Occlusion Devices Market Size, Share & Industry Analysis By Product Type (Cardiac Occlusion Devices, Vascular Occlusion Devices, and Gastrointestinal (GI) Occlusion Devices), By Material (Metal-Based Occlusion Devices, Polymer-Based Occlusion Devices, and Hybrid (Metal + Polymer) Devices), By Indication (Congenital Heart Defects, Structural Heart Disorders, Peripheral Vascular Diseases, Neurovascular Disorders, Gastrointestinal Disorders, and Others), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

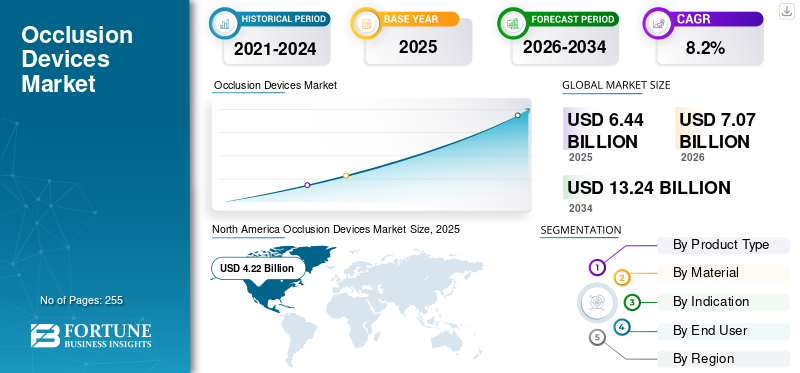

The global occlusion devices market size was valued at USD 6.44 billion in 2025 and is projected to grow from USD 7.07 billion in 2026 to USD 13.24 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period. North America dominated the global market with a market share of 65.53% in 2025.

The global market comprises implantable medical devices designed to block abnormal blood flow or close anatomical defects in cardiac, vascular, neurovascular, and gastrointestinal systems. These devices play a critical role in treating conditions such as atrial septal defects (ASD), left atrial appendage (LAA) closure for stroke prevention, peripheral vascular diseases, and aneurysms. The market is witnessing sustained growth due to the rising prevalence of cardiovascular diseases, which remain the leading cause of death globally, accounting for nearly 18 million deaths annually, according to the World Health Organization.

The increasing adoption of minimally invasive procedures, coupled with technological advancements in device materials and delivery systems, has further strengthened demand. Additionally, the expanding elderly population and growing awareness of stroke prevention therapies are accelerating procedural volumes worldwide. Leading players continue to invest in product innovation, as exemplified by Boston Scientific’s continued expansion of its WATCHMAN portfolio and Abbott’s strengthening of its Amplatzer closure device franchise, which reinforces long-term market momentum.

Download Free sample to learn more about this report.

Occlusion Devices Market Trends

Technological Advancements and Hybrid Device Designs Enhancing Clinical Applications of Occlusion Devices

A notable trend shaping the market is the continuous evolution of device design and materials. Manufacturers are increasingly focusing on hybrid occlusion devices that combine metal frameworks with polymer coatings to improve biocompatibility and reduce thrombus formation. These innovations address long-term safety concerns and enhance procedural outcomes. Advances in delivery systems, including improved steerability and recapturability, are also simplifying complex procedures and expanding physician adoption. Additionally, imaging integration and procedural planning tools are improving placement accuracy, particularly in structural heart interventions. Companies are actively launching next-generation products to maintain a competitive advantage. For example, newer iterations of LAA closure devices feature reduced profiles and enhanced sealing mechanisms, reflecting a broader industry shift toward precision-focused innovation. This trend is expected to continue as regulatory bodies and clinicians increasingly emphasize the importance of long-term patient outcomes.

Market Dynamics

Market Drivers

Rising Adoption of Minimally Invasive Cardiac and Vascular Procedures Driving Adoption of Occlusion Device Products

The primary driver of the market is the rapid shift toward minimally invasive and catheter-based interventions across cardiology and vascular specialties. Physicians increasingly prefer transcatheter occlusion procedures over open surgery due to shorter hospital stays, reduced complications, and faster patient recovery. This trend is particularly evident in left atrial appendage closure, which has gained strong traction as an alternative to long-term anticoagulation therapy for atrial fibrillation patients.

- The growing AFib population, estimated to affect over 33 million people globally, has directly increased demand for LAA closure devices.

Regulatory approvals and product expansions have further fueled adoption. For instance, Abbott’s Amplatzer Amulet LAA Occluder received expanded regulatory approvals across major markets, strengthening physician confidence. Similarly, Boston Scientific has reported consistent double-digit growth in WATCHMAN procedures, driven by broader reimbursement coverage and updated clinical guidelines. In parallel, rising use of embolization devices in neurovascular and peripheral interventions is supporting global occlusion devices market growth, particularly in advanced healthcare systems with high interventional volumes.

