Next-Gen Military Avionics Market Size, Share & Industry Analysis, By Component (Hardware, Software, & Services), By Avionics System Type (Flight Control & Management Systems, Navigation Systems, Communication Systems, Surveillance & Reconnaissance Systems, & Others), By Technology Architecture (Federated Avionics Architecture, Edge Computing in Avionics, MOSA, & Others), By Operational Capability (Network-Centric Warfare Avionics, Multi-Domain Operations Integration, & Others), By Installation Type (Line Fit, Retrofit, & Mid-Life Upgrade Programs), By Platform, and Regional Forecast 2026-2034

Next-Gen Military Avionics Market Size and Future Outlook

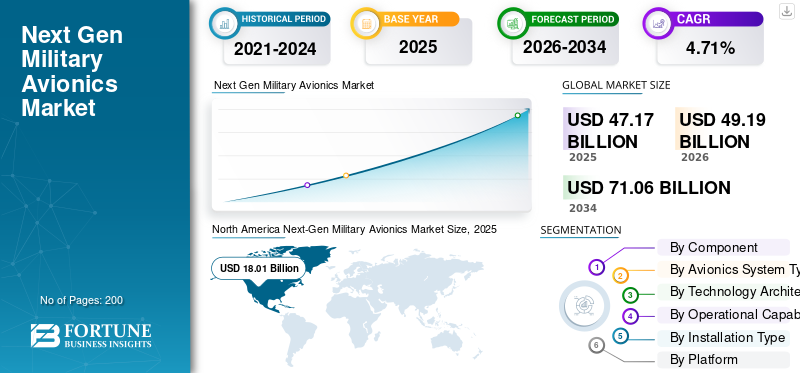

The next-gen military avionics market size was valued at USD 47.17 billion in 2025. The market is projected to grow from USD 49.19 billion in 2026 to USD 71.06 billion by 2034, exhibiting a CAGR of 4.71% during the forecast period. North America dominated the next gen military avionics market with a market share of 38.18% in 2025.

The market covers digital brain and nervous system of military aircraft and UAS mission computers, cockpit/HMI, comms/datalinks, navigation, sensors/radar, EW suites, situational awareness and the software/integration that fuses these for combat missions sold both as line-fit on new platforms and as retrofit/MLU upgrades to extend fleet relevance. It is increasingly defined by open, modular architectures that let operators swap capabilities faster and avoid vendor lock-in.

The market growth is being driven by high-threat, networked wars (EW + contested comms), faster technology refresh cycles, and the need to push compute/AI to the edge for sensor fusion, autonomy, and mission re-tasking while keeping avionics cyber-resilient and upgradeable via MOSA-driven acquisition.

Major key players in the market include Collins Aerospace (RTX), L3Harris, BAE Systems plc, Thales Group, and Leonardo S.p.A. These players are focusing on scaling MOSA-compliant avionics to make upgrades faster and third-party capable, pushing platform-agnostic aircraft missionization and MOSA-enabled integration and adopting advanced EW/countermeasures and resilient electronics to sustain market competition.

Download Free sample to learn more about this report.

Next-Gen Military Avionics Market Trends

Growing Modernization Program and Digital Engineering is Key Market Trend

The market is shifting toward continuous modernization programs such as mission apps updated in blocks, open interfaces, and more compute pushed to the edge for fusion and autonomy. Programs are also moving to digital engineering/digital twin workflows to compress upgrade cycles (simulate before flight test, reduce regression risk, and speed certification evidence). This directly increases spending on software, integration, test automation, and cyber-hardening.

OEMs are investing in open ecosystems (third-party apps, modular mission computing, scalable display/network stacks) as the it upgrades speed and performance. DoD MOSA guidance formalizes this direction and pushes buyers to demand portability and modularity in contracts.

For instance, in February 2026, NIAR disclosed a USD 100 million USAF-sponsored cooperative agreement for digital engineering to support sustainment/mods of legacy platforms and to continue development of aircraft digital twins (e.g., F-16, B-1), reinforcing the shift to digital-first upgrade pipelines.

Market Dynamics

MARKET DRIVER

Download Free sample to learn more about this report.

