Military Batteries Market Size, Share & Industry Analysis, By Type (Rechargeable & Non-Rechargeable), By Composition (Lithium Based (Lithium-Ion Polymer, Lithium-Iron Phosphate (LFP), Lithium Thionyl Chloride (Li-SOCl2) Batteries, Lithium Manganese Dioxide (LiMnO2) Batteries, and Others), Nickel Based (Nickel Cadmium (NiCd), & Others), By Platform (Ground, Airborne, & Marine), By Energy Density (Less than 150 Wh/kg, 150 to 250 Wh/kg, and More than 250 Wh/kg), By Voltage (Less than 6V, 6 to 24V, and More than 24V), By Application, By Point of Sale, and Regional Forecast, 2026-2034

Military Batteries Market Overview

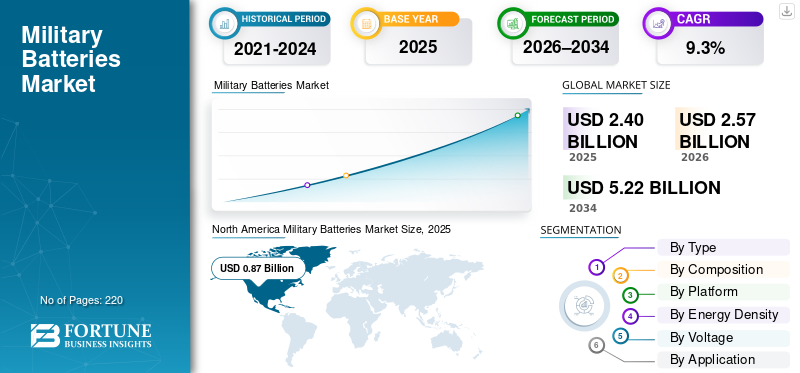

The global military batteries market size was valued at USD 2.40 billion in 2025. The market is projected to grow from USD 2.57 billion in 2026 to USD 5.22 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period. North America dominated the military batteries market with a market share of 36.25% in 2025.

The global military batteries market is expected to grow significantly due to rising global defense budgets, the proliferation of unmanned systems such as UAVs and UGVs, and growing demand for reliable and high performance batteries in electric and hybrid military vehicles. Military batteries using advanced lithium-ion and emerging solid-state technologies for high energy density, lightweight design, and extreme environmental resilience, are essential for powering propulsion systems, communication systems, electro-optics, and mission-critical electronics. Moreover, the push for enhanced energy efficiency in electronic warfare systems and sustainable power solutions during geopolitical tension across the globe is accelerating the market expansion.

- For instance, in September 2025, Ultralife Corporation secured a USD 5.2 million contract from the U.S. Defense Logistics Agency for BA-5390 lithium manganese dioxide military batteries, with deliveries primarily scheduled for 2026 to support mission-critical DoD applications.

Key players such as Ultralife Corporation, EaglePicher Technologies, Bren-Tronics, Saft, and EnerSys, are focusing on innovations such as solid-state batteries for superior safety and density, modular high-capacity lithium ion batteries, and AI-optimized energy management systems for various types of platforms.

Download Free sample to learn more about this report.

MILITARY BATTERIES MARKET TRENDS

Shift Toward Solid-State Battery and AI-enhanced Battery Management Systems (BMS) is a Prominent Trend Observed in Market

The shift toward solid-state and AI-integrated military battery systems is gaining traction in defense applications, driven by demands for higher energy density, enhanced safety, and extended endurance in unmanned systems and electrified platforms. These batteries use solid electrolytes instead of liquid ones along with AI-driven management systems for real-time health monitoring, predictive maintenance, and adaptive power distribution. Such evolution boosts performance against thermal extremes and mechanical stresses while minimizing risks such as thermal runaway in combat scenarios.

- For instance, in February 2025, The U.S. Army Combat Capabilities Development Command (DEVCOM) collaborated with SandboxAQ to deploy AI-driven Large Quantitative Models (LQMs), achieving faster predictions for lithium-ion battery shelf life, performance, and maintenance needs across vehicles, drones, and wearables.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Defense Budget and Investment in Materials is Expected to Drive Market Growth

A primary driver for the military batteries industry is the global surge in defense budgets and accelerated investment in battery material for military operations.

