Military Exoskeleton Market Size, Share, & Industry Analysis, By Component, (Actuators, Sensors, Power Sources, Control Systems, Frames/Chassis, Software, and Others), By Type (Powered (Active) Exoskeletons and Passive Exoskeletons), By Platform (Lower-Body Exoskeletons, Upper-Body Exoskeletons, and Full-Body Exoskeletons), By Application (Soldier Augmentation (Combat), Logistics & Transport, Medical Evacuation & Rescue, Maintenance & Repair, and Training & Simulation), By End-User (Army, Navy, Air Force, and Special Operations Forces), and Regional Forecast 2026-2034

Military Exoskeleton Market Size and Future Outlook

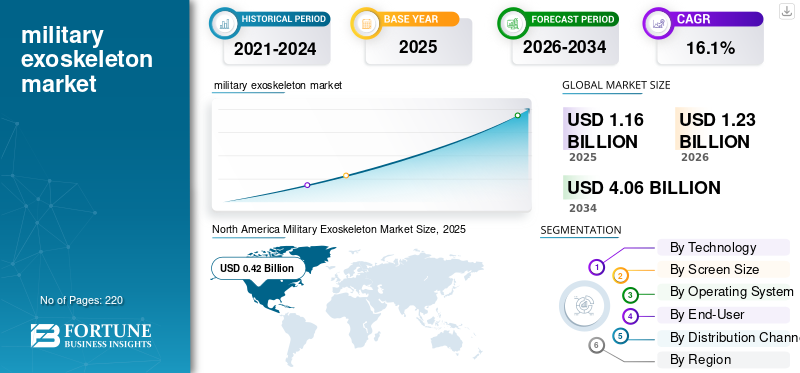

The global military exoskeleton market size was valued at USD 1.16 billion in 2025. The market is projected to grow from USD 1.23 billion in 2026 to USD 4.06 billion by 2034, exhibiting a CAGR of 16.1% during the forecast period. North America dominated the global military exoskeleton market with a market share of 36.20% in 2025.

Military exoskeletons are wearable robotic systems designed to augment the physical abilities of soldiers, such as strength, endurance, and mobility, in combat and logistics. These electromechanical devices integrate actuators, sensors, motors, hydraulics, and advanced materials to provide supplementary power to soldiers for lifting heavy loads, typically over 100 pounds, and maneuver efficiently over difficult terrain. The market includes active (powered) and passive (unpowered) systems for load carriage, spinal cord injury prevention, combat performance enhancement, medical rehabilitation, and special operations support.

The significant growth momentum of the market arises as multiple drivers converge to address contemporary battlefield needs and priorities of defense across the world. Escalating geopolitical tensions, cross-border disputes, and terrorist activities force armed forces to continue making investments in human augmentation technologies that enhance soldier survivability and operational effectiveness. The changing nature of modern warfare, especially concerns related to biological and chemical weapons requiring protection equipment, drives demand for exoskeletons to keep soldiers operating effectively with the additional protection gear without direct exposure to hazardous elements.

The market is relatively concentrated, with large, established defense contractors at the leading edge of innovation and deployment. Key players include Lockheed Martin Corporation, which boasts the ONYX lower-body part system; Raytheon Technologies; BAE Systems; General Dynamics; and Northrop Grumman. It also includes specialized robotics firms such as Sarcos Technology and Robotics Corporation, Ekso Bionics, and SRI International. Competition intensifies as firms invest heavily in R&D for AI-enhanced control systems, extended battery life solutions, and modular platforms adaptable across diverse military applications from logistics to combat support.

Download Free sample to learn more about this report.

Military Exoskeleton Market Key Takeaways

- 2025 Market Size: USD 1.16 billion

- 2026 Market Size: USD 1.23 billion

- 2034 Forecast Market Size: USD 4.06 billion

- CAGR: 16.1% from 2026–2034

- North America dominated the global military exoskeleton market with a market share of 36.20% in 2025.

- The military platform is dominated by lower-body exoskeletons, commanding about 56.20% of the total market share.

- The power sources sub-segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 18.5%.

North America

North America held a market value of USD 0.41 billion in 2025, supported by strong defense spending and ongoing military exoskeleton R&D programs.

Europe

Europe is projected to be the fastest-growing regional market, expanding at a CAGR of over 17.1% through the forecast period due to rising defense modernization initiatives.

