Military Protection Helmet Market Size, Share & Industry Analysis, By Material (Ballistic, Thermoplastic, and Metal), By End User (Law Enforcement Agencies and Military), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

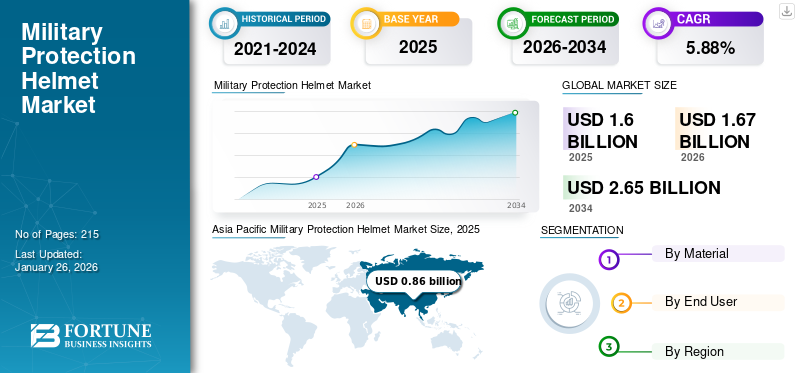

The global military protection helmets market size was valued at USD 1.60 billion in 2025. The market is projected to grow from USD 1.67 billion in 2026 to USD 2.65 billion by 2034, exhibiting a CAGR of 5.88% during the forecast period. North America dominated the military protection helmet market with a market share of 22.66% in 2025.

Military protection helmets, also known as ballistic helmets, are specialized headgear designed to safeguard soldiers from ballistic threats, shrapnel, and blunt impacts during combat. They are typically made from advanced materials such as Kevlar, UHMWPE, and composite fibers, providing lightweight yet durable protection. Modern helmet systems include features such as enhanced impact absorption, modular accessory mounts, and integrated communication systems.

The growth of market is driven by rising global military expenditure, increasing threats from modern warfare (e.g., IEDs and ballistic threats), and advancements in lightweight materials for improved soldier mobility. The integration of smart technologies such as augmented reality displays and communication systems enhances operational efficiency, further boosting demand. Additionally, the need for multi-functional helmets capable of supporting night vision devices and other attachments contributes to their adoption.

Key players in the market such as ArmorSource LLC manufactures advanced ballistic helmets for military and law enforcement, for the U.S. Army and global clients. Moreover, Armor Express headquartered in the U.S., and BAE systems specializes in protective equipment, including helmets, focusing on durability and comfort for law enforcement and military personnel. In addition, all other key players are investing heavily in next-generation combat helmets tailored according to the military needs.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine War

The ongoing conflict between Russia and Ukraine has significantly increased the demand for advanced combat helmets, primarily due to the heightened need for soldier safety in intense combat environments. The war has underscored the importance of protective gear, such as ballistic helmets, in reducing casualties and enhancing operational effectiveness.

The conflict has exposed soldiers to a high risk of ballistic threats, including bullets and shrapnel. Advanced combat helmets, designed to provide superior protection against these hazards, have become essential for military forces. The helmets safeguard against penetrating injuries and also integrate modern technologies such as night vision devices and communication systems, further enhancing their utility in combat scenarios.

The Russia-Ukraine conflict has prompted a global shift in defense priorities, with many countries focusing on bolstering their military capabilities. This includes investing in advanced protective equipment, such as combat helmets, to ensure soldier safety and operational readiness. For instance, in 2025, Ukraine's Ministry of Defense approved 10 models of combat ballistic helmets that meet the highest international protection standards, including six full-size and four high-cut helmets, to enhance soldier safety in the Armed Forces and State Special Transport Service. These helmets, provided by Ukrainian and Bulgarian manufacturers, offer Level 1 protection and can be equipped with modern mounts for night vision devices and communication systems. The conflict has also led to increased defense spending, with nations seeking to enhance their military preparedness in response to evolving security threats. Therefore, owing to all such factors, the military protection helmet industry is expected to grow significantly.

