Mobile Phone Semiconductor Market Size, Share & Industry Analysis, By Component (Processors & SoCs, Baseband & RF Chips, Connectivity ICs, Memory & Storage, Power & Analog ICs, and Others), By Technology Node (Advanced (≤10 nm, incl. 5 nm/3 nm), Mature (16–65 nm), and Legacy (≥90 nm)), By Device Type (Smartphones, Feature Phones, and Others), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

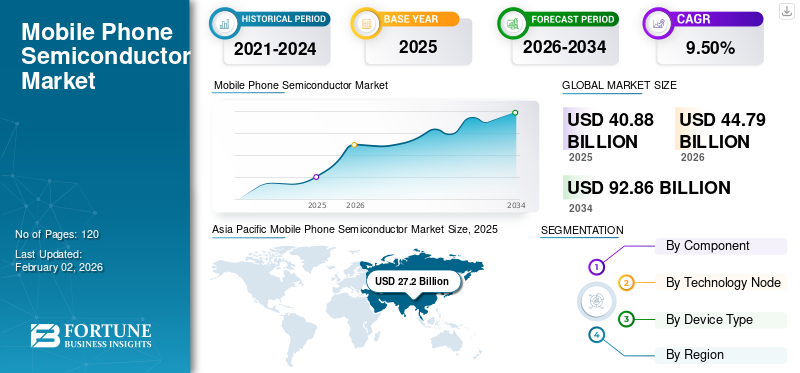

The global mobile phone semiconductor market size was valued at USD 40.88 billion in 2025 and is projected to grow from USD 44.79 billion in 2026 to USD 92.86 billion by 2034, exhibiting a CAGR of 9.50% during the forecast period. Asia Pacific dominated the global market with a share of 66.50% in 2025.

The mobile phone semiconductor market comprises the design, manufacturing, and supply of integrated circuits and components that power smartphones, feature phones, and other mobile devices. These semiconductors include processors & SoCs, baseband & RF chips, connectivity ICs, memory & storage, power & analog ICs, and others, which are essential for device functionality, performance, and connectivity. The continuous innovations in semiconductor process nodes, packaging technologies, and energy-efficient designs, along with strong demand across emerging economies, position this market as a critical enabler of the global mobile ecosystem.

- For instance, in August 2025, the Council for Scientific and Industrial Research launched the Opto Microelectronic Research Centre at CSIO, Chandigarh, to advance semiconductor-based display and optical technologies for strategic and commercial sectors. The semiconductor industry, valued at USD 627 billion in 2024, is projected to reach USD 697 billion in 2025 and USD 1 trillion by 2030.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

5G Expansion Accelerates Demand for Advanced Mobile Phone Semiconductors

The global expansion of 5G technology is a major driver of the mobile phone semiconductor market growth, creating higher demand for cutting edge processors, RF chips, and connectivity solutions to deliver faster speeds and lower latency.

- According to 5G Americas, global 5G connections surpassed 2.25 billion in 2024.

Smartphone makers are responding by adding stronger baseband modems and multi-band antennas that can handle different 5G spectrums. This shift increases the amount of mobile phone semiconductor content in each device while improving power efficiency and processing performance. In addition, 5G is enabling new applications such as AR/VR, ultra-HD video streaming, and cloud gaming, further boosting the need for high-performance mobile phone semiconductors.

MARKET RESTRAINTS

Supply Chain Challenges and Rising Costs Constrain Market Growth

The market faces restraints due to supply chain vulnerabilities, including shortages of raw materials and heavy reliance on limited manufacturing hubs in Asia. The high cost of developing advanced nodes such as 3 nm and 2 nm also restricts wider participation, leaving only a few players able to invest at this scale. In addition, market saturation in developed regions is slowing smartphone replacement cycles, reducing the pace of mobile phone semiconductor demand growth. Furthermore, the rising complexity of integrating multi-band 5G, AI processing, and advanced memory increases production challenges, leading to higher costs and risks of delays.

MARKET OPPORTUNITIES

6G, AI-Enabled Devices, and Emerging Markets Unlock Growth Potential

The market presents strong opportunities with the upcoming development of 6G technology, which will further increase demand for advanced processors and RF solutions.

- For instance, IDTechEx forecasts that 6G technology will begin to emerge around 2028, with full commercialization expected by 2030.

