Military Laser Systems Market Size, Share and Industry Analysis, By Type (Weapons and Non-Weapons), By Weapons (Lethal Weapon and Non-Lethal Weapon), By Non-Weapons (Laser Altimeter, Laser Designator, Laser Pointer/Illuminator, Laser Rangefinder, Laser Terminal, LiDAR System, and Ring Laser Gyroscope), By Technology (Solid-State Laser, Fiber Laser, Semiconductor Laser, Gas Laser, Liquid Laser, and Free-Electron Laser) By Output Power (Below 10 kW, 10 kW to 100 kW, and Above 100 kW), By Application , By Platform, Regional Forecast 2026-2034

Military Laser Systems Market Size and Future Outlook

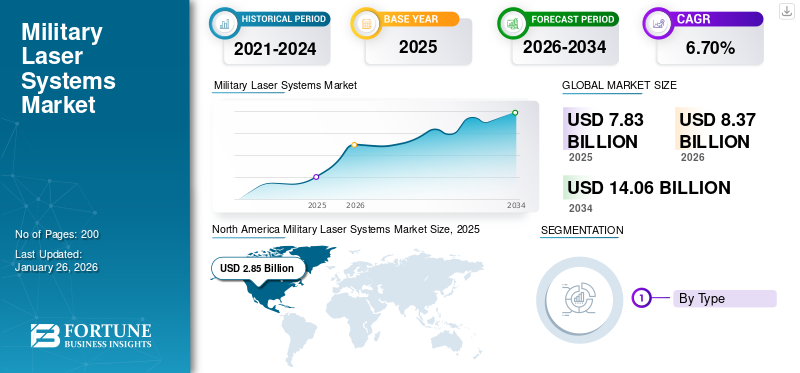

The global military laser systems market size was valued at USD 7.83 billion in 2025 and is projected to grow from USD 8.37 billion in 2026 to USD 14.06 billion by 2034, exhibiting a CAGR of 6.70% during the forecast period. North America dominated the military laser systems market with a market share of 36.38% in 2025.

Military laser systems are an evolutionary leap in defense technology, employing the focused electromagnetic energy to engage and neutralize the threat without the use of conventional kinetic projectiles. The advanced systems have become war-winning assets for contemporary warfare, providing precision targeting, being cost-effective, and operating with operational benefits that augment conventional arms on land, sea, and air platforms.

The laser systems market for the military is a paradigm shift in defense technology, providing revolutionary capability that responds to changing security threats while offering tremendous operational and economic benefits over conventional weapons systems. With geopolitical tensions ongoing and asymmetric threats spreading, laser systems are poised to become standard elements of contemporary military arsenals, radically changing the way armed forces engage and neutralize threats in all areas of operation drives the global market growth.

Military laser systems play a variety of vital roles in defense operations, showing excellent versatility in counteracting today's security threats. They are employed in directed energy weapons, precision target designation, range finding and distance measurement, counter-drone operations, naval defense applications (ship borne systems intended to defend ships against small boat attacks, anti-ship missiles, and airborne threats), communication and surveillance and other systems, platforms, and so on.

Furthermore, the market encompasses several major market players with a broad portfolio with innovative products, and strong regional presence expansion have supported the dominance of these companies in the market. Major players are BAE System (U.K.), Boeing Company (U.S.), Elbit System (Israel), Israel Aerospace Industries Ltd. (Israel), L3Harris Technologies Inc. (U.S.) and other key players in the industry.

Download Free sample to learn more about this report.

Military Laser Systems Market Key Takeaways

- 2025 Market Size: USD 7.83 billion

- 2026 Market Size: USD 8.37 billion

- 2034 Forecast Market Size: USD 14.06 billion

- CAGR: 6.70% from 2026–2034

- North America dominated the military laser systems market with a market share of 36.38% in 2025.

- The non-weapons sub-segment held the largest market share of 83.68% in 2026.

- The lethal weapon segment accounted for 80.15% of the global market share in 2024.

North America

North America recorded a market size of USD 2.85 billion in 2025, capturing 36.38% of the global market share, and is projected to reach USD 3.03 billion in 2026.

Europe

Europe accounted for USD 2.10 billion in 2025, supported by collaborative defense initiatives, increased military spending, and advanced laser system development programs.

Asia Pacific

Asia Pacific reached USD 1.86 billion in 2025 and is expected to witness strong growth driven by rising geopolitical tensions and expanding defense budgets across major economies.

