Military Load Carriage Systems (LCS) Market Size, Share & Industry Analysis, By Component (On‑body platforms, Packs & frames, Pouches & accessories, and Hydration & load‑transfer add‑ons), By Material (Nylon webbing, Laser‑cut laminate, Hybrid (reinforced textiles), and Metal/composite frames), By Procurement channel (Prime contractor, Direct to MoD, and Framework/standing offer), By End user (Army, Marines, Special operations, and Others), and Regional Forecast, 2026-2034

Military Load Carriage Systems (LCS) Market Size and Future Outlook

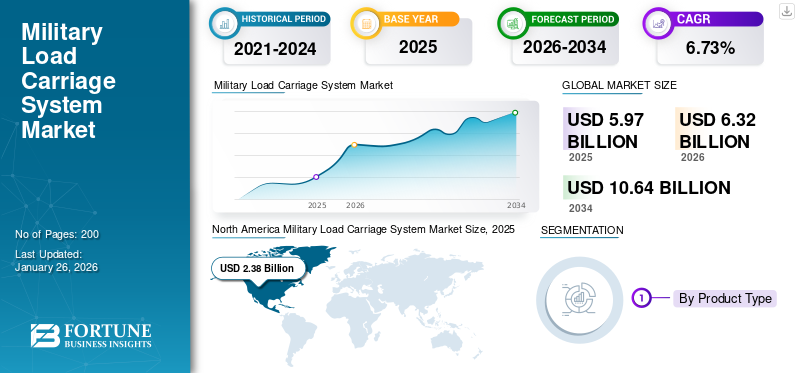

The global military Load Carriage Systems (LCS) market size was valued at USD 2.85 billion in 2025. The market is projected to grow from USD 3.03 billion in 2026 to USD 4.86 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. North America dominated the military load carriage system market with a market share of 34.74% in 2025.

Military Load Carriage Systems (LCS) include vests, plate carriers, backpacks, belts, and modular pouches. Soldiers use these items to carry weapons, ammunition, electronics, and survival gear. The market is growing as soldiers need to carry more equipment, such as radios, batteries, sensors, and body armor. Recent high-intensity conflicts have showcased that mobility and endurance are critical areas to address. Force modernization initiatives focus on survivability and reducing fatigue, which drive the demand for lighter, modular, and more comfortable systems.

Key players such as Point Blank Enterprises, L3Harris, Eagle Industries, Safariland Group, Mehler Protection, and NFM Group shape the market. They focus on modular designs, lightweight materials, and improved load distribution. Their developments involve small but important upgrades such as laser-cut laminates, scalable designs, and better integration with communication and power systems. These changes meet the evolving needs of NATO and European infantry.

Download Free sample to learn more about this report.

MILITARY LOAD CARRIAGE SYSTEMS (LCS) MARKET TRENDS

Modular, Mission-Adaptive Gear is Reshaping and Driving Market’s Growth

A major trend affecting the market is the move from fixed, one-size-fits-all gear to fully modular, mission-adaptive systems. Modern infantry units often engage in diverse missions, such as urban combat, reconnaissance, peacekeeping, and high-intensity warfare, sometimes within the same deployment. Modular load carriage solutions designs allow soldiers to quickly swap out pouches, plates, and packs based on mission needs. This approach helps cut down unnecessary weight while improving mobility and comfort. This trend represents a broader change in military strategy, emphasizing flexible and quickly deployable forces instead of heavy, static infantry units.

In February 2024, European NATO members recognized modular soldier systems as a key requirement in ongoing infantry modernization initiatives. IISS defense equipment reviews noted an increase in the use of scalable load carriage solutions to support multi-role operations among allied forces.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Soldier Load and Mobility Gaps Drive Modernization Spending

One of the main factors propelling the global military Load Carriage Systems (LCS) market is the rise in equipment carried by soldiers in battle. Modern infantry operations require body armor, radios, batteries, sensors, night-vision systems, and mission-specific gear. This often leads to loads that exceed the ideal standard for combat. Recent high-intensity conflicts have shown that overloaded soldiers move more slowly, tire quickly, and become more vulnerable. As a result, militaries are working on developing lighter, modular, and better-balanced load carriage solutions to improve survivability and combat effectiveness without depending on new technologies.

In June 2023, NATO defense officials pointed out key lessons from the Ukraine conflict. They noted that dismounted soldier mobility and endurance are significant capability gaps in talks about modernizing allied forces. This underscores the need for lighter equipment and improved load management systems, according to NATO and IISS assessments.

