Molluscs Market Size, Share & Industry Analysis By Type [Abalone (Live, Chilled, Frozen, Dried, Canned, and Abalone Meat), Mussels (Live, Cooked and Chilled, Frozen, Canned, Smoked, Pickled, and Mussel Meat), and Oysters (Live whole, Frozen, Smoked, Pickled, and Oyster Meat)], By Distribution Channel [Food Service (Bars and Cafes, and Restaurants), and Retail (Grocery Stores and Hypermarkets/Supermarkets, Independent Stores, and Others)], and Regional Forecast, 2026–2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

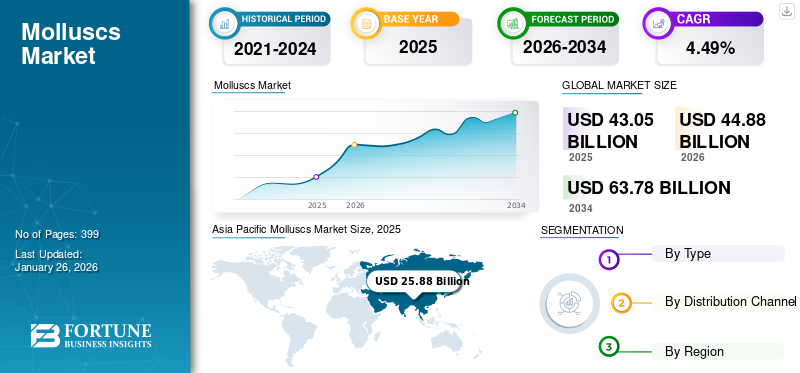

The global molluscs market size was valued at USD 43.05 billion in 2025 and is projected to grow from USD 44.88 billion in 2026 to USD 63.78 billion by 2034, exhibiting a CAGR of 4.49% during the forecast period. Asia Pacific dominated the molluscs market with a market share of 60.10% in 2025. Moreover, the U.S. molluscs market is projected to reach USD 5.31 billion by 2032, with growing demand for seafood across regions.

The global seafood market has experienced notable shifts in consumption patterns and production dynamics over the past decade. Per capita fish consumption has risen steadily from an average of 18.67 kg in 2010 to approximately 20.45 kg by 2020-2022 globally. Asia is the largest consumer, driven by its large population and cultural dietary preferences. Simultaneously, the market has faced challenges due to rising costs. The price of captured fish and seafood has recently surged from USD 1,568.3 per ton in 2007 to around USD 2,100 per ton in 2022, impacting market dynamics and consumer affordability.

The global COVID-19 pandemic significantly impacted the market with profound disruptions in supply chain, production, and consumption owing to the stringent lockdown and trade regulations implemented by governments across the world. As China is the largest producer and consumer of molluscs and was the epicenter of the COVID-19 spread, which started in Wuhan's seafood market, it experienced significant disruptions across its supply chain. These reports negatively influenced public perception, which affected global consumption pattern despite the virus not infecting aquatic plants.

The landscape of the molluscan shellfish market was reshaped by the pandemic. While short-term adaptations, such as diversifying sales channels and product offerings helped mitigate immediate impacts, the sector remained vulnerable to ongoing shifts in consumer behavior, regulatory responses, and global economic conditions. Restoring consumer confidence in seafood safety and resilience in supply chain logistics will be critical for revitalizing the market and supporting its sustainable growth.

Download Free sample to learn more about this report.

Molluscs Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 43.05 billion

- 2026 Market Size: USD 44.88 billion

- 2034 Forecast Market Size: USD 63.78 billion

- CAGR: 4.49% from 2026–2034

Market Share:

- Asia Pacific dominated the molluscs market with a 60.10% share in 2025, driven by high seafood production, cultural consumption habits, and strong aquaculture output.

- By type, oysters held the largest share in 2024 and are expected to grow fastest, supported by global demand for premium seafood and expanding aquaculture initiatives.

Key Country Highlights:

- United States: Expected to reach USD 5.31 billion by 2032, supported by strong seafood demand, high purchasing power, and expansion of sustainable aquaculture.

- China: As the largest producer and consumer, faced significant COVID-19-related disruptions but remains key to global molluscs supply.

- Japan: Demand remains strong due to cultural preferences for oysters and mussels in traditional cuisine.

- Canada: Leading oyster exporter; 46% of domestic oyster output comes from British Columbia, with growing retail and food service presence.

- Spain & Italy: Key European markets with strong demand for premium seafood; Italy leads in retail value sales.

- Chile & Peru: Major aquaculture producers in South America, supporting both domestic demand and exports.

- South Africa: Africa's leading farmed molluscs producer, particularly oysters and mussels, with expanding aquaculture efforts.

- U.A.E. & Qatar: Investing in oyster farming to reduce imports and support sustainable local production.

