Naval Actuators and Valves Market Size, Share & Russia-Ukraine War Impact Analysis, By Platform (Aircraft Carriers, Destroyers, Frigates, Corvettes, Offshore Patrol Vehicles, and Others), By Type (Linear Actuators and Rotary Actuators), By Application (Valves & Actuation, Propulsion System Valve Control, Weapon Handling & Release System, Carrier Flight Deck Operations, Radar Deployment Operations, Navigation System, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

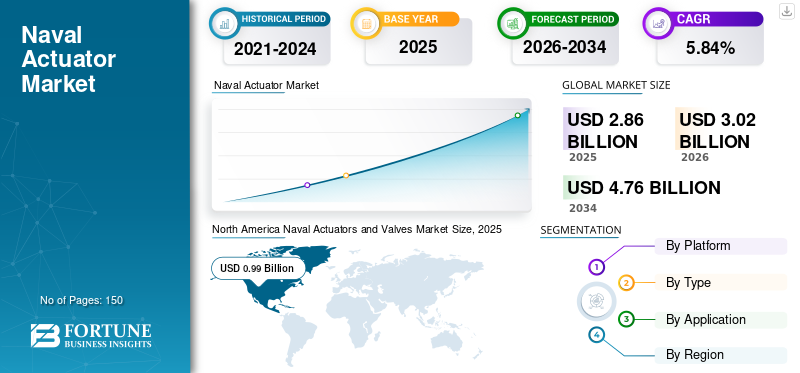

The global naval actuators & valves market size was valued at USD 2.86 billion in 2025. The market is projected to grow from USD 3.02 billion in 2026 to USD 4.76 billion by 2034, exhibiting a CAGR of 5.84% during the forecast period. North America dominated the naval actuators & valves market with a market share of 34.74% in 2025.

Naval actuators and valves are used in a wide variety of naval systems, including safety systems, auxiliary systems, and navigation systems. Naval valves are used to control, direct, and regulate the flow of various types of liquids, steam, gas, and all fluids such as mills and grains. Different valve types are used depending on the customer's specific application. The most commonly used valves include gates, butterflies, angles, and ball plugs. These valves are made of bronze, iron, steel or PVC and are suitable for high pressures and temperatures. In addition, valves are fitted with actuators that monitor pressure and flow when the two values must match. There are different types of actuators including pneumatic, hydraulic, electric, mechanical, hybrid, and manual.

The global naval actuators and valves market share is experiencing significant growth due to increased sea trading activity. Naval actuators and valves enable a valve control mechanism to control flow through the valve. Naval valves are used on ships to control fluid flow through the ship's piping and mechanical systems. Naval propulsion systems are valve control systems designed to convert various forms of energy into mechanical motion to open and close valves and can be used on naval vessels.

Download Free sample to learn more about this report.

Naval Actuators & Valves Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.86 Billion

- 2026 Market Size: USD 3.02 Billion

- 2034 Forecast Market Size: USD 4.76 Billion

- CAGR: 5.84% from 2026–2034

- North America dominated the market with a 34.74% share in 2025.

- The Others ship type segment is expected to lead the market, driven by high procurement of amphibious warships, surface combatants, and support vessels.

- The Linear Actuators segment dominates the market due to its reliability, simple design, and extensive use in naval applications.

Asia Pacific

Fastest-growing region, driven by rising maritime trade and increasing naval modernization programs.

North America

Projected to reach USD 0.99 billion in 2025, supported by growing defense shipbuilding and maritime transport investments.

Europe

Expected to grow steadily, driven by increasing demand for commercial and naval ships and adoption of advanced actuator technologies.

U.S.

Leads the regional market due to strong naval defense spending and expanding shipbuilding activities.

Japan

Projected to reach USD 0.12 billion in 2025, supported by ongoing naval modernization and maritime security initiatives.

Read More

RUSSIAN-UKRAINE WAR IMPACT

Due to Russia-Ukraine War Global Cargo Supply Chain and Global Shipping Industry Impacted Negatively

The Russia-Ukraine war severely affected Ukraine’s shipping sector, including its ports. Conflicts forced operators to divert cargo and vessels. Ukrainian port closures caused severe disruption to European and other supply chains. This caused a severe food crisis due to lack of maritime logistics and connectivity. Shipments of leading players to and from Ukraine and Russia have been suspended due to unforeseen operational impact. Important routes to the Black Sea, especially Odessa and the Sea of Azov, were blocked.