MARKET RESTRAINTS

Budget Trade-offs and Procurement Cycles Limit Rapid Adoption Restrains Market Growth

Despite clear operational requirements, the adoption of advanced military load carriage systems is often held back by budget trade-offs and slow procurement cycles. Defense ministries usually focus on major platforms, such as vehicles, aircraft, and missiles, which leaves soldier-borne equipment competing for limited funding. Even when performance gaps are recognized, upgrades to load carriage systems are often postponed or implemented in stages, especially in Europe and emerging regions. This delays fleet-wide replacement and favors gradual upgrades over quick, large-scale adoption, stifling the military Load Carriage Systems (LCS) market growth.

MARKET OPPORTUNITIES

Infantry Modernization Programs Open Long-Term Upgrade Cycles and Fuel Market Growth

A significant opportunity in the market arises from ongoing and future infantry modernization initiatives, especially in Europe and NATO-aligned forces. As armies update soldier systems to include new radios, sensors, power management units, and body armor, load carriage is now viewed as part of a larger soldier ecosystem rather than standalone equipment. This change creates long-term, multi-phase upgrade cycles. Modular carriers, packs, and pouches can gradually improve and be standardized across units, leading to steady demand instead of one-time purchases.

In March 2024, several European armed forces confirmed multi-year soldier system modernization plans in official defense planning documents. The IISS noted that upgrades to load carriage and personal equipment regularly accompany communications and protective gear programs.

MARKET CHALLENGES

Balancing Weight Reduction with Protection and Long-Term Durability is a Major Obstacle

A key challenge is finding ways to reduce weight without sacrificing protection, durability, or mission reliability. Lighter materials and laser-cut laminates can boost mobility, however they must also endure tough conditions, heavy loads, and extended combat use. Militaries tend to be careful about adopting systems that reduce weight but may increase concerns about wear, tear, or lowered protection, resulting in long testing and qualification processes. This struggle between innovation and trust on the battlefield delays the quick adoption of new designs.

Impact of Russia Ukraine War

Russia-Ukraine War Exposes Infantry Load and Mobility Gaps, Accelerating Load Carriage Modernization

The Russia-Ukraine war has sharply highlighted the need for dismounted infantry to be more survivable, enduring, and mobile. This directly affects the demand for modern load carriage systems. Prolonged trench warfare, urban combat, and intense infantry operations have showcased soldiers carrying heavy loads for long periods, often in difficult environments. Observations from the conflict, outlined by IISS and noted in European defense reviews, emphasize the need for better weight distribution, modular designs, and compatibility with body armor, radios, and power systems. As a result, European militaries, viewing Russia as part of the regional threat, have sped up reviews of soldier equipment. They are prioritizing smaller upgrades to load carriage systems as a quicker, affordable way to improve frontline effectiveness compared to large equipment purchases.

Segmentation Analysis

By Component

Pouches & Accessories Highly Preferred Owing to Modularity and Frequent Replacements

In terms of component, the market is categorized into on‑body platforms, packs & frames, pouches & accessories, and hydration & load‑transfer add‑ons.

Pouches & accessories are the top choice due to their modularity, easy reconfiguration, and are the regularly replaced parts of a soldier’s kit. Unlike essential items such as plate carriers or packs, pouches are frequently adjusted for various mission types, weapon systems, and electronic devices. Combat operations and training cycles wear them out quickly, leading to constant demand. Their compatibility with different vests and belts also makes them easier to purchase in bulk, particularly during rapid force expansions or readiness upgrades.

In May 2023, European defense forces increased their purchases of modular infantry accessories, such as ammunition and utility pouches. This decision follows lessons learned from the Ukraine conflict. It is part of their strategy for quick readiness and replenishment, based on defense equipment assessments from IISS and reports from European Ministries of Defense.

The hydration & load‑transfer add‑ons segment in the market is expected to grow at a CAGR of 7.3% over the forecast period.

By Material

Nylon Webbing Leads Owing to its Durability and Cost-Effectiveness

On the basis of material, the market is classified into nylon webbing, laser‑cut laminate, hybrid (reinforced textiles), and metal/composite frames.

Nylon webbing leads the market with the largest military Load Carriage Systems (LCS) market share as it offers a strong combination of strength, durability, flexibility, and cost. Militaries value nylon for its ability to resist abrasion, moisture, and repeated load stress in various climates, from jungles and deserts to urban areas. It is also easy to produce, repair, and work with existing MOLLE/PALS standards. This makes it the preferred material for pouches, straps, and belts in most armed forces. These practical advantages keep nylon webbing important for both older systems and modern updates.