U.S.

The U.S. market is projected to reach USD 2.66 billion by 2026, supported by substantial Department of Defense investments in directed energy weapons and next-generation defense capabilities.

Japan

The Japan market is projected to reach USD 0.30 billion by 2026, driven by increasing defense modernization efforts and investments in indigenous advanced military technologies.

Read More

Russia/Ukraine War Impact

Ongoing War Accelerated Defense Modernization and Directed Energy Investment

The war has triggered a strategic change among European Union and NATO member nations toward fast acquisition of cutting-edge air defense and counter-UAS systems, with military laser systems as top-priority solutions. In early 2025, the U.S. Army's European Deterrence Initiative provided an additional USD 250 million to accelerate deployment of Stryker-mounted DE M-SHORAD laser systems to Poland and the Baltic States, highlighting the pressing need for mobile directed energy assets to defend critical infrastructure and forward forces.

Germany's Bundeswehr hastened the acquisition of Rheinmetall's 50 kW ground-based laser demonstrators to support base defense tests, paid for with an emergency USD 110 million reprogramming of NATO security assistance funding. France and Italy are co-funding a rapid-response 100 kW laser weapon demonstrator through a common OCCAr program, moving from concept to firing trials in six months a historically unprecedented speeding up of European defense purchasing cycles.

Extensive employment of small kamikaze drones by Ukrainian forces has created the demand for sub-10 kW tactical laser dazzlers, prompting the U.S. Air Force to install additional 5 kW airborne laser pods on MQ-9 Reapers departing Romanian airbases by Q3 2025.

The disruption of global defense supply chains due to the war has showcased the advantage of resilience in domestically manufactured laser systems and has prompted collaborative programs to decrease single-source component dependency.

The U.K. Ministry of Defense powered up its Laser Systems Rapid Development Cell, teaming BAE Systems and QinetiQ, to speed fielding of light dazzler systems to Royal Artillery units operating in Ukraine's interior. These actions build industrial base resilience and highlight the war's significance in reasserting defense industrial policy in the direction of sovereign capability development and intra-alliance technology sharing.

MARKET DYNAMICS

Market Drivers

Growing Defense Budget for Modernization, Geopolitical Security Concerns, Technological Advancement and Operational Cost Efficiency Propel Market Growth

Military laser systems market growth is seeing significant momentum through increased defense spending among leading economies globally, with the key driver of this rising being increased geopolitical tensions and asymmetric warfare threats. Countries such as the U.S., China, and India are investing unprecedented capital toward the development of directed energy weapons with the Pentagon alone spending around USD 1 billion a year on laser weapons-related research and development programs.

The imperative to modernize results from new security threats such as proliferation of unmanned aerial vehicles, hypersonic missiles, and advanced electronic warfare capabilities that cannot be countered by conventional kinetic weapons.

- For instance, in May 2024, the U.S. Army deployed BlueHalo's 20-kilowatt LOCUST laser weapon system overseas, the first combat operational deployment of laser weapons, showing successful prototype-to-battlefield transition with AI-powered targeting software showing high accuracy and lower power consumption.

The market growth path is a result of tremendous technological advancements in solid-state laser technology, fiber laser systems, and power management solutions that improve operational reliability at decreasing system complexity.

Sophisticated beam control systems integrated with artificial intelligence capabilities provide autonomous targeting, significantly enhancing engagement accuracy and reaction times against rapidly moving airborne threats. Advances in the military laser systems in manufacturing of laser diode efficiency, thermal systems, and miniaturization technologies allow for integration on land, shipboard, and airborne platforms without sacrificing mobility or mission flexibility.

Market Restraints

Technical Limitations, Environmental Operational Constraints and High Development Cost Can Hamper Market Growth

Military laser systems face significant technical challenges that restrict mass deployment in various operating environments, specifically concerning atmospheric interference and range effectiveness issues. Atmospheric conditions such as fog, rain, dust, and smoke severely attenuate laser beam quality by scattering and absorption effects, lowering system effectiveness up to 30% in poor conditions. Power requirements for generating electricity are challenging for mobile platforms, with high-energy lasers requiring hundreds of kilowatts to megawatts of electrical power while ensuring tight thermal control within close operation parameters. The military laser systems market is confronted with enormous economic hurdles in the form of prolonged research and development costs, manufacturing complexity, and platform integration needs overburdening defense procurement budgets.

