Military Edge Computing Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Deployment (On-premises and Cloud), By Application (Cybersecurity, Intelligence, Surveillance, and Reconnaissance (ISR), Command and Control (C2), and Others), By End-user (Land, Airborne, and Naval), and Regional Forecast, 2026-2034

MILITARY EDGE COMPUTING MARKET SIZE AND FUTURE OUTLOOK

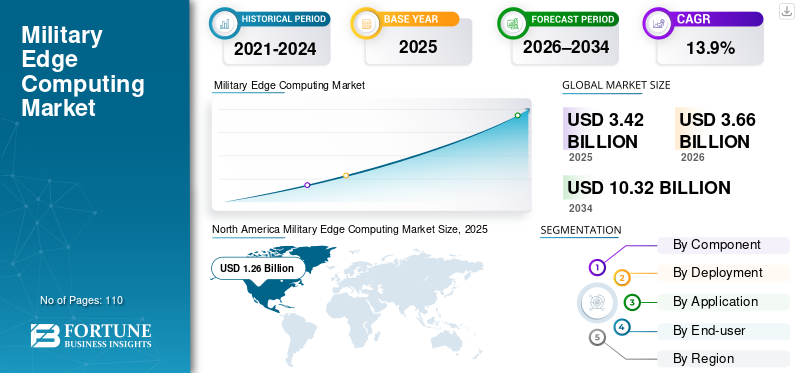

The global military edge computing market size was valued at USD 3.42 billion in 2025. The market is projected to grow from USD 3.66 billion in 2026 to USD 10.32 billion by 2034, exhibiting a CAGR of 13.9% during the forecast period. North America dominated the military edge computing market with a market share of 36.84% in 2025.

Military edge computing platforms are advanced systems designed to process and analyze battlefield data locally, enabling real-time decision-making, autonomous operations, and situational awareness in contested and communications-constrained environments. These platforms are critical for integrating sensor data from unmanned systems, ISR assets, radar, and electronic warfare equipment, where low-latency processing and resilience are essential. The growing adoption of multi-domain operations, autonomous platforms, and AI-driven analytics is driving demand for ruggedized, secure, and scalable edge computing solutions that can operate in austere environments while supporting both human operators and autonomous systems.

Key players such as Lockheed Martin, General Dynamics, Microsoft, and Raytheon Technologies are strengthening their positions through technological innovation, strategic partnerships, and targeted investments in AI-enabled edge solutions. For instance,

- In December 2025, Raytheon (RTX) partnered with Amazon Web Services (AWS) to enhance satellite data processing and mission control operations. This collaboration leverages cloud-based AI/ML services and AWS Outposts to deliver edge computing capabilities for defense applications, enabling faster, more secure, and more scalable processing of mission-critical data.

These companies are focusing on enhancing processing power, cyber-resilience, platform interoperability, and the integration of AI and machine learning at the edge to improve operational efficiency and battlefield effectiveness.

Download Free sample to learn more about this report.

Military Edge Computing Market Key Takeaways

- 2025 Market Size: USD 3.42 billion

- 2026 Market Size: USD 3.66 billion

- 2034 Forecast Market Size: USD 10.32 billion

- CAGR: 13.9% from 2026-2034

- North America dominated the military edge computing market with a 36.84% share in 2025.

- The land segment held the largest market share of 50.6% in 2025.

- The hardware segment accounted for a 53.7% market share in 2025.

North America

North America was valued at USD 1.26 billion in 2025, supported by strong defense modernization and edge AI adoption.

Europe

Europe was valued at USD 0.94 billion in 2025 and is projected to grow at a CAGR of 14.0% during the forecast period.

Asia Pacific

Asia Pacific was valued at USD 0.78 billion in 2025 and is expected to register the highest CAGR over the forecast period.

U.S.

The market was valued at USD 1.11 billion in 2025, accounting for approximately 32.5% of global military edge computing revenues.

Japan

The market was valued at USD 0.08 billion in 2025, representing around 2.3% of global military edge computing revenues.

Read More

IMPACT OF GENERATIVE AI

Real-Time Decision Support and Autonomous Operations Driving Adoption of Generative AI in Military Edge Computing

Generative AI is enhancing the growth of military edge computing by enabling real-time analysis and predictive insights directly at the tactical edge. It allows autonomous systems and commanders to simulate scenarios, anticipate threats, and optimize mission planning without relying on central servers. By generating actionable intelligence locally, even in contested or communications-denied environments, generative AI significantly improves situational awareness, operational responsiveness, and the effectiveness of edge-enabled platforms.

