Tactical Communication Market Size, Share & Industry Analysis, By Platform (Land Based, Airborne, Naval, and Space-Based Systems), By Installation Type (Man-portable, Vehicle-mounted, Aircraft-integrated, Shipborne/Submarine Systems, & Others), By Communication Type (Voice, Data & Video Communication Systems), By Technology (SDR, SATCOM, LOS Radio Systems, BLOS Systems, & Others), By Component (Transceivers & Antennas, Headsets, Terminals, and Handheld Radios, & Others), By Frequency Band (HF, VHF, UHF, & SHF/EHF), By Application, By End User, and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

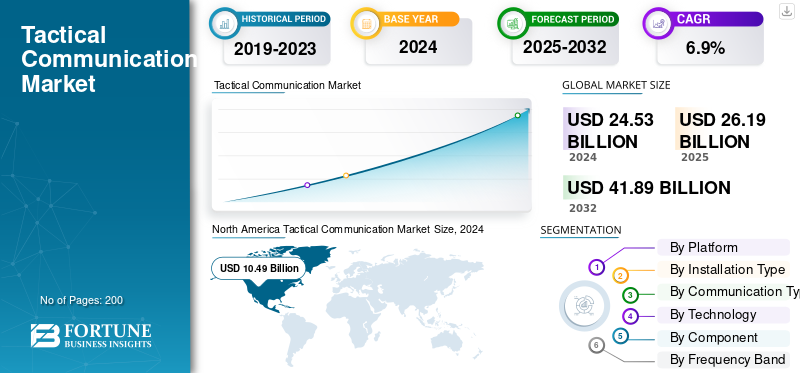

The global tactical communication market size was valued at USD 26.2 billion in 2025. The market is projected to grow from USD 28 billion in 2026 to USD 48.50 billion by 2034, exhibiting a CAGR of 7.10% during the forecast period. North America dominated the tactical communication market with a market share of 42.40% in 2025.

Tactical communication refers to the secure exchange of voice, data, and imagery between military units and command centers in fast-changing, high-risk environments. These systems are built to perform under harsh conditions, supporting missions where reliability and speed are critical. The market is growing as defense forces modernize their networks and shift toward digital, interoperable, and AI-enabled systems. Rising demand for secure communication, real-time situational awareness, cross-force coordination, and software defined radios (SDR) is driving this shift. Governments are also investing heavily in next-generation command networks to enhance decision-making and operational efficiency in modern warfare.

Key players such as L3Harris Technologies, Thales Group, BAE Systems, Collins Aerospace, Elbit Systems, and Rohde & Schwarz are shaping the market with advances in software-defined, frequency-agile, and cyber-secure systems. Their innovations support enhanced communication across air, land, and naval platforms while ensuring network resilience against jamming and interference. Emerging players are exploring edge analytics, satellite integration, and cloud-based control nodes to boost connectivity and reduce latency in field operations.

Download Free sample to learn more about this report.

ACTICAL COMMUNICATION MARKET KEY Takeaways

- 2025 Market Size: USD 26.2 billion

- 2026 Market Size: USD 28.0 billion

- 2034 Forecast Market Size: USD 48.50 billion

- CAGR: 7.10% from 2026–2034

- North America dominated the tactical communication market with a 42.40% share in 2025.

- The Land Based Systems segment accounted for the largest market share of 57.72% in 2026.

- The Man-Portable segment is projected to hold a 31.88% share in 2026.

North America

North America held 42.35% share in 2025, valued at USD 11.09 billion.

Europe

Europe market valued at USD 5.39 billion in 2025.

Asia Pacific

Asia Pacific market valued at USD 5.09 billion in 2025.

U.S.

U.S. Market projected to reach USD 10.91 billion by 2026.

