Montan Wax Market Size, Share & Industry Analysis, By Application (Polymer Processing, Polishes, Coatings, Printing Inks & Carbon Paper, Rubber Processing, and Others), and Regional Forecast, 2026-2034

MONTAN WAX MARKET SIZE AND FUTURE OUTLOOK

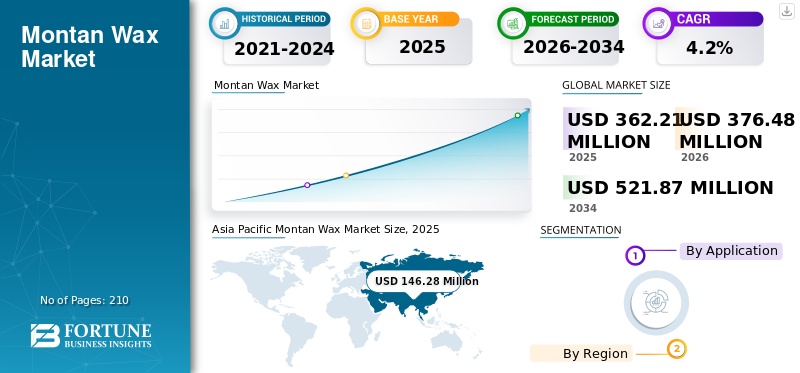

The global montan wax market size was valued at USD 362.21 million in 2025. The market is projected to grow from USD 376.48 million in 2026 to USD 521.87 million by 2034 at a CAGR of 4.2% during the forecast period. Asia Pacific dominated the montan wax market with a market share of 40.38% in 2025.

Montan wax is a high–molecular weight, fossil-derived hard wax extracted primarily from lignite (brown coal). It consists predominantly of long-chain fatty acids, esters, and alcohols, and is valued for its high melting point, hardness, gloss enhancement, and excellent lubrication properties. After refining and chemical modification, it is widely used as a performance additive in PVC processing, coatings, wax polishes, inks, and rubber applications. The primary demand driver for the market is its critical role as an internal and external lubricant in rigid PVC manufacturing, particularly for pipes and profiles used in construction and infrastructure development globally. ROMONTA Group, Clariant, Völpker Spezialprodukte GmbH, and Nanjing Tianshi New Material Technologies Co., Ltd. are the key players operating in the market.

Download Free sample to learn more about this report.

MONTAN WAX MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 362.21 million

- 2026 Market Size: USD 376.48 million

- 2034 Forecast Market Size: USD 521.87 million

- CAGR: 4.2% from 2026–2034

- Asia Pacific dominated the montan wax market with a 40.38% share in 2025.

- The polymer processing segment is anticipated to hold the dominant market share during the forecast period.

- The coatings segment is projected to grow at a CAGR of 4.4% during the forecast period.

North America

North America's market growth is primarily supported by infrastructure renewal projects and sustained demand for rigid PVC pipes

Europe

Europe maintained steady demand, driven by its established PVC manufacturing and coatings industries.

Asia Pacific

Asia Pacific dominated the market with a 40.38% share in 2025, supported by strong polymer processing demand across China and India.

U.S.

The market reached approximately USD 46.88 million in 2025, representing about 12.9% of global sales.

Japan

The market reached approximately USD 18.51 million in 2025, accounting for around 5.1% of global sales.

Read More

MONTAN WAX MARKET TRENDS

Shift toward High-Performance Additives Accelerates Adoption of Specialty Montan Wax Derivatives

A major market trend is the growing demand for modified and micronized montan-wax derivatives tailored for coatings, engineering plastics, and specialty applications. End-users increasingly seek improved scratch resistance, gloss control, and processing efficiency, driving the development of esterified and oxidized grades. Specialty coatings and advanced polymer formulations require consistent, high-purity additives, positioning refined wax made of montan favorably. This trend supports value-added product innovation rather than pure volume growth. As manufacturers focus on formulation performance and differentiation, derivative-based wax products made of montan are gaining importance within high-margin industrial applications globally.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Infrastructure Expansion Boosts PVC Demand Driving Structural Growth in Product Consumption

The primary growth driver for the market globally is its essential role as a lubricant and processing aid in rigid PVC manufacturing. Rapid infrastructure development across Asia Pacific, the Middle East, and parts of Latin America is increasing demand for PVC pipes, profiles, and construction materials. Such wax enhances melt flow, surface finish, and dimensional stability in PVC processing, making it difficult to substitute in high-performance applications. As governments prioritize urbanization, water management, and housing projects, PVC production rises correspondingly, creating steady baseline product demand across industrial economies, driving montan wax market growth in tandem.