The laser‑cut laminate segment is expected to show fastest growth at a CAGR of 11.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Procurement channel

Direct to MoD Procurement Dominates Due to Standardization and Long-Term Force Planning

Based on procurement channel, the market is segmented into, prime contractor, direct to MoD, and framework/standing offer.

Direct procurement by Ministries of Defence is the highest as load carriage equipment is closely related to soldier safety, standardization, and interoperability. Most armed forces prefer to buy these systems centrally to maintain uniform specifications, compatibility with body armor and communications gear, and consistent quality across units. Direct MoD contracting also helps with long-term force planning, lifecycle management, and controlled upgrades over fragmented, unit-level purchasing.

The framework/standing offer is the fastest growing segment at a CAGR of 7.6% across the forecast period.

By End User

Army is the Leading End User Due to Large Dismounted Force Size and Steady Operational Requirements

Based on end user, the market is segmented into army, marines, special operations, and others.

The army segment is at the forefront of the market as it has the most dismounted personnel and engages in a wide range of combat and support missions. Infantry and mechanized units rely on load carriage systems for their daily training, deployments, and ongoing ground operations. This dependence results in higher usage, faster wear, and more frequent replacements compared to other services. Continuous efforts to modernize land forces reinforce the Army’s position, as soldier safety and mobility remain key priorities.

The special operations segment is expected to show the fastest growth rate of 9.1% over the forecast period.

Military Load Carriage Systems (LCS) Market Regional Outlook

North America Dominates with High Defense Spending and Continuous Soldier Modernization

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and the rest of the world (Africa and Latin America).

North America

North America Military Load Carriage Systems (LCS) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 2.38 billion in 2025, representing 39.92% of the global market landscape, and is expected to reach USD 2.51 billion in 2026. The market is the leader in the global Military Load Carriage Systems (LCS) market driven by ongoing defense spending and steady investment in soldier modernization programs, particularly in the U.S. The region has a significant number of active and reserve ground forces, long training cycles, and frequent overseas deployments. These elements generate a constant need for load carriage equipment. Instead of making occasional purchases, North American programs emphasize regular upgrades, quick deployment, and the integration of new communication and protective systems, which consistently maintains high demand.

U.S. Military Load Carriage Systems (LCS) Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.93 billion in 2025, increasing at a CAGR of 5.0% over the ensuing period.

Europe

Europe contributed 29.56% to the global market in 2025, with a valuation of USD 1.76 billion, and is projected to reach USD 1.89 billion in 2026. The region is projected to have a CAGR of 5.3% over the forecast timeframe. This growth is fueled by modernization efforts and a renewed focus on land-force readiness. Ongoing security pressures have pushed European armies to improve tactical gear to enhance soldiers’ performance during long dismounted operations. There is a stronger emphasis on enhancing soldier mobility through lightweight materials, modular load bearing solutions, and ergonomically designed systems that reduce fatigue.

U.K. Military Load Carriage Systems (LCS) Market

In 2025, the U.K. reached approximately USD 0.07 billion, equivalent to around 8.31% of Europe’s industry revenues.

Germany Military Load Carriage Systems (LCS) Market

Germany’s market size reached USD 0.10 billion in 2025, representing roughly 11.99% of Europe’s revenues.

Asia Pacific

Asia Pacific accounted for USD 1.26 billion in 2025, representing 21.16% of the global market share, and is projected to reach USD 1.34 billion in 2026. Asia Pacific is the third largest market and is anticipated to witness fastest growth at a CAGR of 7.9%. The region is observing an increase in the use of modern load carriage systems as militaries grow and professionalize their ground forces. Higher defense budgets and large infantry units are creating a demand for load bearing, lightweight systems that improve endurance in various terrains such as jungles, mountains, and urban areas. Countries in the region are making tactical gear upgrades a priority in their soldier modernization programs. They are focusing on equipment designed for comfort to enhance soldier performance during long patrols and internal security operations. The market is experiencing steady growth as militaries choose established technologies over major redesigns.

China Military Load Carriage Systems (LCS) Market

China’s market is projected to be one of the largest in Asia Pacific, with 2025 revenues hitting USD 0.23 billion, representing roughly 32.96% of Asia Pacific’s sales.

India Military Load Carriage Systems (LCS) Market

In 2025, India captured USD 0.13 million, accounting for roughly 18.60% of Asia Pacific’s revenues.