Development expenses for next-generation laser systems are over USD 200 million per model, not including integration and test costs required for operational qualification. Precision manufacturing requirements for laser parts, such as high-power laser diodes, state-of-the-art optics, and power management components, require costly materials and specialized fabrication techniques that add greatly to unit cost.

- For instance, in April 2024, the Congressional Research Service indicated that the U.S. government had cumulatively spent more than USD 10 billion since 2020 to develop laser weapons, with standalone 150-kilowatt class systems costing more than USD 200 million not including integration costs.

Market Opportunities

Growing Space-Based Defense Application, Hypersonic Threat Countermeasures and Autonomous Systems Integration Poised Significant Growth

Space-based military laser systems offer new growth opportunities for the application in missile defense, especially counteracting hypersonic threat weapons that are not effectively countered by conventional interceptor systems. Deployment into space avoids atmospheric interference issues while offering global coverage capabilities critical for strategic defense systems.

Dual-use missions across military and civilian markets, such as space debris mitigation, satellite maintenance, and asteroid defense missions, open up market growth opportunities beyond conventional defense procurement systems. International collaborations provide frameworks for cost-sharing programs for space-based lasers, lowering individual country financial constraints while increasing shared security capabilities.

Moreover, autonomous targeting integration by artificial intelligence and machine learning algorithms increases system performance with minimized operator workload demands. Modular system architectures allow quick deployment configurations suitable for expeditionary operations, urban warfare environments, and forward operating base protection missions where legacy air defense systems are impractical to employ.

- For instance, in July 2025, armed forces exhibited greater integration of AI-powered targeting platforms with fiber lasers for autonomous engagement of threats, with the British Army expanding Bagira Systems' RTES laser-based training simulators that include real-time tracking and 360-degree hit detection.

Military Laser Systems Market Trends

Growing Adoption of Artificial Intelligence Integration, Autonomous Targeting Capabilities, Miniaturization and Platform Integration Advancement Catalyze Market Growth

The current military laser systems market trends place a focus on the creation of compact, light laser systems adaptable for deployment on a variety of military platforms such as unmanned vehicles, small boats, and individual soldier gear. Development of fiber laser technology allows power scaling with an absence of proportionate size growth, supporting integration with space-challenged platforms that are not previously suitable for directed energy weapons. Modular system architectures enable mission-optimized configurations with less logistical complexity and maintenance in field environments.

- For instance, in August 2025, advances in solid-state laser markets highlighted miniaturization trends with small-scale systems reaching megawatt power levels compatible with airborne platforms, due to Industry 4.0 integration and automated manufacturing processes.

Military laser systems are increasingly using artificial intelligence and machine learning-based technologies to improve targeting precision, threat detection, and engagement decision-making processes without the intervention of human operators. Sophisticated algorithms allow for predictive targeting of rapid-moving air threats and mitigation of atmospheric distortion through adaptive optics control systems. Integration with current command and control networks provides networked engagement capabilities that enable numerous laser systems to engage simultaneously against swarm threats.

Autonomous battle management systems decrease cognitive load on operators and enhance response times necessary for hypersonic threat engagement missions. Commercial AI advancements in autonomous transport and gaming markets offer military laser system technological transfer to improve militarily at decreased development expenses. Machine learning algorithms continually enhance system performance through analysis of operating data, producing self-improving capabilities that increase effectiveness over time.

Market Challenges

Thermal Management Complexity, Power Generation, Atmospheric Effects and Range Limitations May Limit Market Growth

Military laser systems are encountered with ongoing engineering challenges involving power generation capability and thermal management needs that constrain operational deployment across the spectrum of military platforms. High-energy laser systems demand electrical input in the range of hundreds of kilowatts to megawatts and produce considerable waste heat that needs to be effectively managed to avoid damaging components and optical distortion. Mobile platform integration is challenged by the constraints of low onboard power generation capability, with current military vehicles and aircraft offering inadequate electrical output for sustained laser operation.

Thermal management systems demand advanced cooling systems such as liquid cooling circuits, phase-change materials, and heat exchangers that contribute to added weight and complexity of platform installations. Variations in environmental temperatures during operational theaters make thermal control more difficult, especially in extreme climates where ambient heat loads are higher than the cooling capacity of the system. Power distribution and energy storage demands call for platform modifications that compromise mobility, stealth features, and operational flexibility required for new military operations.

