Geospatial Solutions Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Technology (GIS/Geospatial Analytics, Remote Sensing, GPS, and 3D Scanning), By Application (Surveying & Mapping, Planning & Analysis, Geovisualization, Land Management, and Others), and End-Use (Infrastructure Development, Defense & Intelligence, Transportation, Utility, Natural Resources, Business, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

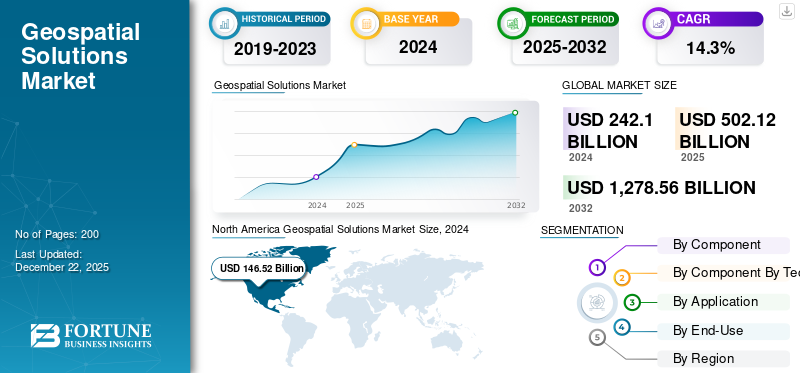

The global geospatial solutions market size was valued at USD 502.12 billion in 2025 and is projected to grow from USD 575.43 billion in 2026 to USD 1,561.61 billion by 2034, exhibiting a CAGR of 13.29% during the forecast period. North America dominated the geospatial solutions market with a market share of 166.65% in 2025.

The global geospatial solutions market has emerged as a critical enabler of digital transformation, integrating technologies such as geographic information systems (GIS), remote sensing, LiDAR, GPS, and 3D visualization into unified platforms for mapping, analysis, and decision-making. The market is projected to grow at a healthy pace, driven by rapid urbanization, infrastructure development, defense modernization, and the increasing adoption of location intelligence across industries. Governments and private enterprises are leveraging geospatial solutions to support smart city initiatives, optimize supply chains, monitor natural resources, and enable climate resilience. At the same time, the rise of autonomous mobility, digital twins, and precision agriculture is accelerating demand for high-resolution, real-time spatial data.

The push for smart cities has created strong demand for 3D mapping, geovisualization, and infrastructure management platforms. The defense and intelligence sector continues to invest heavily in geospatial intelligence (GEOINT) for surveillance, reconnaissance, and border security. The integration of artificial intelligence (AI) and machine learning (ML) into geospatial analytics is transforming how massive datasets are processed, enabling faster insights, automated feature detection, and predictive modeling.

Additionally, the convergence of geospatial data with Internet of Things (IoT) and cloud computing is enabling real-time asset monitoring and scalable solutions, while the open data movement is broadening access for startups and research institutions.

Major players in the geospatial market include global technology and defense leaders such as Esri, Trimble, Hexagon AB, Maxar Technologies, and Google, who drive innovation through advanced GIS software, satellite imagery, and mapping solutions. These companies are shaping applications in defense, urban planning, disaster management, and location-based services.

Download Free sample to learn more about this report.

Geospatial Solutions Market Key Takeaways

- 2025 Market Size: USD 502.12 billion

- 2026 Market Size: USD 575.43 billion

- 2034 Forecast Market Size: USD 1,561.61 billion

- CAGR: 13.29% from 2026–2034

- North America dominated the market in 2025 with a 33.19% share; CAGR of 13.29%.

- Software segment is projected to hold 40.79% market share in 2026.

- GIS/Geospatial Analytics segment is projected to hold 42.25% market share in 2026.

North America

North America was valued at USD 166.65 Billion in 2025 and is projected to reach USD 189.55 Billion in 2026.

Europe

Europe was valued at USD 123.37 Billion in 2025 and is projected to reach USD 141.50 Billion in 2026.

Asia Pacific

Asia Pacific was valued at USD 146.77 Billion in 2025 and is projected to reach USD 170.21 Billion in 2026.

U.S.

The U.S. was valued at USD 141.59 Billion in 2025 and is projected to reach USD 161.23 Billion in 2026.

Japan

Japan is projected to reach USD 35.32 Billion in 2026.