MILITARY EDGE COMPUTING MARKET TRENDS

Embedded AI in Autonomous and Semi-Autonomous Platforms Driving Edge Computing Adoption

A significant trend in the market is the growing integration of embedded artificial intelligence within autonomous and semi-autonomous platforms. Unmanned aerial vehicles, ground robots, maritime drones, and other robotic systems are increasingly equipped with edge computing capabilities that enable local, real-time processing of critical data. These platforms perform AI inference on board, analyzing sensor feeds, navigation information, threat-detection signals, and environmental inputs without relying on centralized servers or continuous communication links. For instance,

- In January 2026, Lantronix launched a Drone Reference Platform that leverages edge computing to enable real-time AI processing directly on drones. The platform supports onboard perception, autonomy, and in-flight decision-making, reducing latency and reliance on external networks.

By processing data locally, these systems can operate effectively in communications-denied or degraded environments, ensuring mission continuity and reducing the dependence on operator intervention. Embedded AI enhances situational awareness, facilitates rapid target recognition, supports adaptive route planning, and enables coordinated behavior among multiple autonomous units.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Budget Increases and Technological Modernization Programs Drive Market Growth

A rise in defense budgets and strategic modernization programs globally is a key driver of the military edge computing market growth. In the U.S., initiatives such as Joint All-Domain Command and Control and the Next Generation Combat Vehicle program are explicitly focused on implementing distributed computing architectures and edge-enabled artificial intelligence to reduce sensor-to-shooter timelines and improve battlefield responsiveness.

European modernization efforts are emphasizing multi-domain interoperability, real-time sensor fusion, and resilient communications, all of which require robust edge computing infrastructure. In the Asia Pacific region, rising geopolitical tensions are fueling investments in autonomous platforms, high-speed data networks, and intelligence, surveillance, and reconnaissance systems that require local processing and edge AI inference.

Unlike generic technology upgrades, these programs are designed to enhance operational effectiveness by enabling autonomous systems to function in communications-denied environments, supporting high-tempo distributed operations, and improving rapid decision-making across air, land, and maritime domains. As a result, increased funding combined with targeted modernization strategies is creating a strong and sustained demand for edge computing solutions purpose-built for military applications.

MARKET RESTRAINTS

Technical Challenges with Connectivity & Bandwidth Restraint Market Growth

Connectivity and bandwidth limitations pose a critical technical challenge for military edge computing, directly affecting operational effectiveness. Although edge nodes are designed to process data locally, many applications, such as real-time targeting, autonomous vehicle coordination, and distributed sensor fusion, still rely on intermittent data exchange with other nodes or command networks.

In operational theaters, communications are often severely constrained by hostile conditions, including deliberate jamming, limited spectrum availability, and contested electromagnetic environments, which degrade or block data transmission.

Additionally, units operating in remote or forward-deployed locations frequently experience network delays or disruptions, making it difficult to synchronize computations, share intelligence, or update software across edge nodes.

MARKET OPPORTUNITIES

Demand for Real-Time Battlefield Decision Support to Boost Market Growth

The growing demand for real-time battlefield decision support is one of the most significant drivers of the market. Modern military operations are increasingly data-intensive and time-sensitive, relying on the rapid collection, analysis, and dissemination of information from a variety of sensors, including intelligence, surveillance, and reconnaissance systems, electronic warfare platforms, radar arrays, and electro-optical/infrared devices.

- In October 2025, Leonardo DRS launched SAGEcore, a rugged AI software platform designed for edge computing on tactical platforms. It processes complex sensor data on-site, enabling real-time threat detection and faster, low-latency decision-making.

Edge computing enables this data to be processed locally, at or near the point of collection, rather than relying solely on centralized servers or distant command centers.

This local processing dramatically reduces latency, allowing commanders and autonomous systems to make critical decisions more quickly and accurately. In high-tempo, contested, and geographically distributed operations, the ability to shorten the sensor-to-shooter timeline can be decisive, directly affecting mission success, force protection, and operational efficiency.

Segmentation Analysis

By End-user

Land Segment Led Market Due to High Data Volume and Tactical Complexity

Based on the end-user, the market is classified into land, airborne, and naval.

The land segment dominated the market in 2025 with a 50.6% share, as ground operations involve the largest and most diverse deployment of vehicles, mobile command units, and sensor networks that generate vast amounts of data requiring immediate processing. Edge computing enables real-time analysis of battlefield intelligence, targeting information, and autonomous ground systems, even in rugged, communications-limited environments.

