Motorcycle Lighting Market Size, Share & Industry Analysis, By Location (Front, Rear, and Others), By Type (Halogen, LED, and Others), By Distribution Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

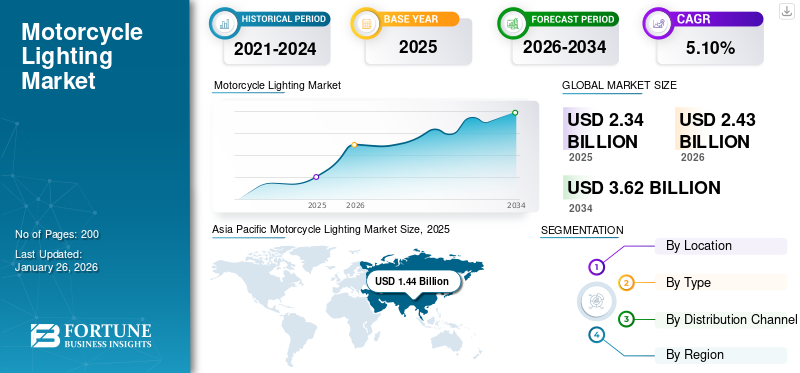

The global motorcycle lighting market size was valued at USD 2.34 billion in 2025 and is projected to grow from USD 2.43 billion in 2026 to USD 3.62 billion by 2034, exhibiting a CAGR of 5.10% during the forecast period. Asia Pacific dominated the global market with a share of 61.62% in 2025.

Motorcycle lighting refers to the integrated illumination systems used for visibility, safety, and aesthetics, including headlights, taillights, turn signals, and auxiliary lights. Modern systems feature LED and adaptive lighting technologies for enhanced brightness and energy efficiency. Advanced options such as automatic high-beam control (AHBC) and dynamic turn signals improve rider safety. Custom lighting, such as neon under glow or RGB accents, also caters to the aftermarket segment. Regulatory standards (e.g., ECE, DOT) govern lighting performance, ensuring roadworthiness. Innovations such as laser headlights and OLED displays are reshaping the industry, balancing functionality with design.

The global market is driven by rising safety regulations, increasing two-wheeler sales, and demand for energy-efficient LED systems. Major players include Osram, a leader in adaptive LED headlights; Stanley Electric, known for OEM lighting solutions for Honda and Yamaha; and Hella, specializing in high-performance auxiliary lighting. Koito Manufacturing (Japan) is known for innovative laser lighting, while Lumax (India) caters to cost-sensitive markets with durable aftermarket kits. Emerging trends include smart lighting with Bluetooth connectivity and solar-powered indicators, particularly in Asia and Europe.

The COVID-19 pandemic disrupted supply chains, delaying raw material procurement for lighting components, particularly LEDs from Asia. However, the surge in last-mile delivery services boosted demand for durable, weather-resistant lighting in commercial motorcycles. Post-lockdown, aftermarket upgrades grew as riders invested in aesthetics and safety. Manufacturers accelerated localized production to mitigate future disruptions, with India and Southeast Asia emerging as key hubs. The crisis also spurred innovation, such as anti-microbial switchgear coatings, aligning with hygiene trends. Over the long term, the market recovered due to pent-up demand and the introduction of stricter lighting safety regulations.

Download Free sample to learn more about this report.

MOTORCYCLE LIGHTING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.34 billion

- 2026 Market Size: USD 2.43 billion

- 2034 Forecast Market Size: USD 3.62 billion

- CAGR: 5.10% from 2026–2034

- Asia Pacific dominated the market with a 61.62% share in 2025.

- The halogen segment held the largest market share in 2024.

- The OEM segment dominated the market in 2024.

North America

North America accounted for USD 0.20 billion in 2025 and is projected to reach USD 0.20 billion in 2026, representing an 8.41% market share.

Europe

Europe reached USD 0.28 billion in 2025 and is expected to grow to USD 0.29 billion in 2026, holding a 12.15% market share.

Asia Pacific

Asia Pacific generated USD 1.44 billion in 2025 and is projected to reach USD 1.50 billion in 2026, holding a 61.62% market share.

U.S.