Read More

RUSSIA-UKRAINE WAR ANALYSIS

Russia-Ukraine War Fuels Demand for Geospatial Intelligence but Disrupts Supply Chains and Data Security

The Russia-Ukraine war has had a profound impact on the global geospatial solutions market growth, reshaping both demand patterns and technological applications. On one hand, the conflict has significantly increased the reliance on geospatial intelligence (GEOINT) for real-time situational awareness, defense planning, and humanitarian response. Governments and defense agencies are using satellite imagery, drone-based reconnaissance, and GIS platforms to track troop movements, assess infrastructure damage, and monitor refugee flows. This surge in demand has accelerated investments in commercial satellite constellations, synthetic aperture radar (SAR) imaging, and secure geospatial data platforms. On the other hand, the war has disrupted global supply chains for geospatial hardware, including GNSS receivers, sensors, and semiconductor components, given the dependence on raw materials and manufacturing routes through Eastern Europe.

Additionally, heightened concerns about cybersecurity and data sovereignty have emerged, as geospatial systems are increasingly vulnerable to hacking, GPS jamming, and misinformation campaigns. Commercial geospatial companies are also facing export restrictions, regulatory hurdles, and a more fragmented market as nations prioritize local control over geospatial data. Overall, while the conflict has fueled short-term growth in defense and security-related geospatial solutions, it has also introduced long-term uncertainties related to supply chain stability, data access, and international collaboration.

GEOSPATIAL SOLUTIONS MARKET TRENDS

Integration of Artificial Intelligence (AI) and Machine Learning (ML) Techniques to Present Significant Trends in the Market

Technological advancements and innovations are pivotal trends increasingly shaping the market. Leading players are concentrating on developing advanced solutions by incorporating Artificial Intelligence (AI) and Machine Learning (ML) to enhance geospatial data analysis through automated image analysis, object detection, and change detection. AI and ML algorithms are capable of processing extensive datasets with greater efficiency. They can derive meaningful insights and automate repetitive tasks involved in geospatial data analysis.

By examining image variability, this distinctive technology assists GIS and data science teams in pinpointing areas where additional training data should be incorporated to enhance model performance. Additionally, several other trends are driving market growth, such as multi-sensor integration, cloud computing, big data analytics, the integration of geospatial data with the Internet of Things (IoT), and strategic partnerships and collaborations.

MARKET OPPORTUNITIES

Smart Cities Development and Adoption of Precision Farming Techniques to Present Several Opportunities for Market Growth

The geospatial solutions market is poised for significant opportunities, driven by expanding applications across industries and advancements in technology. Smart city development remains one of the most lucrative opportunities, as governments worldwide invest in digital twins, intelligent infrastructure, and urban planning platforms that rely heavily on geospatial analytics. In the transportation sector, the rise of autonomous vehicles and mobility-as-a-service (MaaS) is fueling demand for high-definition mapping, real-time navigation, and LiDAR-based road modeling. In agriculture, precision farming supported by satellite imagery and drone-based surveys is helping optimize crop yields, conserve resources, and mitigate climate risks.

The integration of AI, ML, and big data analytics is further opening doors for predictive modeling, automated feature extraction, and large-scale environmental monitoring. Another strong growth area lies in the energy and utilities sector, where geospatial solutions are being applied for grid monitoring, renewable energy siting, and pipeline management. Meanwhile, the defense and intelligence community continues to invest heavily in geospatial intelligence for national security, disaster response, and border monitoring. Emerging markets in Asia Pacific, the Middle East, and Africa are presenting untapped opportunities, supported by rapid urbanization and infrastructure projects. As geospatial solutions shift from niche applications to mainstream decision-support ecosystems, companies that invest in innovation, partnerships, and scalable cloud-based platforms are well-positioned to gain a competitive advantage in this evolving landscape.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for 3D Mapping Technologies to Drive Market Expansion

The rapid pace of urbanization and ongoing infrastructure development initiatives worldwide are driving the need for precise geospatial data to support effective planning, land management, and infrastructure oversight. 3D mapping technologies allow users to visualize environments in three dimensions, facilitating the identification of landmarks, navigation through intricate road systems, and comprehension of the spatial interrelations among various elements. Geospatial solutions are essential for mapping urban regions, evaluating land use patterns, and aiding infrastructure projects such as transportation systems, smart city projects, and utility planning, thereby fostering market growth.