About 2,000 sailors were stranded on 94 ships in Ukrainian ports when the war began. These numbers have decreased slightly. About 80 merchant ships were blocked in the Black Sea and the Sea of Azov for many months. Before the war, Russia occupied up to 90% of Ukraine's Black Sea ports. Russian ships have also been banned from the U.K and EU ports and have been detained for suspected sanctions violations.

In January 2022, French warships detained the Russian roll-on/roll-off cargo ship Baltic Leader en route to St. Petersburg, and more than a dozen superyachts belonging to Russia were confiscated.

Naval Actuators & Valves Market Trends

Naval Strike Missile (NSM) Developed with Control Actuator System (CAS) Technology for Advanced Operations to Drive Market Growth

Control actuator system of the naval strike missile is a separate operational subsystem responsible for controlling the trajectory of the missile by moving the fins in response to commands from the navigation and control system. The CAS, and especially its AIE (Actuator and Ignition Electronics) unit, is also responsible for starting and sequencing the rocket's various power devices and starting the rocket's engine.

Three separate and independent actuators or torque generators to drive the aerodynamic control surfaces are as follows

- Four fin anchors.

- Robust and self-contained electronic unit or Actuator and Ignition Electronics (AIE) that includes power conversion, closed position loop, motor control, self-diagnosis, power supply, and rocket motor start and sequence.

- Connecting cables between AIE and torque generators.

- In January 2023, Kongsberg Defense and Aerospace (KONGSBERG) was awarded a major contract by the Australian Federal Government for Naval Strike Missiles (NSM) and support equipment.

- North America witnessed naval actuators and valves market growth from USD 905.9 Million in 2021 to USD 837.1 Million in 2022.

Download Free sample to learn more about this report.

Naval Actuators & Valves Market Growth Factors

Increased Adoption of Advanced Naval Vessels around the World to Aid Market Expansion

Naval vessels make extensive use of valves and actuators to efficiently operate a variety of systems aboard ships such as weapon release system, navigation system, and hydraulic system.

- In April 2020, Kratos Defense and Security Solutions, Inc, a leading provider of national security solutions, announced that its Kratos Unmanned Systems Division (KUSD) has been selected to participate in an open-ended, multi-entry contract. (IDIQ-MAC) supporting USV (USV) Family of Systems (FoS). The USV FoS includes the platforms and systems that will make up the future unmanned surface fleet of the U.S. Navy. With a maximum contract amount of USD 982.1 million for all of its IDIQ-MAC orders, the government intends to support, maintain, and modernize USV systems and subsystems to meet the Program Executive Agency's current and future unmanned maritime systems operational requirements.

The Draper Laboratory, a non-profit research organization based in Massachusetts, U.S., is one of the 40 companies shortlisted by the U.S. Navy to develop actuator technology, among other advanced technologies. Such research & development of naval actuators and valves is expected to boost the global market.

Surging Demand for Naval Fleet by Armed Forces to Drive Market Growth

Due to the profound changes in the international strategic landscape, the configuration of the international security system has been undermined by the growing hegemonies, unilateralism, and power politics that fueled several ongoing global conflicts. Military powerhouses, such as the U.S., the U.K., China, and India, have been focused on augmenting their naval firepower and several fleet modernization and procurement contracts are underway to address the evolving threats to their national security.

- In March 2019, the U.S. expedited its plans to achieve a proposed 355-ship fleet. The new plans outlined a rough annual expenditure of USD 40 million for fleet maintenance. According to its 30-year shipbuilding plan, the U.S. aims to procure 55 new ships to achieve an effective fleet-size of 314 ships by 2024.

In the Asia Pacific region, prominent countries, such as China and India, are also enhancing their naval fleet size and capabilities to achieve technological superiority over their rival countries.

RESTRAINING FACTORS

Maintenance Delay and Increasing Maintenance Cost Hinder the Market Growth

Naval shipyards face persistent and significant maintenance backlogs that limit the operational readiness of navy's fleets. There are issues associated with different actuators used in different applications. For electro-hydraulic linear actuators, fluid leakage reduces efficiency and creates cleanliness issues. It also requires regular monitoring and maintenance of pumps, fluid tanks, motors, and drain valves. Additionally, electric actuators require proportionally large valves, compressors, and regulators for various operations, adding complexity and cost.

Therefore, major sources of damage such as permanent seal wear, improper assembly or maintenance, risks associated with steam valves, and poor control quality inhibit the actuator market growth.

Navy ships are getting fewer and fewer hours as maintenance delays and costs mount. It is a troubling trend that comes as the U.S. struggles to keep up with China's growing fleet. Operating and support costs rose by about USD 2.5 billion across 10 ship classes, while the number of hours ships operated or trained fell over the 10-year period ending in 2021, according to a report by the Government Accountability Office. Fleet maintenance delays, damage, and cannibalization of parts—moving them from one ship to keep another running—increased during this period.