- For instance, according to the Stockholm International Peace Research Institute (SIPRI), global military expenditure hit USD 2.44 trillion in 2024, up 6.8% from 2023. Moreover, the Department of Defense granted Nano One Materials Corp. USD 12.9 million under the Defense Production Act to ramp up production of Lithium Iron Phosphate (LFP) cathode materials at facilities in Candiac, Québec, and Burnaby, British Columbia. This initiative strengthens North American battery supply chains for safer and cost-effective batteries.

Such defense spending and investment propels demand for high-density military batteries featuring lithium-ion advancements, solid-state designs, and ruggedized packs for extreme environments. As militaries electrify fleets, and deploy extended-endurance UAVs and UGVs, there's escalating need for lightweight, high-capacity batteries to ensure operational endurance, rapid recharging, and reliable performance.

MARKET RESTRAINTS

High Development Costs and Stringent Military Standards to Limit Market Expansion

A primary restraint for the market is the elevated research, development, and certification expenses tied to meeting rigorous military specifications for reliability, safety, and performance under extreme conditions. For instance, advanced lithium-ion and solid-state batteries demand extensive testing for thermal runaway prevention, shock/vibration resistance, and lifecycle endurance which delays procurement and strains defense budgets. These barriers limit rapid adoption by smaller militaries or new entrants and hamper the military batteries market growth during the forecast period.

MARKET OPPORTUNITIES

Growing Integration of Batteries into Electrified Military Platforms Presents Growth Opportunities for Market Growth

The growing integration of advanced batteries into electrified military platforms reflects a shift toward hybrid and all-electric propulsion systems that enhance endurance, stealth, and logistics efficiency for next-generation vehicles and unmanned systems.

- For instance, in June 2024, GM Defense partnered with the University of Texas at Arlington, Pulsed Power and Energy Laboratory, and Naval Surface Warfare Center, is evaluating commercial EV batteries such as GM's Ultium platform for military use under the DoD-funded EEVBEDE project.

Electrified platforms feature modular battery architectures with fast-charging capabilities, high energy density, and ruggedized designs compatible with sensor suites and AI energy management. Such factors accelerate innovation and deployment of next-gen batteries, presenting lucrative opportunities for market growth.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Critical Minerals Acts a Challenge for Market

A primary challenge for the military batteries market is the heavy reliance on scarce critical minerals like lithium, cobalt, and nickel, which face supply chain disruptions from geopolitical tensions, mining bottlenecks, and export restrictions by dominant producers. These vulnerabilities compel stockpiling, alternative sourcing like sodium-ion R&D, and domestic processing investments, but hinder scalability for high-volume programs in UAVs, vehicles, and wearables. Such factors present challenges for the growth of the market during the forecast period.

Segmentation Analysis

By Type

Rising UAV/UGV Adoption and Lithium-Ion Advancements to Propel Rechargeable Segmental Growth

Based on type, the market is divided into rechargeable and non-rechargeable.

The rechargeable segment is anticipated to account for the largest military batteries market share. Rising adoption of UAVs, UGVs, and UUVs demands high-capacity rechargeable batteries for extended reconnaissance and combat missions. Advancements in lithium-ion battery technology deliver higher energy density and lighter weight. Thus, increasing demand for rechargeable batteries for portable devices such as radios, night vision goggles, and wearables to operate longer in harsh environments drives segment growth.

The non-rechargeable segment is anticipated to rise with a steady growth rate with a CAGR of 8.5% over the forecast period.

By Composition

High Energy Density and Development of Batteries for Modern Vehicles to Propel Lithium Based Segmental Growth

By composition, the market is segmented into lithium based, nickel based, and others. Lithium based include lithium-ion polymer, lithium-iron phosphate (LFP), lithium thionyl chloride (Li-SOCl2) batteries, lithium manganese dioxide (LiMnO2) batteries, and others. Nickel based batteries comprises nickel cadmium (NiCd), and nickel metal hydride (NiMH). Others include lead acid batteries, silver-zinc batteries, and others.