MARKET RESTRAINTS

Increasing Demand for Autonomous Vehicles to Evaluate Road Networks Drives Market Expansion

Autonomous vehicles depend heavily on precise geospatial data for effective mapping, navigation, and situational awareness. They necessitate real-time geospatial information to comprehend dynamic environments, including current traffic conditions and construction areas. In contrast to conventional maps, which do not provide daily updates regarding construction zones and driving regulations, maps that utilize specific geospatial data can deliver real-time insights. This encompasses information about parking ramp utilization, thereby improving the user experience. Furthermore, spatial data assists autonomous vehicles in evaluating road networks, parking facilities, and charging stations.

MARKET CHALLENGES

Data Security, High Costs, and Interoperability Issues Pose Key Challenges to Market Progress

The geospatial solutions market, despite its rapid growth, faces several challenges that could hinder widespread adoption. Data security and privacy remain key concerns, as geospatial datasets often contain sensitive information about military facilities, infrastructure, and individual behaviors, making them prime targets for cyberattacks. The high cost of hardware acquisition, including LiDAR systems, drones, and precision sensors, creates financial barriers for small and mid-sized enterprises. Another major challenge is the fragmentation of geospatial data standards, which complicates data sharing and interoperability between different platforms and stakeholders. In many regions, regulatory restrictions on aerial surveys and satellite imaging limit operations in many regions, particularly within defense-sensitive zones.

The industry grapples with the challenge of massive data storage and processing needs, as higher-resolution imagery and 3D mapping generate terabytes of data daily, straining cloud and on-premises infrastructure. Workforce shortages further exacerbate the situation, with a limited pool of professionals skilled in GIS, AI, and advanced geospatial analytics. Moreover, while AI and machine learning are transforming geospatial analytics, concerns about algorithmic accuracy, bias, and reliability continue to slow down enterprise-scale adoption. Collectively, these challenges highlight the need for stronger policies, technological innovations, and collaborative frameworks to ensure sustainable expansion of the market.

SEGMENTATION ANALYSIS

By Component

Software Segment Dominated, Driven by Growing Adoption of Digital Twin Technologies

By component, the segment is categorized into hardware, software, and services.

Software is expected to account for 40.79% of the total market share in 2026 and is anticipated to maintain its dominance in 2025 with a 40.80% share. Demand for software is rising rapidly, driven by the increasing adoption of GIS platforms, spatial analytics, and digital twin technologies. Organizations across infrastructure, utilities, defense, and transportation sectors are increasingly using software for real-time mapping, predictive modeling, and decision-making. The integration of cloud-based and AI-integrated solutions is further enhancing scalability and efficiency.

By Technology

GIS/Geospatial Analytics Demand Strengthened by AI, Big Data, and Cloud Platforms

By technology, the segment is categorized into GIS/Geospatial analytics, remote sensing, GPS, and 3D scanning.

GIS/Geospatial Analytics is projected to represent 42.25% of the market share in 2026 and is anticipated to maintain its dominance in 2025 with a 42.43% share. The GIS/geospatial analytics segment is driven by the rising adoption of advanced spatial data analysis across industries such as urban planning, logistics, defense, and environmental monitoring. The integration of AI and big data analytics enhances predictive modeling, while cloud-based platforms support real-time decision-making, establishing GIS/geospatial analytics as the backbone of modern geospatial adoption.

The 3D scanning segment is expected to grow at a CAGR of 15.2% over the forecast period.

By Application

Surveying & Mapping Demand Fueled by Infrastructure Expansion

By application, the market is divided into surveying & mapping, planning & analysis, geovisualization, land management, and others.

Surveying & Mapping is anticipated to hold a 32.40% market share in 2026. In 2025, the segment is anticipated to dominate the market with a 32.57% share. Surveying and mapping demand is strong, fueled by infrastructure expansion, smart city projects, and resource management. Governments and enterprises rely on high-resolution mapping from drones, LiDAR, and satellites for accurate planning and asset monitoring. The segment remains a foundation of geospatial solutions, driving precision in construction and land management.

The geovisualization segment is expected to grow at a CAGR of 15.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-Use

Infrastructure Development & Mapping Demand Rising with Smart Cities Initiatives and Urbanization

By end-use, the market is segmented into infrastructure development, defense & intelligence, transportation, utility, natural resources, business, and others.

Infrastructure Development is forecast to account for 27.64% of the total market share in 2026.. In 2025, the segment is anticipated to dominate with a 27.59% share. Infrastructure development and mapping solutions are rapidly expanding as countries invest in highways, railways, airports, and utilities. Geospatial tools enable 3D modeling, route optimization, and digital twins for project execution and monitoring. Driven by rapid urbanization and smart infrastructure initiatives, the segment remains one of the fastest-growing application areas for geospatial solutions.

