Off-Highway Electric Vehicle Market Size, Share & Industry Analysis, By Type (BEV and HV), By Application (Construction, Agricultural, and Mining), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

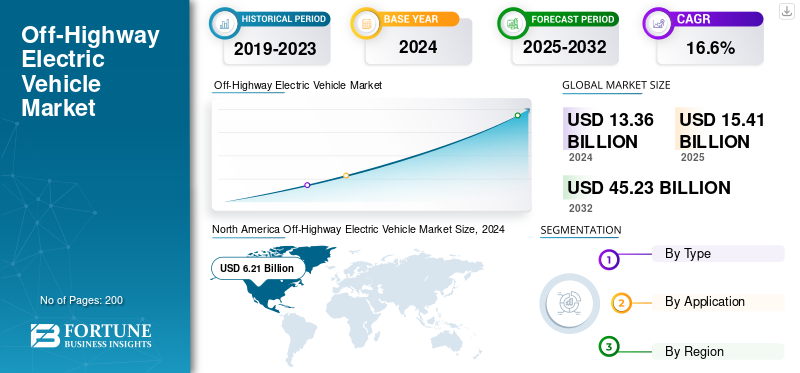

The global off-highway electric vehicle market size was USD 15.41 billion in 2025 and is projected to grow from USD 17.84 billion in 2026 to USD 59.51 billion by 2034, exhibiting a 16.25% CAGR during the forecast period. North America dominated the market with a market share of 46% in 2025.

The market is driven by accelerating decarbonization mandates, tightening site-level emissions standards, and the operational need to reduce fuel dependency in non-road industrial environments. The Off-highway Electric Vehicles market represents a structurally distinct segment of the broader electrification landscape, shaped by duty-cycle intensity, localized operating zones, and high equipment utilization rates. Adoption is primarily concentrated in construction, mining, and agricultural applications where predictable routes, controlled worksites, and centralized fleet ownership support electrification feasibility.

Unlike on-road vehicles, off-highway platforms prioritize torque delivery, load handling, and durability over driving range. This requirement shapes both product design and purchasing behavior. Buyers evaluate electric equipment based on total lifecycle economics, uptime reliability, and integration with existing site infrastructure. As a result, the Off-highway Electric Vehicles market growth follows phased replacement cycles rather than rapid fleet turnover.

Battery electric vehicles gain traction in compact and medium-duty equipment, while hybrid variants bridge performance gaps in heavy-duty and remote operations. Equipment electrification is often paired with digital fleet management and energy optimization systems, reinforcing operational value beyond emissions reduction.

Regionally, Europe and parts of North America lead early adoption due to regulatory pressure and corporate sustainability targets. Asia-Pacific shows selective uptake aligned with infrastructure readiness and industrial policy. Overall, the Off-highway Electric Vehicles market size expands steadily, supported by regulatory alignment, improving battery performance, and rising acceptance among industrial fleet operators focused on long-term cost stability and compliance-driven modernization.

The off-highway electric vehicles are experiencing significant growth driven by increasing environmental concerns, stringent emission regulations, and the rising demand for sustainable and energy-efficient solutions across industries such as agriculture, construction, and mining. Governments worldwide are implementing policies to reduce carbon footprints, encouraging the adoption of electric construction vehicles over traditional diesel-powered machinery. Technological advancements in battery technology, such as improved energy density and faster charging capabilities, are also enhancing the performance and viability of off-highway electric vehicles. Additionally, the lower operating and maintenance costs of electric vehicles compared to Internal Combustion Engine (ICE) vehicles make them an attractive option for businesses aiming to reduce long-term expenses.

Internal Combustion Engine (ICE) vehicles typically rely on fossil fuels, leading to higher greenhouse gas emissions and air pollutants. In contrast, Electric Vehicles (EVs) are designed to operate on electricity, which can be generated from renewable sources, resulting in significantly lower emissions during operation. While the production and disposal of EV batteries can also have environmental impacts, the overall lifecycle emissions of EVs tend to be lower than those of ICE vehicles, particularly as the energy grid becomes greener.

According to Schaeffler, when considering the CO₂ emissions from construction machinery, excavators and wheel loaders account for the largest proportion, at 45% and 18%, respectively.

The construction and mining sectors, in particular, are witnessing a surge in demand for electric equipment due to the need for quieter, emission-free operations in urban and environmentally sensitive areas. Despite challenges such as high initial costs and limited charging infrastructure in remote locations, the market is poised for robust growth as manufacturers invest in R&D and governments offer incentives to accelerate the transition to electric mobility. Overall, the market is expected to expand significantly in the coming years, driven by sustainability goals and technological innovation.