MARKET RESTRAINTS

Environmental Regulations and Lignite Dependence to Limit Market Growth

The market faces structural restraint due to its reliance on lignite mining, a fossil resource increasingly scrutinized under global decarbonization policies. Europe, the historical production hub, continues tightening environmental regulations affecting mining and processing activities. Limited new lignite extraction projects and higher compliance costs restrict capacity expansion. Additionally, sustainability concerns from downstream customers encourage exploration of synthetic or bio-based alternatives. Although substitution remains technically limited in some applications, regulatory pressure creates long-term uncertainty around primary supply growth, potentially capping production expansion and increasing cost volatility.

MARKET OPPORTUNITIES

Emerging Industrialization in Developing Regions to Create Long-Term Demand for Specialty Additives

Developing regions such as Southeast Asia, India, and parts of Africa present meaningful growth opportunities for the market. Expanding construction, packaging, and industrial manufacturing sectors increase demand for PVC, coatings, and rubber products. As these markets modernize, higher-performance additive requirements emerge, favoring refined montan wax derivatives over lower-cost substitutes. Rising domestic manufacturing capabilities also create opportunities for regional distribution partnerships and localized processing. While current volumes remain modest relative to mature markets, urbanization and infrastructure investment provide a steady long-term demand runway for specialty industrial wax applications.

MARKET CHALLENGES

Limited Deposit Availability and Import Dependence Heighten Supply Chain Vulnerability

A critical challenge for the global montan wax industry is its geographically concentrated raw material base. Primary extraction is limited to specific lignite deposits, primarily in Europe and parts of China, creating structural supply constraints. Many consuming regions, including North America, Latin America, and the Middle East, rely heavily on imports. This exposes buyers to freight volatility, geopolitical risks, and currency fluctuations. Any disruption in mining operations or energy pricing in producing regions can disproportionately impact global supply stability, limiting the market’s flexibility and increasing procurement risk for downstream manufacturers.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Infrastructure Investment Accelerates PVC Output, Strengthening Lubricant Demand in Polymer Processing

Based on the application, the market segmentation includes polymer processing, polishes, coatings, printing inks & carbon paper, rubber processing, and others.

The polymer processing segment is anticipated to hold the dominant montan wax market share during the forecast period. The primary driver of montan-based wax demand in polymer processing is the sustained global expansion of rigid PVC production for infrastructure applications, including water pipes, sewer systems, cable conduits, and window profiles. Such wax functions as an efficient internal and external lubricant, improving melt flow, reducing die build-up, and enhancing surface finish during extrusion. As emerging economies intensify investments in urban infrastructure and developed markets upgrade aging water systems, PVC output rises steadily, directly increasing consumption of performance lubricants such as montan-wax.

Demand growth in coatings is driven by increasing performance requirements in industrial, wood, and protective coatings. Such wax improves scratch resistance, slip properties, abrasion durability, and surface aesthetics in both solvent-based and powder coatings. As end-users demand longer-lasting finishes and improved mechanical durability, particularly in automotive components, furniture, and construction materials, formulators increasingly incorporate specialty wax additives. The shift toward higher-value, performance-oriented coating systems supports steady expansion of refined and micronized montan-based wax grades globally.

The coatings segment is anticipated to rise with a CAGR of 4.4% over the forecast period.

MONTAN WAX MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Montan Wax Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was the largest and fastest growing in 2025. Asia Pacific’s product demand is strongly driven by polymer processing, led by China and India’s expanding infrastructure and urbanization programs. Rigid PVC pipes, profiles, and sheets for water management, housing, and industrial construction create sustained lubricant requirements. Coatings and printing inks provide additional momentum, particularly due to packaging growth and industrial manufacturing expansion. As emerging Southeast Asian markets industrialize, demand for performance additives rises correspondingly. The region’s dynamic construction environment makes polymer processing the dominant growth engine for such wax consumption.

Japan Montan Wax Market

Japan’s market size reached approximately USD 18.51 million in 2025, equivalent to around 5.1% of global sales.

China Montan Wax Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 61.73 million, representing roughly 17.0% of global sales.

India Montan Wax Market

India’s market reached approximately USD 29.11 million in 2025, equivalent to around 8.0% of global sales.

