Military Satellite Market Size, Share & Russia Ukraine War Impact Analysis, By Orbit Type (LEO, MEO, and GEO), By Offering (Satellite Manufacturing, Launch Services, and Operational Services), By Type (Nano-Micro Satellite, Small Satellite, Medium Satellite, and Heavy Satellite), By Application (ISR, Communication, and Navigation), By Satellite Component (Structures, Payload, Electric Power System, Instrument Control Unit, Propulsion System, Thermal Control Subsystem, Communication System, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

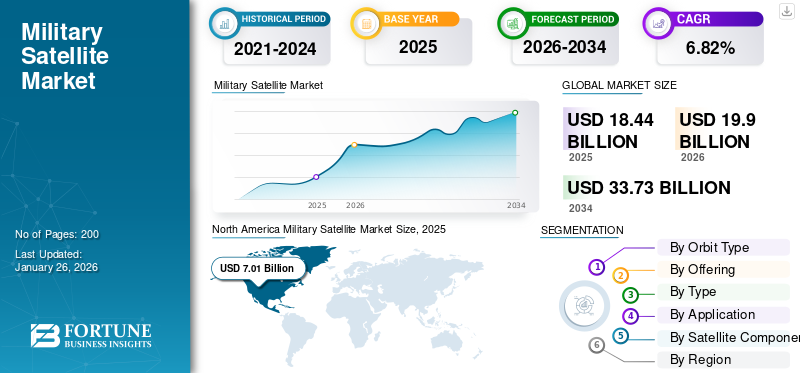

The global military satellite market size was valued at USD 18.44 billion in 2025 and is expected to grow from USD 19.9 billion in 2026 to USD 33.73 billion by 2034 at a CAGR of 6.82% over 2026-2034. North America dominated the military satellite market with a market share of 38.00% in 2025.

A military satellite is used for numerous military applications. It includes missions such as military communication, intelligence gathering, and navigation. These satellites perform functions such as intelligence gathering, navigation, secured communication, surveillance, and early warning. The data collected through these satellites have a direct impact on the operational capability of defense forces. It includes early warning related to movements collecting and communicating intelligence information to the military forces. The information of high-power military surveillance is transferred to forces through electronic and signal intelligence in remote areas.

There is an increase in demand for satellites in the military sector due to the need for secure communications, intelligence gathering, navigation, and tactical support. Key players in the military satellite market include major defense contractors such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, and L3 Harris. These companies develop satellites for the military forces of various countries through various programs to enhance the defense capabilities.

Download Free sample to learn more about this report.

Military Satellite Market Key Takeways

- 2025 Market Size: USD 18.44 billion

- 2026 Market Size: USD 19.90 billion

- 2034 Forecast Market Size: USD 33.73 billion

- CAGR: 6.82% from 2026–2034

- North America dominated the military satellite market with a 38.00% share in 2025.

- The LEO segment is projected to dominate the market with an 83.40% share in 2026.

- The satellite manufacturing segment is expected to account for 50.45% of the market share in 2026.

North America

North America held a 38.00% market share in 2025, valued at USD 7.01 billion, and is projected to reach USD 7.51 billion in 2026.

Europe

Europe accounted for 33.40% of the global market in 2025, valued at USD 6.16 billion, and is expected to reach USD 6.69 billion in 2026.

Asia Pacific

Asia Pacific contributed 25.10% of the global market in 2025, with a valuation of USD 4.63 billion, projected to grow to USD 5.01 billion in 2026.

U.S.

U.S. The military satellite market is projected to reach USD 7.41 billion by 2026.

Japan

Japan The military satellite market is projected to reach USD 0.44 billion by 2026.

Read More

Impact of Russia-Ukraine War

Surge in Demand for Military Satellites

- Real-Time ISR Capabilities:

- The conflict underscored the critical role of satellites in Intelligence, Surveillance, and Reconnaissance (ISR). Ukraine’s reliance on commercial satellites, such as Starlink for secure communications as well as Maxar and Planet Labs for battlefield imagery, highlighted gaps in traditional military systems.