Asia Pacific

Asia Pacific is anticipated to witness significant growth at a CAGR of 15.6%, driven by military modernization programs and increasing investments in soldier augmentation technologies.

U.S.

The U.S. competitive advantage is based on institutional relationships among established defense contractors and military procurement agencies, technological maturity for powered and passive systems, and advanced artificial intelligence integration capabilities.

Japan

Growing defense modernization efforts and investments in robotics and wearable technologies are supporting the adoption of military exoskeleton solutions across defense applications.

Read More

Market Dynamics

Market Drivers

Growing Research and Development on Physiological Performance Enhancement and Spinal Cord Injury Prevention Drives Market Growth

Medical research has identified significant physiological benefits of exoskeleton deployment: scientific studies have pointed out 35-38% reductions in lower back muscle activity when doing assembly tasks and increased task duration from 3.2 to 9.7 minutes under similar comfort conditions. Field testing by the 101st Airborne Division at Vanderbilt University found that about 90% of the soldiers said they could perform tasks for much longer when using exosuits, and 100% would be mostly to adopt the suits if those systems were further developed and made available.

The Australian Defense Force reported that logistics teams, with the use of exoskeletons, demonstrated increases in task efficiency of as high as 15%, displaying practical performance gains in the non-combat domain of operations. Research by the Defense Institute of Physiology and Allied Sciences and Defense Bio-Engineering & Electromedical Laboratory, under India's Defense Research and Development Organization, confirms exoskeletons enable an increase in load-carrying capacity up to 100 kg for 8-hour operational periods, directly addressing spinal cord injury prevention priorities.

- For instance, in August 2024, the U.S. Army contracted with SUITX to provide advanced soldier augmentation technologies in recognition of exoskeletons as important tools for evaluating potential benefits in improving soldier endurance and operational effectiveness.

Market Restraints

High Development Costs, Operational Duration Constraints, and Manufacturing Complexity Hamper Market Growth

The prohibitive unit economics of military exoskeleton systems create a significant barrier to adoption, as production costs exceed practical deployment thresholds for most defense organizations, especially within developing economies. Despite technical maturity, Lockheed Martin's HULC system weighs 24 kg without batteries and shows limited operational endurance; untethered variants, for example, support only 96 hours of operational duration at maximum capacity, with eight lithium-ion batteries stored on the lower lumbar region.

While actuators, control systems, and advanced robotics integration are increasingly integrated into full-body part, hybrid, and soft exoskeleton architectures, this complexity necessitates very specialized manufacturing capabilities and supply chain coordination that existing defense contractors are still developing.

Fundamental technical limitations in battery energy density and endurance remain key factors in limiting military deployment scenarios and operational flexibility. State-of-the-art lithium-ion battery technologies limit powered exoskeleton operational duration to 3-5 hours under continuous use conditions, presenting significant logistical challenges in extended missions, remote environments, and high-altitude terrains with severely limited or entirely absent power infrastructure.

Market Opportunities

Advanced Materials Science, Lightweight Architecture, and Expansion into Specialized Military Operations Cater New Market Opportunities

Materials science breakthroughs in UHMWPE laminates, three-dimensional spacer meshes, and advanced composite architectures allow the building of much lighter exoskeleton frames with preserved structural integrity while reducing wearer cognitive load and physical fatigue from the weight of the device itself.

Next-generation manufacturing technologies such as additive manufacturing and precision 3D printing allow for customized geometries of exoskeleton designs based on individual soldier anthropometrics, thus addressing long-standing ergonomic challenges while enhancing user acceptance rates. The emerging commercial market for adaptive, smart exoskeleton platforms including real-time biometric monitoring, predictive analytics of fatigue onset, and dynamic load distribution demonstrates very strong commercial viability, from military applications to industrial occupational safety.

The market is set for significant expansion in specialized operations domains beyond traditional load-carriage missions, including search-and-rescue operations, medical evacuation support, chemical-biological protection equipment augmentation, and the integration of command-and-control systems for enhanced real-time situational awareness. In particular, intelligence and reconnaissance missions conducted in high-altitude terrains within South Asian ranges are highly compelling use cases for exoskeleton-enabled endurance that directly addresses operational constraints.