Molluscs Market Trends

Rising Consumption of Prepared, Packaged, and Premium Seafood to Contribute to Global Market Growth

Molluscs, such as abalone are considered premium seafood products and perceived as a luxury among individuals. The rise in disposable income in developing regions and increasing demand for premium seafood have further contributed to the growth of the market. For instance, in May 2024, Alila Hanu Bay, one of Oman's luxurious retreat award-winning restaurants, announced the launch of its much-awaited 'white gold' Omani Abalone luxurious dining.

The rapid growth of processed and packaged seafood production can be seen in the numbers where, in 2011, the production was just 56.26 million tons, which rose significantly to 62.92 million tons in 2021. Furthermore, the demand for prepared and preserved fish has shown significant growth in recent years in North American and European countries. This is due to the growing consumption of protein-rich diets and rising demand for processed, prepared, and shelf-stable foods.

Download Free sample to learn more about this report.

Molluscs Market Growth Factors

Substantial Growth of Aquaculture Industry to Support Market Expansion

The substantial growth of the aquaculture industry is one of the significant factors that has driven the global molluscs market growth. Global aquaculture production has expanded significantly since 2000 owing to the growing advancement in technology and increased seafood consumption. In addition, 2022 marked the first year in which the aquaculture production share surpassed capture fisheries production by 51%.

Molluscs, such as mussels, oysters, and abalone are prominent species farmed in aquaculture. As per the FAO, around 76 countries have established aquaculture production of this product. This type of seafood is highly sought after in various cuisines worldwide, driving its demand. Furthermore, aquaculture allows for controlled breeding and cultivation, ensuring a steady supply to meet this demand. For instance, as per the Food and Agriculture Organization, aquaculture is going to be a prominent contributor to the growth of the global seafood production.

The expansion of aquaculture in the last few decades has boosted the growth of production in inland waters. Furthermore, aquaculture has made molluscs more accessible and affordable compared to wild-caught varieties. This accessibility has expanded their market reach to regions where wild molluscs may be scarce or expensive.

Rapidly Growing Food Service Industry to Support Market Growth

The global food service industry has recorded rapid growth in recent years, which has been one of the significant factors supporting the market growth. The industry's substantial growth is owing to the subsequent rise in dining out and rapid advancement in the food delivery industry. Molluscs are known for their flavor, nutritional value, and versatility in culinary applications as they are protein-rich foods and also contain vital ingredients, such as vitamins, iron, omega-3 fatty acids, and minerals, making them attractive to health-conscious consumers.

In addition, as global culinary influences continue to merge, this type of seafood features prominently in both traditional and fusion cuisines, appealing to a broad range of tastes and preferences. For instance, as per the data published by Seafish, a public body based in the U.K. established to support the country’s seafood industry, the seafood foodservice industry recorded a growth of around 8.6% post-pandemic and is expected to show further growth with changing consumer demand and preferences.

RESTRAINING FACTORS

Changing Environmental Factors to Restrain Market Growth

Climate change indicators, such as rising temperature, ocean acidification, rising sea levels, and others have negatively influenced the aquaculture industry, including the molluscs industry. Rising temperature is one of the major factors contributing to the melting ice caps, which increases the sea level.

The increased sea levels further lead to changing ocean currents, which disturb the habitats and growth of this form of seafood. Rising sea levels can also submerge low-lying coastal areas, reducing suitable habitats for molluscs. The increasing acidification of the ocean is caused by the rising atmospheric level of carbon dioxide, which has a significant negative impact on ocean food chains, coral reefs, and molluscs as carbon dioxide absorption harms their shells and inhibits their growth. For instance, as per a report published by the FAO Fisheries & Aquaculture Department, the changing climatic conditions that lead to ocean warming, rising sea levels, and acidification of the sea are driving change in the world's fisheries and aquaculture sector.

Molluscs Market Segmentation Analysis

By Type Analysis

Rising Demand for Luxurious Seafood Fuels Consumption of Oysters

Based on type, the market is classified into abalone, mussels, and oysters.

The oysters segment is anticipated to hold a dominant market share of 28.88% in 2026 and is expected to record the fastest CAGR during the forecast period. The dominance of this segment is attributed to the high production volume and ever-increasing demand for oysters from various countries across the world. Oysters are highly prized as a seafood delicacy in many cuisines globally. They can be consumed in a variety of ways, such as raw on the half-shell, steamed, baked, grilled, fried, or incorporated into dishes, such as soups, stews, and seafood platters.

Mussels is the second-largest segment in the market. Mussels play a vital ecological role in aquatic ecosystems and are a valued food source for people. They are also a focus of aquaculture initiatives worldwide owing to their culinary desirability and nutritional properties. Abalone is a type of marine gastropod mollusc that belongs to the Haliotidae family. These creatures are known for their single, spiral-shaped shell that features a series of small openings along the outer edge.

