Non-Lethal Weapons Market Size, Share & Industry Analysis, By Weapon Type (Chemical Non-Lethal Weapons, Acoustic Non-Lethal Weapons, Electrical Non-lethal Weapons, Blunt Impact Weapons, Projectile Non-Lethal Weapons), By Range (Short Range, Medium Range, Long Range), By System (Standalone, Integrated, Remote), By Component (Delivery Mechanisms, Control Systems & Power Sources), By Application (Law Enforcement Operations, Riot Control, Self-Defense, Crowd Control, Border Control), By End User (Homeland Security, Defense & Personal Defense) & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

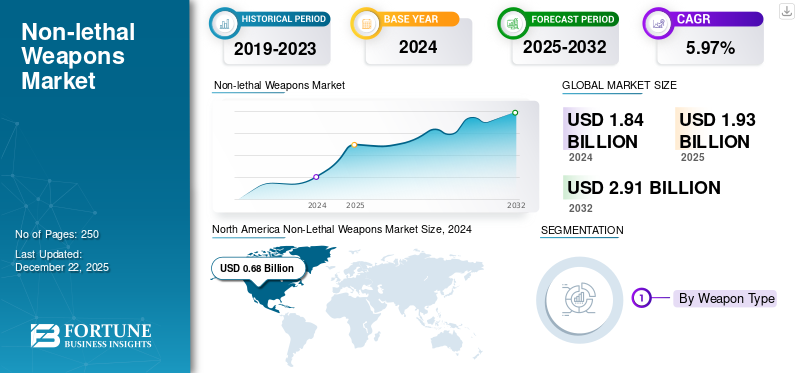

The global non-lethal weapons market size was valued at USD 1.94 billion in 2025 and is projected to grow from USD 2.05 billion in 2026 to USD 3.25 billion by 2034, registering a CAGR of 5.94% over the forecast period. North America dominated the non-lethal weapons market with a market share of 36.72% in 2025.

Non-lethal Weapons (NLWs) are designed to incapacitate or deter individuals without causing permanent harm, serving critical roles in military, law enforcement, and crowd control operations. These weapons encompass various technologies, including electromagnetic systems, chemical agents such as tear gas, acoustic devices, and kinetic energy projectiles, all aimed at achieving operational objectives while minimizing fatalities.

The integration of artificial intelligence (AI) and machine learning (ML) is enhancing the effectiveness of NLWs by improving targeting accuracy and decision-making processes. AI-driven systems can analyze real-time data to assess threats, while autonomous drones and robots can deploy non-lethal munitions in controlled environments, reducing risks to personnel during operations.

Modular design trends in NLW development allow for greater customization and adaptability for specific missions. Manufacturers are focusing on standardized components to reduce costs and improve deployment speed. As research progresses, the aim is to create sophisticated systems that comply with legal and ethical standards while ensuring effectiveness in complex environments.

The market is populated by a mix of established defense contractors and specialized companies. Key players include Axon Enterprise (TASERs, body cameras), Safariland (less-lethal munitions, body armor), Combined Systems Inc. (crowd control solutions), and FN Herstal (less-lethal firearms). These companies develop and distribute a range of products, including electroshock weapons, chemical irritants, impact munitions, and acoustic devices. The market is driven by increasing global security concerns, demand for effective crowd control solutions, and emphasis on minimizing fatalities in law enforcement and military operations.

The COVID-19 pandemic initially disrupted the market due to supply chain disruptions and reduced government spending. However, increased social unrest and protests during the pandemic led to heightened demand for crowd control solutions, partially offsetting the negative impact. Furthermore, the focus on social distancing accelerated the adoption of body cameras, boosting demand for companies such as Axon. Overall, while the pandemic caused initial setbacks, the market demonstrated resilience and experienced renewed development driven by evolving security challenges.

Download Free sample to learn more about this report.

GLOBAL CONFLICTS

Global Conflicts Fuel Market, Geopolitical Tensions Drive Demand and Innovation

The Russia-Ukraine War, the Iran-Israel conflict, and the India-Pakistan tensions, while distinct in their origins and specific dynamics, all exert significant, albeit multifaceted, impacts on the non-lethal weapons market growth. These geopolitical hotspots amplify demand for specific types of non-lethal technologies, influence market trends, and shape the strategic priorities of key players.