Japan

Japan: Market projected to reach USD 0.76 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Real-Time Situational Awareness is key Drivers of Market Growth

Modern military operations rely heavily on instant, secure, and uninterrupted information flow between forces on the ground, in the air, and at sea. As threats evolve and missions become more data-intensive, defense forces are investing in tactical communication systems that enable real-time situational awareness and faster decision-making. These systems allow troops to access live intelligence feeds, video surveillance, and sensor data, helping them respond swiftly to battlefield changes. The growing use of AI-based analytics, networked sensors, and software defined radios (SDR) further enhances mission coordination and operational efficiency.

- For instance, in March 2024, the U.S. Army expanded its Integrated Tactical Network (ITN) program to improve real-time data sharing and situational awareness across its brigade combat teams. Similarly, European defense agencies have accelerated digital battlefield programs to ensure joint interoperability and enhance command responsiveness in multinational missions.

MARKET RESTRAINTS

High Integration Complexity and Legacy System Compatibility are Restraining Market Growth

Despite rapid communication technological development, integrating new tactical communication systems with existing legacy infrastructure remains a major challenge. Many defense networks still rely on outdated analog or proprietary systems that are difficult to align with modern IP-based, software-defined, and encrypted architectures. This creates interoperability gaps between different units, services, and allied forces, often leading to communication delays and data loss in joint missions. Additionally, the high cost of upgrading communication fleets combined with long procurement cycles and cybersecurity concerns, further slows large-scale adoption across developing defense programs.

- For example, in July 2024, several NATO member states reported delays in upgrading their tactical radio networks due to compatibility issues with older encryption protocols and platform-specific software.

MARKET OPPORTUNITIES

Growing Adoption of Software-Defined and Network-Centric Systems is Creating New Opportunities

The shift toward software defined radios (SDR) and network-centric warfare architectures is opening new growth avenues in the market. These systems offer unmatched flexibility, allowing militaries to reprogram frequencies, encryption standards, and waveforms on the fly without changing the hardware. This adaptability is vital for modern, multi-domain missions where forces must communicate seamlessly across land, air, sea, and space. As defense agencies worldwide invest in next-generation battlefield networks, opportunities are rising for companies developing AI-driven routing, secure data mesh networks, and cloud-integrated tactical nodes that enhance coordination and speed of command.

- For instance, in May 2024, Thales Group unveiled a new generation of software-defined tactical radios capable of multi-band, multi-waveform communication for joint and coalition operations.

TACTICAL COMMUNICATION MARKET TRENDS

Integration of Artificial Intelligence and Edge Computing is Transforming Tactical Communication

The tactical communication landscape is evolving with the growing use of AI and edge computing to enhance battlefield connectivity and data processing. AI algorithms are being used to automatically manage signal routing, detect interference, and prioritize mission-critical data, reducing human workload and enhanced communication reliability. Meanwhile, edge computing allows data to be processed closer to the source, enabling faster decision-making even in bandwidth-limited or contested environments. Together, these technologies are transforming tactical networks from simple transmission systems into intelligent, adaptive, and self-healing ecosystems that enhance real-time situational awareness.

- For example, in February 2024, BAE Systems announced trials of its AI-powered tactical communication suite designed to optimize data flow and reduce network congestion in field operations.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Cybersecurity Threats and Electronic Warfare Vulnerabilities Pose Major Challenges

As tactical communication systems become more connected and data-driven, they also become more exposed to cyberattacks and electronic warfare (EW) disruptions. Adversaries are increasingly deploying jamming, spoofing, and cyber-intrusion techniques to compromise secure networks and intercept mission-critical information. This creates a significant challenge for defense agencies trying to maintain confidentiality, reliability, and real-time communication in contested environments. Moreover, developing fully secure, encrypted systems that can withstand high-intensity EW attacks without degrading performance adds complexity and cost to military modernization programs. Ensuring continuous protection across multiple platforms land, air, and sea requires constant innovation in encryption algorithms, anti-jamming waveforms, and resilient network architectures.

- For instance, in April 2024, multiple European defense programs faced temporary communication blackouts during large-scale military exercises after simulated jamming attacks disrupted tactical radio links.

