Network Centric Warfare Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Military Domain Level (Tactical, Operational, and Strategic), By Application (C4ISR, Electronic Warfare, Command & Control, Situational Awareness, Cyber Warfare, Strategic & Tactical Support, and Others), By Procurement Cycle (New Procurement, Mid-Life Upgrades/Modernization, and Service & Lifecycle Support), By Platform (Land Vehicles and Command Posts, Aircraft and Aerial Platforms, Maritime Platforms, and Space), By End User, and Regional Forecast, 2026-2034

Network Centric Warfare Market Size and Future Outlook

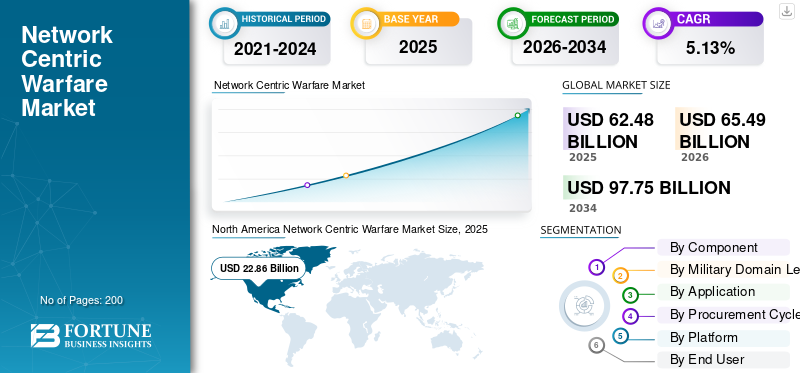

The global network centric warfare market size was valued at USD 62.48 billion in 2025 and is projected to grow from USD 65.49 billion in 2026 to USD 97.75 billion by 2034, exhibiting a CAGR of 5.13% during the forecast period. North America dominated the global network-centric warfare market with a market share of 36.59% in 2025. The industry growth driven by multi-domain operations integration, digital battlefield transformation, secure communications modernization, artificial intelligence-enabled command systems, and increasing defense digitization investments worldwide.

Network-centric warfare is a military doctrine or theory that translates information advantage and technological capabilities into competitive advantage through the computer networking of dispersed forces. The integration of data from various sensors, platforms, and command systems enables real-time information sharing and coordinated actions across all levels of organization.

Key players in the market include established defense contractors such as Lockheed Martin Corporation, Raytheon Technologies (RTX Corporation), Northrop Grumman Corporation, General Dynamics Corporation, BAE Systems PLC, and Thales Group. Specialized technology firms providing products or services to these primes include L3Harris Technologies, Elbit Systems, Leonardo S.p.A., and Cisco Systems.

The Network-centric warfare market is undergoing structural expansion as defense organizations prioritize integrated command architectures, real-time data sharing, and multi-domain operational superiority. Modern military doctrine emphasizes interconnected platforms, distributed decision-making, and rapid situational awareness across land, air, sea, cyber, and space domains. This shift positions network-centric capabilities as foundational to future force structures.

Network-centric warfare market size growth is supported by rising defense budgets, modernization of legacy command and control systems, and increasing reliance on secure, resilient communications networks. Armed forces are investing in interoperable systems that unify sensors, shooters, and decision-makers within a cohesive digital ecosystem. Integration of artificial intelligence, advanced analytics, and edge computing enhances operational tempo and precision.

Network-centric warfare market share remains concentrated among established defense contractors with expertise in command, control, communications, computers, intelligence, surveillance, and reconnaissance architectures. However, competitive dynamics are evolving as cybersecurity firms, software integrators, and specialized technology providers contribute modular and scalable capabilities.

Network-centric warfare market trends indicate accelerated adoption of software-defined networks, secure cloud-enabled defense infrastructure, and cross-domain integration frameworks. Multi-layered cybersecurity, satellite communications, and resilient battlefield networks are strategic priorities. Procurement increasingly favors open architectures that allow incremental capability upgrades and interoperability with allied systems.

Network-centric warfare market growth is expected to remain sustained throughout the forecast period. Expansion is driven by geopolitical tensions, hybrid warfare threats, and the need for data dominance in contested environments. Regional adoption patterns vary according to defense spending and technological maturity, but digital battlefield integration is becoming central to global military modernization strategies.