Russia-Ukraine War

The Russia-Ukraine war's impact on the market is two-fold: direct and indirect. Directly, the conflict has exposed vulnerabilities in existing security infrastructure and highlighted the need for improved border security and internal control measures. This has led to increased demand for surveillance technologies, including drones equipped with non-lethal payloads (e.g., sensors, acoustic deterrents), and counter-drone systems capable of disrupting or disabling enemy drones without causing physical destruction. Furthermore, the widespread displacement of civilians has underscored the importance of humanitarian demining efforts, creating demand for advanced demining tools and protective gear. The conflict has also highlighted the potential of cyber warfare, leading to investments in non-lethal cyber capabilities for defense and information warfare.

Indirectly, the war has heightened anxieties regarding regional stability and potential spillover effects. Neighboring countries have increased their defense spending, including investments in non-lethal solutions for border control, internal security, and civil defense. The war has also accelerated the trend toward technological sovereignty, prompting countries to prioritize domestic production of critical defense equipment, including NLWs. This has created opportunities for local manufacturers and fostered innovation in the non-lethal technology sector. Moreover, the conflict has accelerated the development and deployment of advanced surveillance technologies, such as AI-powered video analytics and facial recognition systems, which are used for monitoring borders, identifying potential threats, and managing refugee populations. Ethical considerations regarding the use of these technologies have also gained prominence.

Iran-Israel Conflict

The ongoing tensions between Iran and Israel, characterized by proxy wars and cyberattacks, have a profound impact on the market, particularly in the realm of cybersecurity and electronic warfare. Both nations are investing heavily in offensive and defensive cyber capabilities, including tools for network intrusion, data exfiltration, and system disruption. The non-lethal nature of these attacks allows for deniability and avoids escalation to conventional warfare. Furthermore, the conflict has spurred demand for advanced electronic warfare systems capable of jamming communications, disrupting radar systems, and disabling drones without causing physical damage.

The threat of physical attacks on critical infrastructure has also led to increased demand for perimeter security systems, including sensors, alarms, and video surveillance technologies. Moreover, there is a growing emphasis on developing non-lethal methods for countering improvised explosive devices (IEDs) and other asymmetric threats. This includes the use of robots and drones for bomb disposal, and advanced detection technologies capable of identifying explosives from a safe distance. The complex and volatile nature of the Iran-Israel conflict necessitates a multi-layered approach to security, incorporating both conventional and non-lethal capabilities.

India-Pakistan Conflict

The long-standing conflict between India and Pakistan, marked by border skirmishes, terrorism, and nuclear brinkmanship, has a significant impact on the market, particularly in the areas of border security, counter-terrorism, and crowd control. Both countries are investing heavily in border surveillance technologies, including sensors, radars, and drones, to monitor the Line of Control and prevent cross-border infiltration. The use of non-lethal deterrents, such as acoustic devices and laser dazzlers, is also becoming increasingly common.

The threat of terrorism necessitates the deployment of NLWs for law enforcement and security forces. This includes the use of tasers, pepper spray, and stun grenades for apprehending suspects without causing serious injury. Furthermore, there is a growing emphasis on developing non-lethal methods for countering IEDs and other terrorist threats. This includes the use of robots and drones for bomb disposal, as well as advanced detection technologies capable of identifying explosives from a safe distance. The frequent incidents of civil unrest and protests in both countries also drive demand for non-lethal crowd control solutions, such as water cannons, tear gas, and rubber bullets. However, the use of these weapons is often controversial, raising concerns about human rights and the potential for abuse.

NON-LETHAL WEAPONS MARKET TRENDS

Evolving Security Concerns and Increasing Preference for Effective Humane Alternatives

The market for non-lethal weapons is experiencing significant growth, fueled by a confluence of factors including increasing concerns about civilian casualties, the need for de-escalation tactics in law enforcement, and the evolving nature of modern conflict. This trend is not solely about military applications; it is impacting law enforcement, private security, and personal protection sectors. The aim to minimize fatalities and injuries, while still effectively controlling crowds, neutralizing threats, or maintaining order, is a primary driver. This has spurred innovation and investment in a diverse range of technologies, including less-lethal ammunition such as beanbag rounds and rubber bullets, acoustic weapons, directed energy devices, and incapacitating sprays.