Russia-Ukraine War Impact

Russia–Ukraine Conflict Accelerates Modernization and Resilience in Tactical Communication Networks.

The Russia–Ukraine war has become a defining moment for the tactical communication industry, revealing how vital secure and resilient networks are to modern combat. The conflict has demonstrated that the ability to maintain uninterrupted, encrypted communication is often as decisive as weapon capability. Both sides have experienced extensive jamming, cyberattacks, and signal disruptions, underscoring the urgent need for anti-jamming, mesh-based, and satellite-supported tactical systems. This has led to a global push among defense forces to modernize their communication infrastructure, focusing on real-time data sharing, AI-based spectrum management, and network redundancy to maintain operational continuity in contested environments.

A key lesson from the conflict is the strategic value of integrating commercial satellite and defense-grade communication technologies. Ukraine’s successful use of Starlink LEO networks to sustain connectivity despite Russian interference showcased the importance of adaptable, multi-layered communication systems. In response, NATO members and allied nations have accelerated investments in software defined radios, secure cloud C2 platforms, and cyber-hardened tactical data links. Overall, the war has shifted tactical communication from being a support function to a strategic capability, one that defines battlefield agility, command efficiency, and information superiority in modern warfare.

- For example, in 2023, Ukraine’s extensive use of Starlink satellite terminals enabled uninterrupted battlefield communication despite heavy Russian electronic warfare

Segmentation Analysis

By Platform

Extensive Ground Force Modernization, Land-Based Systems Segment Dominates Market

In terms of platform, the market is categorized into land based systems, airborne systems, naval systems, and space-based systems.

The Land Based Systems segment is projecteed to dominate the market with a share of 57.72% in 2026. Land-based tactical communication systems hold the largest tactical communication market share, driven by their extensive use across infantry, armored vehicles, and field command units. These systems serve as the operational backbone for real-time coordination, mission planning, and threat response on the battlefield. The widespread adoption of software-defined radios (SDR), mobile command posts, and mesh networking technologies is fueling growth as armies modernize their ground communication infrastructure. Their scalability, lower deployment cost compared to airborne or naval systems, and direct role in ground-force digitization make them the dominating platform segment.

- For instance, in June 2024, the U.S. Army expanded its Integrated Tactical Network (ITN) rollout to deploy advanced SDR-based communication kits across multiple brigade combat teams.

The space-based systems segment is expected to grow at a fastest CAGR of 10.3% over the forecast period.

By Installation Type

Rising Demand for Mobility and Rapid Field Deployment, Man-Portable Segment Dominates Market

On the basis of installation type, the market is classified into man-portable, vehicle-mounted, aircraft-integrated, ship borne/submarine systems, and fixed command post/shelter-based systems.

The Man-portable segment is expected to lead the market, contributing 31.88% globally in 2026. The man-portable segment leads the market as modern military operations increasingly rely on lightweight, easily deployable systems that keep soldiers connected in fast-changing combat zones. These handheld and backpack radios provide secure voice, data, and video transmission directly at the tactical edge, allowing dismounted troops to coordinate with command centers and other units in real time. The growing emphasis on soldier and military modernization, network-centric warfare, and interoperable software-defined radios (SDRs) has made man-portable systems the preferred choice for ground forces worldwide.

- For instance, in April 2024, L3Harris Technologies received a major contract from the U.S. Army to deliver advanced handheld SDRs under its Leader Radio Program, enhancing connectivity and data exchange for deployed troops.

The vehicle-mounted segment is expected to grow at a fastest CAGR of 8.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Communication Type

Growing Need for Secure and Instant Coordination, Voice Communication Segment Dominates Market

Based on communication type, the market is segmented into voice communication systems, data communication systems, and video communication systems.