- NATO members and allied nations have prioritized investments in Low-Earth Orbit (LEO) constellations and AI-driven analytics for real-time decision-making.

- The U.S. Space Force accelerated its Proliferated Warfighter Space Architecture, aiming to deploy 1,000+ small satellites by 2026 for missile tracking and secure communications.

- Defense Budget Reallocations:

- European nations increased defense spending, with the EU assigning USD 9.09 billion for space defense (2023–2027), including secure SATCOM and Earth observation. Germany’s IRIS² project (2023) and France’s CIRCE hyperspectral satellites (2024) reflect this trend.

Supply Chain Disruptions and Adaptations:

- Sanctions on Russia’s Space Sector:

- Bans on Russian rocket engines, such as RD-180 and components, forced Western countries to accelerate domestic alternatives. The U.S. prioritized Blue Origin’s BE-4 engines and ULA’s Vulcan Centaur, reducing dependency on Russian technology by 70% by 2024.

- Impact: Global launch costs increased temporarily, but reusable rockets, such as SpaceX’s Starship, mitigated long-term disruptions.

- Diversification of Component Sources: Sanctions on Russian titanium (critical for satellites) led to partnerships with Japan and Kazakhstan, while the U.S. Defense Logistics Agency stockpiled rare-earth metals in 2023.

Technological Innovation and Commercial-Military Fusion:

- Small Satellites and AI Integration:

- The war accelerated the adoption of CubeSats and microsatellites for tactical ISR. Companies such as Capella Space (synthetic aperture radar) and HawkEye 360 (RF geolocation) witnessed a 300% spike in defense contracts (2022–2024). AI tools now process satellite data in minutes versus days pre-war.

- Ukraine’s use of Palantir’s AI platform to analyze satellite imagery for targeting Russian positions.

- Cybersecurity and Anti-Jamming: Increased electronic warfare, such as the Russian jamming of Starlink, drove demand for quantum encryption, such as Qrypt’s partnerships with NATO and resilient LEO networks.

Military Satellite Market Trends

Growing Adoption of Real-Time Battlefield Intelligence Due to AI-Powered Image Processing

- AI-Powered Image Processing: Revolutionizing Real-Time Battlefield Intelligence:

Download Free sample to learn more about this report.

The integration of AI-powered image processing into military satellites is transforming battlefield decision-making by enabling rapid analysis of vast datasets, from identifying enemy movements to assessing infrastructure damage. Traditional satellite imagery analysis, which could take hours or days, is reduced to seconds due to machine learning algorithms trained on petabytes of geospatial data. According to a 2024 report by Defense News Analytics, militaries leveraging AI-driven satellite systems have reported a 40–60% reduction in target acquisition times and a 30% improvement in mission success rates.

This surge is driven by the need for real-time situational awareness in asymmetric conflicts, such as the Ukraine war, where commercial providers including Planet Labs and BlackSky delivered AI-processed imagery to track Russian artillery positions in near real-time.

- Enhanced Capabilities Driving Satellite Demand:

AI’s ability to automate image analysis while detecting camouflaged vehicles, missile launches, or troop build ups has made high-resolution, high-revisit-rate satellite constellations indispensable. Modern systems combine multi-spectral sensors, Synthetic Aperture Radar (SAR), and AI edge computing to process data in orbit, thus minimizing latency.

For instance, the U.S. National Reconnaissance Office’s (NRO) 2024 Hybrid Space Architecture Program integrates commercial AI analytics platforms such as Palantir’s Apollo with government satellites, enabling seamless data fusion for joint forces. Similarly, NATO’s 2025 AI Readiness Initiative mandates that 50% of member states’ satellite fleets deploy onboard AI processors by 2026, driving demand for upgraded or new satellite deployments.

In May 2024, under the U.S. Space Force’s Project FORGE program, the U.S. Space Force awarded a USD 1.2 billion contract to Anduril Industries and Capella Space to deploy 48 AI-enabled SAR satellites capable of autonomously identifying mobile missile launchers. Initial operational capability is slated for Q4 2025.