Growing adoption of AI-enabled smartphones is creating new requirements for on-device intelligence, driving demand for powerful SoCs and neural processing units. Expanding use cases such as AR/VR, IoT integration, satellite connectivity, and ultra-HD mobile experiences are expected to boost mobile phone semiconductor innovation and adoption. In addition, emerging markets with rising smartphone penetration provide significant growth potential, further expanding the mobile phone semiconductor market share.

MARKET TRENDS

Shift toward Advanced Nodes and Integrated SoCs Shapes Market Evolution

A major trend in the market is the shift toward advanced nodes such as 5 nm and 3 nm, with companies investing heavily in next-generation process technologies. This transition enables higher performance, lower power consumption, and support for AI-driven and 5G-enabled applications. Another notable trend is the growing integration of multiple functions into system-on-chips (SoCs), reducing device size while enhancing efficiency. In parallel, demand for specialized chips such as AI accelerators, image signal processors, and connectivity ICs is rising as smartphones evolve into multifunctional, high-performance devices. For instance,

- In 2025, the global smartphone user base reached nearly 7.42 billion, driven by devices featuring AI-powered functions, foldable displays, and 5G connectivity.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Processors & SoCs Dominate as Core of Mobile Phone Semiconductors

Based on component, the market is divided into processors & SoCs, baseband & RF chips, connectivity ICs, memory & storage, power & analog ICs, and others.

Processors & SoCs segment is expected to lead the market, contributing 38.55% in 2026, as they integrate critical functions such as CPU, GPU, AI, and connectivity, making them essential for advanced smartphone performance.

Baseband & RF Chips hold the second-largest share as 5G and upcoming 6G rollouts require complex modems and RF front-end modules to enable high-speed, multi-band connectivity.

By Technology Node

Advanced Nodes (≤10 nm) lead Market with Highest Growth Potential

Based on technology node, the market is divided into advanced (≤10 nm, incl. 5 nm/3 nm), mature (16–65 nm), and legacy (≥90 nm).

Advanced (≤10 nm, incl. 5 nm/3 nm) segment is expected to lead the market, contributing 50.75% in 2026, due to increasing demand for high-performance, power-efficient chips in premium and AI-driven smartphones.

Mature (16–65 nm) holds the second-largest share as it is widely used for RF, power management, and connectivity ICs, which remain critical across both mid-range and low-end devices.

By Device Type

To know how our report can help streamline your business, Speak to Analyst

Smartphones Remain Largest and Fastest-Growing Segment

Based on device type, the market is divided into smartphones, feature phones, and others.

Smartphones segment is expected to lead the market, contributing 91.51% in 2026 and are expected to grow at the highest CAGR due to massive global adoption, premiumization trends, and rising demand for AI, 5G, and high-performance features.

Feature Phones hold the second-largest share as they still serve cost-sensitive markets and emerging economies, though their growth is relatively limited compared to smartphones.

Mobile Phone Semiconductor Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, Middle East & Africa, and Asia Pacific.

Asia Pacific

Asia Pacific Mobile Phone Semiconductor Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 27.2 billion, contributing 66.50% to global market revenue, and is projected to grow to USD 30 billion in 2026. It dominates due to the strong presence of leading foundries (TSMC, Samsung, and SMIC) and major smartphone OEMs (Samsung, Xiaomi, Oppo, and Vivo) concentrated in the region. In addition, rising consumer demand, large-scale manufacturing capacity, and government support for semiconductor ecosystems further strengthen its leadership. The Japan market is projected to reach USD 6.97 billion by 2026, the China market is projected to reach USD 8.7 billion by 2026, and the India market is projected to reach USD 5.71 billion by 2026.

North America

The North America region captured 15.60% of the global market in 2025, generating USD 6.38 billion in revenue, and is projected to reach USD 6.98 billion in 2026. The region benefits from strong R&D investments, advanced design capabilities, and demand from premium smartphone markets, with the U.S. being one of the largest consumers of high-performance mobile devices. The U.S. market is projected to reach USD 4.07 billion by 2026.

Europe

Additionally, Europe’s strength lies in its advanced semiconductor research, government-backed initiatives such as the EU Chips Act, and its role as a key supplier of semiconductor equipment and specialty materials. The UK market is projected to reach USD 1.03 billion by 2026, and the Germany market is projected to reach USD 0.88 billion by 2026. Europe maintained a strong presence in the global market, reaching USD 3.87 billion in 2025, accounting for 9.50% share, and is expected to reach USD 4.17 billion in 2026.