The lithium based segment is anticipated to account for the largest market share, driven by the high energy density, and lightweight design of lithium batteries. There is a rise in demand for batteries with high energy density for longer mission durations. Moreover, key market players are focused on launching battery modules modern military vehicles, including armored tanks, personnel carriers, and hybrid/electric platforms.

- For instance, in September 2025, Epsilor Electric Fuel Ltd. launched the ELI-52526-GM, a lithium-ion battery of 4,400Wh capacity in a compact NATO 6T form factor, the highest energy density for military vehicles.

The nickel based segment is projected to grow at a steady CAGR of 7.7% over the forecast period.

By Platform

Demand for High Power for Tanks and Tactical Trunks Push Ground Segment Growth

Based on platform, the market is segmented into ground, airborne, and marine.

Ground segment account for the largest market share of the industry as tanks, infantry fighting vehicles, artillery, and tactical trucks form the largest portion of active defense inventories globally. These assets demand constant, rugged power for engine starts, weapon systems, communications, and sensors during prolonged ground maneuvers in diverse terrains. Defense forces of various countries are investing in different projects for the development of energy solutions for ground vehicles in critical military.

- For instance, in December 2023, The U.S. Department of Defense partnered with DIU on the FAStBat project to prototype domestic lithium batteries for soldier power, aviation like the AH-1Z Viper, and ground vehicles, tackling supply chain vulnerabilities and high costs.

The airborne segment is expected to grow with a fastest CAGR of 10.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Energy Density

Optimal Balance for Portable Systems and Tactical Vehicles Supported 150 to 250 Wh/kg Segment Dominance

Based on energy density, the market is segmented into less than 150 Wh/kg, 150 to 250 Wh/kg, and more than 250 Wh/kg.

The 150 to 250 Wh/kg segment held the largest share in market in 2025. The 150 to 250 Wh/kg battery dominates in military applications as it strikes the optimal balance for portable soldier systems, powering radios, night vision, and GPS units over multi-day missions without excessive bulk. Ground platforms are increasingly using this range of batteries for tactical vehicles and UGVs for reliable, high power and sustained electronics which is expected to propel the segment growth.

The more than 250 Wh/kg segment is projected to emerge as the fastest-growing at a CAGR of 10.6% over the forecast period.

By Voltage

Standardized Tactical Equipment Compatibility Fuelled 6 to 24V Segment Growth

Based on voltage, the market is segmented into less than 6V, 6 to 24V, and more than 24V.

The 6 to 24V segment held the highest market share in 2025. The factor attributing to segment growth is the increase in use of batteries with 6 to 24V for widespread tactical equipment, from ground vehicle starter motors in tanks and HMMWVs to soldier-carried radios and weapon sights during frontline engagements. These voltages match standardized MIL-STD interfaces across NATO forces, ensuring seamless interchangeability for infantry squads and mechanized units operating in mud, sand, or extreme cold.

The more than 24V segment is projected to grow with a steady growth rate at a CAGR of 10.9% over the forecast period.

By Application

Surge in Demand for Batteries for Radios, Tactical Data Links, and AI-Enabled Sensors Fuelled Electronics and Communications Equipment Segment Growth

Based on application, the market is segmented into electronics and communications equipment, Unmanned Aerial Vehicles (UAVs) and drones, ground vehicles, remote sensors and monitoring equipment, and others.

The electronics and communications equipment segment held the highest market share in 2025. The factor attributing to segment growth are surge in need for uninterrupted power for software-defined radios, tactical data links, AI-enabled sensors and other critical military equipment that fuse real-time intel across distributed forces. Moreover the devices such as multi-band SATCOM terminals and drone controllers requires battery needs during extended patrols drive the segment growth.

The Unmanned Aerial Vehicles (UAVs) and drones segment is projected to grow with a steady CAGR of 10.9% over the forecast period.

By Point of Sale

Next-Gen Platform Electrification Mandates Boosted OEM Segment Growth

Based on point of sale, the market is segmented into OEM and aftermarket.

The OEM segment held the highest market share in 2025. Defense procurement of next-generation platforms embedding advanced power systems drive the demand for OEM segment. Moreover, the electrification mandates in new UAVs, hybrid armored vehicles, and autonomous ground units demand integrated high-density lithium packs certified for mission-critical reliability during initial deployment, which propels the segment growth.