One significant factor driving the market is the increased scrutiny of law enforcement practices and the demand for accountability in the use of force. Public pressure and legal repercussions associated with excessive force are pushing agencies to adopt less-lethal options. Simultaneously, the rise in civil unrest and protests globally has created a need for effective crowd control methods that minimize the risk of serious injury. Furthermore, the private security sector is increasingly seeking non-lethal options for protecting assets and personnel without resorting to deadly force, contributing to the market's expansion.

Technological advancements are also playing a key role. Research and development is focused on improving the accuracy, range, and reliability of non-lethal weapons, as well as minimizing potential side effects. For example, advancements in directed energy weapons are exploring ways to deliver incapacitating effects without causing lasting harm. The integration of artificial intelligence and data analytics is also contributing to the development of more targeted and precise non-lethal solutions. The overall trend reflects a growing emphasis on finding humane and effective alternatives to lethal force in a variety of security contexts.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increased Political Disputes, Civil Unrest, and Militarization of Homeland Security Agencies Lead to Robust Market Growth

Political instability and civil unrest have become concerning global issues, significantly impacting societies and economies. As these challenges escalate, the demand for NLWs has surged, driven by the need for effective crowd control and public safety measures.

The Allianz Risk Barometer 2024 highlighted that political violence and civil unrest ranked as a major concern for businesses, marking its highest position since 2017. In 2023 alone, anti-government protests erupted in 83 countries, fueled by rising inflation, wealth inequality, and perceived threats to democracy. These alarming trends have prompted governments to equip law enforcement agencies with NLWs to manage crowds effectively while minimizing the risk of fatalities.

The rise in non-state conflicts—from 76 in 2021 to 82 in 2022—underscores the growing instability that necessitates innovative solutions for maintaining order. Ongoing conflicts in regions such as Gaza and Sudan further illustrate the urgent need for effective crowd control measures that prioritize civilian safety.

In addition, the militarization of law enforcement agencies has played a crucial role in expanding the NLW market. Many police departments, particularly in the U.S., have integrated military-grade equipment, including NLWs, into their operations to handle civil disturbances more effectively. This trend is not confined to North America; Latin American countries are also adopting militarized policing practices to address rising crime rates and civil unrest.

For instance, reports from June 2023 indicated that police forces globally were enhancing their capabilities through advanced training and equipment acquisition focused on non-lethal technologies. This includes the deployment of tasers, pepper spray, and other crowd control measures designed to incapacitate individuals without causing permanent harm.

The focus on civilian protection is further reflected in recent developments within the NLW market. Companies are innovating to meet the growing demand for safer alternatives. For example:

For instance, in January 2023, Byrna Technologies Inc. launched Byrna LATAM, a subsidiary aimed at expanding its product line across Latin America. This strategic move allowed Byrna to tap into emerging markets while addressing unique regional security needs.

In April 2023, the Springfield Police Department introduced the Bolawrap restraint device, emphasizing its minimal risk of injury during apprehensions. This device is especially beneficial for handling situations involving individuals experiencing mental health crises or substance abuse issues.

Increasing Emphasis on Civilian Protection and Public Safety to Drive Market Growth

There is a growing demand for personal protection tools among civilians, particularly in urban areas. Products such as pepper sprays, stun guns, and personal alarms are gaining popularity as effective means of self-defense without the ethical implications associated with lethal force. The demand for these products is further supported by regulatory frameworks that encourage the use of non-lethal alternatives.

Governments are increasingly recognizing the importance of minimizing civilian casualties during law enforcement operations, leading to supportive regulatory frameworks that facilitate the use of these tools. For example, in May 2023, the Baltimore Police Department secured a USD 5 million contract with Axon Enterprise Inc. for enhanced non-lethal weaponry, reflecting a commitment to integrating these tools into their operations.

In June 2023, the Los Angeles Police Department began deploying advanced non-lethal tools to enhance community safety. This initiative ensures that officers are equipped with effective means to handle various situations without resorting to lethal force.

MARKET RESTRAINTS

Concerns Regarding Effectiveness and Reliability to Hamper Market

Non-lethal weapons, such as rubber bullets and chemical agents, may yield inconsistent results depending on various factors, including the target's age, health, and body size. Some individuals may not respond as intended to certain non-lethal measures, raising doubts about their reliability in critical scenarios. This inconsistency can lead law enforcement agencies to revert to lethal options if non-lethal methods fail to achieve the desired outcome.

