Nanobody Therapeutics Market Size, Share & Industry Analysis, By Molecule (Caplacizumab (Cablivi), Ozoralizumab (Nanozora), Envafolimab, and Others), By Nanobody Type (Bivalent, Trivalent, Fc-fused / Half-life Extended, and Others), By Disease Indication (Hematological / Blood Disorders, Rheumatoid Arthritis, Oncology, and Others) By Route of Administration (Intravenous, Subcutaneous, and Others), By Distribution Channel (Hospital Pharmacies, Specialty Pharmacies, and Others), and Regional Forecast, 2026-2034

Nanobody Therapeutics Market Size and Future Outlook

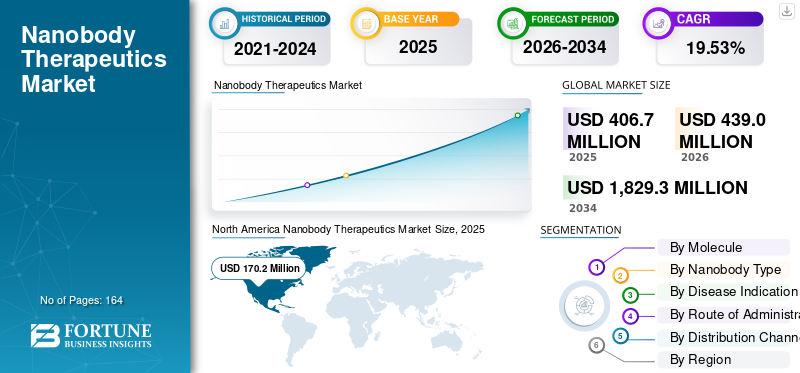

The global nanobody therapeutics market size was valued at USD 406.7 million in 2025. The market is projected to grow from USD 439.0 million in 2026 to USD 1,829.3 million by 2034, exhibiting a CAGR of 19.53% during the forecast period.

Nanobody therapeutics represent a niche biologics market focused on single-domain antibody fragments that bind targets with greater specificity in a smaller, more customizable format than traditional monoclonal antibodies. The expansion of the global market is fueled by growing interest in multivalent and bispecific nanobody formats, and by heightened emphasis on subcutaneous delivery. Additionally, the capacity of nanobody platforms to facilitate distinct targeting strategies in ailments where convenience, tissue penetration, and multi-target actions are crucial.

Key players in the global market include Sanofi, Taisho Pharmaceutical, and 3D Medicines. These firms are vying in the market for approved rare disease and immunology products, PD-L1 nanobody-based immuno-oncology treatments.

Download Free sample to learn more about this report.

Nanobody Therapeutics Market Key Takeaways

- 2025 Market Size: USD 406.7 million

- 2026 Market Size: USD 439.0 million

- 2034 Forecast Market Size: USD 1,829.3 million

- CAGR: 19.53% from 2026–2034

- North America dominated the nanobody therapeutics market in 2025.

- The trivalent segment is projected to grow at a 9.85% CAGR during the forecast period.

- The oncology segment is anticipated to expand at a 0.65% CAGR over the forecast period.

North America

North America led the market with USD 170.2 million in 2025.

Europe

Europe is projected to grow at a 21.26% CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 114.7 million in 2026.

U.S

The market is projected to reach USD 165.0 million in 2026, accounting for 37.6% of global revenue.

Japan

The market is estimated at USD 14.8 million in 2026, representing 3.4% of global revenue.

Read More

NANOBODY THERAPEUTICS MARKET TRENDS

Recent Advances in Antibody Engineering is a Significant Trend Observed in the Global Market

Recent progress in antibody engineering is becoming a significant trend in the nanobody therapeutics sector as companies shift from basic single-target molecules to multivalent, multispecific, and half-life-extended designs. This aids in enhancing target binding, prolonging action duration, and facilitating improved tissue penetration, making nanobody therapies more competitive in challenging diseases. This trend is particularly significant in immunology and inflammation, where engineered nanobody formats are created to target several disease pathways simultaneously while maintaining the compact size benefit of nanobodies. It is also increasing the market's commercial potential by enabling developers to focus on wider and more valuable indications instead of solely niche, rare diseases. Consequently, antibody engineering is enhancing the clinical significance and long-term scalability of nanobody therapies. These factors are supporting the overall global nanobody therapeutics market growth.