- For instance in May 2025, a passive exoskeleton development by India, through the collaboration of TATA Advanced Systems Limited and DRDO, will undergo trials for the Indian Army is targeted for operations at high altitudes owing to the complexity of terrain involved and the reduced atmospheric oxygen that requires human performance enhancement.

Military Exoskeleton MarketTrends

Artificial Intelligence, Autonomous Control System Integration, and Customization Framework Standardization Anticipate Market Trends

Artificial intelligence integration has emerged as perhaps the most revolutionary technological trend transforming military exoskeleton development trajectories; machine learning algorithms provide the autonomous system to adapt to wearer physiology without explicit programming or calibration.

Neural efficiency metrics and advanced neuromuscular control algorithms that map human kinematic states directly to optimal joint torque assistance profiles have been demonstrated in research at Northwestern University and other academic institutions, minimizing computational overhead and allowing intuitive human-machine interaction. Additionally, releases of Cyberdyne's HAL platform, in particular the HAL Lumbar variant targeting healthcare rehabilitation applications, represent commercialization of bio-electrical signal processing technologies that decode user intention from neural input and build intuitive assistance profiles.

Standardization of modular exoskeleton architectures for mission-specific customization is an emerging technological priority, supported through military procurement initiatives and collaboration among the defense industry. ASTM International Committee exoskeleton development of standardized test methods-particularly work item WK65295 for load-handling exoskeleton evaluation-allows for comparative performance evaluation across different manufacturer offerings and helps facilitate procurement decisions based on objective performance benchmarking.

- For instance, in May 2025, German Bionic's unveiling of the Exia platform introduced fully integrated augmented artificial intelligence as a founding design principle, incorporating billions of real-world motion data points into the control software architecture for improved performance optimization.

Market Challenges

Standardization Deficiency and Regulatory Framework Fragmentation Can Restrict Market Growth

The military exoskeleton industry also faces significant challenges rooted in fragmented regulatory environments and the absence of comprehensive standardization frameworks that govern the design, testing, certification, and procurement among national defense establishments. NIST's PoLoTAE development initiative and ongoing ASTM F48 standards committee work since 2017 represent efforts to establish repeatable, internationally harmonized test methodologies; significant gaps remain, however, in military-specific evaluation criteria and performance thresholds.

Field testing discrepancies highlight challenges with standardization, NATO Mountain Warfare Centre of Excellence December 2024 evaluations showed that passive exoskeleton technology degraded soldier performance in dynamic terrain navigation despite benefits witnessed in static load-carrying, which contradicts industry marketing claims and further confuses procurement decisions. Lack of consensus performance benchmarks among the NATO allied forces, U.S. military services, and emerging defense powers inhibits technology interoperability, drives up the cost of manufacturing without the benefit of economies of scale, and makes international military cooperation scenarios more complicated.

Regulatory approval processes for military deployment by the U.S. Department of Defense, European defense ministries, and Asia Pacific military establishments are very different, which means that the development pathways have become fragmented; this prolongs commercialization timelines. Clinical validation requirements, particularly in variants for rehabilitation and medical applications, add to this regulatory burden via FDA device classification frameworks that involve substantial clinical trial investment before market access authorization can be achieved.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Hydrogen Fuel Cell Technology as Emerging Power Solution Cater Significant Advancement Within Power Sources Segment Growth

The global market is segmented by component into the actuators, sensors, power sources, control systems, frames/chassis, software, and others.

The power sources sub-segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 18.5%. The growth is driven by hydrogen fuel cell power systems representing the most strategically affecting field deployment scenarios and mission sustainability. Honeywell was awarded a contract from General Technical Services in April 2024 focused on developing hydrogen fuel cell systems weighing approximately 50% of conventional lithium-ion battery equivalents while delivering comparable power output, specifically designed to reduce soldier battery load from 45 pounds associated with extended missions down to approximately 20-25 pounds due to superior energy density characteristics.

Frames and chassis components retain the lion's share of market position at about 35-40% of the value of exoskeleton components, supported by the superiority of carbon fiber composite material in the characteristics related to the optimization of the strength-to-weight ratio and structural rigidity enhancement for military operational deployment. Increasing stiffness substantially, this established the benchmark architecture that has been incorporated across the designs of subsequent generations of exoskeleton platforms, with the adoption of carbon fiber composites extending across commercial and military applications.

