Nanomaterials Market Size, Share & Industry Analysis, By Product Type (Metal Oxides & Ceramic Nanoparticles, Carbon-based Nanomaterials, Nanoclays & Layered Materials, Nanocellulose, Semiconductor Nanocrystals, and Others), By End Use (Electronics & Semiconductors, Coatings, Polymers & Composites, Energy Storage, Personal Care & Cosmetics, Construction, and Others), and Regional Forecast, 2026-2034

Nanomaterials Market Size and Future Outlook

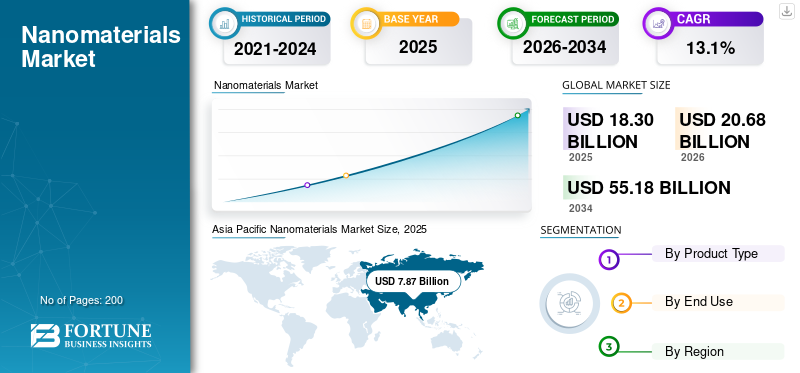

The global nanomaterials market size was valued at USD 18.30 billion in 2025. The market is projected to grow from USD 20.68 billion in 2026 to USD 55.18 billion by 2034, exhibiting a CAGR of 13.1% during the forecast period. Asia Pacific dominated the nanomaterials market with a market share of 43.01% in 2025.

Nanomaterials refer to engineered materials with at least one dimension typically below 100 nm, including metal oxide nanoparticles, carbon-based nanomaterials, nanoclays, nanocellulose, semiconductor nanocrystals, and other nano sized materials. Due to their high surface area and tunable electrical, mechanical, optical, and barrier properties, these materials are widely used to enhance performance in a range of high-performance applications. The major application areas driving demand are electronics, semiconductors, coatings, composites, personal care formulations, and others. The market is expected to grow due to the escalating demand for miniaturized electronics, advanced protective coatings, and lightweight composites.

The global market is led by technology-driven material suppliers and specialty chemical companies, including Cabot Corporation, OCSiAl, NanoXplore, Nanocyl, Resonac, and American Elements. Key players increasingly compete based on high-performance conductive additives, metal oxide nanoparticle scale and purity, dispersion and formulation capabilities, and co-development programs with OEMs. Recent developments indicate a clear strategic direction toward launching next-generation materials tailored to energy storage, next-gen electronics, and EV power devices.

Download Free sample to learn more about this report.

Nanomaterials Market Key Takeaways

- 2025 Market Size: USD 18.30 billion

- 2026 Market Size: USD 20.68 billion

- 2034 Forecast Market Size: USD 55.18 billion

- CAGR: 13.1% from 2026-2034

- Asia Pacific dominated the nanomaterials market with a 43.01% share in 2025.

- The carbon-based nanomaterials segment is projected to grow at the fastest CAGR of 13.8% during the forecast period.

- The energy storage segment is expected to register the highest CAGR of 14.8% during the forecast period.

Asia Pacific

Asia Pacific reached USD 7.87 billion in 2025 and is projected to grow to USD 8.95 billion in 2026.

North America

North America accounted for USD 5.86 billion in 2025 and is projected to reach USD 6.59 billion in 2026.

Europe

Europe reached USD 3.84 billion in 2025 and is projected to grow at a CAGR of 12.2% during the forecast period.

U.S.

The market is anticipated to reach USD 5.81 billion in 2026, accounting for nearly 28% of global revenues.

Japan

Rising demand for advanced materials in electronics, automotive, and energy storage applications is supporting market growth.

Read More

NANOMATERIALS MARKET TRENDS

Battery Performance Enhancement and Conductive Additives to Favor Product Adoption

A key market trend is the rising integration of nanomaterials, especially carbon-based materials and engineered conductive additives into lithium-ion batteries and energy storage systems to improve conductivity, cycle life, and fast-charging performance. This is pushing suppliers to tailor nano-carbon structures, optimize dispersion stability, and offer application-ready formulations that simplify electrode manufacturing. In parallel, electronics miniaturization and advanced packaging are increasing the pull for semiconductor-linked nanomaterials and specialty nano-engineered materials that can enable higher power density and improved thermal management. The aforementioned factors are expected to reinforce product adoption across batteries and electronics, strengthening demand visibility through 2034.