In September 2024, under the EU’s AI-SENTINEL Initiative, the European Defence Fund allocated USD 909 million to develop an AI-powered satellite constellation focused on border surveillance, with Airbus and Leonardo leading the consortium. The first satellite launch is planned for late 2026.

In February 2025, under India’s ISRO-Startup Partnership initiative, India’s Defence Ministry partnered with AI startup SatSure to upgrade its RISAT-2 satellites with real-time flood and insurgent activity detection, backed by a USD 300 million investment.

For instance, in November 2024, under Japan’s Counter-Hypersonic AI Constellation program, Japan’s Defense Ministry announced a USD 950 million program to deploy 12 satellites with infrared sensors and AI processors to track hypersonic glide vehicles, responding to regional threats from China and North Korea.

Increased Demand for Miniaturized Spacecraft Components for Weight Reduction

Weight is one of the most crucial aspects to be considered while designing or manufacturing any airborne machine. Miniaturization can not only save orders of magnitude in mass and volume of individual components but also allow increased redundancy and enable novel spacecraft designs and mission scenarios. These nano-microsatellites are much cheaper and faster to design, build, and launch.

Microsatellites in 62- or 63-degree inclined orbits are able to find the location and characteristics of radars. When these spacecraft are configured to coordinate with imaging satellites, they provide a comprehensive picture of the adversary’s deployments and military movements.

MARKET DYNAMICS

Market Drivers

Rising Security Concerns and Need for Reliable Surveillance to Propel Market Growth

The global military satellite market growth is significant, driven by escalating security concerns stemming from terrorism, cross-border conflicts, and geopolitical tensions. These challenges are fueling the demand for advanced surveillance and reconnaissance capabilities to ensure national security. It plays a pivotal role in providing real-time intelligence, high-resolution imagery, and secure communication platforms, enabling defense forces to monitor adversaries, track troop movements, and respond effectively to emerging threats.

Escalating Global Security Threats: The rise in terrorism-related activities, particularly in conflict-prone regions such as the Sahel, has underscored the need for robust surveillance systems. For instance, the Global Terrorism Index 2024 reported that terrorism-related deaths in the Sahel accounted for 51% of global fatalities, highlighting the urgent need for early warning systems to detect threats such as missile launches or militant activity.

Cross-border tensions, such as the ongoing Russia-Ukraine conflict, have further emphasized the importance of space-based surveillance systems integrated into military operations. In February 2025, Russia launched military satellites from the Plesetsk Cosmodrome to enhance its space-based assets for surveillance and defense purposes.

Cybersecurity and Electronic Warfare: The rise of cyber threats and electronic warfare has necessitated the development of resilient anti-jamming satellites. For instance, in February 2025, Lockheed Martin and Boeing advanced next-generation military communications satellite designs under the MUOS Service Life Extension program. Lockheed's reprogrammable payload processor and Boeing's proven 702MP satellite platform aim to address vulnerabilities in ultra-high-frequency narrowband communication networks.

Geopolitical Instability Driving Investments:Geopolitical instability has led to increased investments in resilient satellite systems to maintain strategic advantages. In March 2025, BAE Systems secured a USD 151 million contract to develop phase two of the U.S. Space Force’s Future Operationally Resilient Ground Evolution (FORGE) Command and Control system. This initiative aims to modernize ground infrastructure for missile-warning satellites while supporting the upcoming Next-Generation Overhead Persistent Infrared (Next-Gen OPIR) constellation.

Therefore, these developments showcase broader trends where countries are prioritizing reliable surveillance systems to navigate complex geopolitical landscapes. This increased focus on the development and deployment of advanced satellites is expected to propel market growth during the forecast period.