North America

In North America market, the principal driver of demand is polymer processing, particularly in rigid PVC pipes and profiles used for infrastructure renewal and residential construction. Aging water systems and government-backed infrastructure investments continue to support steady PVC extrusion activity, where montan-wax serves as a critical internal and external lubricant. Coatings and rubber processing provide secondary support, especially in industrial and automotive segments, but remain comparatively stable. Growth is mature and GDP-aligned, with polymer processing remaining the structural anchor of regional consumption.

U.S. Montan Wax Market

The U.S. market value approximated at around USD 46.88 million in 2025, accounting for roughly 12.9% of global sales.

Europe

Europe’s product demand is primarily driven by polymer processing, supported by the region’s mature PVC manufacturing base for construction and industrial applications. Germany’s domestic extraction also strengthens localized consumption. Coatings represent a meaningful secondary driver, particularly high-performance wood and industrial finishes requiring abrasion resistance and surface modification. While polishes remain steady, they are not growth-led. Regulatory constraints limit rapid expansion, but the combination of established PVC output and advanced coating formulations sustains consistent demand across major European economies.

U.K. Montan Wax Market

U.K.’s market reached approximately USD 16.21 million in 2025, equivalent to around 4.5% of global sales.

Germany Montan Wax Market

Germany’s market reached approximately USD 29.03 million in 2025, equivalent to around 8.0% of global sales.

Latin America

In Latin America, polymer processing is the primary driver of product demand, particularly in Brazil and Mexico, where infrastructure and residential construction stimulate PVC pipe and profile production. Polishes contribute steady demand, especially in consumer-facing surface care markets. Coatings also support industrial expansion, although on a smaller scale. Growth remains tied to economic cycles, but continued urbanization and infrastructure upgrades supports polymer-related consumption. While the region is import-dependent, expanding construction activity sustains moderate, structurally stable demand growth.

Brazil Montan Wax Market

Brazil’s market reached approximately USD 11.31 million in 2025, equivalent to around 3.1% of global sales.

Middle East & Africa

Across the Middle East & Africa, product demand is predominantly driven by polymer processing linked to large-scale construction and infrastructure initiatives. GCC nations and developing African economies are expanding water, housing, and industrial projects, increasing rigid PVC production. Coatings provide supplementary growth, particularly in protective and architectural finishes suited to harsh climates. Rubber and printing applications remain limited in scale. With industrial diversification underway in several economies, polymer processing continues to serve as the principal catalyst for regional product demand.

Saudi Arabia Montan Wax Market

Saudi Arabia’s market reached approximately USD 6.89 million in 2025, equivalent to around 1.9% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Limited Lignite Deposits Concentrate Supply, Strengthening Competitive Control Among Few Global Producers

The global market is moderately consolidated and resource-driven, with competition centered on access to lignite deposits, refining expertise, and derivative customization capabilities. Entry barriers remain high due to deposit-specific extraction requirements and environmental regulations, particularly in Europe. Germany continues to anchor primary production, while China has expanded refined capacity. The market competes more on product consistency and application performance than price alone. Key players include ROMONTA Group, Clariant, Völpker Spezialprodukte GmbH, and Nanjing Tianshi New Material Technologies Co., Ltd. collectively commanding a significant share of global supply.

LIST OF KEY MONTAN WAX COMPANIES PROFILED

- ROMONTA Group (Germany)

- VÖLPKER SPEZIALPRODUKTE GMBH (Germany)

- Clariant (Switzerland)

- Yunphos (China)

- Nanjing Tianshi New Material Technologies Co., Ltd. (China)

- Jiangsu Faer Wax Industry Co., Ltd. (China)

- TianshiWax (China)

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Volume (Ton); Value (USD Million) |

| Growth Rate | CAGR of 4.2% during 2026-2034 |

| Segmentation | By Application, and Region |

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 362.21 million in 2025 and is projected to record a valuation of USD 521.87 million by 2034.

In 2025, Asia Pacific stood at USD 146.28 million.

Registering a CAGR of 4.2%, the market will exhibit steady growth during the forecast period.

The polymer processing application is expected to lead this market during the forecast period.

The infrastructure expansion boosts PVC demand, driving structural growth in such wax consumption and market growth.

ROMONTA Group, Clariant, Völpker Spezialprodukte GmbH, and Nanjing Tianshi New Material Technologies Co., Ltd. are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

A shift toward high-performance additives to accelerate product adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us