Propagation problems in the atmosphere are still major impediments to the success of military laser systems, especially in maintaining beam quality for operational engagement distances. Turbulence, thermal blooming, and atmospheric absorption lower laser power density at target points, necessitating greater original power levels to produce desired effects. Weather dependence restricts operational availability when laser performance decreases significantly owing to scattering and absorption processes.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Growing Strategic Imperative for Active Defense Capabilities Drives Segment Growth

The market is segmented by type into weapons and non-weapons.

The weapons segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 8.8%. The growth is attributed to the urgent operational needs for directed energy weapons to counter emerging asymmetric threats such as unmanned aerial vehicles, hypersonic missiles, and precision-guided munitions. The rapid growth is indicative of strategic military doctrine development focusing on precision engagement with minimal collateral damage, especially for urban warfare and peacekeeping operations where civilian lives need to be avoided.

- For instance, in September 2025, the Australian defense firm Electro Optic Systems supplied its Apollo High Energy Laser Weapon system to a non-disclosed NATO nation, the first high-power directed energy system for sale on the international weapons market with 150-kilowatt capability and internal power supply enough to tackle 200 medium-sized drones.

In 2026, the non-weapons sub-segment holds the market largest share with around 83.68% in global military laser systems market share, the culmination of decades of effective employment in target designation, range finding, communication, and guidance application domains that are the pillars of current precision warfare capabilities. The segment supports well-established supply chains, mature manufacturing processes, and demonstrated reliability over a wide range of environmental conditions that render these systems mission-critical to enable current military operations propels the segmental leadership.

By Weapons

Operational Effectiveness and Combat-Proven Lethality Catalyzed Segment Growth

The market is segmented by weapons into lethal weapon and non-lethal weapon.

The lethal weapon segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 9.2%. The segment also dominated the global market with 80.15% share in 2024. The capability provides quantifiable battlefield effectiveness in the form of established target destruction against a wide range of threats such as drones, missiles, artillery, and combat aircraft. Lethal capabilities are the high priority for military forces since these systems offer abDolute threat neutralization through physical destruction of the target, precluding any resumed enemy operations or reassembled attacks that non-lethal systems cannot promise.

- For instance, in February 2025, the U.S. Navy's USS Preble successfully tested its HELIOS high-energy laser weapon system against an approaching drone, destroying the target fully and verifying the system's deadly capability for use in maritime defense.

The non-lethal weapon segment grows moderately with a market share of around 19.85% as it provides specialized support functions such as crowd control, personnel deterrence, and temporary incapacitation uses that substitute instead of replace lethal systems. Defense buying trends prefer non-lethal systems for targeted situations such as urban warfare, peacekeeping missions, and rules of engagement where temporary incapacitation is preferable to destruction.

By Non-Weapons

Increasing Demand for Precision Guided Munitions Revolution and Terminal Guidance Integration Aids Segment Growth

The market is segmented by non-weapons into laser altimeter, laser designator, laser pointer/illuminator, laser rangefinder, laser terminal, liDar system, and ring laser gyroscope.

The laser terminal segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 9.5%. The growth is attributed to the high demand for precision-guided munitions with sophisticated terminal guidance systems that maximize accuracy and minimize collateral damage. Contemporary precision-guided munitions increasingly rely on laser terminal guidance systems in their terminal approach section, allowing for course correction in the last few kilometers so they can have circular error probabilities under three meters. Furthermore, the segment's growth is fueled by technological advances in miniature laser seekers, high-performance signal processing algorithms, and hybrid guidance systems integrating GPS navigation and terminal laser homing for increased reliability.

- For instance, in July 2024, BAE Systems successfully tested laser-guided rockets at the U.S. Army's Dugway Proving Ground in Utah, demonstrating precision terminal guidance capabilities against new and rapidly evolving targets such as enemy vehicles and mobile missile launchers, with the systems delivering basketball-sized target accuracy at extended ranges.

The laser designator sub-segment holds market leadership with an estimated 65% market share, demonstrating decades of effective deployment in target designation, precision-guided munitions support, and close air support missions that are the backbone of contemporary joint warfare operations. The segment holds technology leadership through ongoing developments in range, accuracy, beam quality, and integration with sophisticated electro-optical systems that improve target acquisition under adverse operational conditions.