The market is projected to reach USD 0.18 billion by 2026, driven by demand for safety features, energy-efficient lighting, and customization.

Japan

The market is projected to reach USD 0.02 billion by 2026, supported by strong motorcycle demand and lighting technology adoption.

Read More

Market Dynamics

Market Drivers

Stringent Government Safety Regulations and Mandatory Lighting Standards to Augment the Market Growth

One of the primary drivers of the global market is the increasing implementation of stringent government safety regulations that mandate advanced lighting systems to reduce accidents and enhance rider visibility. Regulatory bodies worldwide enforce stricter norms for light intensity, beam patterns, and durability, compelling manufacturers to adopt advanced technologies such as LED and adaptive lighting.

For example, the European Union’s updated ECE R148 regulation (2023) requires all new motorcycles to be equipped with Automatic Headlight On (AHO) systems and adaptive brake lights to improve daytime visibility. Similarly, India’s Ministry of Road Transport and Highways (MoRTH) mandated anti-glare LED motorcycle headlights for all two-wheelers from April 2024 to reduce nighttime collisions. These regulations have pushed manufacturers including Bajaj Auto and TVS Motor, to integrate brighter, energy-efficient lighting in their latest models, such as the Bajaj Pulsar N250 and TVS Apache RTR 310.

In the U.S., the National Highway Traffic Safety Administration (NHTSA) advocates for dynamic turn signals (like those used in Audi cars) to be standardized in motorcycles following successful trials by Harley-Davidson’s 2024 models. Meanwhile, Japan’s JAMA (Japan Automobile Manufacturers Association) has set new benchmarks for weather-resistant lighting in response to increased extreme weather events. Osram (Germany) launched its LEDriving XL 100 series in 2024, meeting ECE R149 standards for ultra-bright, low-power consumption headlights.

Stanley Electric (Japan) developed laser-assisted LED lighting for Honda’s 2024 CBR1000RR-R Fireblade, offering 200% wider illumination than conventional LEDs. Lumax (India) introduced vibration-proof LED clusters for rugged bikes including the Royal Enfield Himalayan 450, addressing off-road durability demands. These regulatory shifts improve road safety and accelerate R&D investments in smart lighting, such as BMW Motorrad’s 2025 concept bikes with matrix LED headlights that adapt to road conditions. As governments prioritize accident prevention, the market is poised for sustained growth, driven by compliance-driven upgrades and technological advancements.

Download Free sample to learn more about this report.

Market Restraint

High Costs of Advanced Lighting Technologies and Price Sensitivity in Emerging Markets

One of the most significant challenges facing the market is the substantial cost of advanced lighting systems, particularly for price-sensitive consumers in emerging economies. While LED and adaptive lighting technologies offer superior performance and safety benefits, their higher production and retail costs create a barrier to widespread adoption, especially in markets where affordability is a primary purchasing consideration.

Manufacturers face pressure to keep prices low in countries such as India, Indonesia, and Nigeria, where entry-level motorcycles dominate sales.

For instance, the 2024 Hero Splendor+, one of India’s best-selling bikes, still uses halogen headlights due to cost constraints despite the availability of LED alternatives. Similarly, Bajaj Auto’s Platina 110 retains basic lighting to maintain its sub-USD 1,000 price point, as upgrading to LEDs would increase costs by 15-20%, making the bike less competitive.

Even when regulations mandate better lighting, compliance is slow. Vietnam’s 2023 lighting safety norms required brighter headlights, but many local brands including VinFast, delayed implementation due to supply chain costs. This highlights the tension between regulatory goals and economic realities in developing regions.

Advanced lighting technologies including laser headlights (BMW Motorrad) or matrix LEDs (Ducati), involve expensive R&D, patented components, and specialized manufacturing processes. For example, Osram’s latest Laser Light Modules cost 3x more than standard LED units, limiting adoption to premium bikes including KTM’s 2024 Adventure 1390. Stanley Electric’s adaptive cornering lights, featured in Honda’s 2024 Gold Wing, add USD 500+ to the bike’s MSRP, deterring budget-conscious buyers. While aftermarket LED upgrades are popular in developed markets, their high prices hinder uptake in emerging economies.

