Nuclear Powered Naval Vessels Market Size, Share & Industry Analysis, By Platform (Submarines and Surface Vessels), By Component (Reactor System, Propulsion & Turbine System, Power Generation System, Control & Safety System, Auxiliary Systems, and Others), By Application (Sea-Based Strategic Deterrence, Anti-Submarine Warfare, Anti-Surface Warfare, Intelligence, Surveillance & Reconnaissance, and Others), By End User (Navy and Strategic Defense Forces), and Regional Forecast, 2026-2034

Nuclear Powered Naval Vessels Market Size and Future Outlook

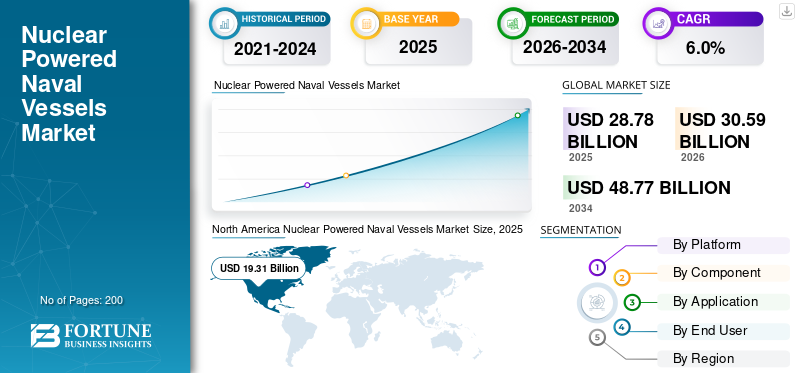

The nuclear powered naval vessels market size was valued at USD 28.78 billion in 2025. The market is projected to grow from USD 30.59 billion in 2026 to USD 48.77 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. North America dominated the nuclear powered naval vessels market with a market share of 67.09% in 2025.

The global nuclear powered naval vessels market includes nuclear powered submarines and selected surface vessels that rely on nuclear reactors and advanced propulsion system integration for long-endurance deployment. The market is being driven by the replacement of the ballistic missile submarine fleet, rising focus on naval capabilities, and continued technological advancements in nuclear propulsion. The growth of the market is also fueled by higher defense budget allocations for strategic deterrence, submarine modernization, and long-cycle expansion of the naval fleet over the long term.

Key players in the market include Huntington Ingalls Industries, General Dynamics, BAE Systems, Naval Group, Rolls-Royce, and TechnicAtome. They are driving the market through submarine construction, reactor integration, and fleet modernization programs rather than just product range. Huntington Ingalls Industries and General Dynamics remain central to the U.S. submarine and carrier base, while BAE Systems supports the U.K.’s Dreadnought, Astute, and SSN-AUKUS pathway, and Naval Group is advancing France’s next-generation strategic submarine program.

Download Free sample to learn more about this report.

Nuclear Powered Naval Vessels Market Trends

Strategic Submarine Recapitalization and Naval Nuclear Infrastructure Expansion Are Emerging as a Major Market Trend

A major trend in the global market is the shift from legacy fleet sustainment to deeper recapitalization of nuclear powered submarines, mainly next-generation ballistic missile submarine programs. The market is no longer being shaped by vessel replacement; it is increasingly driven by investment in yard infrastructure, dry docks, workforce expansion, and broader technological advancements in nuclear propulsion. This is important because the long-term competitiveness of nuclear powered naval vessels now depends as much on industrial readiness and program execution as on platform demand itself.

In May 2025, the U.K. government’s Defense Nuclear Enterprise 2025 Annual Update to Parliament stated that the enterprise is refurbishing dry docks for Astute-class deep maintenance, future-proofing the naval base for Dreadnought and SSN-AUKUS, and supporting a workforce demand projected to exceed 65,000 by 2030.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Ballistic Missile Submarine Replacement and Attack Submarine Modernization Are Driving Market Growth

The major driver for the nuclear powered naval vessels market growth is the steady up-gradation of the ballistic missile submarine fleet alongside continued procurement of nuclear powered submarines for attack and deterrence missions. The market is being supported by programs that are involved in the center of national defense budget priorities and long-term naval capabilities planning. As countries modernize their naval fleet with more capable platforms, the demand for nuclear reactors, advanced propulsion system integration, and next-generation submarine construction continues to support the growth of the market over the forecast period.