Increasing Budgets Flowing into Software-Defined, MOSA-Ready Mission Systems Drives Market Growth

Next-gen military avionics market growth is being driven by rising defense spending on software-defined, MOSA-ready mission systems. Armed forces need aircraft that can operate in contested electromagnetic environments, share data securely, combine inputs from multiple sensors, and accept faster upgrades without waiting for full airframe replacement. There is a growing demand from fleet sustainment, where operators are modernizing legacy aircraft with new mission computers, displays, datalinks, and electronic warfare suites to keep them combat-relevant for longer. MOSA is also changing buying patterns, as militaries are increasingly funding repeatable upgrade blocks based on open architecture, modular computing, and software integration rather than buying fixed, closed hardware only once. DoD formally positions MOSA as a strategy to improve affordable acquisition and sustainment over the full life cycle, while NATO and U.S. airpower doctrine continue to emphasize electromagnetic warfare resilience and operations in contested spectrum conditions.

- For instance, in February 2026, Curtiss-Wright announced it was selected by Boeing to supply MOSA-aligned mission computers for the USAF C-17 Flight Deck Obsolescence and Technology Refresh program.

MARKET RESTRAINTS

Integration/Certification Friction, Supply Chain, and Program Schedule Risk Hamper Market Expansion

Avionics modernization is slowed by integration risk (legacy wiring, EMI/EMC, safety cases), flight control systems and test capacity, and certification gates especially during upgrades in mission computers, EW, and new radar modes. Next-gen systems also rely on constrained items (high-end processors, FPGA/SoC, GaN AESA modules), so vendors often face long lead times, redesigns, and obsolescence churn.

Another restraint for the market is the heavy dependence on large defense programs. When a major platform is delayed, the impact spreads across the supply chain and partner countries, leading to postponed deliveries, redesign work, and retrofit backlogs. In many cases, the complexity of modernization itself becomes a key reason for slower deliveries and rising costs.

MARKET OPPORTUNITIES

Radar/EW Refresh Wave and Upgradeable Architectures Exported Across Global Fleets Creates Significant Market Opportunities

A prominent market opportunity is the installed base fighters, transports, and rotorcraft that will stay in service for decades demanding AESA radar refresh, EW upgrades, secure datalinks, and mission computing and these work packages are avionics-heavy by design. Europe’s high operational tempo and rearmament cycle is transforming into concrete radar and mission-system production orders, creating multi-year demand not just for radars but also for power, cooling, processing, integration labs, and mission software.

For instance, in January 2026, U.K. DE&S announced a USD 441.5 million contract to manufacture/deliver 40 ECRS Mk2 AESA radars for RAF Typhoons explicitly framed as a major capability uplift with long-term integration work.

MARKET CHALLENGES

Cyber Compliance, AI Governance and Trustworthy Autonomy in Safety-Critical Avionics Can Hinder Market Growth

Avionics is becoming a cyber-battlefield as open architectures and connected mission systems widen the attack surface, so primes and their sub-tiers must secure development, supply chain, and compliance often at significant cost particularly for smaller suppliers. Similarly, buyers demand more AI at the edge (fusion, targeting support, autonomy). However, aviation-grade systems must meet safety, testability, explainability, and authorization-to-operate requirements that are slower than commercial AI cycles. To focus on these while keeping upgrade cadence fast, modern avionics needs rapid fielding without breaking airworthiness, interoperability, or classified security boundaries. Government policy currently are explicitly pushing faster AI adoption, which raises the bar on how quickly suppliers must industrialize reliable AI-enabled mission functions.

SEGMENTATION ANALYSIS

By Component

Software Segment Grows Due to MOSA & Block Upgrades Turn Avionics into A Continuous Release Model

The market by component is divided into hardware, software, and services.

The software segment is estimated to be the fastest growing during the forecast period of 2026-2034 with a highest CAGR of 6.73%. Software accelerates as operators move to frequent capability drops (mission apps, sensor-fusion algorithms, EW libraries, cyber hardening, and datalink waveforms). Open interfaces reduce reduced the work from scratch, hence budget shifts to new features and rapid re-certification rather than one-off bespoke builds catalyze the segmental growth.

The hardware segment is accounted for the largest next-gen military avionics market share in 2025 with a 67.64% market share and estimated to register a CAGR of 4.00% during the forecast period.

By Avionics System Type

Mission Systems Segment is Fastest Growing Due to Sensor Fusion & Open Computing's Battle Brain Focus

The market by avionics system type is divided into flight control & management systems, navigation systems, communication systems, surveillance & reconnaissance systems, radar systems, electronic warfare systems, mission systems, and others.

The mission systems segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 6.36%. This growth is due to the modern upgrades starting with mission computing and middleware (OMS/MOSA stacks) as it unlocks faster insertions of new sensors, new EW techniques, and new datalink capabilities

The radar systems segment accounted for the largest market share in 2025 with a 18.60% market share and estimated to have a CAGR of 4.28% during the forecast period.