Abalone can be found in coastal waters around the globe, primarily in temperate and tropical regions. They inhabit rocky shorelines and use their powerful muscular foot to stick to the rocks, which also allows them to move slowly.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel Analysis

Growing Demand from Food Service Industry for Premium Seafood Drives Market Growth

Based on distribution channel, the market is segmented into food service and retail.

The food service segment is anticipated to hold a dominant market share of 7.92% in 2026. Oysters are commonly associated with upscale dining and are popular items on the menus of high-end restaurants and seafood establishments. They are considered a luxury or gourmet choice that attracts patrons willing to pay a premium. Abalone, on the other hand, holds a special place in the food service industry due to its premium status, delicate flavor, and culinary versatility. While traditionally popular in Asian cuisines, particularly Chinese and Japanese, abalone has gained traction in international markets, such as North America and Europe, thereby expanding its presence in diverse culinary settings. With the food service industry expected to grow steadily in the coming years, this segment is poised to drive the market growth.

The retail segment dominates the molluscs market share due to their widespread availability across various retail channels and frequent use of seafood in household cooking. Mollusc products are sold in various forms, including fresh, frozen, canned, and value-added products, such as pre-cooked meals or sauces made from mollusc meat. Consumer demand for this form of seafood varies based on region and preferences, with factors, such as quality, freshness, sustainability, price, and convenience influencing purchasing decisions. In addition to fresh and frozen molluscs, there is a growing market for value-added products, such as mollusc-based soups, sauces, and ready-to-cook meals, catering to consumers seeking convenience.

REGIONAL INSIGHTS

With the impact of the COVID-19 pandemic almost diminished in late 2022, the dynamics of the global fishery products market started changing. Even though the market did not rebound exactly to its pre-pandemic levels, newly re-opened food service establishments, which were one of the major sources of demand, were once again available to seafood suppliers. This boosted the sales ominously in 2022.

Asia Pacific

Asia Pacific Molluscs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 25.88 billion to the global market in 2025, accounting for 60.10% share, and is expected to reach USD 26.99 billion in 2026. The region is the largest in terms of global fish production volume. According to the data published by the FAO in 2021, Asia produced 89% of the total global fish farming volume in the last 20 years. In terms of international trade, the oyster trade expanded steadily during 2021, even beyond 2019. Around 71,000 tons of oysters were imported in 2021, which was 15,000 tons higher than the 2020 imports and even 6,000 tons more than the 2019 imports. This was the result of robust oyster imports from the U.S. The U.S. was the key importer of oysters in 2021, ahead of France and Italy. These imports increased by nearly 30% during 2021. The Japan market is projected to reach USD 4.98 billion by 2026, the China market is projected to reach USD 11.42 billion by 2026, and the India market is projected to reach USD 2.23 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The U.S. is a major global importer of fish and seafood products while also being a key provider of feeds, technology, equipment, and investment capital to other producers around the world. Leveraging these strengths can help the country expand its sustainable aquaculture industry to meet the consumer's rising demand for fresh seafood. The American consumer base is well-positioned for increased seafood consumption, with the middle-class and upper-class segments having relatively high purchasing power. During the COVID-19 pandemic, consumers sought more affordable and conveniently available products, even through online shopping platforms. However, once the pandemic subsided, consumers returned to relying more on food service outlets. The U.S. market is projected to reach USD 4.07 billion by 2026. In 2025, North America held 10.63% of the global market share, reaching a valuation of USD 4.58 billion, and is projected to grow to USD 4.77 billion in 2026.

In Canada, the aquaculture production is primarily exported, with the U.S. being the largest market for farmed shellfish. British Columbia is a significant producer of oysters, accounting for 46% of Canada's oyster output. While the country’s total shellfish production reached 42,540 tons, valued at USD 122 million in 2021, the industry still has room for further growth. According to government data, Canada's fish and seafood imports have grown at a 4.5% compound annual rate from 2017 to 2021, reaching USD 4.6 billion in value, with the U.S. being the largest supplier. The processed fish product market in Canada has also seen significant new product launches, with a focus on ethical, sustainable, and user-friendly claims.

Europe

The European Union's total sales volume of fish and seafood was estimated to be around 3.8 million tons in 2023, representing a decrease of 1.4% annually during the 2018-2023 period. However, this volume is projected to increase by 1.3% per year between 2023 and 2028. Spain was the largest market by total sales volume, reaching 901,000 tons in 2023. Among the 19 EU member states included in the data, Italy had the highest retail value sales at USD 8.3 billion in 2023. The majority of EU member states are expected to experience positive growth during the forecast period. The UK market is projected to reach USD 0.47 billion by 2026, and the Germany market is projected to reach USD 1.02 billion by 2026. The market in Europe reached USD 6.68 billion in 2025, representing 15.52% of total market revenue, and is projected to reach USD 6.93 billion in 2026.