The aftermarket segment is projected to grow with a steady CAGR of 10.0% over the forecast period.

Military Batteries Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Military Batteries Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the military batteries market in 2025 with a valuation of USD 0.87 billion, growing to USD 0.93 billion in 2026, driven by surging defense spending on electrified platforms amid rising demands for unmanned systems and hybrid propulsion. The U.S. leads due to robust military budgets and integration of advanced batteries into next-generation UAVs, vehicles, and soldier power systems for extended missions.

U.S. Military Batteries Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 0.84 billion in 2025. High defense allocations support battery upgrades in modular architectures for UGVs, exoskeletons, and directed-energy weapons, enhancing endurance in austere environments. The U.S. military advances power capabilities by adopting ruggedized packs to counter logistics constraints and power-intensive sensors. In addition, the defense sector in the U.S. constantly invests heavily in research and development of batteries made from advanced materials which drives market growth in the country.

- For instance, in December 2025, U.S. Department of Defense provided USD 1.65 million grant to NanoGraf for development of graphene-wrapped silicon anode lithium-ion batteries, aiming for 50-100% longer runtime in portable military gear.

Europe

Europe is projected to record a growth rate of 9.5% during 2026 to 2034, which is the second highest among all region. The market in the region grows due to security demands from counter-terrorism, military modernization, and NATO operations. The market expands due to investments in high-endurance batteries for portable soldier systems, hybrid vehicles, and unmanned platforms. The U.K., France, and Germany invest heavily in rugged lithium-ion and emerging solid-state batteries for urban operations, extended UAV missions, and armored electrification. Numerous regional players develop advanced power solutions to counter threats like drone swarms and energy-intensive sensors observed in global conflicts.

- For instance, in October 2025, Solus Power secured a UK MOD contract to develop next-generation portable battery systems optimized for soldier-worn gear and extreme environments.

U.K. Military Batteries Market

The U.K. market in 2025 was valued at around USD 0.10 billion, representing roughly 9.4% of global revenues.

France Military Batteries Market

France reached approximately USD 0.06 billion in 2025, equivalent to around 7.3% of global sales.

Asia Pacific

Asia Pacific market reached a valuation of USD 0.58 billion in 2025 and secured the position of the third-largest region in the market. The market grows rapidly due to heavy investments in high-capacity batteries for UAV swarms, naval electrification, and soldier-portable power during regional geopolitical challenges. India, China, and South Korea prioritize lithium-ion advancements and solid-state prototypes for extended-range drones, hybrid armored vehicles, and energy-intensive radars.

Japan Military Batteries Market

The Japan market in 2025 was valued around USD 0.06 billion, accounting for roughly 2.3% of global revenues.

China Military Batteries Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 0.35 billion, representing roughly 14.7% of global sales.

India Military Batteries Market

The India market in 2025 was valued at around USD 0.02 billion, accounting for roughly 1.0% of global revenues.

Latin America and the Middle East & Africa

Latin America exhibits steady market growth during 2026-2034, supported by defense modernization efforts and peacekeeping operations across Brazil, Colombia, and Chile. The Latin America market reached a valuation of USD 0.19 billion in 2025, driven by rising demand for durable batteries in jungle patrol vehicles, UAV border surveillance, and portable soldier systems. Middle East & Africa records robust expansion during 2026-2034, propelled by Gulf state defense procurements, counter-terrorism campaigns, and African Union missions. The market benefits from demand for heat-resistant batteries in desert UAVs, armored convoys, and mobile command posts.

Saudi Arabia Military Batteries Market

The Saudi Arabia market reached around USD 0.03 billion in 2025, representing roughly 1.15% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on High-Density Solid-State and Lithium-Ion Batteries by Key Players to Propel Market Progress

The global market remains consolidated, led by major players such as Ultralife Corporation, EaglePicher Technologies, Saft, Bren-Tronics, EnerSys, and BAE Systems, which command significant shares through innovations in high-energy density cells and thermal-resilient systems. These firms advance market growth with strategic contracts from defense agencies and OEM partnerships, emphasizing development of modular lithium-ion and solid-state batteries for UAV propulsion, soldier power, and hybrid vehicles across various platforms. Moreover, players prioritize advanced packs with extended cycle life to meet demands for prolonged unmanned missions and electrified combat systems.