By Technology Architecture

AI-Embedded Avionics Grows due to Demand for Faster Target Recognition and Sensor Prioritization

The market by technology architecture is divided into federated avionics architecture, edge computing in avionics, AI-embedded avionics, cloud-connected avionics, MOSA (Modular Open Systems Approach), digital twin enabled systems and others.

The AI-embedded avionics segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 6.58%. AI at the edge expands quickly as forces demand faster target recognition, sensor prioritization, threat cueing, and autonomy features that reduce pilot workload and improve survivability. As compute headroom rises in mission computers, buyers demand immediate operational payoff AI-enabled fusion and taking faster decisions offers these without waiting for entirely new aircraft fleets.

The MOSA (Modular Open Systems Approach) segment accounted for the largest market share in 2025 with a 22.14% market share and estimated to record a CAGR of 5.90% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Operational Capability

MDO Integration Booms Due to Cross-Domain Kill Chains & Joint C2 Acceleration

The market by operational capability is divided into network-centric warfare avionics, multi-domain operations integration, swarm coordination system, autonomous navigation, and stealth-optimized avionics.

The multi-domain operations integration segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 6.11%. MDO integration expands quickly as militaries prioritize linking air assets with space, cyber, maritime, and ground fires into time-sensitive kill chains. This capability forces upgrades across mission computers, gateways, datalinks, and software-defined interoperability creating increasing demand.

The network-centric warfare avionics segment accounted for the largest market share in 2025 with a 32.26% market share and estimated to hold a CAGR of 3.70% during the forecast period.

By Installation Type

Mid-Life Upgrade Programs Grows as Extending Existing Fleets Offers the Lowest-Cost Path to Near-Term Capability

The market by installation type is divided into line fit (OEM), retrofit, and mid-life upgrade programs

The mid-life upgrade programs segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 6.00%. The growth is due to most air forces have large legacy fleets with remaining structural life, and avionics upgrades deliver major capability per dollar without buying all-new airframes. These programs bundle multiple subsystems at once (radar, EW, comms, mission computers, cockpit), so they capture the largest integrated contract value.

The line fit (OEM) segment accounted for the largest market share in 2025 with a 40.76% market share and estimated to register a CAGR of 3.50% during the forecast period.

By Platform

eVTOL is Fastest Growing Segment as Mission Concepts Progress from Prototypes Experimentation and Early Fielding

The market by platform is divided into fixed-wing aircraft, rotary-wing aircraft, Unmanned Aerial Systems (UAS), military eVTOL, and space-based military avionics,

The military eVTOL segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 7.86%. eVTOL spending grows quickly off a small base as militaries explore new operational concepts for logistics, ISR, and tactical mobility with lower operating footprints. The avionics stack also includes modern digital features such as fly-by-wire, autonomy-ready navigation and advanced comms, hence has a high share of value in next-gen computing and software-defined control.

The fixed-wing aircraft segment is accounted for the largest market share in 2025 with a 56.57% market share and estimated to register a CAGR of 4.55% during the forecast period.

Next-Gen Military Avionics Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Middle East & Africa, and Latin America.

North America

North America Next-Gen Military Avionics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 18.01 billion, and will maintain a leading share in 2026, with USD 18.60 billion revenue share. The North American market is experiencing significant growth driven by massive U.S. defense modernization, F-35 fleet expansion, and increased AI integration. Other driving factors include rising demand for stealth, Unmanned Aerial Vehicles (UAVs), and enhanced cybersecurity, with major investments from the U.S. and Canada in advanced cockpit, sensor, and communication systems.

U.S. Next-Gen Military Avionics Market

Based on North America's strong contribution, the U.S. market reached USD 17.30 billion in 2025 and is estimated to have a CAGR of 3.75% during the forecast period.

Europe

Europe is projected to grow at fastest growing rate with a CAGR of 6.22% during the forecast period. In 2025, the market value stood at USD 10.67 billion. The European market is experiencing significant growth, driven by urgent defense budget increases, the need to modernize aging fleets, and the integration of AI, electronic warfare (EW), and advanced, secure navigation systems.

U.K. Next-Gen Military Avionics Market

The U.K. market in 2025 was valued at USD 1.24 billion and is estimated to grow at a CAGR of 4.25% during the forecast period.

Russia Next-Gen Military Avionics Market

The Russia market growth in 2025 reached at USD 2.51 billion and is estimated to grow at a CAGR of 9.80% during the forecast period.