By Technology

Advanced Beam Quality, Tactical Deployment Advantages, and Enhanced Efficiency Catalyze Segment Growth

The market is segmented by technology into lethal solid-state laser, fiber laser, semiconductor laser, gas laser, liquid laser, and free-electron laser.

The fiber laser segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 8.4%. The growth is driven by higher beam quality, unparalleled power scalability, and sophisticated thermal management performance that provides unprecedented tactical deployment flexibility. Fiber laser technology attains outstanding beam coherence utilizing optical fiber gain media that provide consistent performance over long operational ranges, allowing military forces to maintain precision targeting capabilities necessary for counter-drone and surgical strike missions. Fiber laser technology is driven by accelerated uptake through artificial intelligence solutions that facilitate autonomous targeting, real-time power optimization, and predictive maintenance features crucial for continuous military operations.

- For instance, in July 2025, the U.S. Army showcased fiber laser cutting abilities for military and defense purposes highlighting improved efficiency and accuracy in the production of airframe parts and electronic enclosures with considerably lower processing times than in conventional manufacturing processes.

In 2026, the solid-state laser sub-segment of the military laser systems market retains market leadership with around 45.36% market share, a testament to decades of effective military adoption, mature manufacturing practices, and established battlefield performance in diverse operating environments. Solid-state laser technology employs crystalline or glass gain mediums that offer outstanding beam quality, compact size features, and minimum power consumption necessary for mobile and airborne military operations such as target designation, range finding, and counter-unmanned aerial system missions.

By Output Power

Growing Strategic High-Energy Applications Anticipate Market Growth

The market is segmented by output power into below 10 kW, 10 kW to 100 kW, and above 100 kW

The above 100 kW segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 9.6%. The growth is driven by growing adoption of strategic missile defense, anti-ship attack, and protection of critical infrastructure. High-energy systems above 100 kW in this category provide adequate power density to counter hypersonic threats, theater ballistic missiles, and combat swarms of drones at long ranges beyond 10 km, meeting pressing operational needs that less-power lasers cannot solve. Ongoing technological advancement in adaptive optics and prognostic power management improves the quality of the beam and engagement reliability in unfavorable weather, further solidifying this class's attractiveness for future generation layered defenses.

- For instance, in February 2025, the U.S. Navy signed a USD 200 million contract with Lockheed Martin and Northrop Grumman to develop a 300 kW-class solid-state laser weapon demonstrator to be mounted on Arleigh Burke–class destroyers, the first joint high-energy laser integration between two major OEMs for fleet-wide trials.

The 10 kW sub-segment is expected to continues lead with around 77.59% market share in 2026, as widespread deployment on vehicle-mounted, hand-carried, and unmanned system payloads for counter-UAV, convoy security, and base defense applications. These low-power lasers provide non-kinetic effects appropriate for disabling sensors, optics, and propulsion modules of small drones and remote-controlled devices, meeting a wide range of tactical applications where strategic high-energy weapons are impractical.

By Application

Increasing Significant Revolutionary Combat Capabilities and Strategic Investment Priority Poised Segment Growth

The market is segmented by application into target designation and ranging, navigation, guidance, & control, defensive countermeasures, communication system, and directed energy weapons.

The directed energy weapons segment held the highest market share of 30.13% in 2024 and the segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 8.5%. The growth is driven by defense modernization expenditures and imperative operational needs for countering advancing asymmetric threats. Military forces globally see directed energy weapons as game-changers that offer speed-of-light engagement in real-time against hypersonic missiles, swarms of drones, and precision-guided munitions that can't be countered by traditional kinetic interceptors.

- For instance, in August 2025, the U.S. Army effectively tested its Directed Energy Maneuver Short-Range Air Defense system mounted on Strykers in live fire exercises at White Sands Missile Range with 100% engagement success against Group 1-3 drone targets and confirming the readiness of the system for operational deployment to forward combat units.

The target designation and ranging segment is expected to hold the highest market share of 23.27% in 2026 and the segment has steady growth with compound annual growth rate 7.2% for 2026-2034, which demonstrates its proven position as indispensable supporting infrastructure for precision-guided munitions and fire control systems. Growth is supported by ongoing demand for precision targeting capabilities that minimize collateral damage while improving accuracy across conventional weapons systems. Procurement trends in defense tend to lean toward designation and ranging systems as they can be used both for offensive precision strike missions and defensive target identification missions critical for force protection operations.

By Platform

Accelerated Tactical Ground-Based Defense Expansion by Emerging Countries Poise Segment Growth

The market is segmented by application into land, naval, airborne, and space.