MARKET RESTRAINTS

High Investment Requirement and Long Development Cycles are Restraining Market Expansion

Key limitations in the market are the high investment requirement associated with building and maintaining nuclear powered submarines and surface vessels. The integration of nuclear reactors, advanced propulsion system technologies, and stringent safety frameworks increases program complexity, timelines, and costs. With rising defense budget allocations, many countries face budget constraints, balancing submarine programs with broader naval fleet modernization.

MARKET OPPORTUNITIES

Expansion of New Entrants into Nuclear Submarine Programs Creates Significant Market Opportunity

Opportunities in the market are the involvement of new countries in developing nuclear powered submarines through partnerships and technology-sharing. This is propelling the market beyond traditional operators and increasing demand for nuclear reactors, improved propulsion system integration, and specialized shipbuilding skills. As countries aim to boost their naval strength and long-term deterrence, collaborative programs are creating new revenue opportunities for established companies such as BAE Systems and Huntington Ingalls Industries. Countries such as South Korea are also exploring advanced naval nuclear capabilities and next-generation propulsion technologies.

In March 2023, the U.S., U.K., and Australia formally announced the AUKUS submarine pathway. Under this venture, Australia will acquire nuclear powered submarines with support from BAE Systems and U.S. shipbuilders, marking a major expansion of nuclear naval capability into a new country.

MARKET CHALLENGES

Limited Industrial Base and Skilled Workforce Constraints are Challenging Market Expansion

Key challenge in the market is the restricted specialized industrial base and shortage of skilled workforce, which are needed to design, build, and maintain nuclear-powered submarines and related propulsion system infrastructure. Nuclear programs require strict regulations, precise engineering, and lengthy training periods for nuclear-qualified personnel. Even as defense budgets grow and demand for advanced naval capabilities rises, these challenges result in bottlenecks in increasing production. Therefore, the market's growth is limited not by demand but by execution capacity over the long term.

Impact of Ongoing Conflicts

Russia-Ukraine War and Middle East Instability Are Reinforcing Demand for Undersea Deterrence and Fleet Survivability

The impact of the Russia-Ukraine war and the broader Middle East conflicts is strengthening the strategic case for nuclear powered naval vessels, especially nuclear powered submarines built for survivability, deterrence, and long-endurance deployment. These conflicts have pushed governments to re-evaluate naval capabilities, harden force posture, and protect critical sea lines under more contested conditions. In market terms, that is supporting higher priority for the ballistic missile submarine fleet, more resilient naval fleet planning, and stronger long-term backing for nuclear reactors and advanced propulsion system programs, even though the market remains constrained by cost and industrial capacity.

In May 2025, the U.K.’s Defence Nuclear Enterprise 2025 Annual Update to Parliament stated that the importance of the country’s nuclear deterrent had become even more apparent because of the continuing uncertainty and conflict in Europe and rising global threats. Also, SIPRI’s April 2025 update reported that world military expenditure reached a record USD 2.718 trillion in 2024, up 9.4% in real terms, reflecting the wider security deterioration linked in large part to the war in Ukraine and heightened regional tensions.

Segmentation Analysis

By Platform

Submarine Segment Leads the Market Due to Strategic Deterrence Requirements and Undersea Survivability Needs

In terms of platform, the market is bifurcated into submarines and surface vessels.

The submarines segment dominates the global market because nuclear propulsion delivers its greatest operational value in undersea platforms that require stealth, endurance, and long-range persistence. At the global level, the strongest program activity is concentrated in ballistic missile submarine recapitalization and attack-submarine modernization rather than in nuclear-powered surface vessels. The broader fleet picture points the same way: The World Nuclear Association states that, among nuclear-powered ships, most are submarines, while official U.S., U.K., and French nuclear-enterprise updates all show current and future investment flowing primarily into submarine programs such as Virginia, Columbia, Dreadnought, Astute/SSN-AUKUS, Barracuda, and SNLE 3G. That is why submarines remain the dominant platform across the market.

The surface vessels segment is expected to grow at a CAGR of 4.3% over the forecast period.

By Component

Reactor System Segment Dominates the Market Due to Its Central Role in Vessel Endurance And Nuclear Propulsion Performance

On the basis of component, the market is classified into reactor system, propulsion & turbine system, power generation system, control & safety system, auxiliary systems, and others.

The reactor system segment held the largest global nuclear powered naval vessels market share in 2025, because it is the core technology that enables long-endurance deployment, high onboard power availability, and sustained submerged operations in nuclear powered submarines and other nuclear powered naval vessels. Moreover, the reactor system carries the highest strategic and technical value because it anchors the entire propulsion system, safety architecture, and mission endurance of the platform.