Segmentation Analysis

By Platform Analysis

Others Segment will Grow at Impressive Rate due to High Demand for Naval Ships

By platform, the market is divided into aircraft carriers, destroyers, frigates, corvettes, offshore patrol vehicles, and others.

The others segment is expected to be the largest market from 2023 to 2030. In the others segment, amphibious warships, large surface combatant, small surface combatant, combat logistics force, and support vessel, are included. The high demand and procurement of these naval ships make the others segment largest in the market share. The frigates segment is the fastest growing as the number of procurements is inline by many countries. The frigates segment is expected to hold a 17% share in 2025.

- In November 2022, the U.K. Ministry of Defense awarded British aerospace firm BAE Systems a USD 4.98 billion contract to build the Royal Navy's next five City-class Type 26 Frigates. British Prime Minister Rishi Sunak announced the agreement on 15 November at the G20 intergovernmental meeting. The contract represents the next phase of the Type 26 or City-class ship program. Also known as the Global Combat Ship (GCS) program, involves the construction of eight City-class battleships.

By Type Analysis

Linear Actuators to Lead Backed by Extensive Use and Reliability

By type, the segment is bifurcated into linear actuators and rotary actuators. Different actuators are used in naval applications depending on the type of actuation. As of 2022, linear actuator is the largest and fastest growing segment in terms of revenue in the market of naval actuators and valves. Linear actuators are simple in construction and require little effort to operate. Linear actuators are used in a wide variety of applications, are fast to operate, and are more reliable than other types of naval actuators and valves. Due to their ease of use, these actuators are preferred over other actuators in naval applications. As a result, the demand for linear actuators is expected to continue increasing during the forecast period.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Increased Operations Demand for Carrier Flight Deck Operations to Aid Segment Growth

By application, the market is bifurcated into propulsion system valve control, weapon handling & release system, carrier flight deck operations, radar deployment operations, navigation system, and others.

The carrier flight deck operations segment is projected to be the largest and fastest growing segment in the market from 2023 to 2030. Optical landing system, Fresnel Lens Optical Landing System (FLOLS), and steering system make up the segment. Carrier flight deck operations are built into many naval ships and cargo ships and require actuator and valve support to function properly. The propulsion system valve control segment is projected to generate USD 0.25 billion in revenue by 2025.

- The navigation system segment is expected to hold a 10.38% share in 2026.

- For example, the steering system, which is part of the carrier flight deck operations, uses the ship's actuators to function properly.

REGIONAL ANALYSIS

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the rest of the world. Asia Pacific is expected to be the fastest growing region in the forecast period.

North America Naval Actuators and Valves Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America dominated the global market in 2025, with a market size of USD 0.99 billion. The major factors behind the naval actuators & valves market growth in the North America region are increasing manufacturing of defense and merchant and cargo ships, growing reliance on domestic and international maritime transport, and investment in naval forces.

Asia Pacific

Moreover, Asia Pacific is expected to be the fastest growing region in the market during the forecast period. The use of maritime transport for trade and the need for efficient maritime transport are factors driving the market in the region.

- The naval actuators & valves market in Japan is expected to reach USD 0.12 billion by 2025.

- China is projected to witness a strong CAGR of 8.47% during the forecast period.

Europe

The Europe market is expected to grow moderately due to increasing demand for commercial and naval ships in countries such as the U.K., France, and Germany. Most companies operating in the region are focused on developing low-cost, advanced autonomous actuators and valves with advanced capabilities.

- Europe is anticipated to grow at a CAGR of 4.39% during the forecast period.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa have a smaller market share for naval actuators and valves due to limited opportunities for companies. Increasing industrialization in key countries, such as Brazil, South Africa, and Saudi Arabia, is expected to accelerate the market growth in the coming years.

KEY INDUSTRY PLAYERS

Large Companies are Focused on Launching Cutting-edge Actuators and Valves to Strengthen Product Portfolio

The new security environment, fueled by heightened geopolitical instability in several countries, is driving demand for advanced naval systems. Players invest heavily in acquiring new naval resources to secure long-term contracts and expand their global presence. In addition, continuous research & development is improving the accuracy and efficiency of subsystems and other technologies aboard navy ships. The market is fragmented with many global naval actuators and valves players present in the market. Prominent naval actuators and valves players in the market studied include MOOG Inc., Honeywell International Inc., Rotork plc, Emerson Electric Co., and Curtiss-Wright Corporation.

List of Top Naval Actuators & Valves Companies:

- MOOG Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- Rotork plc (U.K.)