Global Military Protection Helmets Market Overview

Market Size & Forecast

- 2025 Market Size: USD 1.60 billion

- 2026 Market Size: USD 1.67 billion

- 2034 Forecast Market Size: USD 2.65 billion

- CAGR: 5.9% from 2026–2034

Market Share

- Asia Pacific accounted for the largest share of the market in 2024, supported by high defense budgets in China, India, and South Korea and ongoing soldier modernization programs across the region. Local manufacturing initiatives and advancements in lightweight materials such as UHMWPE further strengthen market growth.

- By material, the ballistic segment dominated the market due to its lightweight, high-strength properties and rising use in protective gear. By end user, the military segment led the market, driven by large-scale modernization programs and increased procurement of helmets with integrated technologies such as night vision and communication systems.

Key Country Highlights

- United States: Leads the North American market due to significant defense budgets, modernization programs, and the presence of leading manufacturers like Gentex Corporation and Revision Military. The focus on integrating night vision, AR systems, and improved shock absorption technologies further boosts growth.

- Europe: Growing demand fueled by NATO standardization and the Russia-Ukraine conflict, prompting procurement of advanced ballistic helmets by Eastern European nations and investments in interoperable helmet technologies.

- Asia Pacific: Rapidly growing market driven by border tensions, modernization programs in India and China, and local initiatives for lightweight, cost-effective ballistic helmets compatible with next-gen combat systems.

- Middle East & Africa: High defense expenditure in Saudi Arabia, UAE, and Israel for protective gear suitable for extreme conditions, with modular helmet designs in demand for varied mission profiles.

MILITARY PROTECTION HELMET MARKET TRENDS

Technology Integration and Lightweight Materials

A prominent trend in the market is the incorporation of cutting-edge technologies such as built-in communication systems, night vision compatibility, and Augmented Reality (AR) displays. These enhancements improve situational awareness, coordination, and operational effectiveness for soldiers on the battlefield. At the same time, manufacturers are focusing on using lightweight, high-strength materials such as advanced composites and ballistic fibers to reduce helmet weight without compromising protection. Therefore, the design and manufacturing of military protection helmets with advanced technologies and innovative materials is expected to drive the growth of the market.

- Asia Pacific witnessed military protection helmets market growth from USD 766.1 Million in 2023 to USD 8.11.4 Million in 2024.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Lightweight Combat Helmets in Military Operations to Boost Market

The increasing demand for lightweight combat helmets is driven by their ability to reduce soldier fatigue while maintaining high levels of ballistic and fragmentation protection. Modern lightweight helmets, such as the Advanced Combat Helmet Generation II and the Next-Generation Integrated Head Protection System (NG-IHPS), use advanced materials such as Ultra-High-Molecular-Weight Polyethylene (UHMWPE) to offer superior protection with significantly reduced weight. These helmets enhance soldier mobility and operational effectiveness during prolonged missions, making them essential for modern warfare scenarios. Additionally, their compatibility with integrated technologies such as night vision systems and communication devices further boosts their adoption in military operations.

MARKET RESTRAINTS

High Development Cost and Supply Chain Complexities to Limit Market Expansion

High development costs are a significant restraint for the military helmet market. The integration of advanced technologies, such as communication systems and night vision devices, increases the cost of production. Additionally, the use of specialized materials such as Kevlar and UHMWPE adds to the expense. These materials are often sourced from limited suppliers, which can lead to supply chain vulnerabilities. Geopolitical tensions and manufacturing bottlenecks can disrupt the supply of these critical materials. Logistical challenges in transporting and storing these materials further complicate the production process. As a result, manufacturers face increased costs and operational risks, which can limit market growth. This complexity makes it challenging for smaller manufacturers to enter the market, affecting overall competition and innovation.

MARKET OPPORTUNITIES

Integration of Military Protection Helmets in Autonomous Systems to Positively Impact Market Growth

The rising defense spending and military modernization programs present a significant opportunity for the military helmet market. As nations prioritize enhancing their military capabilities in response to evolving security threats, there is a growing demand for advanced protective gear, including combat helmets. These modernization efforts often involve substantial government budgets allocated for the procurement of state-of-the-art equipment that meets contemporary warfare requirements. Moreover, the focus on soldier safety and operational effectiveness drives the need for helmets equipped with integrated technologies, such as communication systems and night vision capabilities. This trend boosts sales for manufacturers and also encourages innovation in helmet design and materials. All such factors present significant opportunities for the growth of the market during the forecast period.