Download Free sample to learn more about this report.

Market Trends

Increasing Focus on Sustainability and Decarbonization is the Latest Trend

The increasing focus on sustainability and decarbonization is a major driving force behind the growth of the market. Governments and organizations worldwide are intensifying efforts to combat climate change by reducing greenhouse gas emissions, particularly from industries such as construction, agriculture, and mining, which traditionally rely on diesel-powered machinery. Off-highway electric vehicles offer a cleaner, greener alternative, producing zero tailpipe emissions and significantly lowering the carbon footprint of these sectors. Policies and regulations, such as stricter emission standards and carbon reduction targets, are compelling businesses to transition to electric solutions.

Additionally, many governments are offering incentives, such as subsidies, tax rebates, and grants, to encourage the adoption of off-highway electric equipment. Corporate sustainability goals further support this shift, as companies aim to align with environmental, social, and governance (ESG) principles and meet stakeholder expectations for eco-friendly practices. As a result, the market is gaining momentum, with manufacturers investing heavily in the development of electric machinery to meet the growing demand for sustainable and energy-efficient solutions. This trend supports global decarbonization efforts and positions off-highway electric vehicles as a key component of the future of industrial operations.

The Off-highway Electric Vehicles market trends reflect a measured shift from pilot deployments toward early-scale commercialization. Electrification is progressing selectively, concentrated in applications with predictable duty cycles, controlled environments, and centralized asset management. Construction and agricultural sites increasingly serve as initial adoption zones, while mining applications advance more cautiously due to power density and endurance requirements.

Customer demand trends indicate growing acceptance among fleet operators focused on emissions compliance, noise reduction, and operating cost predictability. Buyers increasingly assess electric equipment as part of broader site electrification strategies rather than standalone assets. This shifts procurement criteria toward system compatibility, charging integration, and service support depth.

Industry drivers remain policy-led but commercially reinforced. Emissions caps, urban construction restrictions, and sustainability reporting obligations accelerate demand. At the same time, fuel price volatility and maintenance cost exposure strengthen the economic case for electrification in high-utilization fleets.

Competitive trends show established original equipment manufacturers expanding electric portfolios, while specialized entrants focus on niche equipment categories. Partnerships between battery suppliers, drivetrain integrators, and equipment manufacturers are common, reducing development risk and shortening time-to-market.

Product trends emphasize modular platforms, scalable battery packs, and hybrid architectures. Manufacturers prioritize flexibility to address varied load profiles across applications. Technology and innovation trends center on battery durability, thermal management, and power electronics optimized for harsh environments.

Regulatory and compliance trends increasingly favor zero-emission worksites, particularly in Europe. Global influences vary, with Asia-Pacific adoption tied closely to industrial policy and infrastructure readiness. Collectively, these trends support steady Off-highway Electric Vehicles market growth anchored in operational practicality rather than rapid disruption.

Download Free sample to learn more about this report.

MARKEY DYNAMICS

MARKET DRIVERS

Advancement in Battery Technology to Drive Market Growth

Technological advancements in battery technology are another critical factor fueling market growth. Improvements in lithium-ion batteries, solid-state batteries, and energy storage systems have enhanced the performance, range, and efficiency of off-highway EVs, making them more viable for demanding applications in construction, agriculture, and mining. Additionally, the development of fast-charging infrastructure and battery-swapping solutions is addressing challenges related to charging times and operational downtime.

For Instance, in 2022, according to the International Energy Agency (IEA), the global investment in battery technology research and development reached USD 86 billion. This investment is driving innovations such as solid-state batteries, which promise even higher energy densities and faster charging times.

Several structural forces underpin the Off-highway Electric Vehicles market growth, shaping adoption across construction, agriculture, and mining applications. The most influential driver is regulatory pressure to reduce emissions in non-road machinery. Governments increasingly mandate lower exhaust output and noise levels, particularly in urban construction zones and environmentally sensitive areas. Electric equipment enables compliance without sacrificing operational capability.

Operating cost optimization represents another major driver. Fleet operators face rising fuel expenses, volatile diesel pricing, and tightening maintenance margins. Electric drivetrains reduce mechanical complexity, lowering service intervals and downtime. Over time, predictable energy costs improve the total cost of ownership, especially in high-utilization fleets.