- The U.S. government is actively bolstering the domestic lithium-ion battery supply chain through the National Blueprint for Lithium Batteries 2021-2030, aiming to secure domestic manufacturing, reduce reliance on foreign suppliers, and advance recycling technologies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Electronics and Advanced Semiconductor Manufacturing to Drive Product Demand

The nanomaterial demand is rising as electronics ecosystems expand and device architectures become smaller, faster, and more performance-sensitive. Nano-enabled materials are increasingly used in conductive pathways, thermal interface materials, protective coatings, and packaging layers to support reliability under higher operating loads. In addition, the growing adoption of EVs and energy storage is structurally increasing the demand for conductive and performance-enhancing additives, thereby supporting the wider penetration of nanocarbons and metal oxide nanoparticles. As more end users prioritize high-performance materials that also reduce weight and improve efficiency, the product use is expected to increase, driving the global nanomaterials market growth during the forecast period.

MARKET RESTRAINTS

Scale-Up Complexity and Qualification Cycles May Constrain Faster Adoption

While nanomaterials enable performance gains, broad industrial-scale-up remains a challenge due to factors such as dispersion challenges, batch-to-batch consistency requirements, and longer qualification timelines. Variability in particle morphology, surface treatment, and contamination control can influence performance, making customers cautious about switching suppliers. In addition, compliance and safe-handling considerations increase the adoption friction for some nano-forms, especially where workplace exposure and downstream regulatory expectations require strict documentation. As a result, despite strong demand fundamentals, commercialization speed is still shaped by qualification depth and manufacturing reproducibility.

MARKET OPPORTUNITIES

Energy Storage Scale-Up and Lightweight Composites to Create Lucrative Growth Pockets

The energy storage scale-up is creating one of the highest-growth opportunities for the market, as battery makers seek conductive additives and engineered materials that improve throughput, lifetime, and reliability under demanding duty cycles. At the same time, lightweighting priorities in transportation and industrial equipment are expanding the use of nano-enabled polymers and composites that can deliver higher strength-to-weight performance and improved durability. Suppliers that can deliver application-ready dispersions and proven manufacturing consistency are positioned to benefit most from these structural demand shifts.

Segmentation Analysis

By Product Type

Metal Oxides & Ceramic Nanoparticles Segment Dominates Due to Broad Industrial Use

Based on product type, the market is segmented into metal oxides & ceramic nanoparticles, carbon-based nanomaterials, nanoclays & layered materials, nanocellulose, semiconductor nanocrystals, and others.

The metal oxides & ceramic nanoparticles segment holds the largest market share, supported by wide use across coatings, construction additives, electronics, and industrial formulations, where nanoscale functionality improves durability, barrier properties, UV resistance, and surface performance. The increasing penetration into high-performance coatings and electronics-linked applications is likely to support the segment’s growth over the forecast period. Metal oxide and ceramic nanoparticles have become integral to modern technology and industry, with major uses spanning environmental protection, life science, biomedical applications, electronics, and energy.

The carbon-based nanomaterials segment is expected to remain the fastest-growing product category, likely to surge at a CAGR of 13.8% over the forecast period. The growth is driven by the accelerating adoption of CNT/graphene-type additives in batteries, conductive composites, EMI shielding, and advanced polymers, where conductivity and mechanical reinforcement are critical. The demand is rising as EV and stationary storage manufacturers seek lower-resistance electrode networks, improved cycle stability, and better rate capability without major formulation redesign. The segment growth is further reinforced by expanding use in thermal management and electrical interconnect applications.

The nanoclays & layered materials segment represents another key category, expanding at a CAGR of 10.8% over the forecast period. The segment growth is driven by their role in enhancing barriers and improving properties in packaging, polymers, and select construction-linked formulations. These materials improve the oxygen and moisture barrier performance, dimensional stability, and flame resistance of polymer systems, making them valuable for high-performance films, rigid packaging, and specialty composite structures. The product’s commercialization is widely supported by compatibility improvements and dispersion solutions that reduce processing penalties at an industrial scale.