A full LED conversion kit for a Royal Enfield Classic 350 costs USD 150 in India, equivalent to 10% of the bike’s monthly EMI, making it unaffordable for many riders. To address cost challenges, manufacturers are exploring localized production and cost-effective designs. Lumax (India) launched "Budget LED" clusters in 2024, offering 70% of premium LED performance at 50% of the cost.

Market Opportunities

Rapid Electrification of Two-Wheelers and Smart Lighting Integration

The global shift toward electric motorcycles and scooters presents a transformative opportunity for the market, as EVs demand energy-efficient, intelligent lighting systems to maximize battery performance and enhance safety. Electric two-wheelers require low-power LED lighting to preserve range, creating a surge in demand for advanced solutions. For example, Ola Electric’s 2024 S1 Pro features adaptive LED headlights with proximity sensors that adjust brightness based on speed and traffic conditions, setting a new benchmark for EV lighting. Similarly, TVS Motor’s iQube Electric integrates OLED taillights with battery-status indicators, showcasing how lighting is becoming a key differentiator in the EV space.

Governments are accelerating this trend through regulations and subsidies. The European Union’s 2024 Green Mobility Initiative mandates automatic lighting systems for all new electric two-wheelers. India’s FAME-III scheme (expected 2025) may offer tax incentives for bikes with smart LED lighting. These policies are pushing manufacturers to innovate. Hella’s 2024 "E-Light" series, designed exclusively for EVs, reduces power draw by 40% compared to conventional LEDs, making it ideal for startups such as Ather Energy and Gogoro.

The rise of connected motorcycles further expands opportunities. Harley-Davidson’s 2024 LiveWire features Bluetooth-enabled mood lighting, while KTM’s "E-Drive" prototypes use lighting-as-a-communication tools (e.g., turn signals that sync with navigation). Startups including Damon Motors, even test hazard-predictive lighting that uses AI to anticipate collisions. Yamaha filed a patent for solar-powered LED indicators for its E01 electric scooter, reducing battery drain. China’s New 2024 EV lighting norms require auto-dimming headlights to prevent glare, benefiting suppliers including Stanley Electric. Piaggio Partnered with Osram to develop AI-driven lighting for its electric Vespa lineup, launching in 2025.

The EV boom opens doors for aftermarket players for retrofit smart lighting kits. Companies including Denali Electronics, now offer plug-and-play LED systems for popular e-bikes including the Zero SR/S, catering to tech-savvy riders. As EVs dominate urban mobility, lighting will evolve from a safety feature to an integrated smart system, driving sustained motorcycle lighting market growth.

Motorcycle Lighting Market Trends

Adoption of Adaptive and Connected Lighting Systems is a Market Trend

A significant trend reshaping the global market is the rapid integration of adaptive and connected lighting technologies, which enhance safety and rider experience through intelligent functionality. Unlike traditional static lights, these systems adjust to riding conditions dynamically, offering superior visibility and energy efficiency. For instance, BMW Motorrad’s 2024 R 1300 GS features adaptive cornering lights that pivot with lean angles, significantly improving nighttime curve visibility. Similarly, Ducati’s Multistrada V4 now includes matrix LED headlights that selectively dim portions of the beam to avoid blinding oncoming traffic while maintaining optimal illumination.

Government regulations are accelerating this shift. The European Union’s ECE R149 regulation (2024) mandates auto-adjusting high beams for new motorcycle models, pushing manufacturers like KTM and Triumph to adopt the technology. In Asia, India’s draft Bharat Stage VII norms (expected 2025) propose similar requirements, prompting local brands such as Bajaj and TVS to invest in adaptive lighting R&D.

Connectivity is another key driver. Harley-Davidson’s 2025 models will debut Bluetooth-linked lighting that syncs with smartphones for customizable aesthetics and hazard alerts. Aftermarket players including Denali Electronics, also capitalize on this trend with plug-and-play adaptive LED kits for popular bikes.

As AI and IoT advance, lighting evolves from a passive component to an interactive safety and design feature, ensuring sustained market innovation. Honda’s 2024 Patent: Filed for radar-guided adaptive headlights that adjust based on traffic density. Unveiled "Connected Light" modules with real-time firmware updates for OEMs.