Download Free sample to learn more about this report.

Network Centric Warfare Market KEY TAKEAWAYS

- 2025 Market Size: USD 62.48 billion

- 2026 Market Size: USD 65.49 billion

- 2034 Forecast Market Size: USD 97.75 billion

- CAGR: 5.13% from 2026–2034

- North America dominated the network centric warfare market with a 36.59% share in 2025.

- The hardware sub-segment accounted for the largest market share of 56.18% in 2025.

- The tactical sub-segment held a leading share of 45.15% in 2025.

North America

North America held 36.59% share in 2025, valued at USD 22.86 billion.

Europe

Europe market is expected to witness steady growth during the forecast period.

Asia Pacific

Asia Pacific is the fastest-growing regional market, driven by rising defense modernization investments.

U.S.

U.S. Market remained the dominant contributor within North America in 2025.

Japan

Japan Market is projected to record steady growth through the forecast period.

Read More

Network Centric Warfare Market Trends

Software-Defined Radio Proliferation and Edge Computing Advancement Anticipate Market Growth

The proliferation of Software-Defined Radios and the advancement of edge computing architectures are the defining technological trends that reshape the network centric warfare landscape by introducing unparalleled flexibility in tactical communications and distributed data processing capabilities. SDRs are revolutionizing military communications as they support frequency agility, multiband operability, and encrypted data exchange critical to joint-force missions and allied coalition operations.

- In October 2025, the Indian Army inked a landmark contract for the procurement of its first indigenously designed and manufactured Software Defined Radios developed by DRDO and produced by Bharat Electronics Limited, incorporating Mobile Ad hoc Network capabilities for network-centric operations.

Open architecture adoption is a defining trend in the Network-centric warfare market. Defense agencies increasingly demand modular, upgradeable systems to avoid vendor lock-in. This approach enables incremental capability enhancement.

Cloud-enabled defense infrastructure is expanding. Secure cloud environments support centralized data aggregation, analytics, and collaboration. Hybrid deployment models balance resilience and flexibility. Edge computing integration enhances battlefield responsiveness. Processing data closer to sensors reduces latency and supports real-time decision-making. This trend aligns with distributed operational concepts.

Cyber resilience investment continues to grow. Zero-trust architectures, encryption enhancements, and continuous monitoring frameworks are integrated into network-centric systems. Security considerations now shape procurement decisions. Space-based connectivity is gaining strategic importance. Satellite networks enable global communication and positioning capabilities. Integration of space assets strengthens cross-domain coordination.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Geopolitical Instability and Real-Time Situational Awareness Requirements Drives Market Growth

The tightening geopolitical situation and regional conflicts have become a critical catalyst that drives investment in network centric warfare systems capabilities, wherein nations are putting a premium on information superiority and ensuring quicker strategic decision-making mechanisms. Russia's continued aggression in Ukraine has structurally altered the European security architecture, forcing NATO member states to accelerate defense modernization programs, especially on electronic warfare, cybersecurity, and multi-domain C4ISR integration via initiatives such as the European Defence Fund and Permanent Structured Cooperation (PESCO).

- In January 2025, the US Army Aviation Missile Technology Consortium awarded Northrop Grumman a USD 481 million contract to expand software development for the Integrated Battle Command System. Of this total, USD 347.6 million will be put toward Polish defense efforts and USD 133.7 million toward US military and Guam Defense System applications.

Defense modernization programs represent the primary driver of the Network-centric warfare market. Armed forces seek integrated command and control frameworks capable of linking distributed assets across multiple domains. Digital transformation initiatives prioritize interoperability and rapid information exchange. Growing complexity of modern warfare accelerates demand. Multi-domain operations require seamless coordination among land, air, maritime, cyber, and space platforms. Network-centric architectures enable synchronized mission execution and enhanced situational awareness.

Advances in secure communications technologies further support market expansion. Satellite communications, software-defined radios, and encrypted data links improve reliability and resilience. These capabilities are critical in contested environments where electronic warfare threats are increasing. Artificial intelligence integration strengthens operational value. AI-driven analytics support target identification, predictive logistics, and real-time threat assessment. Automated decision-support systems reduce response times and improve mission effectiveness.