Worksite electrification strategies also accelerate demand. Construction and industrial operators increasingly integrate renewable power, energy storage, and charging infrastructure at centralized sites. Off-highway electric vehicles align naturally with these ecosystems, strengthening adoption where grid access or on-site generation is available.

Noise reduction requirements influence equipment selection. Electric machinery operates with significantly lower acoustic output, enabling extended working hours and compliance with urban noise regulations. This driver is strongest in municipal construction and indoor or semi-enclosed industrial environments.

Technological maturity supports adoption. Advances in battery durability, power electronics, and thermal management improve performance consistency under heavy loads. Evidence includes expanding pilot fleets transitioning into commercial deployments.

Target segments most affected include compact construction equipment, material handling machinery, and agricultural vehicles operating on fixed routes. Mining adoption remains selective but growing, particularly in underground operations prioritizing air quality and worker safety.

MARKET RESTRAINTS

Limited Charging Infrastructure to Limit Market Growth

The limited availability of charging infrastructure is a significant restraining factor for the off-highway electric vehicle market growth. Unlike on-road electric vehicles, which benefit from a growing network of public charging stations, electric construction equipment often operates in remote or rural areas such as construction sites, agricultural fields, and mining locations, where charging infrastructure is sparse or nonexistent. This lack of infrastructure can lead to operational challenges, including prolonged downtime for charging and logistical difficulties in transporting vehicles to charging points.

According to a report by the International Energy Agency (IEA), the global ratio of electric vehicles to public charging points was approximately 8:1 in 2022, highlighting the existing gap in charging infrastructure. For off-highway applications, this gap is even more pronounced due to the specialized nature of the equipment and the demanding environments in which they operate.

Despite favorable long-term dynamics, several constraints continue to moderate the Off-highway Electric Vehicles market growth. High upfront acquisition costs remain the most persistent barrier. Electric powertrains, advanced battery systems, and specialized power electronics increase capital expenditure compared with conventional diesel equipment. This limits adoption among cost-sensitive operators and small fleet owners.

Battery performance limitations under extreme operating conditions also constrain broader deployment. Off-highway vehicles frequently operate under high loads, uneven terrain, and extended duty cycles. In cold climates or high-temperature mining environments, battery efficiency and degradation rates become operational concerns. These factors require oversizing battery packs, further increasing costs and weight. Charging infrastructure availability represents another structural restraint. Many construction sites, remote agricultural fields, and mining locations lack reliable grid access. Temporary or mobile charging solutions remain costly and operationally complex. This restricts adoption primarily to fixed or semi-fixed sites with predictable energy availability.

Operational flexibility concerns influence buyer decisions. Diesel equipment offers rapid refueling and continuous operation, which electric alternatives struggle to match in high-intensity applications. Downtime for charging can disrupt workflows unless carefully planned, reducing productivity in time-sensitive projects. Supply chain constraints add further pressure. Battery material sourcing, power semiconductor availability, and specialized component manufacturing introduce procurement risk. Lead times can be unpredictable, complicating fleet planning.

These restraints affect segments unevenly. Large construction firms with centralized operations manage constraints more effectively. Smaller contractors, remote agricultural users, and open-pit mining operations face greater adoption challenges. As a result, market penetration progresses selectively rather than uniformly across applications and regions.

Market Opportunities

Investment In Infrastructure To Provide Ample Opportunities Within The Market

Investment in charging infrastructure is crucial for the growth of the off-highway electric vehicle market, as the availability and accessibility of charging stations directly influence the transition from conventional combustion-powered machinery to electric alternatives. Given the unique operational environments of off-highway vehicles, such as construction sites, mining locations, and agricultural fields, it is essential to develop specialized charging solutions that cater to these specific needs.

Collaborating with energy companies, infrastructure providers, and industry stakeholders can facilitate the establishment of charging stations strategically located at operational sites, minimizing downtime and maximizing productivity. These partnerships can also promote the deployment of fast-charging technologies that accommodate the demanding usage patterns typical of off-highway applications. Furthermore, integrating renewable energy sources, such as solar or wind, into the charging infrastructure can further enhance sustainability, making off-highway electric vehicles a more attractive option for businesses seeking to reduce their carbon footprint. Ultimately, a robust charging infrastructure not only alleviates concerns about range anxiety but also incentivizes the adoption of electric vehicles, driving growth in the E-OV market.

The Off-highway Electric Vehicles market presents several high-quality opportunities as electrification expands beyond early adopters. Construction equipment represents the most immediate opportunity. Urban projects increasingly impose emissions and noise restrictions, favoring electric excavators, loaders, and compact machinery. These environments offer predictable duty cycles and charging access, supporting faster adoption.