Escalating Geopolitical Tensions and Cross-Border Conflict to Drive Deployment of Surveillance/Reconnaissance Satellites and Investment in Secure Military Communication Networks

Escalating Geopolitical Tensions and Satellite Surveillance Demand:

Rising geopolitical instability, depicted by conflicts such as the Russia-Ukraine war, territorial disputes in the South China Sea, and heightened Middle Eastern tensions, has underscored the critical role of space-based surveillance. Nations are prioritizing real-time intelligence to monitor adversarial movements, preempt threats, and secure strategic advantages. According to a 2024 report by Euroconsult, global government spending on Earth observation satellites—a core component of military reconnaissance—is projected to surge to USD 25.3 billion annually by 2025, up from USD 18.9 billion in 2023.

This growth is driven by the need for high-resolution imaging, hyperspectral sensors, and AI-driven analytics to process vast data streams. For instance, Ukraine’s use of commercial satellites including Maxar and Capella Space to track Russian troop movements has validated the tactical necessity of persistent surveillance, prompting NATO allies to accelerate sovereign satellite deployments.

Secure Military Communications as a Strategic Imperative:

Modern warfare’s reliance on networked systems necessitates secure, resilient communication channels that are unaffected by jamming and cyberattacks. Traditional ground-based networks are vulnerable, making satellites indispensable. Quantum encryption and Low-Earth Orbit (LEO) constellations are emerging as game-changers, offering latency reductions and enhanced security. For instance, the U.S. Space Force’s Proliferated Warfighter Space Architecture aims to deploy hundreds of LEO satellites by 2025 to ensure redundancy and global coverage.

Increasing Use of AI in Satellite Manufacturing Propels Market Growth

The integration of Artificial Intelligence (AI) has brought about major transformations in the space sector. The newly developed military's reconnaissance satellites use artificial intelligence to analyze and sort captured images. Furthermore, AI-enabled automatic learning systems and intelligent ground stations optimized the control of CubeSats constellations.

Enhanced data processing, laser communication systems, and transmission capacity drive the growth of the market. In November 2019, the U.S. Department of Defense (DoD) signed a contract worth USD 731.8 million with General Dynamics Corporation for the sustainment of the Mobile User Objective System (MUOS), a next-generation military satellite communication system.

MARKET RESTRAINTS

Limited Investments from Emerging Economies Due to High R&D and Launch Costs of Military Satellites Hinder Market Growth

High R&D and Launch Costs Act as Barriers to Entry:

Emerging economies face significant challenges in developing original satellites for military applications capabilities due to the exorbitant costs of R&D, advanced sensor technologies, and satellite launches. In 2024, according to Euroconsult, building a single military-grade satellite with secure communication payloads or high-resolution imaging systems can cost USD 500 million to USD 1 billion, excluding launch expenses, which range from USD 50 million to USD 200 million per mission depending on orbit and vehicle.

Nigeria, Indonesia, and Colombia, allocated approx. USD 4–6 billion annually to total defense budgets in 2024; such investments are prohibitive. Compounding this, emerging markets often lack domestic aerospace ecosystems, forcing reliance on foreign contractors including Arianespace or SpaceX, which prioritize established clients. For instance, in March 2024, Egypt’s delayed NileSat-4 communications satellite, initially slated for 2025, faced indefinite postponement due to budget reallocations toward urgent naval modernization amid Red Sea security threats.

Strict Government Restrictions and Issues Related to Cyber Threats Hamper Market Growth

The space industry is facing numerous restrictions from national as well as government agencies. On an international level, there are five United Nations Treaties on outer space, which are the Rescue Agreement, Outer Space Treaty, Registration Convention, Liability Convention, and Moon Agreement. In addition to that, the activities carried out by non-government organizations require supervision and authorization from the state. Such stringent norms hinder the market growth. Furthermore, issues related to cyber-attacks and spoofing also hamper the growth of the market.

Market Opportunities

High Demand for Cost-Effective Constellation Deployments Due to Small Satellite Miniaturization Drives Growth Opportunities

Miniaturization and Cost Efficiency Revolutionizes Military Satellites:

Advances in Small Satellite (SmallSat) miniaturization, including CubeSats and microsatellites, have drastically reduced development and launch costs, enabling cost-effective deployment of large constellations. Modern SmallSats now integrate advanced capabilities such as Synthetic Aperture Radar (SAR), electro-optical imaging, and encrypted communications at a fraction of traditional satellite costs.