Market Restraints

Interoperability Challenges and Legacy System Integration Complexities Hamper Market Growth

There are also significant constraints weighing on the network centric warfare market due to interoperability challenges that continue to hinder fast and seamless communication and data sharing between diverse military assets from different manufacturers and technology providers.

Moreover, military forces of different nations or service branches often have diverse legacy systems that were not designed to be integrated with contemporary network-centric technologies, therefore making the integration landscape quite complex, where updating or replacing embedded older platforms requires substantial capital investment along with extended implementation timelines.

High development and integration costs constrain the Network-centric warfare market. Complex systems require advanced hardware, secure software platforms, and extensive testing. Budget allocation challenges can delay procurement cycles. Cybersecurity vulnerabilities present significant risk. As networks expand, exposure to cyber intrusion and electronic warfare increases. Ensuring secure architectures demands continuous investment and specialized expertise.

Legacy system integration remains a technical challenge. Many defense organizations operate outdated infrastructure incompatible with modern network-centric frameworks. Upgrading these systems requires phased implementation and additional funding. Interoperability complexity across allied forces adds operational constraints. Differences in standards, encryption protocols, and procurement policies complicate seamless integration. Harmonization efforts can be time-consuming and politically sensitive.

Market Opportunities

Artificial Intelligence Integration and Autonomous System Proliferation Drives Future Market Growth

The integration of AI, machine learning algorithms, and autonomous defense platforms has opened up transformative opportunities for the network centric warfare market, enhancing decision-making and operational efficiencies that will fundamentally reshape military command architectures. AI-driven fusion engines will revolutionize capabilities in NCW systems by enabling faster data processing, superior decision-support mechanisms, and improved network resilience in contested environments, where traditional communication links may be degraded or denied.

- In February 2024, successful 5G military demonstrations by Lockheed Martin featured the integration of the OSIRIS testbed with unmanned aerial vehicles during the Steel Knight 2024 exercise to support secure, simultaneous connections and real time data exchange between tactical radars and command systems.

Modernization of legacy command infrastructures presents a major opportunity within the Network-centric warfare market. Many armed forces require comprehensive system replacement or upgrade to meet digital operational standards. Emerging economies offer additional growth potential. Rising defense budgets in developing regions create demand for integrated communication and surveillance systems. Local industrial partnerships facilitate capability development.

Space and cyber domain integration represents a significant opportunity. As warfare expands into new domains, demand for unified command frameworks increases. Network-centric architectures provide cross-domain synchronization. Artificial intelligence deployment offers incremental value creation. Vendors that deliver scalable analytics and automation capabilities can differentiate offerings and secure long-term contracts.

Market Challenges

Spectrum Management Complexities and Workforce Skill Deficits Hinder Market Growth

The significant challenges faced by the network centric warfare industry include spectrum management complexities and critical shortages of skilled workforce who can operate and maintain increasingly sophisticated networked defense systems.

As adversarial threats continue to proliferate, electronic warfare capabilities are evolving rapidly, with the shift toward network-centric operations placing an increased focus on real-time data sharing and situational awareness, necessitating advanced spectrum management tools and trained operators to retain dominance in contested electromagnetic environments.

SEGMENTATION ANALYSIS

By Component

Artificial Intelligence AI and Machine Learning Integration Driving Exponential Software Growth

The global market is segmented by component into hardware, software, and services.

Software

The software sub-segment is emerging as the fastest-growing component within the network centric warfare market, with expectations to achieve a compound annual growth rate of 6.98% through 2026-2034, substantially greater than the overall market expansion trajectory. This accelerated growth is basically due to the increasing integration of artificial intelligence, machine learning algorithms, and advanced analytics platforms that allow for automated threat detection, predictive battlefield intelligence, and autonomous decision-making capabilities across multi-domain operational environments.

This segment includes command and control platforms, data fusion engines, cybersecurity systems, artificial intelligence analytics, and mission planning tools. Increasing reliance on digital decision-support capabilities shifts value concentration toward software-centric architectures. Open standards and modular frameworks allow continuous upgrades without full hardware replacement. As defense agencies prioritize real-time intelligence and interoperability, software contributes disproportionately to Network-centric warfare market share. Subscription-based and upgrade-driven models enhance recurring revenue potential.