Agricultural electrification creates another growth avenue. Electric tractors and utility vehicles suit controlled farm operations where energy access is stable. Precision agriculture further amplifies demand, as electric platforms integrate more easily with digital monitoring, autonomous functions, and variable power management. This segment benefits from rising sustainability requirements across food supply chains.

Mining applications offer a longer-term opportunity, particularly for underground operations. Electric vehicles reduce ventilation costs, heat generation, and worker exposure to exhaust. As battery energy density improves, electric haul trucks and loaders gain commercial viability in confined environments where operational efficiency gains are measurable. Technology-driven opportunities continue to expand. Advances in battery chemistry, thermal management, and modular power systems improve vehicle range and durability. Swappable battery architectures reduce downtime and address charging constraints in remote locations. Integration of telematics and energy management software enables predictive maintenance and optimized fleet utilization.

Geographic expansion provides additional upside. Asia-Pacific and parts of Europe benefit from policy-driven electrification mandates and infrastructure investment. Emerging markets adopt electric off-highway vehicles selectively in government-backed projects and industrial zones. Regulatory alignment supports opportunity creation. Incentives tied to emissions reduction, urban air quality, and occupational safety improve the total cost of ownership. Sustainability and Environmental, Social, and Governance considerations increasingly influence procurement decisions, positioning electric off-highway vehicles as strategic assets rather than experimental alternatives.

MARKET CHALLENGES

Competition with Established Technologies to Bring New Challenges for the Market Players.

The off-highway electric vehicle market faces significant competition from established diesel-powered machinery, which has long dominated the industry due to its well-established infrastructure and operational familiarity. Diesel vehicles benefit from a global network of refueling stations, a wealth of service and maintenance expertise, and a reliable performance track record, creating a strong preference among operators who are accustomed to their proven capabilities in demanding environments such as construction, mining, and agriculture. This entrenched reliance on diesel technology fosters resistance to changing established habits and preferences, making it challenging for electric alternatives to gain traction. Additionally, many operators view diesel machines as being synonymous with reliability and efficiency, factors that are crucial for the high-stakes operations typical of off-highway applications.

Transitioning to electric vehicles not only necessitates overcoming this inertia, but it also requires demonstrating clear advantages, such as lower operating costs, reduced emissions, and improved performance, to encourage users to make the shift. As the E-OV market evolves, addressing these competitive challenges through innovation, enhanced charging infrastructure, and compelling value propositions will be essential for attracting the traditional user base that has historically relied on diesel-powered equipment.

SEGMENTATION ANALYSIS

By Type

Hybrid Vehicle Segment Dominates Market Owing to Increasing Demand in the Construction Sector

The market is segmented based on technology: BEV and HV.

The hybrid vehicle (HV) segment is currently dominating the market, driven primarily by the increasing demand from the construction sector. The hybrid vehicle (HV) segment will account for 72.54% market share in 2026. Hybrid off-highway vehicles, which combine Internal Combustion Engines (ICE) with electric propulsion systems, offer a balanced solution that addresses the limitations of fully electric vehicles while providing significant environmental and operational benefits. In the construction industry, where heavy machinery operates in demanding and often remote environments, hybrid vehicles provide the flexibility of using diesel power when needed, and electric power for quieter, emission-free operations in urban or sensitive areas.

Hybrid Electric Vehicles combine internal combustion engines with electric propulsion components. This architecture offers a transitional pathway for electrification in off-highway applications. HEVs reduce fuel consumption and emissions while retaining operational flexibility.

Construction applications dominate HEV adoption. Large excavators, cranes, and earthmoving equipment benefit from hybrid systems that recover energy during braking and load lowering. These systems improve fuel efficiency without requiring extensive charging infrastructure. Contractors operating across diverse sites favor HEVs due to their adaptability and extended operating range.

In agriculture, HEVs are used in high-power tractors and harvesters where continuous operation is critical. Hybrid systems provide supplemental power during peak loads while maintaining refueling convenience. This configuration supports productivity in large-scale farming operations where downtime carries high opportunity costs. Mining applications leverage HEVs primarily in surface operations. Hybrid haul trucks reduce fuel consumption and emissions while supporting long haul cycles. Mining operators value HEVs as a risk-mitigated approach, balancing sustainability goals with operational reliability.