The average cost to build and launch a military SmallSat has fallen to USD 10–50 million, compared to USD 500+ million for legacy systems. This cost reduction has spurred the demand for proliferated constellations, which enhance redundancy, global coverage, and resilience against anti-satellite threats. For instance, the U.S. Space Development Agency’s (SDA) increased Warfighter Space Architecture plans to deploy over 1,000 SmallSats by 2027 to support missile tracking and secure communications. This demonstrates the strategic shift toward scalable and affordable architectures.

Enhanced Resilience and Tactical Advantages:

Constellations of SmallSats offer tactical advantages such as rapid refresh rates, reduced vulnerability to single-point failures, and seamless integration with AI-driven analytics. Unlike monolithic satellites, distributed constellations provide persistent surveillance and real-time data fusion that are critical for modern battlefields. The war in Ukraine highlighted this shift, with SpaceX’s Starlink and ICEYE’s SAR satellites delivering tactical intelligence at unmatched speeds. In 2024, the U.S. Department of Defense allocated USD 2.1 billion to hybrid architectures combining commercial SmallSats such as Planet Labs HawkEye 360 with military-grade systems, accelerating the responsive space paradigm.

Segmentation Analysis

By Orbit Type

Low Earth Orbit (LEO) Segment Dominates Due to Increasing Demand for Real-Time Global Communications Capabilities

Based on orbit type, the market share is split into LEO, MEO, and GEO.

The LEO segment is projected to dominate the market with a share of 83.40% in 2026. Satellites in low earth orbit provide better resolution and detection as well as shorter transmission delays between space and Earth. Furthermore, less power is required to transmit signals to and from LEO compared to higher orbits. Globally, interest in leveraging LEO satellites for secure communications, surveillance, and other defense needs is increasing. For instance, in April 2024, The U.S. Space Force’s Proliferated Warfighter Space Architecture (PWSA) announced that it is deploying hundreds of Low Earth Orbit (LEO) satellites positioned approximately 1,200 miles above Earth to enhance military communication and missile tracking. By 2026, the PWSA aims to achieve global coverage with thousands of satellites for secure and efficient military operations.

The GEO segment is projected to record steady growth during 2025-2032. This growth will be influenced by benefits such as its operation at higher altitudes which covers wide areas on Earth. The recent trend of evolving GEO satellites to address the increase in threats due to modern warfare is expected to stimulate the development of GEO military satellites. For instance, in April 2024, The U.S. Space Force announced the Maneuverable GEO program, which aims to develop geostationary satellites capable of dynamic movement to enhance agility and tactical advantages in military operations.

To know how our report can help streamline your business, Speak to Analyst

By Offering

Satellite Manufacturing Segment Leads Due to High Cost of Spacecraft Components

In terms of offering, the market is segregated into satellite manufacturing, launch services, and operational services.

The communication segment dominated the global market with a market share of 8.51% in 2026.

The satellite manufacturing segment is expected to account for 50.45% of the market share in 2026 and will showcase a similar growth trend during 2025-2032. The growth is attributed to the rising demand for reconnaissance satellites for Intelligence, Surveillance, and Reconnaissance (ISR) missions and the high cost associated with spacecraft components. Governments of various countries are investing heavily in the development of satellites for surveillance, reconnaissance, and other operations, enhancing military capabilities and operational effectiveness. For instance, in February 2025, the U.K. government signed an approximately USD 166.8 million contract with Airbus for the manufacturing and development of the Oberon satellite system with two satellites designed for space-based Intelligence, Surveillance, and Reconnaissance (ISR). Thus, the growing emphasis on the development of versatile, high-performance satellites for military applications is expected to drive the satellite manufacturing segment.