Segmentation Analysis

By Location

Rising Safety Norms to Drive the Demand for Front Motorcycle Lights

By location, the market is segmented into front, rear, and others.

In 2024, the front lighting segment dominated with the largest market share, driven by growing concerns over motorcycle safety as accident rates continue to climb. High-performance headlights have become essential for rider visibility, especially during nighttime or low-light conditions, prompting OEMs to integrate sophisticated headlight technologies into their motorcycle designs. This focus on enhanced illumination and safety features is fueling expansion in the headlight segment, making it the fastest-growing segment.

Meanwhile, the rear lighting segment is projected to experience substantial growth in the coming years. Breakthroughs in lighting technology, particularly the adoption of LED and OLED systems, have revolutionized tail light design and functionality. These modern solutions provide superior brightness, longevity, and energy efficiency compared to conventional incandescent bulbs. Additionally, they offer greater versatility in styling, allowing for distinctive shapes, dynamic lighting patterns, and customizable aesthetics. The motorcycle industry's increasing embrace of these advanced rear lighting technologies is expected to be a key growth driver for this market segment.

The others category encompasses auxiliary and specialty lighting systems that complement the primary front and rear configurations, though they represent a smaller market.

By Type

Affordability with Competitive Pricing, especially for Price Sensitive Market Makes Halogen Dominate the Market

Based on type, the market is segmented into halogen, LED, and others.

In 2024, the halogen segment held the largest market share. In price-sensitive markets, affordability is a key factor for manufacturers and consumers. Among halogen lights led lights, halogen lights have a much lower upfront cost than LED and Xenon alternatives, making them a preferred choice for motorcycle manufacturers. This cost advantage helps maintain competitive pricing, especially for entry-level and mid-range models. In emerging economies, where motorcycles are a primary mode of transport for many, this affordability drives the continued preference for halogen lighting.

LED segment is projected to grow at a high CAGR during the forecast period. LEDs provide exceptional design versatility, enabling manufacturers to develop innovative and visually appealing lighting solutions. Their compact size and adaptability allow unique lighting signatures, enhancing motorcycle aesthetics and supporting brand identity. With LEDs, designers can incorporate complex shapes, intricate patterns, and dynamic lighting effects, pushing creative boundaries and creating eye-catching designs. This flexibility allows manufacturers to customize lighting systems for specific models and consumer preferences, accelerating LED technology adoption.

By Distribution Channel

Stringent Safety Regulations and Standards Fueling Demand for the OEM Segment

Based on distribution channel, the market is bifurcated into OEM and aftermarket.

In 2024, the OEM segment dominated the motorcycle lighting market share. A key factor driving growth in OEM lighting is the global push for stricter safety regulations. Governments and regulatory bodies enforce rigorous standards, requiring automatic headlights (AHO), daytime running lights (DRLs), and enhanced visibility in low-light conditions. These mandates compel OEMs to integrate advanced, compliant lighting systems into their motorcycles, boosting demand for high-quality lighting solutions from OEM suppliers that meet these stringent requirements.

Meanwhile, the aftermarket segment will gain significant market share in the coming years. Motorcycle enthusiasts increasingly opt for customization to differentiate their bikes, replacing old discharge gas lamps and incandescent lamps with new advanced lighting systems. Aftermarket lighting products, including LED lights, HID kits, and auxiliary lights, provide diverse customization choices, from color temperature to beam patterns. This trend propels the aftermarket sales channel's growth as manufacturers and suppliers leverage it to deliver innovative, distinctive lighting solutions.

Motorcycle Lighting Market Regional Outlook

Based on region, the market is segmented into North America, Europe, Asia Pacific, and rest of the world.