By Type

Advanced Artificial Intelligence Control Systems and Autonomous Adaptation Capacity Drives Segmental Growth

The global market is segmented by type into the powered (active) exoskeletons and passive exoskeletons.

The powered exoskeletons dominate the military exoskeleton market share, commanding about 63.87% total market share through superior performance capabilities, emerging artificial intelligence integration that allows the autonomous adaptation of the system without requiring calibration or user training. Indeed, integrating electromyography sensors, inertial measurement units, and neural network controllers has allowed powered exoskeletons to decode user intention from biometric signals and to autonomously optimize joint assistance profiles without explicit programming or subject-specific adjustment of parameters, thereby realizing intuitive human-machine interaction superior to passive system performance and allowing rapid soldier adoption without extensive training protocols.

Passive exoskeletons are the second-fastest-growing segment, projected to grow at growth rates of over 14.7% through the forecast period, driven by institutional recognition of cost-benefit advantages and operational simplicity enabling deployment across resource-constrained military organizations and developing defense establishments lacking advanced power infrastructure. Mechanical energy storage and spring-dampener architectures reduce weight burden relative to powered systems incorporating battery packs and actuator complexity. This therefore enables soldiers to wear passive systems without comprehensive training, further drives segmental growth.

By Platforms

Comprehensive Multi-Joint Integration and Operational Versatility Anticipate Segmental Growth

The global market is segmented by platform into the lower-body exoskeletons, upper-body exoskeletons, and full-body exoskeletons.

Full-body exoskeletons are the fastest-growing platform segment, projected to grow at more than 17.2% annually through the forecast period. The growth is driven by institutional recognition of comprehensive performance augmentation, enabling both upper and lower extremity assistance for a variety of military operational tasks ranging from logistics to munitions handling and combat support functions. The growth momentum for full-body exoskeleton markets accelerates with the convergence of advanced materials science, miniaturized power systems, and neural network control algorithms that make intuitive human-machine interfaces possible, automatically optimizing assistance profiles across different body segments without any need for user intervention or training.

The military platform is dominated by lower-body exoskeletons, commanding about 56.20% of the total market share through technological maturity, operational validation across military field environments, and institutional procurement momentum establishing baseline performance specifications for emerging technologies. In this respect, the global lower-body exoskeleton segment achieves a share of 38% within the broader industrial wearable exoskeleton ecosystem, demonstrating superior performance reliability and consistent support.

By Application

Enhanced Combat Capability and Tactical Effectiveness Integration Drives Segmental Growth

The global market is segmented by application into the soldier augmentation (combat), logistics & transport, medical evacuation & rescue, maintenance & repair, and training & simulation.

Soldier augmentation combat applications are the fastest-growing application segments, projected at growth rates exceeding 17.9% through the forecast period, driven by institutional recognition that exoskeleton technology enables comprehensive soldier performance enhancement across strength, agility, endurance, and cognitive operational requirements in contested tactical environments. Convergence of augmented reality headsets, neural control interfaces, and AI-driven autonomous assistance develops a comprehensive combat soldier ecosystem capable of real-time threat assessment, improved situational awareness, and autonomous movement assistance in high-stress tactical operations, establishing technological differentiation unavailable in prior generations of military systems.

Dominance in the logistics segment extends through specialization into high-altitude supply chain management and casualty evacuation operations, where exoskeleton technology provides critical endurance enhancement, enabling soldiers to maintain supply line operations across the elevation of austere environments where traditional human endurance was severely constrained. Logistics segment dominance perpetuates through operational mathematics that are compelling: exoskeleton-enabled individual soldiers achieve load-carrying capacity equivalent to previous-generation small-team logistics operations, enabling squad-level operational independence and extended mission radius without additional personnel or vehicle support.

To know how our report can help streamline your business, Speak to Analyst

By End User

Tactical Capability Enhancement and Elite Force Performance Augmentation Anticipate Segmental Growth

The global market is segmented by end user into the army, navy, air force, and special operations forces.

Special operations forces are the fastest-growing end-user segment, projected at growth rates of more than 17.5% through 2026-2034, driven by institutional emphasis on force multiplication, enhancement of operational flexibility, and tactical superiority to enable specialized missions beyond conventional forces. Growing focus on specialized tactical needs rapid deployment, austere environment operations, extended endurance across diverse terrains sets up discrete technology needs different from conventional army logistical applications, driving accelerated exoskeleton development to particularly address elite force operational characteristics.