HEVs face fewer infrastructure constraints than BEVs, but their complexity increases maintenance requirements. Additionally, long-term regulatory pressure may limit hybrid viability as emissions standards tighten. Even so, HEVs maintain a significant Off-highway Electric Vehicles market share in heavy-duty segments where full electrification remains technically or economically challenging.

The Battery Electric Vehicle (BEV) segment is poised for significant growth in the market, driven by advancements in battery technology, declining costs, and increasing regulatory pressure to reduce emissions. BEVs, which rely entirely on electric power, offer zero-emission solutions that align with global sustainability goals and stringent environmental regulations. Moreover, governments worldwide are offering incentives to promote the adoption of electric vehicles. For example, the European Union’s Green Deal and the U.S. Inflation Reduction Act include subsidies and tax benefits for electric vehicle purchases, further accelerating BEV adoption.

Battery Electric Vehicles represent the most advanced and commercially deployed segment within the Off-highway Electric Vehicles market. BEVs rely entirely on onboard battery systems to deliver propulsion and auxiliary power. Their adoption is strongest in applications with predictable workloads, controlled environments, and access to charging infrastructure.

In construction, BEVs are increasingly deployed for compact and mid-sized equipment, including excavators, loaders, and telehandlers. Urban construction sites favor BEVs due to zero tailpipe emissions and reduced noise levels. These attributes support compliance with municipal regulations and improve worker safety. BEVs also offer high torque at low speeds, which aligns well with earthmoving and lifting operations.

Agricultural BEV adoption centers on utility tractors, material handlers, and support vehicles. Farms with centralized operations and access to grid power can integrate BEVs into daily workflows. Electric drivetrains simplify maintenance by eliminating complex transmission components, improving equipment uptime during peak seasons. Precision agriculture further strengthens BEV value by enabling seamless integration with digital control systems.

Despite these advantages, BEVs face challenges related to charging time, battery replacement costs, and cold-weather performance. These constraints limit adoption in remote or infrastructure-constrained regions. Nonetheless, BEVs account for a growing share of the Off-highway Electric Vehicles market size, particularly in regulated environments with strong emissions policies.

By Application

To know how our report can help streamline your business, Speak to Analyst

Increase in Infrastructure Activities is Anticipated to Boost Construction Segment Growth

Based on application, the market is segregated into construction, agricultural, and mining.

The construction segment dominated the market in 2024, driven by the increasing demand for sustainable and efficient machinery in urban and infrastructure development projects. The construction industry is under growing pressure to reduce emissions and noise pollution, particularly in urban areas where environmental regulations are becoming stricter. Off-highway electric vehicles, including electric excavators, loaders, and cranes, offer a zero-emission alternative to traditional diesel-powered equipment, making them highly attractive for construction companies aiming to comply with these regulations and improve their environmental footprint. The construction segment is expected to lead the market, contributing 50.17% globally in 2026.

Construction represents the largest application segment within the Off-highway Electric Vehicles market. Adoption is driven by urbanization, infrastructure renewal, and regulatory pressure on emissions and noise. Electric construction equipment supports compliance with environmental standards while enabling work in noise-sensitive zones.

BEVs dominate compact equipment categories. Mini excavators, skid steer loaders, and compact loaders are well-suited to electric power due to limited duty cycles and centralized charging. Rental companies increasingly adopt electric fleets to meet contractor demand and regulatory compliance.

Hybrid systems prevail in larger construction equipment. High-power machines require extended operating hours and mobility across sites. Hybrid architectures deliver efficiency gains while preserving operational flexibility. This dual-track adoption supports broad market penetration across equipment classes. Technology integration enhances construction electrification. Telematics, energy monitoring, and fleet optimization tools improve utilization and reduce operating costs. Construction remains the primary contributor to the Off-highway Electric Vehicles market growth due to favorable economics and regulatory alignment.

Moreover, the agricultural and mining segments are also anticipated to gain significant growth during the forecast period. The growth is driven by the increasing need for sustainable and efficient solutions in these industries. In agriculture, the adoption of electric vehicles, such as electric tractors, harvesters, and sprayers, is gaining momentum as farmers seek to reduce operational costs and minimize their environmental impact. In the mining sector, the shift toward electric vehicles is being driven by the need to reduce emissions, improve safety, and lower operating costs, particularly in underground mining operations. Diesel-powered machinery in mines contributes to air pollution and poses health risks to workers, making electric vehicles a safer and cleaner alternative.