Asia Pacific

Asia Pacific Motorcycle Lighting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 1.44 billion in 2025, capturing 61.62% of global revenue, and is estimated to reach USD 1.5 billion in 2026. Asia Pacific is dominant and expected to grow at the highest CAGR over the forecast period. Rising disposable incomes and rapid urbanization in emerging Asia Pacific economies such as India, Indonesia, Vietnam, and Philippines have substantially increased motorcycle ownership. As more people enter the middle class, they can afford personal transportation, and motorcycles often represent an accessible and practical solution to navigating increasingly congested urban environments. Each new motorcycle sold adds to the demand for OEM lighting components, and the growing fleet of vehicles naturally drives the aftermarket demand for replacements and upgrades over time. The Japan market is projected to reach USD 0.02 billion by 2026, the China market is projected to reach USD 0.48 billion by 2026, and the India market is projected to reach USD 0.73 billion by 2026.

North America

North America contributed 8.41% to the global market in 2025, with a valuation of USD 0.2 billion, and is projected to reach USD 0.2 billion in 2026. North America held a considerable market share in 2024. Beyond technological integrations, the consumer landscape is shifting towards a preference for customization and personalization in motorcycle accessories, including lighting. More riders are looking for options that serve a functional purpose and reflect their style. This trend has spurred manufacturers to offer a wide assortment of lighting products, from neon under glows to customizable LED accents—allowing riders to express their individuality. The U.S. market is driven by increasing demand for advanced safety features, energy-efficient solutions, and aesthetic enhancements. With the adoption of stricter regulations on lighting standards and growing consumer interest in customizations, manufacturers are focusing on innovative designs and technologies to meet evolving market needs. The U.S. market is projected to reach USD 0.18 billion by 2026.

Europe

Europe accounted for USD 0.28 billion in 2025, representing 12.15% of the global market share, and is projected to reach USD 0.29 billion in 2026. Safety regulations in Europe have become increasingly stringent, particularly regarding vehicle visibility. Directives such as the UNECE regulations set high standards for headlight performance, taillight intensity, and the mandatory inclusion of features including Daytime Running Lights (DRLs) on many new models. These regulations are designed to reduce accidents by making motorcycles, scooters, and even some bicycles more conspicuous to other road users, especially in varying light conditions. The UK market is projected to reach USD 0.03 billion by 2026, while the Germany market is projected to reach USD 0.06 billion by 2026.

Rest of the World

The rest of the World is expected to grow at a rapid CAGR during the forecast period. The market in Latin America and Middle East & Africa has expanded significantly, propelled by shifting consumer preferences. In urban areas, where traffic congestion is an increasing issue, motorcycles are often seen as a practical alternative to cars. Motorcycles and scooters not only navigate through heavy traffic easily but also provide economical solutions for commuting.

Competitive Landscape

Key Market Players

Vast Product Portfolio, Strong R&D Capabilities Developing Cutting-Edge Solutions Makes Osram Licht AG as the Leader

Osram Licht AG, a German multinational, leads the global motorcycle lighting market share, recognized for its cutting-edge automotive lighting solutions. The company’s leadership stems from its strong R&D capabilities, high quality LED and laser-based lighting technologies, and stringent global safety standards compliance. Osram supplies OEMs with advanced lighting systems, including adaptive headlights, energy-efficient LED modules, and intelligent lighting solutions that enhance visibility and safety. Its product portfolio covers headlamps, taillights, turn signals, and auxiliary lights, catering to premium and performance motorcycles. Strategic decision partnerships with major automotive manufacturers and a focus on innovation solidify Osram’s position as a market leader.

Hella GmbH & Co. KGaA, a German automotive parts supplier, is another key player in the market, known for its high-performance and durable lighting solutions. The company specializes in LED and halogen lighting systems, offering adaptive headlights, dynamic turn signals, and energy-efficient daytime running lights (DRLs). Hella’s strong OEM partnerships and focus on safety-compliant designs make it a preferred supplier for leading motorcycle brands. Its product range includes advanced projection headlamps, auxiliary lights, and customizable LED strips, ensuring superior visibility and aesthetic appeal for modern motorcycles.

List of Key Motorcycle Lighting Companies Profiled in the Report

- Lumax (India)

- FIEM Industries Ltd. (India)

- Koito Manufacturing Co., Ltd. (Japan)

- Varroc (India)

- Oracle Lighting (S.)