Hardware

The hardware sub-segment would witness a dominant market position, accounting for about 56.18% of the network centric warfare market in 2025, as the establishment and maintenance of secure battlefield connectivity in real time require physical communication infrastructure, sensor systems, computing platforms, and ruggedized equipment.

Hardware constitutes the foundational layer of the Network-centric warfare market. This segment includes communication devices, software-defined radios, satellite terminals, sensors, secure routers, ruggedized servers, and edge computing modules. Demand is driven by modernization of tactical communication networks and battlefield connectivity infrastructure.

Hardware procurement often aligns with platform upgrades and new system integration programs. While capital intensive, hardware typically represents a lower margin segment compared to software and services. However, its strategic importance remains high because physical infrastructure determines network reliability and resilience. Growth is steady, supported by continuous replacement cycles and integration of advanced electronic warfare protection features.

Services

Services encompass integration, maintenance, cybersecurity monitoring, training, and lifecycle support. As system complexity increases, demand for long-term service contracts grows. Governments prioritize managed services to ensure operational continuity. This segment supports predictable cash flow and strengthens vendor-client relationships. Service-driven value expansion reinforces sustained Network-centric warfare market growth across extended program lifecycles.

By Military Domain Level

Multi-Domain Command and Control Integration Driving Operational Segments Growth

The global market is segmented by military domain level into tactical, operational, and strategic.

Operational Level

The fastest growth rate among the segments would be obtained by the operational sub-segment of the network centric warfare market, growing at a CAGR of 5.58% through 2026-2034, considerably above tactical domain expansion rates. Basically, the accelerated growth is based on the military forces transitioning toward multi-domain operations that necessitate integrated command-and-control systems with coordinated capabilities in land, air, sea, cyber, and space to be included in unified operational architectures.

Operational-level systems coordinate activities across larger formations and regional theaters. Data aggregation, mission planning, and logistics integration define this layer. Investments aim to synchronize assets across domains and maintain command visibility.

Tactical Level

Tactical-level systems focus on frontline connectivity and unit-level coordination. Secure radios, handheld devices, and vehicle-mounted communication modules dominate this segment. Demand is driven by need for situational awareness at the operational edge. Tactical integration supports rapid decision cycles and mission flexibility.

The tactical sub-segment would continue to maintain its leading position in the market with a share of around 45.15% in the global network centric warfare market in 2025, due to the vital need for real-time communication and coordination systems from the soldier level to battalion-level command elements.

Strategic Level

Strategic-level systems support national command authorities and cross-theater coordination. These architectures integrate space, cyber, and intelligence networks. Although lower in volume, strategic systems command high value due to complexity and security requirements.

By Application

Cyber Domain Integration and Multi-Domain Operations Enablement Anticipate Market Growth

The global market is segmented by application into C4ISR, electronic warfare, command & control, situational awareness, cyber warfare, strategic & tactical support, and others.

Cyber Warfare

The cyber warfare sub-segment of the network centric warfare market is observing the fastest growth trajectory, as it moves ahead at a CAGR of 7.17% during 2026-2034. Such accelerated growth is fundamentally driven by military forces' integration of cyberspace as the fifth operational domain, which requires advanced defensive and offensive cyber capabilities seamlessly coordinated with operations in land, air, sea, and space within unified multi-domain frameworks.

Cyber warfare capabilities protect network infrastructure and support offensive cyber operations. Investment in cyber defense supports resilience and regulatory compliance.

C4ISR

The C4ISR sub-segment enjoys a dominant market position, accounting for 37.46% of the market share in the year 2025 due to the integral dependence on integrated command, control, communications, and intelligence capabilities that enable almost all modern military operations in each operational domain.

Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR) applications represent the largest share of the Network-centric warfare market. Integration of sensors and command nodes enables persistent awareness and coordinated response. This segment anchors overall market value.

Electronic Warfare

Electronic warfare integration enhances resilience against jamming and cyber threats. Network-centric systems incorporate spectrum monitoring and adaptive response capabilities. Growth reflects rising electronic conflict intensity.