Agriculture represents a growing but more selective segment. Adoption depends on farm size, crop type, and regional energy infrastructure. Electric utility vehicles and small tractors are increasingly used for material handling, planting, and maintenance tasks.

BEVs offer advantages in controlled farm environments. Reduced noise benefits livestock operations, while lower operating costs improve margins. Integration with autonomous systems and precision agriculture platforms further enhances value. Hybrid systems serve larger agricultural machinery. Tractors and harvesters require sustained power output and long operating hours. Hybrid drivetrains support fuel efficiency gains without disrupting established workflows.

Regional variation shapes adoption. Developed markets with stable energy infrastructure and sustainability incentives show stronger uptake. Emerging markets adopt electric agricultural equipment selectively, often through pilot programs or government-supported initiatives. Mining adoption reflects a longer investment horizon and higher technical barriers. Electric vehicles offer compelling benefits in underground mining, including reduced ventilation costs, improved air quality, and lower heat generation.

BEVs are increasingly deployed for underground loaders and haulage vehicles. These applications deliver quantifiable operational savings, supporting investment justification. Battery swapping and fast charging mitigate downtime concerns. Surface mining remains dominated by hybrid solutions. Large payload requirements and extended routes challenge BEV feasibility. Hybrid trucks offer emissions reduction while maintaining performance.

Mining electrification progresses cautiously, driven by safety, sustainability, and cost optimization. While adoption volumes remain lower, mining contributes disproportionately to long-term Off-highway Electric Vehicles market growth due to high equipment value and lifecycle savings.

Regional Insights

The market is segmented into North America, Europe, Asia Pacific, and the Rest of the World based on the region.

North America Off-Highway Electric Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Off-Highway Electric Vehicles Market Analysis

North America Holds the Highest Share, Driven by Increasing Demand for Electric Equipment in Various Sectors

The market in North America reached USD 7.09 Billion in 2025, representing 46.00% of total market revenue, and is projected to reach USD 8.12 Billion in 2026. North America commands the largest off-highway electric vehicle market share. As industries strive to enhance efficiency and sustainability, the transition to electric-powered machinery is becoming increasingly prevalent. In construction, electric vehicles are favored for their ability to operate quietly and with reduced emissions, making them ideal for urban projects where environmental regulations are stringent. Similarly, in mining, electric vehicles lower operational costs, improve safety, and reduce the carbon footprint of mining operations.

The agriculture sector is also embracing electric technology as farmers seek to adopt more sustainable practices while maximizing productivity through advanced electric machinery. This growing trend reflects a broader commitment to reducing environmental impact and promoting innovation across industries, positioning North America as a leader in the off-highway electric vehicle industry.

North America shows structured adoption driven by emissions regulation, labor safety standards, and fleet electrification strategies. Construction leads demand, supported by public infrastructure programs. Mining electrification progresses through underground applications. OEM presence, financing access, and charging pilots strengthen adoption. Market growth remains pragmatic, shaped by total cost ownership and regulatory clarity rather than aggressive mandates.

United States Off-highway Electric Vehicles Market:

The United States represents the largest regional contributor to the Off-highway Electric Vehicles market size. Adoption concentrates on urban construction and underground mining. Federal and state incentives support pilot deployments, while private operators prioritize hybrid solutions for flexibility. Strong OEM ecosystems and rental fleet participation accelerate market penetration, though infrastructure availability continues to shape adoption pace.

The U.S. is anticipated to lead the market. The United States is poised to lead the market in North America due to several favorable conditions that enhance its position as a frontrunner in this emerging sector. Substantial investments in clean energy initiatives and infrastructure development have created a conducive environment for the adoption of electric vehicles, including off-highway machinery. U.S. regulatory frameworks increasingly emphasize sustainability, incentivizing manufacturers and operators to transition to lower-emission solutions.

Europe Off-Highway Electric Vehicles Market Analysis

Europe contributed approximately USD 5.43 Billion to the global market in 2025, accounting for 35.23% share, and is expected to reach USD 6.32 Billion in 2026. Europe holds the second-largest share in the off-highway electric vehicle industry, driven by a combination of regulatory support, technological advancements, and a strong focus on sustainability. European governments are implementing stringent environmental regulations that encourage the adoption of electric vehicles across various sectors, including construction, mining, and agriculture.

Europe demonstrates policy-led adoption anchored in emissions compliance and sustainability targets. Construction electrification dominates, particularly in urban and low-emission zones. Hybrid equipment remains relevant for heavy-duty use. Regulatory consistency and carbon reduction commitments support long-term Off-highway Electric Vehicles market growth across construction, agriculture, and selective mining applications.