Segmentation Analysis

By Material

Ballistic Segment Dominated Market Owing to its Lightweight, Strength, and Versatility

By material, the market is segmented into ballistic, thermoplastic, and metal.

Ballistic materials dominate the market due to their exceptional combination of lightweight, high-strength, and impact-resistant properties, making them ideal for manufacturing protective gear such as helmets, body armor, and vehicle protection. The growth of the segment is driven by increasing defense spending, rising global security concerns, and the need for advanced protective equipment for the military.

- For instance, in February 2025, MKU Limited successfully delivered its innovative Kavro Doma 360 ballistic helmets to the Indian Army, marking a significant milestone in enhancing soldier protection. The helmet offers uniform protection against threats such as AK-47 bullets and features a low-back face signature, reducing the risk of head trauma.

By End User

Military Segment Leads Due to Soldier Modernization Programs and Increased Defense Spending

By end user, the market is segmented into law enforcement agencies and military.

Military is the largest and fastest growing segment in the market due to ongoing soldier modernization programs aimed at equipping troops with advanced protective gear that enhances safety and operational efficiency. Additionally, increased defense spending by countries worldwide to address rising geopolitical tensions and evolving security threats has driven the demand for state-of-the-art military helmets. These helmets integrate advanced technologies such as communication systems, night vision devices, and augmented reality displays, further boosting their adoption.

Military Protection Helmet Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Military Protection Helmet Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 0.36 billion in 2025 and is projected to reach USD 0.38 billion in 2026. The growth of the market in North America is driven by significant defense budgets and ongoing modernization programs in the United States and Canada. The U.S. Department of Defense prioritizes equipping soldiers with advanced helmets that integrate cutting-edge technologies such as night vision systems, communication devices, and augmented reality displays. The region also benefits from the presence of leading manufacturers such as Gentex Corporation and Revision Military, which focus on innovative helmet designs using lightweight materials such as Kevlar and UHMWPE. Additionally, increasing emphasis on mitigating Traumatic Brain Injuries (TBIs) during combat has led to the adoption of helmets with enhanced shock absorption capabilities. Rising geopolitical tensions and the need for advanced protective gear for special operations further bolster market demand.

Europe

Europe contributed 18.14% to the global market in 2025, with a valuation of USD 0.29 billion, and is projected to reach USD 0.3 billion in 2026. In Europe, the market is expanding due to growing defense spending, particularly in response to the Russia-Ukraine conflict. Eastern European countries are rapidly procuring modern helmets to enhance soldier safety amid rising security threats. NATO’s standardization initiatives have also driven demand for interoperable helmets compatible with communication systems and other battlefield technologies. European manufacturers such as Schuberth GmbH and Revision Military are investing in lightweight, high-performance helmets tailored for diverse combat scenarios. Additionally, government-backed procurement programs ensure faster adoption of advanced protective gear across EU member states. The integration of smart features such as threat detection sensors further supports advanced global combat helmet market growth in this region.

Asia Pacific

Asia Pacific accounted for USD 0.86 billion in 2025, representing 53.17% of the global market share, and is projected to reach USD 0.89 billion in 2026. Asia Pacific accounted for the largest market share and is witnessing rapid growth in the market due to increasing defense budgets in China, India, South Korea, and Japan. Ongoing border disputes and regional security challenges drive demand for modern protective gear to safeguard soldiers in high-risk environments. India’s military modernization programs include large-scale procurement of lightweight ballistic helmets compatible with night vision devices and communication systems. China is focusing on indigenously producing cost-effective yet durable helmets using advanced materials such as UHMWPE. South Korea emphasizes technological enhancements such as augmented reality integration for improved situational awareness. Local manufacturing initiatives across the region reduce dependency on imports while supporting market expansion.