Many weapons have limitations in range and accuracy, which can compromise their effectiveness in dynamic environments. For example, the Air Force Security Forces Center has emphasized the need for reliable and precise non-lethal options; however, it recognizes that some devices may not perform effectively at longer distances or under varied conditions. This limitation can deter agencies from fully integrating these weapons into their operational protocols.

The Department of Defense has been actively revising its guidelines on non-lethal weapon usage following reports indicating inconsistent performance across different environments. These revisions aim to establish clearer standards for effectiveness and reliability while also reflecting ongoing concerns about current capabilities.

For instance, in August 2023, the U.S. Army evaluated various non-lethal weapon systems as part of its commitment to enhancing operational readiness. This highlighted the need for improved training protocols to ensure that personnel can effectively utilize these weapons in real-world scenarios.

In July 2023, a study published by the National Institute of Justice emphasized that while non-lethal weapons are valuable tools for de-escalation, their operational success is often contingent on rigorous testing and evaluation processes. The study called for enhanced research into the physiological effects of various non-lethal technologies to better understand their impact on diverse populations.

MARKET OPPORTUNITIES

Security Needs, Technology, and Ethical Considerations Boost Market Growth

The market presents a significant opportunity driven by increasing global instability and a growing emphasis on minimizing harm in conflict situations. The demand stems from law enforcement agencies, military organizations, and private security firms seeking solutions for crowd control, border security, and active shooter scenarios. One key opportunity lies in advanced surveillance technologies. AI-powered video analytics, drone-based surveillance, and long-range acoustic devices are crucial for early threat detection and preemptive intervention. Similarly, the market is ripe for innovative counter-drone systems that can neutralize drone threats without causing collateral damage.

Another area of progress is in less-lethal munitions. Research and development of safer, more accurate, and target-specific munitions present a chance to refine existing technologies and reduce the risk of unintended injury. This includes exploring bio-chemical alternatives for irritants and developing more effective impact munitions with variable force options. Moreover, the market needs sophisticated cyber warfare tools. The development and deployment of non-lethal cyber weapons that can disrupt enemy networks and infrastructure without physical destruction are becoming increasingly critical in modern warfare. Focus is needed on capabilities such as data exfiltration and network intrusion for intelligence gathering.

Addressing the ethical considerations surrounding NLWs is also a key opportunity. Companies that prioritize responsible development, comprehensive training programs, and adherence to international human rights standards will gain a competitive advantage. Investing in research and development to explore safer technologies is paramount for the long-term sustainability of the market.

MARKET CHALLENGES

Concerns Regarding Effectiveness and Reliability to Hamper Market Growth

The market faces several key challenges. Ethical concerns surrounding their use are paramount, with potential for misuse and unintended harm necessitating strict regulation and comprehensive training. Public perception and acceptance are also crucial, as negative publicity can hinder adoption. Technical limitations pose another hurdle. Achieving the desired effectiveness without causing serious injury remains a balancing act, requiring continuous innovation and improvement in weapon accuracy and control.

Market fragmentation and a lack of standardized testing procedures make it difficult to compare different products and ensure quality. Furthermore, the high cost of research and development can be a barrier to entry for smaller companies. Finally, navigating complex legal frameworks and export controls can be challenging for manufacturers, particularly in the international market. Balancing national security interests with human rights concerns requires careful consideration and adherence to international norms.

SEGMENTATION ANALYSIS

By Weapon Type

Chemical Non-Lethal Weapons Dominate Owing to High Effectiveness and Ease of Use

By weapon type, the market is classified into chemical non-lethal, acoustic-, electrical-, and projectile non-lethal weapons, blunt impact weapons, and others.

The chemical non-lethal weapons segment is projected to reach 25.63% of the global market share in 2026, driven by several key factors, such as high effectiveness in crowd control and a high adoption rate due to ease of use and portability. Furthermore, continuous technological advancements are leading to the development of more sophisticated chemical agents with enhanced capabilities.

For instance, in June 2023, Combined Systems, Inc. (CSI) launched a new line of pepper spray projectiles designed for long-range deployment, enhancing the effectiveness of chemical agents in crowd control situations. In September 2022, Safariland LLC introduced a series of improved tear gas grenades featuring enhanced dispersal patterns and a reduced risk of unintended injuries.

The projectile non-lethal weapons segment is estimated to grow at the highest CAGR over the forecast period. Increased accuracy and range, reduced risk of injuries, and increased adoption and versatility of NLWs are some of the factors driving market progress. For instance, in August 2023, FN Herstal launched a new line of less-lethal ammunition featuring improved accuracy and reduced recoil, enhancing the effectiveness and user-friendliness of their projectile weapons.