The launch services segment is anticipated to showcase significant growth during the forecast period. The growth is attributed to the increasing satellite launch contracts between military forces and space agencies. Moreover, advancements in launch technologies, such as reusable rockets developed by companies including SpaceX, have significantly reduced the cost and increased the efficiency of satellite launches.

By Type

Small Satellite Segment to Record Highest CAGR Led by Wide Application in Military Communication

By type, the market share is divided into nano-micro, small, medium, and heavy.

The micro satellite segment dominated the global market with a market share of 46.57% in 2026. This is due to the rising demand for small satellites for C4ISR capabilities from defense forces across the globe. Countries are making huge investments in small satellite constellations for secure communication missile tracking missions, and space-based reconnaissance applications. For instance, in December 2024, South Korea announced its plans to launch its third military reconnaissance satellite using a SpaceX rocket as part of its initiative to deploy five spy satellites by 2025 for enhanced surveillance of North Korea. The satellite will feature Synthetic Aperture Radar (SAR) sensors for all-weather monitoring, with small satellites weighing less than 500 kg scheduled for launch between 2026 and 2028.

The nano-micro segment captured the largest market share in 2024. The dominance is due to the highest number of microsatellites launched during 2017-2021. The rising demand for spy satellites from military forces for real-time navigation data drives the segment's growth.

By Application

Communication Segment Holds Leading Position Due to Growing Use in Military Communication

By application, the market is sub-segmented into Intelligence, Surveillance, and Reconnaissance (ISR), communication, and navigation.

The communication segment dominated the global market with a market share of 8.51% in 2026 owing to increasing demand for military communication for enhanced situational awareness and Command, Control, and Communications (C3) capabilities. As global defense spending increases and technological advancements accelerate, nations are prioritizing satellite-based systems for tactical communications, surveillance, and strategic operations to ensure operational superiority and security. For instance, in March 2024, Boeing received a USD 439.6 million contract to build the 12th Wideband Global SATCOM (WGS-12) satellite for the U.S. Space Force, designed to provide secure, high-capacity communications in contested environments using anti-jam technology and Protected Tactical Waveform in the Ka-band.

The navigation segment is estimated to showcase significant growth during the forecast period. Satellite navigation is used to plan and track the movements of convoys as well as search and rescue operations of injured soldiers with less response time. Defense forces use it for aviation, ground, and maritime navigation.

The ISR segment is estimated to register the fastest-growth owing to the increase in demand for satellites for ISR missions such as gathering information on enemy positions, monitoring troop movements, and providing early warnings of potential threats. There is an increasing demand for ISR satellites as nations invest in advanced satellite systems to bolster intelligence, surveillance, and operational capabilities amidst evolving global security challenges. For instance, in 2024, the U.K. successfully launched its first military satellite, Tyche, to enhance its Intelligence, Surveillance, and Reconnaissance (ISR) capabilities.

By Satellite Component

Payload Segment Held Highest Shares in Market Due to Rising Demand for Earth Observation Imagery Payloads

By satellite component, the market is classified into structures, payload, electric power system, instrument control unit, propulsion system, thermal control subsystem, communication system, and others.

Among these, the payload segment held the highest share in 2024. The segment’s leading position in the market can be attributed to growing demand for LEO-based satellite and earth observation imagery payloads. Key players in the market are focusing on the development of advanced payload systems to enhance satellite communication capabilities and increase the military satellite market share. For instance, in 2023, Boeing unveiled its Protected Wideband Satellite (PWS) design featuring the Protected Tactical SATCOM Prototype (PTS-P) payload, integrated into the U.S. Space Force's Wideband Global SATCOM (WGS)-11 satellite. The PTS-P payload incorporates advanced anti-jam technologies such as jammer geolocation, adaptive nulling, and frequency hopping to ensure secure communications for warfighters in disputed environments.

Propulsion systems are anticipated to show remarkable growth during 2025-2032. Growing demand for medium and heavy satellites for military missions drives the growth of the segment.