Germany Off-Highway Electric Vehicles Market

Germany emphasizes industrial efficiency and emissions reduction. Construction and material handling lead adoption, supported by advanced manufacturing capabilities and pilot programs. Hybrid systems retain importance for heavy equipment. Strong engineering expertise and regulatory enforcement position Germany as a technology reference market within Europe’s off-highway electrification landscape.

United Kingdom Off-Highway Electric Vehicles Market

The United Kingdom focuses on urban construction, electrification, and sustainability compliance. Noise restrictions and carbon targets drive BEV deployment in compact equipment. Hybrid adoption supports larger machinery. Government-backed infrastructure initiatives and rental fleet electrification strengthen market development, though broader adoption remains sensitive to cost and infrastructure readiness.

Asia-Pacific Off-Highway Electric Vehicles Market Analysis

In 2025, the Asia Pacific market stood at USD 2.05 Billion, representing 13.32% of global demand, and is projected to grow to USD 2.42 Billion in 2026. The Asia Pacific region holds a significant share in the off-highway electric vehicle sector, driven by rapid industrialization, urbanization, and increasing investments in infrastructure development. Countries such as China, Japan, and India are at the forefront of this growth, as they recognize the need for sustainable solutions in sectors such as construction, mining, and agriculture. As industries in the region continue to prioritize innovation and sustainability, the demand for off-highway electric vehicles is expected to rise, solidifying the region's position as a significant player in this evolving market.

Asia-Pacific exhibits the fastest Off-highway Electric Vehicles market growth, driven by infrastructure expansion and manufacturing scale. China leads volume deployment, while Japan emphasizes reliability and automation. Construction dominates demand, with mining and agriculture adopting selectively. Regional diversity results in uneven adoption but strong long-term potential.

Japan Off-highway Electric Vehicles Market

Japan prioritizes reliability, automation, and energy efficiency. Electric off-highway vehicles support construction, disaster response, and controlled industrial environments. Adoption remains cautious, emphasizing hybrid architectures and advanced battery management. Strong OEM innovation and precision engineering underpin gradual but stable market expansion.

China Off-Highway Electric Vehicles Market

China represents the largest production base and a major demand center. Government support, manufacturing scale, and urban construction activity accelerate BEV adoption. Mining and agriculture adopt selectively. Domestic OEMs drive rapid deployment, positioning China as a critical contributor to the global Off-highway Electric Vehicles market share.

Latin America Off-Highway Electric Vehicles Market Analysis

Latin America remains an emerging market characterized by selective adoption. Mining leads demand due to underground safety benefits, while construction pilots grow in major cities. Economic volatility and infrastructure constraints limit scale, but sustainability commitments and international partnerships support gradual market development.

Middle East & Africa Off-Highway Electric Vehicles Market Analysis

The Middle East & Africa region shows early-stage adoption centered on flagship construction projects and mining operations. Energy availability supports electrification pilots, particularly underground mining. Market growth depends on infrastructure investment and regulatory incentives, positioning the region as a longer-term opportunity rather than a near-term volume driver.

Rest of the World

Rest of the World recorded a market size of USD .84 Billion in 2025, capturing 5.45% of the global market share, and is projected to reach USD .97 Billion in 2026.

Off-Highway Electric Vehicles Industry Competitive Landscape

The competitive landscape of the Off-highway Electric Vehicles market remains moderately concentrated, shaped by established original equipment manufacturers (OEMs), emerging electric specialists, and strategic technology partners. Incumbent players leverage deep application knowledge, global dealer networks, and customer trust built through decades of off-highway equipment delivery. Their positioning emphasizes gradual electrification, reliability, and compatibility with existing fleet operations.

Leading OEMs typically pursue hybrid-first strategies. This approach reduces operational risk while supporting emissions compliance and fuel efficiency. Strengths include robust after-sales infrastructure, financing capabilities, and integrated service offerings. However, these players often face slower innovation cycles and higher cost structures, limiting rapid BEV scalability in heavy-duty segments.

Emerging electric-focused manufacturers occupy niche positions. These players target compact construction equipment, underground mining vehicles, and specialty agricultural machinery. Their competitive advantage lies in purpose-built electric platforms, simplified drivetrains, and faster product iteration. Weaknesses include limited global reach, smaller service networks, and dependence on external battery suppliers.