The army end-user segment leads in the market, with around 61.80% total end-user share, supported by comprehensive organizational scale and massive logistics requirements, including ammunition supply, equipment transport, and casualty evacuation operations that represent some of the fundamental sustainment functions in most global military deployments. Army-wide procurement focus on load-carrying exoskeletons reflects a fundamental logistics reality wherein ammunition supply, equipment transport, and sustainment operations are consuming around 30-40% of combat support personnel capacity and form a compelling organizational imperative for exoskeleton-enabled logistics optimization.

Military Exoskeleton Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Military Exoskeleton Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America continues to lead the market, with around 35.73% of global market military exoskeleton share, and accounted for 0.41 million market value in 2025. The dominance due to heavy funding by the U.S. Department of Defense of over USD 50 million yearly for exoskeleton-related research and development. This includes a fully funded USD 6.9 million and 48 month Other Transaction Agreement granted to the U.S. Army Natick Soldier Research, Development and Engineering Center for extensive operational evaluations on varied platform architectures.

The U.S. competitive advantage is based on institutional relationships among established defense contractors and military procurement agencies, technological maturity for powered and passive systems, and advanced artificial intelligence integration capabilities that establish performance benchmarks beyond international competitive offerings.

Europe

Europe is emerging as the fastest-growing regional market, projected to grow at rates over 17.1% through the forecast period. Growth is driven by the rise in geopolitical tensions since the invasion of Ukraine by Russia and subsequent NATO Industrial Capacity Expansion Pledge commitments laying down collaborative defense procurement frameworks that plan to allocate 50% of the collective defense budgets to collaborative sourcing mechanisms by 2030. Germany leads European market development with significant government investment in R&D, focusing on the integration of AI (artificial intelligence), robotics, and advanced materials, while national capability demonstrations across automotive manufacturing and industrial logistics applications create pathways for civilian-military technology convergence. The European Defense Industry Programme framework sets aside a dedicated budget of EUR 1.5 billion for enhancing the readiness of the defense industry, thereby facilitating cross-border technology partnerships between defense OEMs and robotics specialists accelerating market growth.

Asia Pacific

Asia Pacific shows the second-fastest growth rate with a 15.6% CAGR, growth in the region is consolidated in military modernization programs across China, India, and Japan as a response to border security challenges and strategic military capability advancement imperatives that prioritize soldier augmentation technologies. Indian military exoskeleton development requires both DRDO-led laboratory development programs and private sector partnerships, as represented by TATA Advanced Systems Limited-DRDO passive exoskeleton technology collaboration currently undergoing Indian Army trials with a facility for 75% load transfer to ground for enhanced operations in high-altitude Siachen and Ladakh terrains, supported by indigenous passive systems such as JaipurBelt and ArmMax deployed across Indian Army, Air Force, and National Disaster Response Force operations, catalyzing the market global military exoskeleton market growth.

Rest of the World

The rest of world segment-itself divided among the Middle East & Africa and Latin America-shows a moderately rising trajectory of growth, reflecting emerging defense technology adoption initiatives, with highly selective procurement activity concentrated among the high-income and upper-middle-income nations pursuing strategic military capability advancement.

COMPETATIVE LANDSCAPE

Key Market Players

The market is moderately concentrated, with competitive dynamics characterized by a fragmented yet consolidating industry structure, where top players hold combined market shares of approximately 55% and emerging startups represent nearly 20% of the competitive landscape. Market concentration can be considered consolidated, with dominant influence concentrated among 1-5 major players; however, the competitive intensity remains high as continuous technological differentiation opportunities exist and specialized niche segments attract new entrants, fostering bifurcated competition between established defense contractors leveraging government relationships and capital resources and emerging innovation-focused firms pursuing disruptive technologies and specialized applications.

The competitive environment reflects moderate rivalry intensity, with differentiation revolving around proprietary control systems incorporating artificial intelligence, lightweight material innovations, power efficiency breakthroughs, and load-bearing capacity optimization rather than pricing-based competition, as military procurement places significant weight on performance specifications, reliability certifications, and operational effectiveness over cost minimization. Market consolidation momentum is high, as represented by strategic acquisitions such as Ekso Bionics' December 2024 acquisition of Parker Hannifin Corporation's Human Motion and Control business unit, integrating Indego product line capabilities to bolster rehabilitation market positioning and diversify revenue streams beyond military applications.