Middle East & Africa and South America

Middle East & Africa and South America are expected to grow more slowly in the market, with the CAGR of 6.8% and 5.6% respectively. This slow growth is due to lower smartphone penetration compared to mature markets and limited local semiconductor manufacturing infrastructure. Economic challenges, high import dependency, and slower rollout of advanced networks such as 5G further constrain growth. Middle East & Africa recorded a market size of USD 1.92 billion in 2025, capturing 4.70% of the global market share, and is projected to reach USD 2.05 billion in 2026.

Latin America

The Latin America market generated USD 1.52 billion in 2025, representing 3.70% of the global market landscape, and is expected to reach USD 1.59 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Products to Strengthen Market Positioning

Players launch new product portfolios to enhance their market positioning by leveraging technological advancements in mobile, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. Such strategic product launches help companies maintain and grow their market share in a rapidly evolving landscape.

LIST OF KEY MOBILE PHONE SEMICONDUCTOR COMPANIES PROFILED

- Samsung Electronics Co., Ltd. (South Korea)

- Qualcomm Technologies, Inc. (U.S.)

- MediaTek Inc. (Taiwan)

- Arm Holdings plc (U.K.)

- Skyworks Solutions, Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Broadcom Inc. (U.S.)

- Intel Corporation (U.S.)

- Micron Technology, Inc. (U.S.)

- Qorvo, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Intel Corporation announced senior leadership appointments to support its strategy of strengthening core products, building a trusted foundry, and enhancing engineering culture. Kevork Kechichian was appointed Executive VP and GM of the Data Center Group, leading Intel’s cloud and enterprise Xeon processor business.

- In August 2025, MediaTek announced the upcoming launch of the Dimensity 9500, strategically scheduled one day ahead of Qualcomm’s Snapdragon 8 Gen 2 Elite debut. This move highlights MediaTek’s competitive positioning in the high-end mobile chipset segment.

- In August 2025, Qualcomm Technologies announced the Dragonwing Q-6690 that features built-in Wi-Fi 7, 5G, Bluetooth 6.0, and UWB, supporting rugged handhelds, retail PoS, and smart kiosks with over-the-air upgradable software packs.

- In June 2025, Samsung introduced the Exynos 2500, its first chip manufactured using an advanced 3nm process technology. The launch represents a noteworthy upgrade, aimed at delivering improved performance, efficiency, and intelligence in next-generation smartphones.

- In May 2025, Qualcomm introduced the Snapdragon 7 Gen 4, a mid-range mobile chipset designed to bring flagship-level experiences to affordable smartphones. The chip offers enhanced performance, gaming optimization, and on-device AI, with devices from Honor and Vivo expected by the end of May 2025.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.50% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component · Processors & SoCs · Baseband & RF Chips · Connectivity ICs · Memory & Storage · Power & Analog ICs · Others (Sensors, etc.) |

|

By Technology Node · Advanced (≤10 nm, incl. 5 nm/3 nm) · Mature (16–65 nm) · Legacy (≥90 nm) |

|

|

By Device Type · Smartphones · Feature Phones · Others (Satellite Phones, etc.) |

|

|

By Region · North America (By Component, By Technology Node, By Device Type, and Region) o U.S. o Canada o Mexico · South America (By Component, By Technology Node, By Device Type, and Region) o Brazil o Argentina o Rest of South America · Europe (By Component, By Technology Node, By Device Type, and Region) o U.K. o Germany o France o Italy o Spain o Russia o Benelux o Nordics o Rest of Europe · Middle East & Africa (By Component, By Technology Node, By Device Type, and Region) o Turkey o Israel o GCC o North Africa o South Africa o Rest of the Middle East & Africa · Asia Pacific (By Component, By Technology Node, By Device Type, and Region) o China o India o Japan o South Korea o ASEAN o Oceania · Rest of Asia Pacific |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 40.88 billion in 2025 and is projected to reach USD 44.79 billion by 2034.

In 2025, the market value stood at USD 27.2 billion.

The market is expected to exhibit a CAGR of 9.50% during the forecast period.

The processors & SoCs led the market by component.

The mobile phone semiconductor market is driven by growing demand for advanced smartphones with 5G connectivity, AI-enabled processing, and higher memory and storage capacity to support applications such as gaming, imaging, and on-device intelligence.

Samsung Electronics Co., Ltd., Qualcomm Technologies, Inc., MediaTek Inc., and Arm Holdings plc are the top players in the market.

Asia Pacific dominated the global market with a share of 66.50% in 2025.

Key factors favoring adoption include 5G/6G rollout, AI-enabled smartphones, rising memory needs, and advanced features such as AR/VR, high-res imaging, and satellite connectivity.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us