Command & Control

Command and control applications provide centralized decision frameworks. Digital dashboards and secure data channels enable synchronized operations. Adoption aligns with doctrine emphasizing real-time coordination

By Procurement Cycle

Advanced Predictive Maintenance and Sustainment Services Expansion Propel Segmental Growth

The global market is segmented by procurement cycle into new procurement, mid-life upgrades/modernization, and service & lifecycle support.

Service & Lifecycle Support sub-segment lead the network centric warfare market growth, and is estimated to be the fastest growing with a 5.56% CAGR during the forecast period of 2026-2034. The accelerated growth rate pertains to military forces' increasing dependence on specialist sustainment services that offer system integration, training, maintenance, lifecycle management, and predictive analytics.

The new procurement sub-segment maintains the dominant market position, with 61.34% share of the market in 2025, driven by military forces' sustained investment in deploying next-generation command and control systems, advanced sensor networks, and integrated communication platforms that collectively establish modernized digital battlespace architectures.

By Platform

Growing Launches of Low Earth Orbit Satellite Constellation Proliferation and Deployment Drives Segmental Growth

The global market is segmented by platform into land vehicles and command posts, aircraft and aerial platforms, maritime platforms, and space.

The network centric warfare market’s fastest growth trajectory comes from the space sub-segment, projected to grow at a CAGR of 6.96% during the forecast period of 2026-2034, or significantly above the terrestrial platform expansion rates. The fundamental reasons for this accelerated growth rate lie with military forces deploying proliferated satellite constellations providing persistent, global coverage for communications, surveillance, reconnaissance, and positioning capabilities that collectively form the backbone of modern multi-domain command and control architectures.

Land vehicles & command posts sub-segment dominates the market share with around 36.63% in 2025 in the platform market of network centric warfare due to continuous investment by military forces for deploying integrated command vehicles, mobile tactical operation centers, and networked armored platforms that together establish distributed command architecture.

To know how our report can help streamline your business, Speak to Analyst

By End User

Multi-Domain Operations Coordination and Joint Task Force Modernization Drives Market Growth

The global market is segmented by end user into land forces, naval forces, air forces, and joint commands / defense agencies.

Joint commands & defense agencies sub-segment is estimated to be the fastest growth rate of 6.52% CAGR during the forecast period, significantly higher than that of the other service branches' growth. This is essentially due to the unified combatant commands established in recent years that will need state-of-the-art C4ISR architecture, allowing smooth coordination between military operations across geographical and operational regions.

The land forces sub-segment maintains the dominant market position with a share of about 31.88% in the end-user market in 2025, driven by continued investment by military forces in deploying integrated tactical networks, battlefield management systems, and mobile command platforms that support ground combat operations across all operational environments.

Network Centric Warfare Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America Network-centric warfare Market Analysis:

North America continues to have the leading position in the global market, with around 36.58% of the global network centric warfare market share. The dominance is a result of the defense budget's focus on modernization of military capabilities, including investment in the Pacific Deterrence Initiative of USD 9.9 billion for resilient and distributed basing, missile warning and tracking architecture, and autonomous systems deployment.

North America represents the largest Network-centric warfare market, driven by sustained defense modernization and multi-domain integration initiatives. Advanced command architectures and secure communications upgrades support continuous capability enhancement. Strong investment in artificial intelligence and cyber resilience reinforces technological leadership. These factors sustain significant Network-centric warfare market share and consistent growth across tactical, operational, and strategic programs.

United States Network-centric warfare Market:

The United States dominates the Network-centric warfare market through extensive procurement, research funding, and digital battlefield transformation programs. Integration of C4ISR and secure cloud-enabled defense systems remains a priority. Joint-domain operations doctrine drives cross-platform interoperability investment. High defense budgets support steady Network-centric warfare market size expansion nationwide.

The U.S. market represents the transformation of military operations, wherein information dominance and integration of near real-time data are the driving factors toward operational effectiveness. The shift in strategy toward multi-domain operations within the U.S. military necessitates seamless integration of capabilities across air, land, maritime, space, and cyber domains that anticipate growth in the U.S. market.

