position, By Lighting Type, By Functionality, By Sales Channel and Country) o China (Vehicle Type) o India (Vehicle Type) o Japan (Vehicle Type) o South Korea (Vehicle Type) o Rest of Asia Pacific (Vehicle Type) · Rest of the World (By Vehicle Type, By Lighting Position, By Lighting Type, By Functionality, By Sales Channel and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 108.67 billion in 2025 and is projected to reach USD 187.47 billion by 2034.

In 2025, the Europe market value stood at USD 44.01 billion.

The market is expected to exhibit a CAGR of 6.3% during the forecast period of 2026-2034.

The SUV segment leads the market by vehicle type.

Stringent emission regulations and cost-effective electrification are key factors expected to drive the market growth.

Volkswagen Group, Toyota Motor Corporation, Hyundai Motor Group, BMW Group, and Mercedes-Benz Group are some of the top players in the market.

Europe dominates the market with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us