- For instance, in September 2025, Sanofi’s brivekimig, a dual-target Nanobody VHH inhibiting TNF and OX40L, reported positive Phase 2a results in hidradenitis suppurativa. This shows how engineered multi-target nanobody designs are now being used to improve efficacy and expand the role of this therapeutics in immune-mediated diseases.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Biologics is Propelling Market Growth

Rising demand for biologics is a major driver of the market. Healthcare systems and drug developers are increasingly favoring highly targeted therapies for complex and chronic diseases. This demand is pushing companies to invest in next-generation biologic formats that can deliver strong efficacy with improved convenience and differentiated engineering. Nanobody therapeutics benefit from this shift, as they combine the biologic precision of antibodies with smaller size, flexible design, and growing use in inflammatory and immune-mediated diseases. As biologics demand rises, developers are also seeking platforms that can support multi-target action, better tissue penetration, and subcutaneous administration, all of which strengthen the commercial case for nanobodies. This is helping expand nanobody development beyond rare diseases into larger immunology and specialty-care markets. All these factors cumulatively drive the overall market growth.

- For instance, in January 2025, MoonLake Immunotherapeutics announced that it had initiated three new clinical trials and expanded the nanobody into additional inflammatory indications, while noting that data from the program may support the first Biologics License Application (BLA) for sonelokimab.

MARKET RESTRAINTS

Manufacturing Complexity to Impede Market Growth

The complexity of manufacturing is a significant limitation in the market, as these products necessitate specific biologics process development, scaling, quality assurance, and production systems that meet regulatory standards. Despite being smaller than traditional antibodies, companies encounter difficulties in creating reproducible commercial-scale production and in overseeing formulation, stability, and supply consistency throughout trials and subsequent launches. This lengthens development timelines, elevates CMC-related costs, and may delay the shift from clinical success to market launch. The pressure intensifies as companies enter late-stage studies and prepare for biologics submissions, as manufacturing preparedness is essential for both approval and market entry. Consequently, the complexity of manufacturing may restrict velocity, heighten cost challenges, and pose an obstacle for smaller developers in the industry.

- For instance, in November 2025, in its Q3 update, MoonLake Immunotherapeutics stated that operating expenses increased partly due to higher spending with contract manufacturing organizations to support clinical ramp-up and preparations for the anticipated BLA submission for sonelokimab.

MARKET OPPORTUNITIES

Improvements in Drug Delivery to Offer Market Growth Opportunities

Advancements in nanobody drug delivery are generating significant opportunities in the market, as they enhance the usability of these biologics, increase convenience for patients, and optimize them for long-term treatment applications. As businesses transition from hospital-centered management to more patient-friendly approaches, nanobody therapies can enter wider chronic disease markets where convenience is important. Enhanced delivery systems further increase adherence, decreasing administrative burdens, and enabling differentiation from traditional biologics. This is particularly crucial for subcutaneous nanobody products, as device innovation can enhance commercial adoption while maintaining the fundamental therapeutic mechanism. Consequently, enhancements in delivery are improving the patient experience and expanding the market potential for nanobody-based medications. All these factors would drive the market growth in the coming years.

- For instance, in January 2024, Taisho Pharmaceuticals launched of the Nanozora 30 mg Autoinjector for subcutaneous injection which is designed to improve ease of use for rheumatoid arthritis patients.

MARKET CHALLENGES

High Cost of Development is a Prominent Challenge to Market Growth

Significant development expenses pose a key obstacle in the nanobody therapeutics sector, as these products still need costly discovery, biologics engineering, multi-phase clinical trials, CMC scaling, and regulatory readiness before they can be transformed into marketable assets. Although nanobodies present technical benefits, companies must still finance lengthy development periods across various indications, leading to heightened capital requirements and greater execution risk. This issue is particularly evident in the current market, as numerous prominent nanobody programs remain in late-stage or multi-indication development rather than having achieved widespread commercial maturity. Consequently, developers need to invest significantly in trials, manufacturing preparedness, and regulatory efforts long before substantial revenue is attained. This may hinder portfolio growth, restrict smaller companies' involvement, and increase market reliance on robust funding access or collaborations. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Molecule

Strong Market Presence across the Globe Led to Dominance of the Caplacizumab (Cablivi) Segment

In terms of molecule, the market is divided into caplacizumab (Cablivi), ozoralizumab (Nanozora), envafolimab, and others.

The Caplacizumab (Cablivi) segment led the global market in 2025. Caplacizumab is the first and most established commercial nanobody therapeutic, giving it a major advantage over other molecules that are either limited to one country or still in the pipeline. The product has a broader regulatory and commercial footprint, with approvals in the U.S. and Europe well ahead of most competing nanobody drugs, helping it build physician familiarity and market revenue faster. It also addresses Acquired Thrombotic Thrombocytopenic Purpura (aTTP), a life-threatening rare blood disorder where early diagnosis and rapid treatment are critical, which supports strong clinical adoption. In addition, Sanofi has continued expanding the product’s market presence through patient identification efforts and regional launches, further strengthening its leadership.

- For instance, in Q2 2025, Sanofi reported that Cablivi sales increased by 29.6% to USD 77.9 million, driven by more patients being identified for treatment in the U.S. and Europe.