Middle East & Africa

In 2025, Middle East & Africa held 4.17% of the global market, reaching a valuation of USD 0.07 billion, and is projected to grow to USD 0.07 billion in 2026. The Middle East market is fueled by high defense spending driven by geopolitical instability and counterterrorism operations. Saudi Arabia, the UAE, and Israel are investing heavily in modernizing their armed forces with state-of-the-art protective equipment. Helmets designed for extreme desert conditions with heat-resistant materials are particularly favored in this region. Modular designs that allow customization based on mission requirements, such as integrating communication or night vision systems, are in high demand. Partnerships with global manufacturers enable access to advanced technologies while fostering local production capabilities to meet growing regional needs.

Latin America

Latin America contributed approximately USD 0.03 billion to the global market in 2025, accounting for 1.86% share, and is expected to reach USD 0.03 billion in 2026. In Latin America, the growth of the market is supported by increasing investments in homeland security and law enforcement modernization programs. Brazil, Colombia, and Mexico are procuring ballistic helmets for military forces engaged in counterinsurgency operations and border security missions. Lightweight designs compatible with communication systems are prioritized to enhance mobility during jungle warfare scenarios.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations and Technological Advancements by Key Companies Resulted in their Dominating Position

The military protection helmet market is dominated by key industry players who have established themselves through strategic innovations and technological advancements. These companies focus on developing helmets with advanced materials such as Kevlar and UHMWPE, ensuring both lightweight and high-strength protection. Integration of modern technologies such as communication systems and night vision devices further enhances their market position. Strong research and development investments allow these companies to address evolving soldier safety needs effectively. Their global reach and strategic partnerships with defense agencies ensure consistent supply and adoption of their products.

LIST OF KEY MILITARY PROTECTION HELMET COMPANIES PROFILED

- ArmorSource LLC (U.S.)

- Armor Express (U.S.)

- Avon Rubber p.l.c. (U.K.)

- BAE System (U.K.)

- Indian Armour System Pvt Ltd (India)

- MKU Limited (India)

- Morgan Advanced Material (U.K.)

- Honeywell International Inc. (U.S.)

- Point Blank Enterprises Inc. (U.S.)

- DuPont de Nemours Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: ArmorSource secured a USD 18.6 million contract from the U.S. Defense Logistics Agency to deliver up to 30,000 ultra-lightweight CREW II Advanced Combat Vehicle Crewman (ACVC) helmets over five years, following a successful delivery of 14,000 units.

- March 2025: Leading Technology Composites (LTC) has been awarded an USD 856.7 million contract by the U.S. Army to produce 406,384 Next Generation Integrated Head Protection Systems (NG IHPS) and night vision device brackets. The NG IHPS offers enhanced protection against handguns, moderate rifles, and fragmenting munitions.

- February 2025: MKU Limited delivered its Kavro Doma 360 ballistic helmet to the Indian Army, offering lightweight, all-weather protection against high-calibre threats such as AK-47 and NATO rounds, with a back face signature under 20 mm for reduced trauma.

- February 2023: The U.S. Defense Logistics Agency awarded a second contract to Avon Rubber p.l.c. to supply second-generation Advanced Combat Helmet contract SPE1C1-22-D-1516. The total contract was valued at around USD 6.7 million.

- February 2023: The U.S. Army awarded a contract to ArmorSource LLC. to deliver 14,000 Advanced Combat Vehicle Crewman Helmets (ACVC-H). The agreement was valued at around USD 6 million.

REPORT COVERAGE

The global military protection helmet market research report provides an in-depth technical analysis of the market, covering its size, growth trends, and future projections. The global market is characterized by its growing size and technological advancements. The market is valued at significant figures and is projected to expand further due to ongoing modernization efforts and increasing defense budgets worldwide. Key players in the industry focus on developing helmets with advanced materials and integrated technologies, enhancing soldier safety and operational efficiency.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.88% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.60 billion in 2025 and is projected to record a valuation of USD 2.65 billion by 2034.

The market is expected to exhibit a CAGR of 5.88% during the forecast period of 2026-2034.

The military segment led the market by end user.

The key factor driving the market is the growing demand for lightweight combat helmets in military operations.

ArmorSource LLC, Armor Express, Avon Rubber p.l.c. are the top players in the market.

Asia Pacific region dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us