Rest of the World

In 2025, the Rest of the World market stood at USD 0.56 billion, representing 9.36% of global demand, and is projected to grow to USD 0.58 billion in 2026. The rest of the world (Middle East & Africa and Latin America) has a comparatively smaller share and is anticipated to grow at a CAGR of 6.8% over the forecast period. Market trends are driven by operational demand instead of extensive local development. Armed forces in the Middle East and parts of Africa focus on durable, load-bearing tactical gear that can endure harsh climates while enhancing soldier mobility during counter-insurgency and border security missions. On the other hand, Latin American forces emphasize affordability and modularity. They are slowly adopting lightweight materials and ergonomically designed systems through phased procurement.

Middle East & Africa Military Load Carriage Systems (LCS) Market

The Middle East & Africa’s market size achieved USD 0.28 billion in 2025, and is expected to reach USD 0.50 billion in 2034, representing roughly 82.62% of the rest of the world’s sales.

Latin America Military Load Carriage Systems (LCS) Market

Latin America reach USD 0.06 million in 2025, accounting for roughly 17.38% of rest of the world’s revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape is defined by Specialized Manufacturers and Ongoing Soldier-Centric Improvements

The market’s competitive landscape includes many specialized defense and tactical gear manufacturers along with large prime contractors. Companies compete based on proven durability, adherence to military standards, and established relationships with defense ministries. Performance and reliability tested in battle are more important than design changes, showcasing cautious approach taken in soldier equipment procurement.

Competition relies more on improvements in modularity, lightweight materials, and ergonomic load bearing systems that enhance soldier mobility and operational endurance. Vendors work on refining tactical gear to support modernization efforts, ensuring compatibility with body armor, communications, and power systems. This steady, evolutionary approach helps suppliers meet operational needs while dealing with long procurement cycles and cautious military buyers.

LIST OF KEY MILITARY LOAD CARRIAGE SYSTEMS (LCS) COMPANIES PROFILED

- Point Blank Enterprises, Inc. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Safariland Group (U.S.)

- Eagle Industries (U.S.)

- Mehler Protection GmbH (Germany)

- NFM Group (Norway)

- Source Tactical Gear (Israel)

- Crye Precision LLC (U.S.)

- FirstSpear LLC (U.S.)

- Blackhawk (U.S.)

- UF PRO (Slovenia)

- KDH Defense Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: The Canadian Army awarded Logistik Unicorp a contract valued at ~USD 14.6 million to supply modernized load carriage and protective equipment under the Dismounted Infantry Capability Enhancement (DICE) program, covering vests, packs, and modular accessories.

- November 2024: Public Services and Procurement Canada approved multiple suppliers to deliver trial samples of next-generation load-bearing vests, modular pouches, and integrated soldier equipment as part of the DICE modernization and evaluation phase.

- August 2024: The UK Ministry of Defence issued a re-competition notice for the VIRTUS integrated soldier system torso sub-system, covering body armor and load carriage components to support long-term infantry modernization.

- July 2024: Galvion received a follow-on order valued at ~USD 16 million to supply additional Batlskin helmet systems for the Canadian Army’s DICE program, reinforcing continued investment in integrated soldier systems alongside load carriage upgrades.

- April 2024: European NATO members highlighted infantry load management and mobility improvements as near-term priorities in defense readiness updates, accelerating demand for lightweight and modular load carriage equipment.

- February 2021: The U.S. Army kept distributing the Modular Scalable Vest (MSV) to active combat units. This was part of its Soldier Lethality and Protection modernization effort, which displayed a steady need for modular load carriage and plate carrier systems.

- July 2021: The German Bundeswehr moved forward with procurement under its Infanterist der Zukunft Erweitertes System (IdZ-ES) program. This program includes improved load-bearing and modular carriage components that work with communications and protection systems.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component

|

|

By Material

|

|

|

By Procurement channel

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.03 billion in 2026 and is projected to reach USD 4.86 billion by 2034.

In 2025, North Americas market value stood at USD 0.99 billion.

The market is expected to exhibit a CAGR of 6.1% during the forecast period of 2026-2034.

By Component, the pouches & accessories segment leads.

Rising soldier load and mobility gaps drive modernization spending and market growth.

Point Blank Enterprises, L3Harris Technologies, Safariland Group, Eagle Industries, Crye Precision, FirstSpear, Mehler Protection, NFM Group, UF PRO, KDH Defense Systems, and Blackhawk, are some of the top companies in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us