- For instance, in May 2025, Ultralife Corporation secured a USD 5.2 million U.S. Defense Logistics Agency contract for BA-5390 lithium manganese dioxide batteries tailored for mission-critical DoD applications.

Other prominent players such as L3Harris Technologies, Northrop Grumman, and Raytheon focus on scalable production of fast-charging modules, AI-enhanced management systems, and extreme-environment solutions.

LIST OF KEY MILITARY BATTERIES COMPANIES PROFILED IN REPORT

- Ultralife Corporation (U.S.)

- EaglePicher Technologies (U.S.)

- Saft (France)

- KULR Technology Group, Inc. (U.S.)

- EnerSys (U.S.)

- Epsilor (Israel)

- GS Yuasa Corporation (Japan)

- Arotech Corporation (U.S.)

- Tadiran Batteries (Israel)

- Concorde (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Ultralife Corporation announced a USD 5.2 million award from the U.S. Defense Logistics Agency for lithium manganese dioxide BA-5390 military batteries, with shipments primarily slated for 2026 to support critical DoD missions.

- September 2025: EnerSys introduced Hawker ARMASAFE iON-X 24-volt rechargeable lithium-ion batteries (105 Ah and 162 Ah models) for tactical vehicles, robotics, and silent watch operations, meeting MIL-PRF-32565C standards with high energy density and long cycle life.

- May 2025: DEVCOM C5ISR Center researchers unveiled advanced rechargeable lithium-ion batteries for soldier-worn electronics, offering superior capacity and performance in extreme hot/cold environments to enable prolonged missions.

- April 2025: Saft America Inc. secured a USD 7.5 million indefinite-quantity contract from the U.S. Defense Logistics Agency for storage batteries supporting H1, Seahawk, and CH-53 helicopters across all military branches.

- March 2025: EaglePicher Technologies secured a nearly USD 20 million U.S. Air Force contract to produce specialized silver-zinc batteries for Minuteman-3 ICBM guidance systems, with exclusive manufacturing in Joplin over the next five years.

- January 2025: Æsir Technologies Inc. secured a USD 15.8 million U.S. Navy contract via BlueForge Alliance to build and equip a 17,000 sq ft plant expansion, boosting production capacity for critical submarine battery packs and potential job growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and By Region |

|

By Type |

· Rechargeable · Non-Rechargeable |

|

By Composition |

· Lithium Based · Nickel Based · Others |

|

By Platform |

· Ground · Airborne · Marine |

|

By Energy Density |

· Less than 150 Wh/kg · 150 to 250 Wh/kg · More than 250 Wh/kg |

|

By Voltage |

· Less than 6V · 6 to 24V · More than 24V |

|

By Application |

· Electronics and Communications Equipment · Unmanned Aerial Vehicles (UAVs) and Drones · Ground Vehicles · Remote Sensors and Monitoring Equipment · Others |

|

By Point of Sale |

· OEM · Aftermarket |

|

By Region |

· North America (By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and Country) o U.S. (By Platform) o Canada (By Platform) · Europe (By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and Country) o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific (By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and Country) o China (By Platform) o Japan (By Platform) o India (By Platform) o South Korea (By Platform) o Rest of Asia Pacific (By Platform) · Latin America (By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and Country) o Brazil (By Platform) o Mexico (By Platform) o Rest of Latin America ( By Platform) · Middle East & Africa (By Type, By Composition, By Platform, By Energy Density, By Voltage, By Application, By Point of Sale, and Country) o UAE (By Platform) o Saudi Arabia (By Platform) o Rest of the Middle East & Africa (By Platform) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.40 billion in 2025 and is projected to reach USD 5.22 billion by 2034.

In 2025, North Americas market value stood at USD 0.87 billion.

The market is expected to exhibit a CAGR of 9.3% during the forecast period of 2026-2034.

By platform, the ground segment is expected to lead the market.

The rise in defense budget and investment in battery materials are driving market expansion.

Ultralife Corporation (U.S.), EaglePicher Technologies (U.S.), and Saft (France) and among others are some of the major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us