North America Network Centric Warfare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific Network-centric warfare Market Analysis:

The network centric warfare market growth capabilities is accelerated in the Asia Pacific region due to geopolitical tensions, border disputes, and huge defense budget allocations amounting to USD 632.2 billion in 2025. Driven by China, which accounts for 47.31% market share in region with value of USD 7.37 billion, including Japan, South Korea, Taiwan, and Australia collectively increasing the spending on defense modernization initiatives, the expansion in this region's NCW is characteristic of its emphasis on indigenous defense manufacturing and investment in indigenous RDT&E.

Asia-Pacific represents a high-growth Network-centric warfare market driven by rising defense spending and regional security competition. Countries invest in advanced command systems, secure communications, and surveillance integration. Rapid modernization initiatives support increasing Network-centric warfare market size across tactical and strategic domains regionally.

Japan Network-centric warfare Market:

Japan’s Network-centric warfare market focuses on resilient communication infrastructure and interoperability enhancement. Investment supports integration of land, maritime, and air assets within unified command systems. Emphasis on cybersecurity and satellite connectivity strengthens operational readiness. These initiatives contribute to steady Network-centric warfare market growth aligned with national security strategy.

China Network-centric warfare Market:

China’s Network-centric warfare market is driven by large-scale defense digitization and integration of multi-domain command frameworks. Significant investment in secure communications and artificial intelligence strengthens networked operations. Expansion of satellite and cyber capabilities supports rising Network-centric warfare market share within regional and global defense modernization efforts.

Europe Network-centric warfare Market Analysis:

Acceleration in network centric warfare market share development in Europe has become high, with the entire European Union Member States reaching unprecedented defense spending. R&D spending by emerging European countries is increasing steadily. Synchronized joint strategic initiatives take priority in sovereign technology infrastructure including AI, quantum computing, semiconductors, and secure cloud capabilities. This shows geopolitical determination to reduce dependencies from outside and establish European technological sovereignty.

Europe’s Network-centric warfare market is shaped by multinational defense cooperation and interoperability objectives. Member states invest in secure communication frameworks and modernization of legacy systems. Emphasis on joint exercises and coordinated command structures supports cross-border integration. Moderate but stable Network-centric warfare market growth reflects ongoing digital transformation across European armed forces.

Germany Network-centric warfare Market:

Germany’s Network-centric warfare market emphasizes secure communications, interoperability, and cyber resilience. Modernization programs focus on upgrading command networks and integrating digital platforms across land and air forces. Investment in secure data infrastructure supports long-term capability development. These initiatives sustain measured Network-centric warfare market growth aligned with national defense priorities.

United Kingdom Network-centric warfare Market:

The United Kingdom Network-centric warfare market prioritizes digital integration across joint forces. Programs emphasize secure data sharing, multi-domain coordination, and cyber defense capability. Defense modernization funding supports system upgrades and new procurement. Strong alignment with allied interoperability standards reinforces steady Network-centric warfare market growth.

Middle East & Africa Network-centric warfare Market Analysis:

The Middle East defense market is expanding considerably, with value of USD 4.15 billion in 2025, with a CAGR of 4.54% from 2026-2034. This has opened huge procurement opportunities for advanced C4ISR systems owing to the persistent regional security threats, geopolitical tensions, and counter-terrorism operations demanding better architectures for command and control and situational awareness.

The Middle East and Africa Network-centric warfare market is influenced by security challenges and modernization priorities. Governments invest in integrated command systems and secure communications. International partnerships support capability development. Market growth depends on defense budgets and regional stability trends.

Latin America Network-centric warfare Market Analysis:

Latin America is witnessing a moderate yet stable growth in the market size, with Brazil heading the largest regional defense budget. This growth is attributed to rising cross-border tensions, threats related to transnational organized crime, and modernization of existing military equipment driving demand for advanced communication systems, weapon platforms, and intelligence capabilities.

Latin America demonstrates gradual development within the Network-centric warfare market. Defense modernization focuses on secure communications and surveillance upgrades. Budget constraints limit large-scale transformation, but selective procurement supports incremental growth. Regional cooperation initiatives contribute to steady Network-centric warfare market expansion.

Network-centric warfare Industry Competitive Landscape

Key Industry Players

Network-centric warfare Industry Competitive Landscape

The global network centric warfare market is highly competitive, with established defense prime contractors such as Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation (Raytheon), BAE Systems PLC, L3Harris Technologies, and Thales Group controlling a large market share due to an extensive portfolio of government contracts, proprietary IP in intelligence surveillance and reconnaissance (ISR) systems, and vertically integrated manufacturing capabilities.