The land segment is estimated to be the fastest growing segment during the forecast of 2026-2034 with a highest CAGR of 8.3%. The growth is driven by pressing needs for mobile directed energy weapons effective in response to UAS swarm, rocket, artillery, and mortar threats in expeditionary environments. Ground platform expansion is motivated by the technology's magazine without end effect, removing ammunition resupply limitations and enabling continuous area defense in extended engagements. Modular power and cooling, along with improvements in fiber laser efficiency, allow tactical vehicles to provide needed electrical power from onboard generators without sacrificing mobility or combat duration.

- For instance, in August 2025, the U.S. Army's Stryker-mounted High Energy Laser prototype program, funded with USD 350 million in FY 2026 for 150–300 kW class systems, is a prime example of rapid transition from testing to forward operating units, providing direct-fire capabilities integrated on combat vehicle chassis with minimal platform modification.

The airborne sub-segment dominates the market with about 38.75% share, mirroring widespread integration of laser systems on unmanned and manned platforms for precision strike, target designation, and stand-off defense missions. The U.S. Air Force MQ-9 Reaper has been operationally deployed with 5–10 kW laser pods since 2023, with over 1,200 flight hours in CENTCOM theaters and >95% mission-capable rates for counter-UAS operations. Airborne platforms are augmented by strong onboard power generation and cooling systems, permitting continuous high-energy engagements that are not threatened by line-of-sight obstruction issues experienced by ground forces.

To know how our report can help streamline your business, Speak to Analyst

Military Laser Systems Market Regional Outlook

By geographic, the market is categorized into North America, Europe, Asia Pacific, and Rest of World.

NORTH AMERICA

North America recorded a market size of USD 2.85 billion in 2025, capturing 36.38% of the global market share, and is projected to reach USD 3.03 billion in 2026. The growth is fueled by record defense budget appropriations and strategic modernization programs in the U.S. and Canada. The market's strong growth is a testament to strategic focus on countering asymmetric threats such as unmanned aerial systems, hypersonic missiles, and precision-guided munitions that conventional kinetic interceptors cannot economically counter. Government agency and prime contractor defense industry partnerships with major players such as Lockheed Martin, Raytheon, Northrop Grumman, and up-and-coming experts including BlueHalo enable short technology development cycles through Other Transaction Authority contracts that simplify procurement.

The U.S. market is projected to reach USD 2.66 billion by 2026. The U.S. spearheads this regional growth by investing Department of Defense funds of over USD 1.2 billion every year into the development of directed energy weapons, underpinned by in-depth funding mechanisms such as the FY 2025 defense budget request of USD 849.8 billion that focuses on integrating cutting-edge weapon systems. Congressional appropriations show enduring commitment in multi-year programs, with the Pentagon reserving USD 25 billion for the Golden Dome missile defense program focused on satellite-based laser interceptors and ground-directed energy capabilities. The successful overseas deployment by the U.S. Army of BlueHalo's 20-kilowatt LOCUST laser weapon system in May 2024 is the first operational combat use of laser weapons, showing successful transition from prototype development to battle capability.

- For instance, in March 2025, HII's Mission Technologies received a contract from the U.S. Army Rapid Capabilities and Critical Technologies Office to design an open architecture High-Energy Laser weapon system which is able to acquire, track, and destroy Group 1-3 Unmanned Aircraft Systems, with prototype slated to go into low-rate initial production after successful field testing.

North America Military Laser Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

EUROPE

In 2025, Europe represented USD 2.1 billion, accounting for 26.75% of the worldwide market, and is projected to grow to USD 2.27 billion in 2026. Taking advantage of mutual defense strategies such as the European Defense Fund's USD 7.3 billion budget for 2021-2027 and NATO's newly implemented 5% GDP defense budget target that jointly manages over USD 800 billion in defense modernization spending. The U.K. takes a lead in regional development via its DragonFire laser weapon system, backed by USD 100 million joint funding from the Ministry of Defense and industry partners MBDA, Leonardo, and QinetiQ, with successful high-power trials of firing precision equating to striking a USD 1 coin from one kilometer away. The UK market is projected to reach USD 0.42 billion by 2026, and the Germany market is projected to reach USD 0.46 billion by 2026.