Supplier power also remains high for critical components, such as advanced actuators, precision sensors, lithium-ion battery systems, and lightweight composite materials that are sourced from specialized suppliers, imposing material cost pressures on platform developers and limiting margin expansion potential for mid-tier competitors.

List of Key Military Exoskeleton Companies Profiled:-

- Lockheed Martin Corporation (U.S.)

- Sarcos Technology and Robotics Corporation (U.S.)

- RTX Corporation (U.S.)

- Ekso Bionics Holdings, Inc. (U.S.)

- Rostec State Corporation (Russia)

- China North Industries Corporation (Norinco) (China)

- ASELSAN A.S. (Turkey)

- Bionic Power Inc (Canada)

- Mawashi Science & Technology (Canada)

- LIG Nex1 Co., Ltd. (South Korea)

- Safran S.A. (France)

- B-Temia Inc. (Canada)

- BAE Systems plc (U.K.)

- Roam Robotics, Inc. (U.S.)

- Tata Advanced Systems Ltd. (TASL) (India)

KEY INDUSTRY DEVELOPMENTS

- May 2025: The Henry M. Jackson Foundation secured a USD 9.37 million cost-plus-fixed-fee contract (HT9425-24-C-0031) to provide research support services for exoskeletons, benefiting the Telemedicine and Advanced Technology Research Center.

- October 2024: The U.S. Army's 1st Field Artillery Battalion at Fort Sill, Oklahoma, carried out a three-day "proof of concept" evaluation of commercially available exoskeleton systems, overseen by Army Capabilities Command for logistics related to artillery ammunition and equipment.

- June 2024: The Indian Army, Indian Air Force, and NDRF acquired passive exoskeleton systems from Newndra Innovations, based in Rajasthan. These included variants such as the JaipurBelt (weighing 1.8 kg) and ArmMax, which assist in load carrying from 5 to 35 kg without the need for batteries or any external power sources.

- February 2024: Aptima Inc. received a USD 249,961 Phase I Small Business Innovation Research (SBIR) contract (HT9425-24-P-0030) from the Defense Health Agency to create a quasi-passive hand exoskeleton called GRIPMASTER, designed to enhance grip strength for military casualty transport, utilizing machine learning algorithms.

- September 2023: USSOCOM granted a contract to Sarcos Robotics for a pre-production version of the Guardian XO, a full-body robotic exoskeleton that operates autonomously for up to eight hours on a single battery, with a capacity to carry loads of up to 200 lbs.

REPORT COVERAGE

The global military exoskeleton market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.1% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation

|

By Component · Actuators · Sensors · Power Sources · Control Systems · Frames/Chassis · Software · Others By Type · Powered (Active) Exoskeletons · Passive Exoskeletons By Platform · Lower-Body Exoskeletons · Upper-Body Exoskeletons · Full-Body Exoskeletons By Application · Soldier Augmentation (Combat) · Logistics & Transport · Medical Evacuation & Rescue · Maintenance & Repair · Training & Simulation By End User · Army · Navy · Air Force · Special Operations Forces |

|

By Region North America (By Component, By Type, By Platform, By Application, By End User, By Country) · U.S. (By End User) · Canada (By End User) Europe (By Component, By Type, By Platform, By Application, By End User, By Country) · U.K. (By End User) · France (By End User) · Germany (By End User) · Russia (By End User) · Rest of Europe (By End User) Asia Pacific (By Component, By Type, By Platform, By Application, By End User, By Country) · China (By End User) · Japan (By End User) · India (By End User) · South Korea (By End User) · Rest of Asia Pacific (By End User) Rest of World (By Component, By Type, By Platform, By Application, By End User, By Sub-Region) · Middle East & Africa (By End User) · Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.16 billion in 2025 and is projected to reach USD 4.06 billion by 2034.

In 2024, the market value stood at USD 0.36 billion.

The market is expected to exhibit a CAGR of 16.1% during the forecast period.

The special operations forces segment is expected to hold the highest CAGR over the forecast period.

The growing research and development on physiological performance enhancement and injury prevention are the key factors that drives the market growth.

Lockheed Martin Corporation, Raytheon Technologies, BAE Systems, General Dynamics, Northrop Grumman, Sarcos Technology, and Robotics Corporation, among others are the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us