By End Use

Electronics & Semiconductors Segment Dominates Due to High-Value Applications and Technology Integration

Based on end use, the market is segmented into electronics & semiconductors, coatings, polymers & composites, energy storage, personal care & cosmetics, construction, and others.

To know how our report can help streamline your business, Speak to Analyst

The electronics & semiconductors segment accounted for the largest global nanomaterials market share in 2025. The massive demand is mainly due to the increasing usage in conductive layers, dielectric and protective coatings, CMP/cleaning chemistries, and thermal interface solutions that support device reliability and miniaturization. Growth is reinforced by rising chip complexity, higher power density, and greater thermal management requirements across consumer electronics, industrial automation, and EV power electronics. Nano-engineered materials enable improved performance consistency in precision-driven manufacturing environments.

The energy storage segment is expected to grow at the fastest pace, with a CAGR of 14.8% over the forecast period, driven by expanding EV and stationary storage deployments and the need for conductive and performance-enhancing additives in electrodes, separators, and protective coatings. Nanomaterials improve electrical conductivity pathways, mechanical integrity, and electrode utilization, thereby delivering better power capability and cycle stability under fast-charging and high-throughput conditions. In addition, nano-enabled coatings and additives are increasingly used to stabilize interfaces and manage heat, strengthening adoption across next-gen battery designs.

The polymers & composites segment represents another major growth pocket, projected to grow at a CAGR of 13.5% over the analysis period, as nano-enabled reinforcement improves strength, stiffness, conductivity, and functional performance across transportation, industrial, and consumer applications. Nanomaterials enhance crack resistance, fatigue life, and barrier properties while enabling lightweighting, which is critical for automotive and mobility platforms aiming to improve efficiency. Growth is reinforced by higher adoption of advanced composites in industrial equipment and renewable systems.

Nanomaterials Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Nanomaterials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching a value of USD 7.87 billion, and is projected to reach USD 8.95 billion in 2026. The region’s leadership is supported by its massive manufacturing base across electronics, batteries, specialty chemicals, and engineered materials. The demand is strengthened by the high-volume consumption of nano-enabled additives in conductive applications, performance coatings, and lightweight composites used in industrial production. In addition, the large-scale investments in EV supply chains and stationary storage are increasing the pull for nano-carbons and functional oxides that improve electrode conductivity and durability.

China Nanomaterials Market

The China market is expected to be valued at USD 3.97 billion in 2026, accounting for ~19% of global revenues, driven by its leadership across electronics manufacturing, battery cell production, and downstream industrial ecosystems that consume nano-enabled materials at scale. China’s broad base of component manufacturing also increases the product uptake for thermal management, EMI shielding, and performance enhancement in advanced parts.

To know how our report can help streamline your business, Speak to Analyst

India Nanomaterials Market

The India market is expected to reach USD 0.91 billion in 2026, representing roughly 4% of global revenues. Demand is driven by expanding industrial manufacturing, rising infrastructure activity, and the increasing adoption of advanced performance additives in coatings, polymers, and construction-linked materials.

North America

North America reached USD 5.86 billion in 2025 and is projected to increase to USD 6.59 billion in 2026, supported by technology-driven demand across electronics, energy storage, aerospace-grade composites, and specialty coatings. The region benefits from strong R&D intensity and commercialization pathways that the enable faster adoption of high-performance nanomaterials in advanced applications. In addition, growth in EV and stationary storage deployments is strengthening the demand for nano-carbons and functional oxides used to enhance conductivity, cycle stability, and electrode performance.

U.S. Nanomaterials Market

The U.S. market is anticipated to be valued at USD 5.81 billion in 2026, accounting for ~28% of global revenues, supported by the robust demand from advanced electronics, energy storage, defense, textiles, and automotive industries. The product adoption is reinforced by strong downstream qualification ecosystems, where performance, reliability, and consistency drive higher-value purchasing decisions.

Europe

The Europe market reached a valuation of USD 3.84 billion in 2025 and is projected to grow at 12.2% over the forecast period. The region is shaped by strong specialty chemicals capabilities, advanced industrial manufacturing, and the growing integration of nano-enabled materials in electronics, automotive systems, and high-performance coatings. The region is increasingly focused on performance materials that deliver durability, lightweighting, and energy-efficiency improvements, supporting the demand for nanocarbons, nanoclays, and functional oxides.

Germany Nanomaterials Market

The Germany market is expected to reach USD 0.99 billion in 2026, accounting for ~5% share of the global market. The demand is supported by its strong base of advanced manufacturing, automotive engineering, specialty chemicals, and industrial equipment production. High-performance requirements in coatings, composites, and precision industrial formulations reinforce product demand.