Additionally, in November 2022, Rheinmetall AG introduced a new 40mm less-lethal grenade launcher capable of firing a variety of projectiles, including rubber balls and sponge rounds, providing versatility for security forces.

By Range

Medium Range Segment Led Owing to High Demand and Adoption Rate for Law Enforcement and Military Applications

By range, the market is segmented into short range (below 30 meters), medium range (30 to 100 meters), and long range (above 100 meters).

The medium range (30 to 100 meters) segment dominated by range type, holding 43.06% of the market share in 2026 due to several factors, including its versatility, effectiveness in crowd control, and increasing adoption by law enforcement agencies and military forces. Medium-range NLWs typically include devices such as rubber bullets, bean bag rounds, and acoustic hailing devices, which can incapacitate targets without causing permanent harm.

For instance, in August 2023, Byrna Technologies Inc. announced that its Byrna HD launchers were being adopted by various law enforcement agencies across the U.S. for crowd control and personal defense. This highlights the effectiveness of medium-range options in maintaining public safety while minimizing casualties.

The long range (above 100 meters) segment is estimated to grow at the highest CAGR over 2025-2032. This growth is fueled by technological innovations that enhance the range and effectiveness of non-lethal options, allowing military and law enforcement agencies to engage targets from greater distances while minimizing risks to civilians.

For instance, in September 2023, Rheinmetall AG announced successful tests of its new long-range acoustic hailing device designed for military applications. This device allows for communication and crowd dispersal at distances exceeding 1,000 meters, showcasing the potential of long-range NLWs in modern conflict scenarios.

By System

Standalone Systems Segment Dominate Owing to Their Versatility and Effectiveness in Various Operational Scenarios

By system, the market is categorized into standalone systems, integrated systems, and remote systems.

The Standalone System segment is captured 40.63% of the market share in 2026 due to their versatility and effectiveness in various operational scenarios. These systems offer law enforcement and military agencies the capability to manage civil unrest, crowd control, and other non-combat situations without resorting to lethal force. The increasing global emphasis on human rights and the need for less aggressive policing methods further drive the demand for standalone NLW systems.

For instance, in July 2023, Combined Systems Inc. (CSI) introduced a new range of less-lethal munitions, including advanced chemical agents and impact munitions, aimed at improving safety and effectiveness during crowd management operations.

Remote systems are recognized as the fastest-growing segment within the global market, primarily due to advancements in technology that enhance operational safety and effectiveness. These systems allow personnel to engage threats from a distance, reducing the risk of harm to operators while maintaining control over potentially volatile situations.

For instance, in September 2023, Rafael Advanced Defense Systems Ltd. announced that it is developing remote-controlled systems equipped with non-lethal options for border security applications. This initiative responds to the growing demand for safer engagement methods in conflict zones.

By Component

Control Systems Led Due to Rising Emphasis on Precision Targeting and Minimization of Collateral Damages

By component, the market is categorized into delivery mechanisms, control systems, and power sources.

The control systems segment is projected to reach 41.11% of the market share in 2026. Control systems are crucial components of NLWs, enabling precise targeting and minimizing collateral damage. These systems integrate sensors, processors, and actuators to enhance accuracy and reliability. The growing emphasis on reducing unintended injuries and ensuring effective crowd control has made control systems a dominant segment in the market.

For instance, in May 2023, Axon Enterprise Inc. secured a USD 5 million contract with the Baltimore Police Department to equip officers with advanced non-lethal weapons featuring enhanced control systems.

The delivery mechanisms segment is estimated to grow at the highest rate during 2025-2032. Rising demand for portable and easy-to-use weapon systems for law enforcement and military applications, along with the integration of advanced technologies such as electro-optical sensors and programmable logic controllers, is driving segment progress. Additionally, there is a growing emphasis on modular and customizable delivery systems, contributing to market growth.

For instance, in April 2023, Byrna Technologies Inc. announced that the Córdoba Provincial Police force in Argentina would purchase 10,000 Byrna launchers, demonstrating the growing adoption of non-lethal delivery systems.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increased Public Safety Concerns Boosted Law Enforcement Operations Segment Growth

By application, the market is categorized into law enforcement operations, riot control, self-defense, crowd control, border control, and others.