The envafolimab segment is anticipated to rise with a CAGR of 0.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Nanobody Type

Strong Commercial Success Supported the Dominance of Bivalent Segment

Based on nanobody type, the market is classified into trivalent, Fc-fused/half-life extended, bival

ent, and others.

The bivalent segment captured the leading market position in 2025. They were the first format to attain significant commercial success, exemplified by Caplacizumab (Cablivi). This provided the segment a preliminary revenue edge compared to multivalent and Fc-fused formats, which remain more restricted in the number of approved products. Bivalent formats hold significant commercial value as they offer enhanced target binding while maintaining the size and engineering benefits of nanobodies. In the present market, this has enabled bivalent nanobodies to gain physician trust and achieve broader treatment adoption more swiftly than newer formats. Furthermore, the segment is set to hold 75.8% share in 2026.

- For instance, Sanofi’s cablivi is a bivalent anti-vWF Nanobody and is witnessing a significant revenue growth.

The trivalent segment is anticipated to rise with a CAGR of 9.85% over the forecast period.

By Disease Indication

Strong Volume of Hematological/Blood Disorders Supported the Segment Dominance

Based on disease indication, the market is classified into hematological/blood disorders, rheumatoid arthritis, oncology, and others.

The hematological/blood disorders segment dominated with the largest nanobody therapeutics market share in 2025, driven by the most established and highest-selling nanobody therapeutic, Caplacizumab (Cablivi). It is used for Acquired Thrombotic Thrombocytopenic Purpura (aTTP), a serious blood disorder that requires urgent treatment. Since nanobody therapeutics are still at an early commercial stage, the presence of a strong approved product in hematology gave this segment a clear revenue advantage over oncology and autoimmune indications. The segment also benefited from earlier approvals and wider commercial expansion of Cablivi across major markets, which helped build physician awareness and treatment adoption. In addition, rare blood disorders often require highly targeted therapies, which supports the value proposition of nanobody-based treatments. Furthermore, the segment is set to hold 75.8% share in 2026.

- For instance, in December 2025, Sanofi announced that Cablivi was approved in China for Acquired Thrombotic Thrombocytopenic Purpura (aTTP), expanding access for this rare, life-threatening blood clotting disorder.

The oncology segment is anticipated to rise with a CAGR of 0.65% over the forecast period.

By Route of Administration

Presence of Approved Products and Expanding Clinical Pipeline Led to the Dominance of Subcutaneous Segment

On the basis of route of administration, the market is divided into intravenous, subcutaneous, and others.

In 2025, the subcutaneous segment dominated the market. Most approved and emerging nanobody therapeutics are designed to facilitate easier and more convenient dosing outside complex infusion settings. This route is commercially important as it reduces administrative burden, improves patient convenience, and aligns well with long-term treatment in oncology and immune-related diseases. In the current nanobody market, Envafolimab and Nanozora strengthened the subcutaneous base, while several pipeline products are being developed for subcutaneous dosing. This gives the segment a broader commercial foundation than intravenous therapies, which are more dependent on hospital-based use. Furthermore, the segment is set to hold 88.4% share in 2026.

- For instance, in September 2025, Glenmark announced the start of a multi-country Phase 3 trial for Envafolimab, describing it as a subcutaneous PD-L1 inhibitor and noting its potential to improve treatment accessibility in cancer care.

The intravenous segment is anticipated to rise with a CAGR of 14.23% over the forecast period.

By Distribution Channel

Higher Usage in Hospital Settings Led to Dominance of Hospital Pharmacies Segment

Based on distribution channel, the market is segmented into hospital pharmacies, specialty pharmacies, and others.

The hospital pharmacies segment dominated the market in 2025. The market is still led by products used in serious and specialty disease settings, where treatment is usually started and managed in hospitals. Caplacizumab (Cablivi) is used for aTTP, a rare and life-threatening blood disorder that needs urgent diagnosis, plasma exchange, and close medical supervision. In this treatment setting, hospital pharmacies became the primary point of drug access, dispensing, and clinical coordination. Early approved nanobody products had limited retail presence and were more closely linked to specialist or institutional care. Furthermore, the segment is set to hold 52.0% share in 2026.

In addition, specialty pharmacies are projected to grow at a 23.21% rate during the forecast period.

Nanobody Therapeutics Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, and the rest of the world.

North America

North America Nanobody Therapeutics Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market size attained USD 161.7 million in 2024 and dominated the market. In 2025, the region maintained its leading share, with USD 170.2 million. The growth in North America is mainly supported by the strong commercial base of Cablivi in the U.S., high rare-disease diagnosis rates, and faster uptake of innovative biologics in specialist care settings.

U.S. Nanobody Therapeutics Market

The U.S. market led the North American region and is projected to reach approximately USD 165.0 million in 2026, representing about 37.6% of the global market.