The Voice Communication Systems Systems segment is projecteed to dominate the market with a share of 53.69% in 2026. Voice communication systems continue to dominate the market as they remain the most essential and reliable mode of command and control in real-time military operations. Instant voice exchange allows troops, commanders, and allied units to coordinate efficiently, especially in fast-moving or high-stress combat scenarios where every second matters. The introduction of encrypted digital radios and adaptive waveform technologies has further strengthened the relevance of secure voice channels in contested or jammed environments.

- For example, in January 2024, BAE Systems upgraded its tactical radio suite for the British Army, enhancing encrypted voice communication and reducing interference during joint operations.

The segment of data communication systems is growing at a CAGR of 7.6% growth across the forecast period.

By Technology

Shift Toward Interoperable and Adaptive Networking, Software-Defined Radio (SDR) Segment Dominates Market

Based on technology, the market is segmented into Software-Defined Radios (SDR), SATCOM, Line-of-Sight (LOS) Radio Systems, Beyond-Line-of-Sight (BLOS) Systems, tactical data links, Cellular / MANET, and encryption & cyber-hardened communication systems.

The Software-Defined Radios (SDR) segment is expected to lead the market, contributing 24.61% globally in 2026. The Software Defined Radio (SDR) segment holds the leading position in the market as militaries worldwide transition from traditional analog systems to flexible, software-upgradable platforms. SDRs allow forces to reconfigure frequencies, waveforms, and encryption protocols in real time, enabling seamless communication across joint and coalition operations. Moreover, SDRs offer enhanced cyber resilience, AI-based spectrum management, and compatibility with both Line-of-Sight (LOS) and Beyond-Line-of-Sight (BLOS) communication architectures, making them vital to future-ready defense communication systems.

- For instance, in March 2024, Thales Group launched its latest Synaps-X SDR family, supporting wideband networking and AI-driven signal optimization for multi-domain missions.

The segment of SATCOM is set to fastest growth at a CAGR of 8.4% growth across the forecast period.

By Component

High Procurement Volume and Mission-Critical Role, Transceivers & Antennas Segment Dominates Market

Based on by component, the market is segmented into transceivers & antennas, headsets, terminals, handheld radios, networking & routing equipment, encryption devices & cyber modules, power systems/batteries, and software & control interfaces.

The transceivers and antennas segment leads the market as these components serve as the fundamental building blocks of every tactical network enabling the secure transmission and reception of voice, data, and video across all platforms. Their reliability directly impacts range, clarity, and resilience against jamming, making them indispensable for mission success. The ongoing replacement of legacy analog systems with digital, multi-band, and software-defined transceivers, paired with high-gain, low-profile antennas, is fueling steady demand across land, air, and naval applications.

Others segment consist of software & control interfaces is set to grow at rate of 8.2% growth across the tactical communication market forecast period

By Frequency Band

Rising Adoption of High-Bandwidth and Multi-Domain Networks, UHF (Ultra High Frequency) Segment Dominates Market

Based on frequency band, the market is segmented into HF (High Frequency), VHF (Very High Frequency), UHF (Ultra High Frequency), and SHF/EHF (Super/Extremely High Frequency).

The UHF segment has emerged as the leading frequency band in the market, driven by its ability to support high-speed data, secure voice, and video transmission across multiple domains. Unlike VHF, which is more limited to short-range ground operations, UHF offers broader bandwidth, better encryption compatibility, and integration with satellite and airborne networks making it ideal for modern, network-centric warfare. It underpins advanced systems such as Link 16 tactical data links, software-defined radios (SDRs), and beyond-line-of-sight (BLOS) communication frameworks, all essential for real-time situational awareness and joint-force interoperability.

- For instance, in May 2024, L3Harris Technologies ramped up production of its AN/PRC-158 multi-channel UHF/VHF SDRs, central to the U.S. Army’s Integrated Tactical Network for secure broadband communication.

The segment of SHF/EHF (Super/Extremely High Frequency) is set to fastest growth at a CAGR of 8.3% growth across the forecast period.