MILITARY SATELLITE REGIONAL OUTLOOK

The market is divided into North America, Asia Pacific, Europe, and the rest of the world.

North America

North America Military Satellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global military satellite market in 2024 with an annual valuation of USD 6.55 billion. Increasing defense spending and technological advancements, with significant investments in space-based capabilities to enhance military operations supports the region’s growth. For instance, The U.S. Space Force allocated funding USD 28.7 billion under the Continuing Resolution (CR) passed by Congress for modernization and resilience in satellite systems. Moreover, the Pentagon authorized USD 30 million to fund Resilient GPS satellites, supplementing existing constellations with smaller, cost-effective satellites. The U.S. market is projected to reach USD 7.41 billion by 2026. In 2025, North America represented USD 7.01 billion, accounting for 38.00% of the worldwide market, and is projected to grow to USD 7.51 billion in 2026.

Europe

Europe is expected to record notable growth during the projected period. There are rising defense modernization initiatives and geopolitical tensions, which are driving demand for secure communication and surveillance systems. For instance, in 2022, Poland signed a contract worth USD 612 million with Airbus for observation satellites and France's BRO nanosatellite program, which plans to deploy 20-25 satellites by 2025 to enhance maritime tracking and security. In addition, there is an increasing investment in space infrastructure and the need for autonomous launch capabilities to support defense operations, which pushes the growth of the market. Moreover, ESA is strengthening its support for the next generation of commercial-led European launch services through its Boost program, extending contracts with four companies to advance the deployment of their launch capabilities. Thus, advancement in launch systems is expected to increase satellite deployments, which propels the growth of the region in the market. The UK market is projected to reach USD 0.71 billion by 2026, while the Germany market is projected to reach USD 0.62 billion by 2026. The Europe market generated USD 6.16 billion in 2025, representing 33.40% of the global market landscape, and is expected to reach USD 6.69 billion in 2026.

Asia Pacific

Asia Pacific will showcase significant growth due to growing expenditure on the space sector from the governments of India, China, and Japan. In August 2021, China launched the TJS 7 satellite in geostationary orbit. It will be mainly used to carry out communication technology test missions. Furthermore, in January 2019, India launched Microsat-R, a satellite on board its Polar rocket PSLV C44. Thus, an increasing number of military communication satellite launches from Asian countries drive the regional market expansion. The region's growing need for satellite communications for military application, Earth observation, and reconnaissance fuels market growth. This includes deploying satellites for strategic communications and surveillance. For instance, in 2025, China deployed an experimental satellite in Geostationary Orbit (GEO) to practice space-based jamming, as reported by the People's Liberation Army. This development indicates China's efforts to enhance its space-based electronic warfare capabilities, particularly targeting communications satellites. The Japan market is projected to reach USD 0.44 billion by 2026, the China market is projected to reach USD 3.48 billion by 2026, and the India market is projected to reach USD 0.65 billion by 2026. Asia Pacific contributed 25.10% to the global market in 2025, with a valuation of USD 4.63 billion, and is projected to reach USD 5.01 billion in 2026.

The Japan market is projected to reach USD 0.44 billion by 2026, the China market is projected to reach USD 3.48 billion by 2026, and the India market is projected to reach USD 0.65 billion by 2026.

Rest of the World

Meanwhile, the rest of the world is anticipated to grow at a steady CAGR in the forthcoming years. The growth in this region is led by the increasing spending on the space sector in Middle Eastern countries. In July 2020, Israel launched its Ofek 16 reconnaissance satellite to provide intelligence capabilities and technological superiority to the country. Countries in the Middle East region are focusing on the development of satellites for commercial and civil purposes. For instance, in 2025, The UAE's Sirb satellite constellation, led by an Emirati consortium, aims to launch three Synthetic Aperture Radar (SAR) satellites into LEO by late 2026 or early 2027. Rising regional tensions, the need for enhanced surveillance and defense capabilities, and the established commercial satellite industry in the region drive investment in LEO satellites for real-time ISR. Moreover, countries in the region, such as Brazil are investing in satellite manufacturing significantly. For instance, the development of the SGDC-1 satellite supports secure military communications. This fosters local expertise and infrastructure development for satellite production for the military sector in the region. Moreover, partnerships with international aerospace firms enhance local satellite manufacturing capabilities, enabling the Middle East to meet military demands efficiently. Rest of the World contributed approximately USD 0.65 billion to the global market in 2025, accounting for 3.50% share, and is expected to reach USD 0.69 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Major OEMs Emphasize New Product Launches, Contracts, and Agreements with Space Agencies to Increase Market Share