South America

South America is home to a wide variety of mollusc species, including different types of clams, mussels, oysters, scallops, and abalone. Each species may have unique cultivation or harvesting methods and distinct customer demands. The mollusc industry in South America encompasses both aquaculture and wild harvesting. Aquaculture practices have been developed for species, such as mussels, oysters, and scallops, with countries, including Chile, Peru, and Mexico being prominent producers. Wild harvesting of molluscs also takes place along the coastlines of many countries, providing a means of livelihood for local coastal communities.

Middle East & Africa

The seafood industry in the Middle East & Africa involves both aquaculture and wild harvesting practices. Aquaculture operations have been developed for species, such as oysters, mussels, and abalone, primarily in South Africa, Namibia, and Morocco. South Africa is one of the leading producers of farmed molluscs in Africa, particularly oysters and mussels. Other significant producers include Namibia, Morocco, Egypt, and Tunisia, where aquaculture operations are expanding to meet domestic demand and create lucrative export opportunities. The Middle East & Africa region captured 4.54% of the global market in 2025, generating USD 1.95 billion in revenue, and is projected to reach USD 2.04 billion in 2026.

Gulf countries heavily rely on imported oysters from nations with well-established oyster farming industries, such as France, Ireland, and Australia. This reliance is due to limited local production and high demand from affluent consumers. Some Gulf countries, particularly the U.A.E. and Qatar, are investing in aquaculture projects to enhance local oyster production. These initiatives aim to reduce dependence on imports and ensure a sustainable supply of high-quality oysters for domestic consumption and export.

Latin America

In 2025, Latin America generated USD 3.96 billion, contributing 9.21% to global market revenue, and is projected to grow to USD 4.14 billion in 2026.

KEY INDUSTRY PLAYERS

Higher Focus On New Product Launch and Geographical Expansion Among Prominent Players to Cement Their Market Position

The presence of diverse players with extensive production capabilities, widespread distribution networks, and a focus on sustainable practices characterize the global molluscs market. These companies have secured their positions through strategic initiatives, market presence, and industry influence.

ITOCHU Corporation holds a prominent position in the global market due to its extensive network of suppliers and distributors, coupled with a diverse portfolio of seafood products. This strategic advantage enables ITOCHU to maintain a significant presence across various regions. Abagold Ltd., based in South Africa, specializes in premium abalone production, distinguishing itself in the high-quality seafood segment of the market. The company's focus on sustainable aquaculture practices and recent expansion into North America will further enhance its market standing. For instance, in December 2022, the company announced its expansion in North America as the region has a wealthy Chinese consumer base with an appetite for abalone.

List of Top Molluscs Companies:

- Aqunion (Pty) Ltd. (South Africa)

- Abagold Ltd. (South Africa)

- Craig Mostyn Group (Australia)

- Omega Seafood Limited (Australia)

- Glenbeigh Shellfish Limited (Ireland)

- Mida Food Distributors Inc. (Philippines)

- Vilsund Blue A/S (Denmark)

- Southern Ocean Mariculture Pty Ltd. (Australia)

- ITOCHU Corporation (Japan)

- Shingen Foods Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS:

- May 2024: After an investment of around USD 0.53 million, the Carlingford Oyster Company upgraded its facilities and equipment to improve its efficiency and quality and expand its presence in Europe.

- May 2024: ARC Restaurant, a downtown luxury restaurant based in Vancouver, announced the launch of an oyster and wine bar pop-up inside its signature Chef's Bench for a limited time.

- April 2024: Mulwara Export, one of the most well-known Australian meat and meat products, such as beef and seafood suppliers, recently announced the addition of frozen oysters to its diver product portfolio during FHA 2024.

- February 2024: Blue Oyster Environmental (BOE), a vertically integrated oyster aquaculture company, announced its collaboration with Solar Oysters, a sustainable aquaculture technology producer. The collaboration will focus on the development of a new prototype of The Solar Oyster Production System (SOPS), which will operate on Hoopers Island Oyster Company's lease.

- January 2024: TheSeafoodCompany Group's retail brand, Seaco, known for supplying premium seafood items, such as mussels, oysters, and abalone, announced the launch of an online fresh seafood delivery service in Singapore.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies in the market’s competitive landscape by type and distribution channels. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the aforementioned growth factors, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.49% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

The Fortune Business Insights study shows that the market size was valued at USD 43.05 billion in 2025.

The market is likely to record a CAGR of 4.49% over the forecast period.

The oysters segment is the leading type segment in the market.

Growing aquaculture industry is expected to drive the global market growth.

ITOCHU Corporation, Abagold Ltd., and Aqunion (Pty) Ltd. are a few of the key players in the market.

Asia Pacific dominated the molluscs market with a market share of 60.10% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 399

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us