Regional market expansion mirrors increased defense cooperation in response to growing security threats posed by the conflict in Eastern Europe and developing asymmetric threats demanding precision engagement capabilities. Standardization requirements by NATO shape interoperability efforts ensuring that laser systems can be integrated across the platforms of alliance member nations, yielding economies of scale while lowering the cost of individual nation procurements through joint purchasing agreements. The European Defense Industrial Reinforcement through Common Procurement Act (EDIRPA) offers the financial incentives for multinational defense initiatives, whereas the draft Security Action for Europe (SAFE) instrument would trigger a maximum of USD 150 billion of loans for multi-member state procurement initiatives.

- For instance, in March 2024, the U.K. Royal Navy successfully carried out high-power firing trials of the MOD's DragonFire laser directed energy weapon system at the MOD's Hebrides Range, successfully targeting aerial threats with precision and proving operational capability for 2027 naval deployment.

ASIA PACIFIC

The Asia Pacific market generated USD 1.86 billion in 2025, representing 23.70% of the global market landscape, and is expected to reach USD 1.99 billion in 2026. Asia Pacific is estimated to be the second fastest growing region with a compound annual rate of 7.6% spurred by rising geopolitical tensions and high defense budget hikes in key economies such as China, India, Japan, and South Korea. Defense spending budget allocation by India is USD 415.9 billion projected for 2025-2029, with particular focus on the development of indigenous directed energy weapons by Defense Research and Development Organisation efforts to address import dependence while developing sovereign capabilities. The Japan market is projected to reach USD 0.3 billion by 2026, the China market is projected to reach USD 0.77 billion by 2026, and the India market is projected to reach USD 0.39 billion by 2026.

Regional tensions within the South China Sea, Korean Peninsula, and Indo-Pacific maritime territories compel pressing needs for precision engagement systems that are able to counter drone swarms, missile threats, and electronic warfare capabilities that conventional systems are not well suited to counter. Military industrial partnerships between private contractors and government agencies facilitate rapid prototype creation, with governments such as Japan providing USD 1.8 billion for vehicle-mounted laser system demonstrations while South Korea's DAPA has funded USD 63.4 million development programs since 2019.

- For instance, in July 2024, South Korea's Defense Acquisition Program Administration released news of the world's first mass production deployment of laser weapons using the Block-I system, meeting a 100% success rate in disabling test targets and making the country the leader in wide scale military use of lasers.

REST OF THE WORLD

The Rest of World comprising Middle East & Africa and Latin America regions express consistent growth potential based on defense modernization initiatives, strategic alliances, and heightened security demands necessitating superior technological solutions. The market in Rest of the World reached USD 1.03 billion in 2025, representing 13.17% of total market revenue, and is projected to reach USD 1.07 billion in 2026.

Middle Eastern countries such as Saudi Arabia, United Arab Emirates, and Israel spearhead regional spending with large defense budget outlays. UAE seeking vital technology transfers through strategic alliances with Israeli defense vendors. Development of Israel's Iron Beam laser system is regional technological leadership, whereby cooperative development by Elbit Systems and Rafael Advanced Defense Systems targets operational deployment readiness by late 2024, providing cost savings alternatives over legacy interceptors costing USD 50,000 per unit against zero or near-zero costs of laser engagements.

- For instance, in September 2025, Israel's Defense Ministry reported that the Iron Beam laser anti-missile system successfully passed operational tests and reached full operational maturity, being the world's first high-power laser interception system available for military deployment by the end of the year.

The Latin American market demonstrates expansion opportunity through largest military spending underpinning indigenous defense industry growth in all firms involved in aircraft, missile systems, and naval platforms. Regional market growth indicates the increasing acceptance of laser systems' affordability and accuracy capabilities critical to the anticipation of asymmetric threats such as drone swarms, border security issues, and terrorism-related activities that cannot be countered efficiently by conventional systems.

COMPETATIVE LANDSCAPE

Key Market Players

Escalating Investments in Advanced Technological Components by Key Players Propel Market Growth Potential

The military laser systems market illustrates a very competitive landscape that is dominated by longstanding defense contractors with large research and development capabilities, strategic government alliances, and successful operational deployment history. The competitive landscape is marked by extensive technological differentiation, huge investment requirements, and intimate coordination between industry leaders and government defense organizations to develop directed energy capabilities into various military platforms.