The law enforcement operations segment dominated the market in 2024. Increasing instances of civil unrest, political tensions, and the need for effective crowd control solutions are expected to augment segmental growth. Law enforcement agencies are increasingly adopting non-lethal weapons to manage protests and riots without causing fatalities, thereby adhering to human rights standards and reducing collateral damage.

For instance, in April 2023, China introduced an electromagnetic gun designed for riot control, which utilizes electromagnetic force to fire projectiles at varying speeds, enhancing crowd management capabilities without lethal consequences.

The riot control segment is estimated to witness the fastest-growth during the forecast period. Heightened concerns over public safety and civil disturbances, increasing incidents of protests and riots globally, and growing investment in advanced riot control technologies are key factors driving segment growth. For instance, in January 2023, the U.S. Department of Homeland Security allocated funds for new non-lethal riot control equipment to enhance response capabilities during large-scale protests. Furthermore, companies are innovating with electroshock weapons and directed energy systems that offer more humane alternatives to traditional riot gear.

By End User

Homeland Security Segment Dominated Owing to Increased Civil Unrest and Requirement of Crowd Control Measures

By end user, the market is categorized into homeland security, defense, and personal defense.

The homeland security segment dominated the market in 2024, due to increasing civil unrest, political instability, and the growing need for effective crowd control measures. Governments globally are investing in non-lethal technologies to manage protests and riots without resorting to lethal force, which aligns with public safety concerns and human rights considerations.

The defense segment is estimated to grow at the highest rate during the forecast period. Rising defense expenditures and increasing border disputes are fueling the segment. Countries are increasingly equipping their military forces with NLWs to handle civilian interactions during conflicts, thereby minimizing casualties while maintaining operational effectiveness.

For instance, in October 2021, Apastron Private Limited in India announced the development of non-lethal weapons inspired by traditional combat techniques, responding to recent border tensions and the need for effective crowd management.

NON-LETHAL WEAPONS MARKET REGIONAL OUTLOOK

Based on region, the market is studied across North America, Europe, Asia Pacific, and the rest of the world.

NORTH AMERICA

North America Non-Lethal Weapons Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 0.71 billion, accounting for 36.72% of the worldwide market, and is projected to grow to USD 0.75 billion in 2026, and is likely to remain dominant throughout the forecast period due to robust investments in defense and law enforcement infrastructure. The regional military and law enforcement agencies are increasingly adopting non-lethal alternatives for crowd control, riot mitigation, and counter-terrorism operations, driven by a strong emphasis on public safety and reducing civilian casualties.

The U.S. Department of Defense (DoD) and law enforcement agencies heavily invest in the research, development, and deployment of advanced non-lethal solutions. Moreover, the U.S. market is driven by increased security concerns, the need for effective crowd control, and advancements in technology. Additionally, leading defense contractors such as Raytheon Technologies, General Dynamics, and Axon Enterprise are driving innovation in areas such as acoustic devices, directed-energy weapons, and chemical agents. The U.S. market is projected to reach USD 0.62 billion by 2026.

Furthermore, the presence of major manufacturers accelerate market development. For instance, in August 2023, Northrop Grumman Corporation unveiled an upgraded version of its RWS that integrates non-lethal capabilities. This allows operators to switch between lethal and non-lethal modes seamlessly, enhancing tactical flexibility.

ASIA PACIFIC

Asia Pacific contributed 24.01% to the global market in 2025, with a valuation of USD 0.47 billion, and is projected to reach USD 0.49 billion in 2026. The Asia Pacific region is estimated to be the second-largest market for NLWs. Escalating security concerns, geopolitical tensions, and increased defense budgets in China, India, and Japan are driving this growth. The rise in civil unrest and terrorism has prompted military and law enforcement agencies to invest in non-lethal solutions that minimize collateral damage while effectively managing conflicts. The Japan market is projected to reach USD 0.10 billion by 2026, the China market is projected to reach USD 0.22 billion by 2026, and the India market is projected to reach USD 0.14 billion by 2026.

Additionally, the emphasis on indigenous defense manufacturing is further propelling market growth. For instance, in August 2023, a consortium of Japanese defense firms unveiled new non-lethal crowd control technologies for deployment in urban areas during civil disturbances.