Europe

Europe’s market size is anticipated to grow at a CAGR of 21.26% during the forecast period. The region is being driven by early access to Cablivi, strong specialist hospital networks, and rising future opportunities from late-stage nanobody assets in inflammatory and respiratory diseases.

U.K. Nanobody Therapeutics Market

The U.K. market in 2026 is estimated at around USD 18.7 million, representing roughly 4.3% of global revenues.

Germany Nanobody Therapeutics Market

Germany’s market size is projected to reach approximately USD 24.5 million in 2026, equivalent to around 5.6% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach USD 114.7 million by 2026. Asia Pacific is one of the strongest growth regions as it already has two important commercial anchors: Envafolimab in China and Nanozora in Japan. The growth is also being strengthened by product-format improvements.

Japan Nanobody Therapeutics Market

The Japanese market in 2026 is estimated at around USD 14.8 million, accounting for roughly 3.4% of global revenues.

China Nanobody Therapeutics Market

China’s market is projected to reach revenues of around USD 67.8 million in 2026, representing roughly 15.5% of global sales.

India Nanobody Therapeutics Market

The Indian market in 2026 is estimated at around USD 3.3 million, accounting for roughly 0.7% of global revenues.

Rest of the World

The rest of the world regions are expected to experience slower growth throughout the forecast period. The regional growth is currently more pipeline-led than approval-led. The primary driver is the potential future expansion of Envafolimab through the Glenmark licensing and multi-country Phase 3 program.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Expansion of Clinical Pipeline to Strengthen Market Position

The global nanobody therapeutics market is moderately concentrated, with major players such as Sanofi, Taisho Pharmaceutical Co., Ltd., and 3D Medicines Inc., accounting for a notable share of market activity. These companies are focusing on approved-product expansion, late-stage pipeline advancement, and engineered multivalent or bispecific nanobody formats to improve their competitive position. The market is also witnessing increased emphasis on subcutaneous delivery, indication expansion in immunology and oncology, and broader regional commercialization strategies. Companies are increasingly using clinical data generation, lifecycle extension, and strategic licensing agreements to strengthen long-term market presence.

- For instance, in February 2026, MoonLake Immunotherapeutics announced positive Phase 2 topline results for sonelokimab in axial spondyloarthritis, further strengthening its position in the inflammatory-disease nanobody pipeline.

Other significant participants include Alphamab Oncology, MoonLake Immunotherapeutics, and others. These companies are expected to prioritize new indication development, geographic expansion, and next-generation nanobody engineering to improve their competitive positions over the forecast period.

LIST OF KEY NANOBODY THERAPEUTICS COMPANIES PROFILED

- Sanofi (France)

- 3D Medicines Inc. (China)

- Taisho Pharmaceutical Co., Ltd. (Japan)

- Alphamab Oncology (China)

- MoonLake Immunotherapeutics (Switzerland)

- Other Prominent Players

KEY INDUSTRY DEVELOPMENTS

- January 2026: MoonLake Immunotherapeutics announced a positive outcome from its Type B meeting with the U.S. FDA for sonelokimab in hidradenitis suppurativa, supporting its planned BLA submission in H2 2026.

- December 2025: Alphamab Oncology’s Envafolimab received another U.S. FDA Orphan Drug Designation for gastric cancer and gastroesophageal junction cancer. The company noted this was the third orphan designation for Envafolimab.

- September 2025: MoonLake Immunotherapeutics reported week 16 Phase 3 VELA-1 and VELA-2 results for sonelokimab in moderate-to-severe hidradenitis suppurativa.

- April 2025: Sanofi announced that lunsekimig, its IL-13/TSLP Nanobody VHH, is expanding beyond asthma and is being developed for chronic rhinosinusitis and COPD as well.

- January 2024: Glenmark announced a license agreement for Envafolimab (KN035) covering India, APAC, the Middle East & Africa, Russia/CIS, and Latin America.

REPORT COVERAGE

The global nanobody therapeutics market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market over the forecast period. It provides understanding of essential factors, including pipeline analysis, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers, and acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.53% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Molecule, Nanobody Type, Disease Indication, Route of Administration, Distribution Channel, and Region |

| By Molecule |

|

| By Nanobody Type |

|

| By Disease Indication |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 406.7 million in 2025 and is projected to reach USD 1,829.3 million by 2034.

In 2025, the North American market value stood at USD 170.2 million.

The market is expected to exhibit a CAGR of 19.53% during the forecast period.

By molecule, the Caplacizumab (Cablivi) segment led the market in 2025.

Growing interest in multivalent and bispecific nanobody formats and heightened emphasis on subcutaneous delivery are the key factors driving the market.

Sanofi, 3D Medicines Inc., and Taisho Pharmaceutical Co., Ltd. are some of the prominent players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us