The transportation segment is expected to grow at a CAGR of 15.7% over the forecast period.

GEOSPATIAL SOLUTIONS MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America Geospatial Solutions Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market generated USD 166.65 billion in 2025, representing 33.19% of the global market landscape, and is expected to reach USD 189.55 billion in 2026. The U.S. Department of Defense, NASA, and NOAA use geospatial platforms for surveillance, climate monitoring, and national security, fueling steady demand. Urban digital twins, traffic management, and smart infrastructure are further initiatives expanding adoption at the city-level. Private sector growth is strong as well, with logistics, real estate, and insurance firms integrating location intelligence to enhance operational efficiency. The U.S. market is projected to reach USD 161.23 billion by 2026.

The U.S. dominates the North American geospatial market due to its strong government investments in defense, intelligence, and infrastructure modernization, along with the presence of leading technology firms and satellite operators. In 2025, the U.S. market is estimated to reach USD 141.59 billion, making it the largest single-country market for geospatial solutions, accounting for nearly half of global demand. Defense and intelligence agencies continue to rely heavily on GEOINT, satellite imagery, and advanced GIS for surveillance, threat detection, and mission planning. At the state and city level, demand is growing for digital twins and smart city platforms to manage infrastructure, mobility, and disaster resilience.

Europe

Europe is projected to record a growth rate of 14.4% during the forecast period, making it the second-highest amongst all the regions, reaching a valuation of USD 123.37 billion in 2025. Demand is concentrated in infrastructure, environment, and defense. The EU Copernicus program has expanded access to satellite data, driving adoption in agriculture, forestry, and climate resilience. Western European nations such as the U.K., Germany, and France are leading adopters. Germany stands out in automotive geospatial applications for autonomous driving, the U.K. is advancing digital mapping and smart city planning, and France emphasizes aerospace and defense use cases. The UK market is projected to reach USD 36.27 billion by 2026, while the Germany market is projected to reach USD 32.08 billion by 2026. Europe contributed 24.57% to the global market in 2025, with a valuation of USD 123.37 billion, and is projected to reach USD 141.5 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 146.77 billion in 2025, representing 29.23% of the global market share, and is projected to reach USD 170.21 billion in 2026, securing the position of the third-largest regional market. China’s demand is fueled by the BeiDou navigation system, surveillance infrastructure, and massive smart city projects. Japan is deploying geospatial solutions in autonomous vehicles, disaster response, and 3D city modeling. India is the fastest-growing market in the region, with smart city initiatives, infrastructure expansion, and precision agriculture driving adoption of GIS, LiDAR, and drone-based mapping. Infrastructure development across highways, railways, and airports remains the biggest driver, requiring accurate mapping and monitoring. The Japan market is projected to reach USD 35.32 billion by 2026, the China market is projected to reach USD 68.48 billion by 2026, and the India market is projected to reach USD 46.01 billion by 2026.

Rest of World Final

The Rest of the World, including the Middle East, Africa, and Latin America, represents a high-potential growth frontier for geospatial solutions. In the Middle East, demand is led by megaprojects such as NEOM (Saudi Arabia) and Dubai Smart City, which rely on GIS, 3D mapping, and digital twin platforms. Oil and gas companies use geospatial tools for exploration and pipeline monitoring. In Africa, product adoption is growing in agriculture, urban planning, and disaster management, with governments and NGOs using GIS to address food security, deforestation, and public health. In Latin America, the market is set to record USD 24.28 billion in 2025, while the Middle East & Africa region is set to attain USD 41.05 billion in the same year. In 2025, the Rest of the World market stood at USD 65.33 billion, representing 13.01% of global demand, and is projected to grow to USD 74.17 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Drone Imaging, Emerging Markets, and Technological Advancements, along with Innovations, are Central areas of Focus for Leading Industry Players

The global geospatial solutions market is relatively fragmented, with key players, Pix4D (Switzerland), Microsoft Corporation (U.S.), Uber Technologies Inc. (U.S.), L3Harris Geospatial Solutions Inc. (U.S.), TomTom International BV (Netherlands), Living Map (U.K.), Google LLC (U.S.), and Others. Major players focus on drone imaging, emerging markets, and technological advancements to increase their market share. For instance, in May 2022, RailTel Corporation of India Ltd, in partnership with Esri India, a supplier of GIS software and solutions, signed a memorandum of understanding (MoU) to provide cloud-based GIS solutions for users in the government sector. This collaboration would include software, cloud infrastructure, and related services, facilitating the shift of government organizations from on-premises infrastructure to cloud and GIS solutions.