The propulsion and turbine system is expected to show the second fastest growth, registering a CAGR of 6.5% over the forecast period.

By Application

Due to the Central Role of Nuclear Submarines in Strategic Deterrence Posture, the Sea-Based Strategic Deterrence Segment Dominates the Market

The market is further divided by application into sea-based strategic deterrence, anti-submarine warfare, anti-surface warfare, intelligence, surveillance & reconnaissance, and others.

The sea-based strategic deterrence segment dominated the global market in 2025, because the highest-value and most strategically protected programs in this domain are tied to the ballistic missile submarine fleet. These platforms sit at the core of national deterrence strategy, resulting funding for nuclear reactors, advanced propulsion system integration, and long-term sustainment tends to remain more resilient compared other applications. Additionally, major nuclear-vessel operators continue to prioritize replacement and modernization of deterrent submarines ahead of most other fleet investments, keeping this application at the center of the market’s long-term demand structure.

The intelligence, surveillance & reconnaissance segment is expected to grow at a CAGR of 5.4% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Navy Segment Leads the Market Due to Direct Operational Control of Nuclear Fleets and Long-Term Platform Sustainment Responsibility

Based on end user, the market is segmented into the navy and strategic defense forces.

The navy segment dominates the global market in 2025, because nuclear-powered platforms are procured, operated, maintained, and modernized through naval institutions; some vessels also serve strategic deterrence missions. The Royal Navy operates the U.K.’s nuclear submarine force, and France’s submarine recapitalization is also tied directly to French naval requirements. That keeps the Navy as the dominant end user because it absorbs the broadest share of procurement, lifecycle support, crew readiness, and fleet sustainment across nuclear powered submarines and other nuclear powered naval vessels.

The strategic defense forces segment is expected to show the fastest market growth, registering a CAGR of 7.1% over the forecast period.

Nuclear Powered Naval Vessels Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Nuclear Powered Naval Vessels Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share for nuclear powered naval vessel solutions, and is anticipated to grow at a CAGR of 5.5% during the forecast period. The region represents the world’s largest operating base of nuclear powered submarines and nuclear-powered carriers with the strongest visible program pipeline for future fleet replacement. The U.S. alone anchors the region through the ballistic missile submarine recapitalization cycle, continued Virginia-class procurement, and ongoing carrier modernization, while the broader Naval Nuclear Propulsion Program supports the full lifecycle of the U.S. nuclear-powered naval fleet.

U.S. Nuclear Powered Naval Vessels Market

Based on the strong contribution of the North American market and the dominance of the U.S. within the region, the U.S. market stood at around USD 19.31 billion in 2025, growing at a CAGR of 5.5% during the forecast period.

Europe

Europe held a market share of 24.82% in 2025. Europe is the second major region in the market and is heavily invested in submarine-led nuclear programs. The regional share is focused in the U.K., France, and Russia, with the U.K. advancing Dreadnought, Astute, and SSN-AUKUS, France progressing SNLE 3G and Barracuda, and Russia continuing to underpin a large nuclear-submarine fleet. The region, therefore, benefits from both strategic deterrence renewal and attack-submarine modernization, but growth is still constrained by industrial capacity, workforce availability, and the long execution cycle of naval nuclear programs.

France Nuclear Powered Naval Vessels Market

France’s market reached approximately USD 1.32 billion in 2025, equivalent to around 18.42% of the market revenue.

U.K. Nuclear Powered Naval Vessels Market

The U.K. market stood at around USD 2.16 billion in 2025, representing roughly 30.21% of the market revenue.

Asia Pacific

Asia Pacific dominated the global market and is anticipated to grow at a CAGR of 8.4% over the forecast period. Asia Pacific is an emerging region and holds a relatively small market for submarines, mainly dominated by China and India. The region has been witnessing high demand for submarines due to the need to have deterrence capabilities from the sea, balancing strategic considerations, and the growth of indigenous development capabilities of submarines. The commissioning of INS Arihant into the Indian Navy created a strategic precedence in the region; also, for China, building its submarine fleet is of significant importance.

China Nuclear Powered Naval Vessels Market

The Chinese market 2025 revenues stood at around USD 1.47 billion, representing roughly 71.02% of the global sales.

Japan Nuclear Powered Naval Vessels Market

The Japanese market in 2025 stood at around USD 0.57 billion, accounting for roughly 27.42% of the global revenues.