By Application

Increasing Demand for Secure Communication, Integrated Decision-Making and Network-Centric Warfare, Command and Control (C2) Segment Dominates Market

Based on application, the market is segmented into Command and Control (C2) (HQ/TOC/CP C2, Tactical Battle Management Services (TBMS), Mobile/Edge C2 Nodes, and Coalition/Interoperability Gateways), Situational Awareness & ISR Sharing (Sensor Backhaul & Payload Transport, COP & Track Management, and Edge Dissemination & Analytics), Combat Net Radio Networks, Logistics and Support Communications, and Emergency/Humanitarian Operations.

The Command and Control (C2) segment dominates the market as modern defense forces prioritize real-time coordination, rapid decision-making, and joint-force interoperability. C2 systems act as the digital backbone of battlefield management linking troops, vehicles, aircraft, and naval units into a unified, responsive network. The growing adoption of AI-driven command platforms, cloud-enabled tactical networks, and secure data fusion systems is strengthening this segment’s dominance.

Tactical communication systems are also playing a vital role in public safety and disaster response, ensuring reliable coordination among military, police, and emergency agencies during crises.

The segment of situational awareness & ISR sharing is set to fastest growth at a CAGR of 8.1% growth across the forecast period.

By End User

Large-Scale Modernization and High Operational Deployment, Ground Forces Segment Dominates Market

Based on end user, the market is segmented into ground forces, airborne units, maritime forces, joint & special operations commands, and homeland security & paramilitary agencies.

The ground forces segment holds the dominant share of the market, driven by the vast number of deployed personnel and vehicles requiring secure, real-time connectivity. These systems serve as the lifeline for infantry units, armored formations, and field command posts, enabling coordination, mission updates, and threat response in complex terrains. The surge in soldier modernization programs, mobile command network integration, and software-defined radio (SDR) adoption has accelerated demand across armies worldwide.

The segment of airborne units sharing is set to fastest growth at a CAGR of 8.0% growth across the forecast period.

Tactical Communication Market Regional Outlook

Massive Defense Modernization and Advanced C2 Programs, North America Dominates Market

By region, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World.

North America Tactical Communication Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

North America accounted for USD 11.09 Billion in 2025, representing 42.35% of the global market share, and is projected to reach USD 11.75 Billion in 2026. led primarily by the U.S., which alone contributes over 92.98% share in 2024 of the regional share. The U.S. Department of Defense continues to invest heavily in network-centric warfare, AI-driven command systems, and software-defined radio (SDR) deployments under initiatives such as the Integrated Tactical Network (ITN) and Joint All-Domain Command and Control (JADC2) programs for public safety and disaster management, strengthening inter-agency coordination during large-scale emergencies. The U.S. market is estimated to reach USD 10.91 billion by 2026.

Europe

The Europe market was valued at USD 5.39 Billion in 2025, capturing 20.59% of global revenue, and is estimated to reach USD 5.81 Billion in 2026. during the forecast period. Growth is supported by increasing defense modernization initiatives and investments in advanced communication technologies. Within the region, The UK market is estimated to reach USD 1.26 billion by 2026, and the Germany market is estimated to reach USD 1.35 billion by 2026.

Asia Pacific

In 2025, Asia Pacific held 19.41% of the global market, reaching a valuation of USD 5.09 Billion, and is projected to grow to USD 5.5 Billion in 2026. The Asia Pacific tactical communication market is expected to witness significant growth, driven by increasing investments in indigenous software-defined radio (SDR) production, satellite-based tactical communication systems, and soldier modernization programs across countries such as China, India, Australia, and Japan. These initiatives are aimed at enhancing operational efficiency and strengthening strategic autonomy. The Japan market is estimated to reach USD 0.76 billion by 2026, the China market is estimated to reach USD 2.18 billion by 2026, and the India market is estimated to reach USD 0.96 billion by 2026.