The airborne segment is expected to witness the highest CAGR of 16.5% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Hardware Dominated Market as Ruggedized Processing Units and AI Accelerators Handle Real-Time Battlefield Data

Based on the component, the market is divided into hardware, software, and services.

The hardware segment held 53.7% market share as military edge computing relies on ruggedized, high-performance processors, AI accelerators, and storage systems that can operate in extreme battlefield conditions. Unlike software, which can be updated or scaled flexibly, these hardware components are critical for handling real-time data from sensors, autonomous platforms, and ISR systems, ensuring low-latency processing and operational reliability in environments with limited connectivity and high electromagnetic interference.

The software segment is expected to witness the highest CAGR of 16.7% during the forecast period.

By Deployment

On-Premises Led Due to Security, Low Latency, and Communications-Denied Environments

Based on deployment, the market is categorized into on-premises and cloud.

The on-premises segment dominated with 63.5%, as military operations require full control over sensitive data and mission-critical workloads that cannot rely on public or cloud networks due to security, latency, and connectivity constraints. Tactical environments often operate in contested or communications-denied areas, making local processing essential for real-time decision-making, autonomous systems, and sensor fusion. The need for secure, resilient, and low-latency operations makes on-premises edge infrastructure the preferred choice for defense organizations.

The cloud segment is expected to witness the highest CAGR of 18.1% during the forecast period.

By Application

Intelligence, Surveillance, and Reconnaissance (ISR) Led Market as Real-Time Data Processing is Critical for Decision-Making

Based on the application, the market is segmented into cybersecurity, intelligence, surveillance, and reconnaissance (ISR), command and control (C2), and others.

The Intelligence, Surveillance, and Reconnaissance (ISR) segment led the market with 36.1% share as modern battlefield operations generate massive volumes of real-time data from drones, satellites, ground sensors, and reconnaissance platforms that must be processed instantly to provide actionable intelligence. Edge computing enables local analysis of video feeds, radar signals, and sensor inputs, reducing latency and ensuring rapid threat detection and situational awareness even in contested or communications-denied environments.

The cybersecurity segment is expected to witness the highest CAGR of 15.9% during the forecast period.

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

MILITARY EDGE COMPUTING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Military Edge Computing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market was valued at USD 1.26 billion in 2025. North America holds the majority of the military edge computing market share due to the region’s early and large-scale adoption of advanced digital warfare technologies and sustained investment in distributed computing architectures. Strong collaboration between the Department of Defense and leading defense contractors and cloud technology providers has accelerated the integration of AI-enabled edge solutions across land, air, and maritime platforms. For instance,

- In September 2025, Google Cloud was awarded a USD 470 million contract to deliver a U.K. sovereign cloud for the U.K. Ministry of Defence (MOD). The solution will be built on Google Distributed Cloud (air-gapped), ensuring data sovereignty, high security, and strict control of sensitive defense data within the U.K.

U.S. Military Edge Computing Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was valued at USD 1.11 billion in 2025, accounting for roughly 32.5% of military edge computing sales. The U.S. is driving demand through programs such as Joint All-Domain Command and Control, large-scale ISR modernization, and the deployment of autonomous and semi-autonomous platforms that require real-time data processing at the tactical edge.

Europe

Europe is projected to record a growth rate of 14.0% in the coming years, and was valued at USD 0.94 billion in 2025. Heightened regional security concerns and a strong shift toward joint and coalition operations drive this. European nations are investing in multi-domain command and control systems, advanced ISR platforms, and secure battlefield networks to enhance interoperability across NATO forces, all of which require low-latency edge data processing.

U.K. Military Edge Computing Market

The U.K. market in 2025 was valued at USD 0.20 billion, representing roughly 5.8% of global Military Edge Computing revenues.

Germany Military Edge Computing Market

Germany’s market was valued at USD 0.15 billion in 2025, equivalent to around 4.3% of global Military Edge Computing sales.

Asia Pacific

Asia Pacific is expected to grow with the highest CAGR, and was valued at USD 0.78 billion in 2025. The region is rapidly expanding due to its mature publishing industry, high digital literacy, and strong adoption of e-learning and professional development platforms. Countries like the U.K., Germany, and France have well-established digital infrastructure and a culture of paying for premium content, including eBooks, journals, and subscription-based publications. Additionally, stringent copyright laws and robust digital rights management encourage publishers to invest in digital platforms. At the same time, growing demand for multilingual content across the region supports the widespread use of Military Edge Computing solutions.

Japan Military Edge Computing Market

The Japan market in 2025 was valued at USD 0.08 billion, accounting for roughly 2.3% of global Military Edge Computing revenues.