Rest of Europe Next-Gen Military Avionics Market

The Rest of Europe market in 2025 was valued at USD 4.67 billion and is estimated to grow at a CAGR of 5.42% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 13.01 billion in 2025 and secures the position of the second-largest region in the market. Growth is driven by rapid military modernization, increasing geopolitical tensions, and rising defense budgets, particularly in China and India.

China Next-Gen Military Avionics Market

The China market in 2025 was valued at USD 5.48 billion and is estimated to grow at a CAGR of 5.33% during the forecast period.

India Next-Gen Military Avionics Market

The India market reached USD 2.15 billion in 2025, and is estimated to grow at a CAGR of 6.28% during the forecast period.

Japan Next-Gen Military Avionics Market

The Japan market in 2025 recorded a share of USD 1.68 billion and is predicted to grow at a CAGR of 7.62% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate during the forecast period. The Latin America market was valued at USD 1.28 billion and Middle East & Africa market reached USD 4.20 billion in 2025. The market is expanding rapidly, driven by defense modernization, geopolitical tensions, and rising adoption of AI-driven, interoperable systems. Key growth drivers include upgrades to aging fleets, increased localized production, and adoption of advanced sensor and electronic warfare systems.

Gulf Countries Next-Gen Military Avionics Market

The Gulf Countries market in 2025 reached at USD 1.93 billion and is predicted to grow at a CAGR of 4.87% during the forecast period.

Brazil Next-Gen Military Avionics Market

The Brazil market in 2025 was valued at USD 0.41 billion and is projected to grow at a CAGR of 1.89%during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

MOSA Modernization Contracts Are Shifting Competition Toward Open, Upgradeable Mission Stacks

The market competition is being defined by companies that can deliver plug-and-play avionics architectures, making future upgrades cheaper and faster. Collins Aerospace (RTX) is pushing MOSA through its Mosarc family via the U.S. Army’s H-60M MOSA avionics upgrade award, positioning it as a reusable architecture play across fleets. Boeing’s C-17 cockpit refresh is pulling in new mission computer hardware (Curtiss-Wright) and signals a broader wave of tech refresh programs where suppliers win by de-risking obsolescence and shortening upgrade cycles.

Suppliers are also racing to own major share of the avionics value chain such as EW suites, secure networking, mission computing, and integration toolchains are being bundled into larger scopes. BAE is expanding its footprint through aircraft EW modernization (e.g., EPAWSS production/installation paths on F-15 variants), keeping EW and mission survivability spend resilient.

LIST OF KEY NEXT-GEN MILITARY AVIONICS MARKET COMPANY PROFILED

- RTX Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- BAE Systems plc (U.K.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Elbit Systems Ltd. (Israel)

- Hensoldt AG (Germany)

- Bharat Electronics Limited (BEL) (India)

- Israel Aerospace Industries (IAI) (Israel)

- Mitsubishi Electric Corporation (Japan)

- Aselsan A.S. (Turkey)

KEY DEVELOPMENT

- February 2026: Elbit to supply Helmet Display and Tracking System (HDTS) for Israeli Air Force UH-60 Black Hawk fleet.

- February 2026: Collins Aerospace (RTX) demonstrates Sidekick mission autonomy software in flight on GA-ASI’s YFQ-42A CCA platform

- February 2026: Israel MoD signs around USD 130 million deal with Elbit to integrate Israeli C2/avionics/EW and DIRCM on CH-53K helicopters.

- December 2025: CEVS (Collins/Elbit) completes Critical Design Review for Zero-G HMDS+ under U.S. Navy IJHMCS, targeting F/A-18E/F and EA-18G integration.

- December 2025: Boeing delivers first B-52 Radar Modernization Program flight-test aircraft with APQ-188 AESA, new mission computers and large cockpit displays for Edwards AFB testing.

REPORT COVERAGE

The global next-gen military avionics market growth analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and next-gen military avionics market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key avionics industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.71% from 2026-2034 |

| Unit | USD Billion |

|

Segmentation |

By Component

By Avionics System Type

By Technology Architecture

By Operational Capability

By Installation Type

By Platform

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 47.17 billion in 2025 and is projected to reach USD 71.06 billion by 2034.

In 2025, the European market value stood at USD 10.67 billion.

The market is expected to exhibit a CAGR of 4.71% during the forecast period.

The AI-embedded avionics segment is expected to hold the highest CAGR over the forecast period.

Increasing budgets for software-defined, MOSA-ready mission systems drives the market growth.

Collins Aerospace (RTX), L3Harris, BAE Systems plc, Thales Group, and Leonardo S.p.A. are the top key players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us