LIST OF KEY GEOSPATIAL SOLUTIONS MARKET PLAYERS

- Pix4D (Switzerland)

- Microsoft Corporation (U.S.)

- Uber Technologies Inc. (U.S.)

- ·L3Harris Geospatial Solutions Inc. (U.S.)

- TomTom International BV (Netherlands)

- Living Map (U.K.)

- Google LLC (U.S.)

- Mappedin Inc. (Canada)

- Bentley Systems Inc. (U.S.)

- ·SAP SE (Germany)

KEY INDUSTRY DEVELOPMENTS

- June 2024 - The Air Force granted 14 companies roles on a six-year, USD 220 million contract for comprehensive geospatial support services. Air Force officials aimed to establish a group of contractors to assist in promoting improved and collaborative situational awareness within the service branch and throughout the military. Additionally, agencies beyond the Defense Department are permitted to place orders under the Geospatial Support and Services 2.0 contract, as stated by the Pentagon in its awards digest.

- April 2023 - NV5 Global, Inc., a company based in the U.S. that offers technology, conformity assessment, and consulting solutions, acquired the commercial geospatial technology and software division of L3Harris Technologies, Inc., referred to as Visual Information Solutions (VIS). This strategic acquisition strengthens NV5's dedication to broadening its geospatial product and service portfolio via a subscription-based model. Additionally, it improves NV5's capacity to deliver geospatial information management and analytics, thereby reinforcing its support for the defense and intelligence sectors.

- March 2023 - NV5 Global Inc. declared that its subsidiary, Axim Geospatial, LLC, obtained national security geospatial contracts totaling USD 9 million from intelligence agencies and the Department of Defense. The contracts awarded include the creation and integration of dependable geospatial intelligence (GEOINT) sourced from both traditional and non-traditional means.

- February 2023 - The Environmental Systems Research Institute, Inc. (ESRI) launched the ArcGIS Reality software, an advanced solution designed for high-precision 3D mapping and the creation of digital twins. This platform effectively combines geographic information systems (GIS) with reality mapping data to produce precise and detailed digital representations of diverse environments. Such capabilities empower the construction sector, urban planners, and even entire nations to effectively capture and visualize their physical landscapes utilizing imagery data.

- September 2021 - Woolpert Inc., a leading architecture, engineering, geospatial (AEG), and strategic consulting firm based in the U.S., acquired AAM Pty Limited for an undisclosed sum. This acquisition enables Woolpert to enhance its geographical footprint and capabilities in mapping activities within the Asia-Pacific region. AAM Pty Limited is an Australia-based company that provides geospatial services, specializing in aerial mapping, surveying, GIS, and the creation of innovative geospatial processes and technologies.

REPORT COVERAGE

The geospatial solutions market report delivers a comprehensive analysis of the market. It encompasses all significant elements, including research and development capabilities and the optimization of operational services. Furthermore, the report provides insights into the global market share of geospatial solutions, prevailing trends, regional assessments, an analysis based on Porter’s Five Forces, and a competitive overview of various companies featured, highlighting the market competition and key industry advancements. In addition to the aforementioned aspects, it primarily emphasizes several factors that have played a role in the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

|

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Technology

|

|

|

By Application

|

|

|

By End-Use

|

|

|

By Geography · North America (By Component, Technology, Application, End-Use, and Country) o U.S. (By Component) o Canada (By Component) · Europe (By Component, Technology, Application, End-Use, and Country) o U.K. (By Component) o Germany (By Component) o France (By Component) o Russia (By Component) o Rest of Europe (By Component) · Asia-Pacific (By Component, Technology, Application, End-Use, and Country) o China (By Component) o Japan (By Component) o India (By Component) o Rest of Asia-Pacific (By Component) · Rest of the World (By Component, Technology, Application, End-Use, and Country) o Middle East & Africa (By Component) o Latin America (By Component) |

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 502.12 billion in 2025.

The market is likely to grow at a CAGR of1 3.29% over the forecast period (2026-2034).

The market size in North America stood at USD 166.65 billion in 2025.

Some of the top players in the market are Pix4D (Switzerland), Microsoft Corporation (U.S.), Uber Technologies Inc. (U.S.), L3Harris Geospatial Solutions Inc. (U.S.), TomTom International BV (Netherlands), and Living Map (U.K.).

U.S. dominates the market in geospatial solutions.

By application, the surveying & mapping segment dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us