This competitive advantage is sustained by several industry leaders having huge investments in R&D, estimated at over several billion dollars annually, which ensures continuous innovation in AI-enabled fusion engines, protocols for quantum-resistant encryption, software-defined radio architecture, and resilient satellite communication constellations.

The Network-centric warfare industry competitive landscape is characterized by dominance of major defense contractors complemented by specialized cybersecurity and software integration firms. Competition centers on interoperability, secure architecture design, and lifecycle service capability. Vendors differentiate through system integration expertise and compliance with stringent defense standards.

Leading contractors hold significant Network-centric warfare market share through large-scale command and control programs and multi-domain integration projects. Their portfolios typically span hardware, software, and managed services. Long-standing relationships with defense ministries provide procurement continuity.

Mid-tier firms and emerging technology providers focus on artificial intelligence, cybersecurity, and edge computing. These companies influence Network-centric warfare market trends by introducing scalable analytics platforms and modular architectures. Partnerships with prime contractors facilitate integration into broader programs. Strategic alliances are central to competitive positioning. Vendors collaborate across space, cyber, and communications sectors to deliver comprehensive solutions. Open architecture frameworks enhance interoperability and customer retention.

List of Network Centric Warfare Market Companies Profiled

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- RTX Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- BAE Systems plc (U.K.)

- Thales Group (France)

- General Dynamics Mission Systems, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- HENSOLDT AG (Germany)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Indra Sistemas, S.A. (Norway)

- Kongsberg Defence & Aerospace AS (Japan)

- Fujitsu Defense & National Security Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Scytalys, a company from Greece that focuses on interoperability systems, has secured two contracts from Canada as part of the Tactical Integrated Command, Control, and Communications (TIC3) Air Project (Line of Effort 4). With a total value of around USD 9.7 million, these contracts involve the development, implementation, and integration of a minimum of five Link-22 Tactical Data Link (TDL) systems.

- October 2025: The Saab Gripen is among the eight competitors for the Indian Air Force’s anticipated procurement of 114 Multi-Role Fighter Aircraft (MRFA). Saab, a leading Swedish defense technology company, has revealed its collaboration with domestic manufacturers to accelerate the indigenization of the aircraft.

- October 2025: The Integrated Battle Command System (IBCS) of the US Army successfully shot down missile threats in a flight test conducted at the White Sands Missile Range in New Mexico. This test represented the completion of the Follow-On Operational Test and Evaluation, an important step toward the full operational deployment within army air defense units.

- June 2025: The Government of Pakistan revealed that it has signed the biggest defense export deal in its history. This agreement with Azerbaijan involves the supply of 40 JF-17 Thunder fighter jets, amounting to USD 4.6 billion, along with a USD 2 billion investment package.

- September 2025: Collins Aerospace, part of RTX, has obtained a significant contract with the NATO Communications and Information Agency for its Electronic Warfare Planning and Battle Management (EWPBM) solution.

REPORT COVERAGE

The global network centric warfare market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the global market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product type launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.13% from 2026-2034 |

| Unit | USD Billion |

| Segmentation | By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Region |

|

By Component

By Military Domain Level

By Application

By Procurement Cycle

By Platform

By End User

|

|

| By Region |

North America (By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Country)

Europe (By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Country)

Asia Pacific (By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Country)

Middle East (By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Country)

Latin America (By Component, By Military Domain Level, By Application, By Procurement Cycle, By Platform, By End User, By Sub-Region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 62.48 billion in 2025 and is projected to reach USD 97.75 billion by 2034.

In 2025, the Europe market value stood at USD 17.12 billion.

The market is expected to exhibit a 5.13% CAGR during the forecast period of 2026-2034.

The space sub-segment is expected to hold the highest CAGR over the forecast period.

Geopolitical instability and real-time situational awareness requirements drives the market growth

Lockheed Martin Corporation, Raytheon Technologies (RTX Corporation), Northrop Grumman Corporation, General Dynamics Corporation, BAE Systems PLC, Thales Group and among others are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us