Rest of the World

The rest of the world includes the Middle East & Africa and the Latin America region. The rest of the world holds a comparatively smaller market share. It is expected to grow at a high CAGR of 9.0% during the forecast period. Visible opportunity sits in Latin America, mainly, especially through Brazil’s PROSUB pathway, which includes the development of a conventionally armed submarine with nuclear propulsion. The Middle East & Africa sub-region does not yet have a comparable operational base. As a result, the rest of the World contributes only a minimal share currently, but it still carries long-term relevance as selected countries explore future naval nuclear capability development.

Latin America Nuclear Powered Naval Vessels Market

The market in Latin America reached around USD 0.24 billion in 2025, accounting for roughly 94.57% of the rest of the world revenue.

Middle East & Africa Nuclear Powered Naval Vessels Market

The Middle East & Africa market stood at around USD 0.01 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Main Shipbuilders & High-Stakes Defense Projects Strengthen the Market Position

The competitive landscape of the global market for nuclear-powered naval vessels is characterized as an oligopoly owing to the presence of a small number of firms that have wide involvement in areas including nuclear reactor manufacturing, submersible shipbuilding, and advanced propulsion systems engineering. Some of the leading companies in this segment include Huntington Ingalls Industries, General Dynamics, BAE Systems, Naval Group, Rolls-Royce, and TechnicAtome.

Huntington Ingalls Industries and General Dynamics anchor the U.S. submarine and carrier base, while BAE Systems plays a central role in the U.K.’s nuclear submarine programs, and Naval Group leads France’s strategic and attack-submarine pipeline. These companies are also benefiting from rising defense budget allocations and ongoing technological advancements in nuclear propulsion, which are expanding long-term program visibility over the forecast period. As a result, the growth of the market is being driven by sustained government-backed demand rather than commercial competition, reinforcing a stable but highly specialized competitive structure in the powered naval vessels market.

List of Key Nuclear Powered Naval Vessels Companies Profiled

- Huntington Ingalls Industries, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems plc. (U.K.)

- Naval Group (France)

- Rolls-Royce Holdings plc. (U.K.)

- TechnicAtome (France)

- Leonardo S.p.A. (Italy)

- General Dynamics Mission Systems, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: General Dynamics Electric Boat announced it had received USD 12.40 billion in contract modifications for the construction of two FY2024 Virginia-class submarines, marking one of the largest recent contract actions directly tied to the nuclear powered submarines segment.

- March 2025: HII announced it had been awarded the Australian Submarine Supplier Qualification (AUSSQ) pilot contract with an initial value of USD 6.05 million, to accelerate Australian supplier qualification into the U.S. nuclear-powered submarine industrial base.

- January 2025: The U.K. Ministry of Defense announced the Unity contract with Rolls-Royce, worth approximately USD 11.23 billion, to support the design, manufacture, and in-service support of the nuclear reactors powering the Royal Navy’s submarine fleet.

- March 2024: The U.S. Navy’s proposed FY2025 budget requested USD 9.56 billion for the Columbia-class program, including USD 3.34 billion in procurement funding to complete the second boat and USD 6.22 billion in advance procurement for future boats, underlining the strategic weight of the ballistic missile submarine segment.

- March 2024: Brazilian official reporting on PROSUB stated that the program’s budget was running at around USD 7.97 billion, highlighting Latin America’s main long-term entry point into the market through a nuclear-propelled submarine pathway.

- March 2023: The U.S. Department of the Navy’s FY2024 President’s Budget requested USD 5.80 billion for the Columbia-class ballistic missile submarine program and USD 1.90 billion for incremental funding for Ford-class aircraft carriers CVN-80 and CVN-81.

- March 2023: Australia’s official AUKUS nuclear-powered submarine pathway announcement mentions that the phased approach would result in USD 3.95 billion of investment in Australia’s industrial capability and workforce over the next four years.

REPORT COVERAGE

The global nuclear powered naval vessels market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry experts' developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By Component

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 28.78 billion in 2025 and is projected to reach USD 48.77 billion by 2034.

In 2025, the North America market value stood at USD 19.31 billion.

The market is expected to exhibit a CAGR of 6.0% during the forecast period.

The submarines segment led the market by platform.

Ballistic missile submarine replacement and attack submarine modernization are driving market growth.

Key players in the Nuclear Powered Naval Vessels market include Huntington Ingalls Industries, General Dynamics, BAE Systems, Naval Group, Rolls-Royce Holdings plc, and TechnicAtome.

The North America region dominated the market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us