Strategic partnerships increasingly define competition. OEMs collaborate with battery manufacturers, software providers, and energy companies to strengthen electric ecosystems. Joint development reduces capital risk and accelerates technology readiness. Rental companies and fleet operators also play a strategic role, influencing adoption through pilot programs and standardized procurement.

Geographically, competition varies. Asia-Pacific markets favor domestic manufacturers with scale advantages, while Europe rewards compliance-oriented innovation. North America emphasizes performance validation and total cost metrics. Across regions, differentiation increasingly depends on lifecycle support, digital monitoring capabilities, and modular electrification strategies.

The competitive landscape of the off-highway electric vehicle market is characterized by a dynamic interplay of established industry leaders and emerging innovators, all vying for a significant share in this rapidly evolving sector. Key players include traditional heavy machinery manufacturers like Caterpillar, John Deere, and Volvo Group, which are increasingly investing in electric technologies and diversifying their product lines to include electric variants of their popular models. These companies leverage their extensive experience, brand recognition, and existing customer relationships to promote new electric offerings. Concurrently, new entrants and startups, such as Nikola Corporation, Lordstown Motors, and Xos Trucks, are disrupting the market with specialized electric solutions that cater to niche applications and emphasize sustainability.

KEY INDUSTRY PLAYERS

Increase in Demand for Electric Vehicles in Different Sectors is Anticipated to Bring Ample Opportunities for the Market

Caterpillar is poised to be a leading key player in the market. As a prominent manufacturer in the construction and mining sectors, Caterpillar has been actively investing in electric technology to enhance the efficiency and sustainability of its machinery. The company’s focus on developing cutting-edge electric solutions enables it to meet the growing demand for environmentally friendly equipment that complies with stringent emission regulations.

The market is increasingly becoming consolidated, characterized by a few dominant players that hold significant market shares and influence over industry trends. Major companies such as Caterpillar, Volvo, and Komatsu are leading the charge with substantial investments in research and development, enabling them to innovate and deliver advanced electric solutions. These established firms benefit from economies of scale, robust supply chains, and strong brand recognition, allowing them to compete against smaller entrants effectively.

LIST OF KEY OFF-HIGHWAY ELECTRIC VEHICLE COMPANIES PROFILED

- Caterpillar (U.S.)

- Volvo Group (Sweden)

- Komatsu (Japan)

- Deere & Company (U.S.)

- Sandvik AB (Sweden)

- Hitachi Construction Machinery Co., Ltd (Japan)

- Epiroc Mining Limited (India)

- Kobelco Construction Machinery Co., Ltd (Japan)

- J C Bamford Excavators Ltd (U.K.)

- CNH Industrial N.V. (Italy)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Caterpillar expanded its off-highway electrification portfolio, introducing battery-electric and hybrid construction prototypes to reduce emissions while maintaining heavy-duty performance across infrastructure and mining applications.

- July 2024: Volvo Construction Equipment advanced electric compact machinery, deploying next-generation battery systems to support urban construction projects requiring low noise and zero-emission operation.

- October 2024: Komatsu strengthened hybrid off-highway platforms, integrating energy recovery systems to improve fuel efficiency and operational flexibility across mining and large construction equipment.

- February 2025: Hitachi Construction Machinery partnered with battery suppliers, enhancing thermal management and durability for electric excavators used in demanding construction environments.

- May 2025: Sandvik expanded electric underground mining solutions, focusing on battery swapping and automation capabilities to improve productivity, safety, and energy efficiency in confined mining operations.

REPORT COVERAGE

The market report provides detailed market analysis and focuses on key aspects such as leading companies, services, and product applications. Besides this, it offers insights into the market trends and highlights vital industry developments. In addition to the factors above, it encompasses several factors that have contributed to the market's growth over recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.25% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

|

|

|

|

By Region North America ( By Type, By Application)

Europe ( By Type, By Application )

Asia Pacific ( By Type, By Application )

Rest of the World ( By Type, By Application ) |

Frequently Asked Questions

Fortune Business Insights global off-highway electric vehicle market report says that the market was valued at USD 15.41 billion in 2025 and is projected to record a valuation of USD 59.51 billion in 2034.

The market is expected to register a growth rate of 16.6% during the forecast period.

The increased shift toward vehicle electrification is anticipated to boost the off-highway electric vehicle market growth.

North America led the market in 2025.

The U.S. is expected to take the lead in the market in 2025, driven by regulatory frameworks that increasingly prioritize sustainability. These regulations create incentives for manufacturers and operators to adopt lower-emission solutions, encouraging a significant shift toward environmentally friendly practices.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us