U.K. Nanomaterials Market

The U.K. market is expected to reach USD 0.61 billion in 2026, accounting for approximately 3% of global revenues. The product demand is supported by steady demand in specialty coatings, advanced materials development, and select electronics and industrial manufacturing applications. The product adoption is driven by requirements for enhanced durability, protective performance, improved conductivity, and functional upgrades in engineered polymer systems and formulated products.

Rest of the World

The rest of the world reached USD 0.73 billion in 2025 and is projected to rise to USD 0.83 billion in 2026, supported by gradual industrial expansion, urbanization-led infrastructure development, and increasing adoption of performance additives in coatings, polymers, and construction-linked formulations. While the region remains smaller in absolute size, the demand is improving as manufacturing capabilities expand and downstream users adopt nano-enabled materials to enhance durability, barrier properties, and mechanical performance in cost-sensitive environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansion and Collaborations Emerge as Key Strategies of Leading Players to Strengthen Industry Position

The global market is led by major players such as nano-specialists, including Cabot Corporation, OCSiAl, Resonac, NanoXplore, Nanocyl, and American Elements. The companies are making investments in research & development and collaborating with other prominent technology providers to gain a competitive advantage. Companies OCSiAl, NanoXplore, and Cabot have invested significantly in capacity expansion, product innovation, and collaboration with government bodies, which is set to create a favorable environment for market growth. Overall, competitive advantage is increasingly moving to players that can combine scale, consistent nano-quality, and co-development.

LIST OF KEY NANOMATERIALS COMPANIES PROFILED

- American Elements (U.S.)

- Borregaard (Norway)

- Cabot Corporation (U.S.)

- Meta Materials Inc (Canada)

- Nanocyl (Belgium)

- Nanorh (India)

- NanoXplore (Canada)

- OCSiAl (Luxembourg)

- Resonac (Japan)

- Suzhou Tsingcarbo Nanomaterials Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- November 2025: OCSiAl announced the signing of a land lease for developing its flagship Luxembourg-based graphene nanotube production center in Differdange. The move signified a major scale-up step for graphene nanotube manufacturing capacity.

- July 2025: Cabot Corporation launched LITX® 95F, a conductive carbon engineered for lithium-ion batteries used in energy storage systems, targeting enhanced conductivity and longer cycle life for ESS applications. The product is positioned to help battery makers improve electrode network formation and maintain stable performance under high cycling intensity typical of grid-scale storage.

- April 2025: Canatu signed a one-year joint development agreement (JDA) with DENSO to improve the performance of Canatu’s carbon nanotubes for demanding applications. The collaboration highlights the shift toward OEM-linked co-development, where nano-material performance validation and customization are increasingly required to accelerate qualification and scale-up in automotive and electronics supply chains.

- November 2024: OCSiAl opened its first European graphene nanotube production facility in Belgrade, Serbia, with a capacity of 60 tons/year for graphene nanotube synthesis and dedicated dispersion lines. The company also outlined an expansion roadmap to increase output (including plans referenced for expansion toward the end of 2025) and to strengthen supply for battery and polymer customers in Europe.

- September 2024: Resonac and Soitec signed a joint development agreement to develop 200mm SmartSiC™ silicon carbide wafers, supporting high-performance SiC adoption for next-generation EV-linked power devices. The collaboration aims to strengthen material readiness for scaling SiC wafer supply as EV inverters and fast-charging systems shift toward higher-efficiency power electronics.

- September 2024: Cabot Corporation was selected for an award negotiation of up to USD 50 million from the U.S. DOE to support a new U.S.-based facility producing battery-grade CNTs and conductive additive dispersions at commercial scale. The project is positioned to strengthen the domestic supply of conductive nanomaterials for lithium-ion battery value chains and improve resilience for EV and ESS customers.

REPORT COVERAGE

The market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 18.30 billion in 2025 and is projected to reach USD 55.18 billion by 2034.

In 2025, the market value stood at USD 7.87 billion.

The market is slated to exhibit steady growth at a CAGR of 13.1% during the forecast period of 2026-2034.

The electronics & semiconductors end use segment led in 2025.

The expansion of electronics and advanced semiconductor manufacturing is a key factor expected to drive market growth.

Cabot Corporation, OCSiAl, NanoXplore, Nanocyl, Resonac, and American Elements are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Battery performance enhancement and conductive additives are major factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us