The competitive environment for military laser systems shows fierce competition fueled by precision targeting capability, energy output level, platform suitability, and defense-grade reliability needs. Leaders compete through strategic government alliances, large investment in research and development, collaborative development programs with technology suppliers, and involvement in defense consortia to speed up deployment schedules while meeting military standards. Firms emphasize modular architecture, scalability capabilities, over-the-air software updates, and sophisticated energy management systems in order to increase operational flexibility and preserve competitive positions.

- For instance, in October 2024, Elbit Systems entered into a contract with the Israeli Ministry of Defense to attain operational deployment of next-generation, Israeli-made high-power military laser systems for the Iron Beam ground-based system, and successful tests were concluded in September 2025.

Competitive tactics highlight collaboration with the military for operational testing, winning long-term government contracts based on demonstrating performance, and mergers and acquisitions to increase technological capabilities and presence in the marketplace. The semi-consolidated nature of the marketplace enables established contractors to capitalize on years of experience while new specialists bring innovative technology and cost-effective solutions to given application segments.

List of Key Global Military Laser Systems Market Companies Profiled:-

- BAE Systems (U.K.)

- The Boeing Company (U.S.)

- Elbit System (Israel)

- Israel Aerospace Industries Ltd. (Israel)

- L3Harris Technologies Inc. (U.S.)

- Leidos Holdings, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- MBDA (France)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Rheinmetall AG (Germany)

- Safran S.A. (France)

- Textron Inc. (U.S.)

- Thales Group (France)

Key Industry Developments

- September 2025: Elbit Systems has successfully tested the Iron Beam system and is progressing on the ongoing development of an advanced, Israeli-produced, high-power military laser, which could significantly enhance defense capabilities. In accordance with a contract signed with the Ministry of Defense, Elbit Systems, in collaboration with partners, is striving for a major breakthrough that will facilitate the operational implementation of an advanced, Israeli-made, high-power military laser within the ground-based Iron Beam system.

- August 2025: Coherent's aerospace and defense segment has secured a USD 30 million deal to create high-power lasers for the U.S. Navy. This agreement includes the creation of pulsed fiber lasers for remote sensing and illumination while advancing the development of a 400-kilowatt directed-energy subsystem by incorporating a 50-kilowatt laser with a beam-control assembly.

- July 2025: The U.S. Army intends to acquire a couple of new laser weapons mounted on vehicles as part of a new initiative aimed at intercepting incoming drones and missiles, enhancing its existing primary system.

- June 2025: Coherent's aerospace and defense segment has secured a USD 30 million deal to create high-power lasers for the U.S. Navy. This agreement includes the creation of pulsed fiber lasers for remote sensing and illumination while advancing the development of a 400-kilowatt directed-energy subsystem by incorporating a 50-kilowatt laser with a beam-control assembly.

- March 2025: The Pentagon has announced that the U.S. State Department has approved the initial sale of advanced precision kill weapon systems to Saudi Arabia, valued at approximately USD 100 million. The approved Advanced Precision Kill Weapon System (APKWS) is a laser-guided rocket capable of striking both aerial threat and ground targets.

REPORT COVERAGE

The global military laser systems market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the military laser systems market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historic Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.70% from 2026-2034 |

|

Unit |

USD Billion |

|

By Segmentation |

By Type, By Weapons, By Non-Weapons, By Technology, By Output Power, By Application, By Platform, By Region |

|

By Type

By Weapons

By Non-Weapons

By Technology

By Output Power

By Application

By Platform

|

|

|

By Region |

North America (By Type, By Weapons, By Non-Weapons, By Technology, By Output Power, By Application, By Platform, By Country)

Europe (By Type, By Weapons, By Non-Weapons, By Technology, By Output Power, By Application, By Platform, By Country)

Asia Pacific (By Type, By Weapons, By Non-Weapons, By Technology, By Output Power, By Application, By Platform, By Country)

Rest of World (By Type, By Weapons, By Non-Weapons, By Technology, By Output Power, By Application, By Platform, By Sub-Region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.37 billion in 2026 and is projected to reach USD 14.06 billion by 2034.

In 2025, the market value stood at USD 2.85 billion

The market is expected to exhibit a CAGR of 6.70% during the forecast period of 2026-2034.

The land segment in platform is expected to hold the highest CAGR over the forecast period.

Growing defense budget modernization, geopolitical security concerns, technological advancement and operational cost efficiency drive market growth

Raytheon Technologies, Lockheed Martin, Elbit Systems, Thales Group, Leonardo DRS, Inc., and among others are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us