The military satellite market is highly competitive, driven by a rise in global defense budgets, technological advancements, and the increasing importance of space-based capabilities in the military sector. Some of the top players in the industry are Boeing (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman (U.S.), and Airbus (Netherlands). Moreover, leading companies maintain their dominance through innovation in secure communication systems, advanced imaging capabilities, and resilient satellite architectures. In addition, market players are focusing on the advancement in satellite technologies and the integration of artificial intelligence to strengthen their presence in the market.

List of Key Military Satellite Companies Profiled

- Airbus (Netherlands)

- BAE Systems (U.K.)

- Boeing (U.S.)

- IAI (Israel)

- ISRO (India)

- L3 Harris Technologies, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- ST Engineering (Singapore)

- Thales Group (France)

- Viasat, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In April 2025, Millennium Space Systems, a Boeing subsidiary, is doubling its satellite manufacturing capacity to meet a growing backlog of defense contracts, aiming to increase production from 1-2 satellites monthly to 6-12. The expansion was driven by military programs, including a USD 414 million contract for missile-tracking satellites and a multi-billion dollar order from the U.S. Space Force.

- In March 2025, Lockheed Martin is set to launch its self-funded LM 400 technology demonstration satellite aboard Firefly Aerospace's Alpha rocket to validate new technologies for various missions, enhancing capabilities for military, commercial, and civil applications. The LM 400 is particularly suited for military use in remote sensing communications.

- In February 2025, Airbus secured the U.K. Ministry of Defence's Oberon contract to design and construct two Synthetic Aperture Radar (SAR) satellites, enhancing day-and-night, all-weather Intelligence, Surveillance, and Reconnaissance (ISR) capabilities. These ultra-high resolution SAR satellites will strengthen operational capabilities for the UK MOD and allied defense forces.

- In December 2024, Lockheed Martin’s newest technology demonstration called the Tactical Satellite (TacSat), was completed and is ready for launch in 2025 aboard a Firefly Aerospace Alpha rocket. TacSat is an intelligence, surveillance, and reconnaissance spacecraft with a mission to prove specialized sensing and communications capabilities in orbit.

- In May 2024, Airbus Defence and Space delivered the first Sentinel-5 instrument for the European Space Agency (ESA) that will be integrated into MetOp Second Generation Satellite A. The UVNS (Ultraviolet Visible Near-infrared Short-wave infrared Spectrometer) instrument will contribute to the improved monitoring of air quality, changes in the ozone layer, and emissions from wildfires.

REPORT COVERAGE

The military satellite market research report provides a detailed analysis and focuses on key aspects such as top space companies, types, satellite component, and leading applications. The report provides a detailed analysis of the sector and focuses on important aspects such as key players, orbit type, offering, type, application, and component depending on various regions. Moreover, the report includes development trends, competitive landscape analysis, investment plans, business strategy, growth opportunities, and the status of regional development. In addition to the factors mentioned above, the market report encompasses several direct and indirect factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.82% from 2026-2034 |

|

Segmentation

|

By Orbit Type

|

|

By Offering

|

|

|

By Type

|

|

|

By Application

|

|

|

By Satellite Component

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 18.44 billion in 2025 and is projected to reach USD 33.73 billion by 2034.

The market is projected to grow at a CAGR of 6.82% during the forecast period (2026-2034).

The nano-micro segment is expected to be the leading segment by type in this market during the forecast period.

Boeing is the leading player in the global market.

North America held the highest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us