- Osram GmbH (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Hella GmbH & Co. KGaA (Germany)

- Uno Minda (India)

- NEOLITE ZKW Lightings Pvt. Ltd. (India)

Key Industry Developments

- In May 2025, Uno Minda announced the consolidation and shifting of 2W lighting manufacturing plants at Bahadurgarh and Sonipat to a new location at Kharkhoda, Haryana.

- The new manufacturing facility is being set up to meet the continuous increase in the demand from OEMs and will also avoid the efficiency loss of 3 plant operations. It is expected to commence its operations from 2026-27.

- In March 2025, Uno Minda Introduced the Premium Ultimo Pro+ LED Lighting Bulb Range for motorcycles in the Indian Aftermarket. The Ultimo Pro+ LED lighting range comes in three variants of power outputs-20W, 15W, and 10W, with lumen outputs of 2000, 1700, and 1100, respectively. This allows riders to choose the right illumination level based on their needs, ensuring optimal visibility for an enhanced riding experience. The sleek, modern design adds a stylish touch to motorcycles, making it the perfect combination of performance and aesthetics for riders navigating city streets or highways.

- In September 2024, HEX Innovate partnered with Lone Rider to power their new auxiliary motorcycle lights. As part of this collaboration, HEX Innovate will supply their market-leading ezCAN product proposition (privately labeled as MotoCAN), enabling Lone Rider to integrate and configure their new lighting range – MotoLights. The partnership between HEX Innovate and Lone Rider signifies a shared commitment to innovation, quality, and customer satisfaction.

- March 2023 – FIEM Industries Ltd. signed an MoU with Gogoro India to expand its product portfolio in the Motorcycle EV segment. This collaboration includes FIEM manufacturing Lighting & Rear View Mirror Hub Motor Assembly, Electric Control Unit (ECU), and Motor Control Unit (MCU) for Gogoro, supported by Gogoro's technical expertise and support in manufacturing, production, quality, and testing. In addition to this new product line, FIEM already supplies lighting and rear-view mirrors to Gogoro.

- In April 2022, Plastic Omnium informed decisions to acquire the European and North American lighting businesses of Varroc Engineering for EUR 600 million, equivalent to USD 634 million. This acquisition was a key step for Plastic Omnium in expanding its presence in the automotive lighting market.

Investment Analysis and Opportunities

Technological Advancements to Generate Opportunities for Market Growth

The global motorcycle lighting market forecast indicates significant growth due to rapid technological advancements, particularly in LED, adaptive lighting, and smart connectivity solutions. One of the key innovations is adaptive headlight systems (AHS), which adjust beam patterns based on riding conditions, improving nighttime safety. For instance, BMW Motorrad’s latest models feature adaptive headlights that pivot with the bike’s lean angle, enhancing visibility on curves—a technology now mandated in the EU’s updated vehicle safety regulations (GSR). Another major trend is integrating IoT-enabled lighting systems, allowing riders to control lights via smartphone apps for customization and diagnostics. Companies including Honda have introduced Bluetooth-connected LED lighting in their premium models, enabling dynamic color changes and automatic brightness adjustments.

Additionally, pioneered by brands including Osram, laser lighting technology offers ultra-bright, energy-efficient illumination, gaining traction in high-end motorcycles. Governments worldwide are pushing stricter safety norms, such as India’s mandatory Automatic Headlamp On (AHO) rule and the U.S. NHTSA’s emphasis on DRLs (Daytime Running Lights), further driving demand for advanced lighting. These innovations and regulatory support create lucrative opportunities for manufacturers to expand their market presence.

Report Coverage

The global motorcycle lighting market report analyzes the market in-depth and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, and technology adoption. Besides this, the market research report provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.10% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Location

By Type

By Distribution Channel

By Region

|

Frequently Asked Questions

Fortune Business Insights reports that market size was USD 2.34 billion in 2025 and is anticipated to reach USD 3.62 billion by 2034.

The market will exhibit a CAGR of 5.10% over the forecast period.

By type, the halogen segment dominates the market.

Increasing safety concerns and supportive government regulations to augment the market growth.

Leading companies include Lumax, FIEM Industries Ltd., Oracle, Hella, OSRAM, Varroc, and Uno Minda.

Asia Pacific held the largest share of the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us