China Military Edge Computing Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at USD 0.35 billion, representing roughly 10.2% of global Military Edge Computing sales.

India Military Edge Computing Market

The India market in 2025 was valued at USD 0.15 billion, accounting for roughly 4.3% of the global market share.

South America and Middle East & Africa

The Middle East & Africa region is expected to grow at the second-highest CAGR in the market. It is driven by increasing investments in defense modernization and the need to enhance real-time situational awareness across complex operational environments. Countries in the Middle East are rapidly upgrading ISR capabilities, border surveillance systems, and unmanned platforms to address persistent regional conflicts and asymmetric threats, driving demand for localized data processing and AI-enabled edge solutions.

South America is expected to grow at a stable CAGR, driven by gradual defense modernization and steady investments in surveillance, border security, and internal security operations, rather than large-scale force transformation.

GCC Military Edge Computing Market

The GCC market was valued at USD 0.11 billion in 2025, representing roughly 3.2% of global Military Edge Computing revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Implement Strategic Initiatives to Adapt to Technological Advances

Market players are expanding their edge computing portfolios to meet the growing demand for low-latency, secure, and AI-enabled battlefield solutions. They are implementing various strategic initiatives, such as partnerships, joint ventures, and acquisitions, to expand their technological capabilities and global presence.

LIST OF KEY MILITARY EDGE COMPUTING COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Raytheon Technologies (U.S.)

- General Dynamics (U.S.)

- BAE Systems (U.K.)

- Thales Group (France)

- Leonardo (Italy)

- Hewlett Packard Enterprise (U.S.)

- Cisco Systems (U.S.)

- L3Harris Technologies (U.S.)

- IBM Corporation (U.S.)

- Microsoft (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Oracle announced that the Royal Navy has deployed its Roving Edge Infrastructure aboard HMS Prince of Wales, highlighting a key advancement in the military edge computing market. The rugged, cloud-at-the-edge system enables secure, on-board AI processing and data analysis in disconnected or contested environments, allowing faster decision-making while maintaining full control over sensitive military data.

- October 2025: One Stop Systems (OSS) showcased rugged, battlefield-ready edge computing systems at the 2025 AUSA conference. Their ultra-dense, enterprise-class compute solutions are designed to bring data center capabilities directly to the battlefield, supporting Army ground vehicles, aviation, and C5ISR platforms.

- July 2025: The U.K. Ministry of Defence (MOD) announced to launch of a USD 241.9 million AI and Edge Services Framework to modernize defense operations. The initiative, part of the ASGARD Transformative Capability Initiative, aims to enhance real-time decision-making through AI/ML and edge computing to deliver low-latency, reliable battlefield systems.

- April 2025: Vantiq and C4i Systems launched “VANGUARD AIX”, an AI-powered edge computing solution for defense and emergency operations. The system combines Vantiq’s real-time intelligence platform with C4i’s rugged AI Accelerator, including a large language model, to enhance situational awareness, threat detection, and autonomous responses.

- February 2025: Anduril demonstrated its Menace Family of Systems during the U.S. Marine Corps’ Steel Knight exercise, showcasing advanced edge computing and communications at the tactical edge. The system enabled real-time aggregation and sharing of multi-domain sensor data, giving Marines faster situational awareness and decision-making in disconnected and contested environments.

- February 2025: One Stop Systems (OSS) secured USD 6 million in DoD contracts to deliver AI edge computing for P-8A Poseidon aircraft and Virginia Class submarines. Their rugged systems provide real-time sensor processing and AI at the edge, enhancing operational performance in critical military missions. These contracts reinforce OSS’s role as a key provider of high-performance defense computing solutions.

- June 2024: Shield AI and Parry Labs successfully integrated Shield AI’s Hivemind AI Pilot with Parry Labs’ EC Micro edge computing system on a Kratos MQM-178 Firejet. The AI autonomously piloted the aircraft using only onboard computing, demonstrating rapid deployment, advanced autonomy, and scalable edge computing for multiple platforms.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Application, End-user, and Region |

| By Component |

|

| By Deployment |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.42 billion in 2025 and is projected to reach USD 10.32 billion by 2034.

In 2025, the market value stood at USD 1.26 billion.

The market is expected to exhibit a CAGR of 13.9% during the forecast period of 2026-2034.

By End-user, the land segment led the market.

Budget increases and technological modernization programs drive market growth.

Lockheed Martin, General Dynamics, Microsoft, and Raytheon Technologies are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us