- Emerson Electric Co. (U.S.)

- Curtiss Wright Corporation (U.S.)

- Wartsila (Finland)

- Rockwell Automation, Inc. (U.S.)

- Woodward, Inc (U.S.)

- Flowserve Corporation (U.S.)

- Schlumberger Ltd (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2022 - Elettronica signed a contract to equip two Indonesian Navy 90m offshore patrol vessels currently under construction at PT Daya Radar Utama shipyard with the Navy's Electronic Radar Countermeasure System. An Indonesian shipyard plans to build more of her 90-meter maritime patrol ships for the navy. This is the first contract in Indonesia in the history of Elettronica, one of the world leaders in electronic warfare for over 70 years and one of the best jammers in the world.

- August 2022 - General Dynamics National Steel and Shipbuilding Corporation (NASSCO) has been awarded a USD 1.4 million contract for the detailed design and construction of three U.S. Navy vessels. The contract includes the construction of two John Lewis-class (T-AO) fleet oilers, T-AO 211 and 212, and one Expeditionary Sea Base (ESB) vessel, ESB 8. Also included is the option to procure an additional refueling vessel, the T-AO 213. The latest deal follows the recently awarded USD 600 million contract modification for long-term lead material procurement for ESB 8, T-AO 211, and 212.

- June 2022 - Naval Surface Warfare Center, Philadelphia Division receives initial order from Other Transaction Authority (OTA) for the design, development, and supply of a miniature actuator test rig for the evaluation of electrohydraulic actuators by the Maritime Sustainment Technology Innovation Consortium (MSTIC).

- April 2022 – Triumph has been awarded a multi-year contract to manufacture actuators and control systems for the U.S. Navy's Jammer Mid-Band (NGJ-MB) pods. The contract, signed by Raytheon Intelligence & Space, covers the production needs of Low-Rate Initial Production (LRIP) Lot I and II. The multi-year deal also includes product manufacturability improvements and his one-off engineering.

- January 2022 - BURCKHARDT COMPRESSION and KB DELTA entered into a strategic partnership for compressor valve parts. Burckhardt Compression serves as a global distributor and service partner for KB Delta's product portfolio of compressor valve components. KB Delta and Burckhardt Compression have worked together for several years as KB Delta supplies Burckhardt Compression.

REPORT COVERAGE

The research report offers a thorough analysis of the industry and focuses on important factors such as top manufacturers, product categories, and popular uses for the service. The report also identifies significant developments in the market and provides insights into market dynamics trends. The report includes several additional factors in addition to those mentioned above that have influenced the market's growth prospects in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.84% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

| Segmentation |

By Platform

|

|

By Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global naval actuators and valves market size was valued at USD 2.86 billion in 2025 and is projected to grow from USD 3.02 billion in 2026 to USD 4.76 billion by 2034, exhibiting a CAGR of 5.84% during the forecast period.

The market gore at a CAGR of 5.84% over the forecast period.

The market is primarily driven by the increased adoption of advanced naval vessels, growing sea trade activities, and modernization of naval fleets. Rising investments in defense shipbuilding and the development of advanced actuator control systems are also boosting demand.

North America dominated the market in 2025 with a 34.74% share, attributed to strong naval procurement programs, high defense budgets, and advanced shipbuilding infrastructure in the U.S. and Canada.

The Asia Pacific region is expected to grow at the fastest rate due to increasing naval investments, rising maritime trade, and fleet modernization programs in countries such as China, India, and Japan.

The market primarily features linear actuators and rotary actuators. Linear actuators are the most widely used due to their ease of operation, reliability, and suitability for a variety of naval applications.

The war has disrupted global shipping routes, especially in the Black Sea and Sea of Azov, leading to delays in cargo movement, suspension of shipping operations, and restricted access to ports. This has indirectly affected supply chains and procurement in the naval sector.

They are used in propulsion system valve control, weapon handling & release systems, carrier flight deck operations, radar deployment, and navigation systems, ensuring efficient operation of shipboard mechanical systems.

Key companies include MOOG Inc., Honeywell International Inc., Rotork plc, Emerson Electric Co., Curtiss-Wright Corporation, Wartsila, Rockwell Automation, Woodward Inc., Flowserve Corporation, and Schlumberger Ltd.

Trends include the integration of Control Actuator Systems (CAS) in naval strike missiles, development of autonomous actuator systems, and advanced materials for higher durability under extreme marine conditions.

Challenges include high maintenance costs, technical failures such as fluid leakage in hydraulic actuators, delays in ship maintenance schedules, and the complexity of operating large-scale naval valve systems.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us