Middle East & Africa

Middle East & Africa contributed approximately USD 2.72 Billion to the global market in 2025, accounting for 10.40% share, and is expected to reach USD 2.92 Billion in 2026. and is expected to witness strong growth during the forecast period. The modernization of command and control (C2) networks, expanding border security programs, and sustained defense spending in countries such as Israel, Saudi Arabia, and the UAE are driving the adoption of advanced tactical communication systems. The region is projected to register the highest CAGR of 7.2% over the forecast period.

Rest of the World

The Rest of the World market, comprising regions outside the major established markets, accounted for approximately 7.22% of the global tactical communication market in 2024. Growth is supported by increasing investments in defense modernization, communication infrastructure development, and security enhancement programs, which are expected to drive steady demand for tactical communication solutions during the forecast period. The Latin America region captured 7.24% of the global market in 2025, generating USD 1.9 Billion in revenue, and is projected to reach USD 2.03 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Defense Giants and Regional Innovators Shape Competitive Landscape of Tactical Communications

The market is characterized by a balanced mix of established defense giants and emerging technology innovators competing to deliver secure, interoperable, and data-centric communication networks. Major players such as L3Harris Technologies (U.S.), Thales Group (France), BAE Systems (U.K.), Collins Aerospace (U.S.), Elbit Systems (Israel), and Rohde & Schwarz (Germany) hold dominant positions, driven by strong portfolios in software-defined radios (SDR), tactical data links, and AI-enabled communication suites. These companies are actively engaged in defense modernization programs, often partnering with national armed forces to integrate advanced systems for land, air, and naval platforms. Their competitive advantage lies in multi-domain interoperability, cyber resilience, and scalable architectures that align with evolving network-centric warfare strategies.

Emerging players and regional manufacturers particularly from India, South Korea, and the Middle East are gaining traction through indigenous SDR development, modular tactical nodes, and satellite-based backhaul integration. Strategic collaborations and government-backed R&D initiatives are accelerating innovation across the ecosystem, with growing emphasis on AI-driven routing, mesh networking, and low-latency battlefield connectivity. The competitive environment is increasingly shaped by long-term contracts, technology transfers, and joint ventures that strengthen national defense capabilities while ensuring interoperability with allied forces.

LIST OF KEY TACTICAL COMMUNICATION COMPANIES PROFILED

- L3Harris Technologies (U.S.)

- Thales Group (France)

- BAE Systems (U.K.)

- Collins Aerospace (U.S.)

- Elbit Systems Ltd. (Israel)

- Rohde & Schwarz GmbH (Germany)

- General Dynamics Mission Systems (U.S.)

- Leonardo S.p.A. (Italy)

- ASELSAN A.S. (Turkey)

- Indra Sistemas S.A. (Spain)

- Hensoldt AG (Germany)

- Ultra Electronics (U.K.)

- Barrett Communications (Australia)

- Codan Communications (Australia)

- Harris Communications India Pvt. Ltd. (India)

- Safran Electronics & Defense (France)

- Bharat Electronics Limited (India)

- Hanwha Systems (South Korea)

- ST Engineering (Singapore)

- Lockheed Martin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Elbit Systems (Israel) announced new export contracts for its E-LynX SDR platform, supporting digital battlefield transformation projects in multiple NATO member countries.

- February 2024: Collins Aerospace (U.S.) introduced its ARC-210 Gen6 airborne communication system, providing enhanced UHF/VHF connectivity and secure IP-based voice and data capabilities for multi-domain operations.

- January 2024: Rohde & Schwarz (Germany) expanded its tactical radio production facility to meet European defense modernization demand, focusing on anti-jamming transceivers and adaptive high-bandwidth antennas.

- December 2023: ASELSAN (Turkey) partnered with the Turkish Armed Forces to deploy its 9661 V/UHF SDR systems across land and airborne platforms, reinforcing national defense communication capabilities.