EUROPE

The Europe market generated USD 0.43 billion in 2025, representing 22.32% of the global market landscape, and is expected to reach USD 0.45 billion in 2026. Europe is anticipated to be the fastest-growing region in the global market due to increasing concerns about civil unrest, terrorism threats, and stringent regulations surrounding lethal force use. The law enforcement agencies are investing heavily in non-lethal technologies to enhance crowd control while adhering to human rights considerations. The presence of established defense technology companies fosters innovation and collaboration, further driving market. The UK market is projected to reach USD 0.12 billion by 2026 and the Germany market is projected to reach USD 0.09 billion by 2026.

For instance, in January 2022, Rheinmetall AG developed an advanced version of its Maske smoke grenade system designed for non-lethal crowd dispersal, showcasing ongoing innovation within the sector.

REST OF THE WORLD

Rest of the World contributed approximately USD 0.33 billion to the global market in 2025, accounting for 16.94% share, and is expected to reach USD 0.35 billion in 2026. The rest of the world is experiencing moderate growth in the market, driven by increasing awareness of public safety needs and rising incidences of civil unrest. Countries in the Middle East & Africa, and Latin America are beginning to recognize the importance of adopting non-lethal solutions as part of their security strategies. However, limited budgets and varying levels of regulatory support can hinder more rapid adoption compared to other regions.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Players are Focusing on Integrating Advanced Technologies to Gain a Strong Foothold

The market is relatively fragmented, presenting opportunities for new companies to enter and gain a foothold. However, the massive presence of leading companies can create challenges for new market entrants. To succeed, market players are focusing on integrating advanced technologies to enhance additional capabilities. Players in the market can take advantage of the growing demand and utility of advanced technologies to maximize their revenue potential.

LIST OF KEY NON-LETHAL WEAPON COMPANIES PROFILED

- Nammo AS (Norway)

- Safariland LLC (U.S.)

- Ultra Electronics Holdings plc (U.K.)

- Spectra Group (UK) Ltd. (U.K.)

- Maxam Outdoors Inc. (U.S.)

- Senken Group Co., Ltd. (China)

- FN Herstal S.A. (Belgium)

- Rheinmetall Denel Munition (Pty) Ltd. (South Africa)

- Combined Systems Inc. (CSI) (U.S.)

- Genasys Inc. (formerly LRAD Corporation) (U.S.)

- Byrna Technologies Inc. (U.S.)

- Piexon AG (Switzerland)

- MKU Ltd. (India)

- LHB Industries Inc. (U.S.)

- Digital Ally Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2024 – Wuhan Marine Electric Propulsion Device Research Institute developed an AI-based smart Water Cannon for border control application amid escalating tensions in the South China Sea.

- March 2024 – Maldives announced that it has signed a defense agreement with China under which China would provide aid-based non-lethal weapon systems and related training.

- October 2023 – Moog Inc. announced that it is expanding its RWS capabilities to include non-lethal options, catering to military modernization efforts focused on reducing collateral damage.

- August 2023 — Northrop Grumman Corporation unveiled an upgraded version of its RWS that integrates non-lethal capabilities. This allows operators to switch between lethal and non-lethal modes seamlessly, thereby enhancing tactical flexibility.

- June 2022 – FN Herstal entered into a licensing agreement with Fiocchi Munizioni SpA to manufacture and supply 5.7x28mm ammunition for non-lethal applications in Europe.

REPORT COVERAGE

The global non-lethal weapons market research report covers growth factors such as increasing demand for various applications, adoption of projectile-based non-lethal technologies and advanced chemical agents related to end users, and changing security outlook. The report also includes market size of all regions and includes in-depth information about market segments such as weapon type, range, system, component, application, end-users, and region.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.94% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Weapon Type

|

|

By Range

|

|

|

By System

|

|

|

By Component

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

The global non-lethal weapons market size is projected to grow from USD 2.05 billion in 2026 to USD 3.25 billion by 2034, exhibiting a CAGR of 5.94% during the forecast period.

The market will likely grow at a CAGR of 5.94% over the forecast period (2026-2034).

The market size of North America stood at USD 0.71 billion in 2025.

The top ten players in the industry are Nammo AS, Safariland LLC, Ultra Electronics Holdings PLC, Spectra Group (UK) Limited, Maxam Outdoors Inc., Senken Group Co. Ltd., FN Herstal S.A., Rheinmetall Denel Munition (Pty) Ltd., Combined Systems Inc. (CSI), and Genasys Inc. (formerly LRAD Corporation).

The U.S.s significant investment in defense and security anticipates its dominance.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us