- November 2023: Bharat Electronics Limited (India) achieved a milestone by initiating mass production of Secure Manpack SDRs for the Indian Army under its Tactical Communication System (TCS) program.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.10% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform · Land Based Systems · Airborne Systems · Naval Systems · Space-Based Systems |

|

By Installation Type · Man-portable · Vehicle-mounted · Aircraft-integrated · Shipborne / Submarine Systems · Fixed Command Post / Shelter-based Systems |

|

|

By Communication Type · Voice Communication Systems · Data Communication Systems · Video Communication Systems |

|

|

By Technology · Software-Defined Radios (SDR) · SATCOM · Line-of-Sight (LOS) Radio Systems · Beyond-Line-of-Sight (BLOS) Systems · Tactical Data Links · Cellular/MANET · Encryption & Cyber-Hardened Communication Systems |

|

|

By Component · Transceivers & Antennas · Headsets, Terminals, and Handheld Radios · Networking & Routing Equipment · Encryption Devices & Cyber Modules · Power Systems/Batteries · Software & Control Interfaces |

|

|

By Frequency Band · HF (High Frequency) · VHF (Very High Frequency) · UHF (Ultra High Frequency) · SHF/EHF (Super/Extremely High Frequency) |

|

|

By Application · Command and Control (C2) o HQ/TOC/CP C2 o Tactical Battle Management Services (TBMS) o Mobile/Edge C2 Nodes o Coalition/Interoperability Gateways · Situational Awareness & ISR Sharing o Sensor Backhaul & Payload Transport o COP & Track Management o Edge Dissemination & Analytics · Combat Net Radio Networks · Logistics and Support Communications · Emergency / Humanitarian Operations |

|

|

By End User · Ground Forces · Airborne Units · Maritime Forces · Joint & Special Operations Commands · Homeland Security & Paramilitary Agencies |

|

|

By Region · North America (By Platform, By Installation Type, By Communication Type, By Technology, By Component, By Frequency Band, By Application (By Command and Control (C2) and By Situational Awareness & ISR Sharing), By End User, and By Country) o U.S. (By Platform) o Canada (By Platform) · Europe (By Platform, By Installation Type, By Communication Type, By Technology, By Component, By Frequency Band, By Application (By Command and Control (C2) and By Situational Awareness & ISR Sharing), By End User, and By Country) o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Italy (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific (By Platform, By Installation Type, By Communication Type, By Technology, By Component, By Frequency Band, By Application (By Command and Control (C2) and By Situational Awareness & ISR Sharing), By End User, and By Country) o China (By Platform) o India (By Platform) o Japan (By Platform) o Australia (By Platform) o South Korea (By Platform) o Rest of Asia Pacific (By Platform) · Middle East (By Platform, By Installation Type, By Communication Type, By Technology, By Component, By Frequency Band, By Application (By Command and Control (C2) and By Situational Awareness & ISR Sharing), By End User, and By Country) o Saudi Arabia (By Platform) o UAE (By Platform) o Israel (By Platform) o Qatar (By Platform) o Turkey (By Platform) o Rest of the Middle East (By Platform) · Rest of the World (By Platform, By Installation Type, By Communication Type, By Technology, By Component, By Frequency Band, By Application (By Command and Control (C2) and By Situational Awareness & ISR Sharing), By End User, and By Country) o Africa (By Platform) o Latin America (By Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 28 billion in 2026 and is projected to reach USD 48.50 billion by 2034.

In 2025, the market value stood at USD 11.09 billion.

The market is expected to exhibit a CAGR of 7.10% during the forecast period.

The land based systems segment led the market by platform.

Rising demand for real-time situational awareness is driving market growth.

L3Harris Technologies (U.S.), Thales Group (France), BAE Systems (U.K.), Collins Aerospace (U.S.), Elbit Systems Ltd. (Israel), Rohde & Schwarz GmbH (Germany), General Dynamics Mission Systems (U.S.), Leonardo S.p.A. (Italy), ASELSAN A.S. (Turkey), and Indra Sistemas S.A. (Spain), among others are the top companies in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us