Market Restraints

High Procedure Costs and Limited Reimbursement to Limit Market Growth

Despite strong clinical adoption, high device and procedure costs remain a key restraint for the market, particularly in price-sensitive regions. Occlusion devices often carry premium pricing due to their complex manufacturing processes, the use of advanced materials such as Nitinol, and stringent regulatory requirements. In emerging economies, limited reimbursement coverage and high out-of-pocket expenses restrict patient access, especially for elective structural heart procedures. Even in developed markets, reimbursement policies vary significantly by country and indication, creating uncertainty for hospitals and providers.

- For example, while LAA closure procedures are well reimbursed in the U.S., coverage remains inconsistent in parts of Europe and the Asia Pacific, which slows broader adoption.

Additionally, hospitals face budgetary pressures, particularly public healthcare institutions, which can delay capital purchases and limit the uptake of newer-generation devices. These financial barriers are compounded by the need for specialized infrastructure and trained interventional specialists, further constraining market penetration in low- and middle-income regions.

Market Opportunities

Expansion in Emerging Markets and New Clinical Indications Creating New Growth Avenues

The market presents significant growth opportunities in emerging economies and through the expansion of clinical indications. Rapid improvements in healthcare infrastructure across the Asia Pacific, Latin America, and parts of the Middle East are enabling greater access to advanced interventional procedures. Countries such as China and India are witnessing a rise in investments in cath labs and cardiac centers, creating a favorable environment for the adoption of occlusion devices.

In addition, manufacturers are actively pursuing new indications and patient segments. Ongoing clinical trials exploring occlusion therapies for broader stroke prevention and congenital heart defect management are expected to unlock new revenue streams. Strategic collaborations between device manufacturers and regional distributors are also accelerating market entry. For instance, partnerships aimed at expanding local manufacturing and training programs are helping global players establish a stronger foothold in high-growth regions. As awareness increases and reimbursement frameworks evolve, these markets are expected to contribute disproportionately to future growth.

Market Challenges

Regulatory Complexity and Clinical Learning Curve Pose Challenges

The market faces several challenges, including stringent regulatory pathways and the steep clinical learning curve associated with advanced interventional procedures. Regulatory approvals require extensive clinical evidence, often leading to prolonged development timelines and high R&D costs. Smaller manufacturers, in particular, face difficulties navigating complex approval processes across multiple geographies.

Furthermore, the successful adoption of occlusion devices depends heavily on the expertise of physicians and the institutional experience. Inadequate training or low procedural volumes can impact outcomes, limiting adoption in smaller hospitals. Concerns related to device-related complications, such as device migration or incomplete closure, also necessitate robust post-market surveillance. These challenges highlight the importance of comprehensive physician training programs, long-term clinical data, and close collaboration between manufacturers and healthcare providers to ensure sustained market growth.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Large Application of Lower Body Exoskeletons to Drive Segment Dominance

Based on product type, the market is classified into cardiac occlusion devices, vascular occlusion devices, and gastrointestinal (GI) occlusion devices.

The vascular occlusion devices segment held the largest global occlusion devices market share in 2025. Vascular occlusion devices hold a significant share of the global market, driven by their extensive use across peripheral and neurovascular interventions. These devices are widely employed in embolization procedures for treating aneurysms, arteriovenous malformations, tumors, and uncontrolled bleeding, making them essential in both emergency and elective settings.

The cardiac occlusion devices segment is expected to grow at a CAGR of 9.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Material

Increasing Preference for Metal-Based Occlusion Devices Led to Dominance of Segment

Based on material, the market is segmented into metal-based occlusion devices, polymer-based occlusion devices, and hybrid (metal + polymer) devices.

The metal-based occlusion devices segment dominated the global market in 2025. By material, the metal-based occlusion devices segment held a share of 67.5% in 2025. Metal-based occlusion devices dominate the market owing to their proven mechanical strength, flexibility, and long-term durability. Nitinol-based devices, in particular, offer excellent shape memory and radial force, making them ideal for cardiac and vascular applications. Their extensive clinical track record and regulatory approvals across major markets have established strong trust among physicians. Despite emerging alternatives, metal-based devices continue to be the preferred choice for complex interventions, thereby sustaining their high market share.

Additionally, hybrid (metal + polymer) devices are projected to grow at a CAGR of 12.0% during the study period.

By Indication

Increasing Diagnosis Rates of Structural Heart Disorders Led to Dominance of Segment

Based on indication, the market is segmented into congenital heart defects, structural heart disorders, peripheral vascular diseases, neurovascular disorders, gastrointestinal disorders, and others.

The structural heart disorders segment dominated the global market in 2025. By indication, the structural heart disorders segment held a share of 32.4% in 2025. Structural heart disorders represent the leading indication segment due to increasing diagnosis rates and growing adoption of procedures. Conditions such as LAA closure for stroke prevention and septal defect repairs are driving demand. The expanding elderly population and advancements in transcatheter techniques have made structural heart interventions safer and more accessible. Continuous guideline updates and expanding reimbursement coverage further support the segment’s dominance.

Additionally, gastrointestinal disorders are projected to grow at a CAGR of 10.5% during the study period.

By End-user

Growing Number of Hospitals & Specialty Clinics Led to Segment’s Dominance

Based on end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025. Hospitals and ambulatory surgical centers account for the largest share of occlusion device usage due to their advanced infrastructure and access to skilled interventional specialists. Most occlusion procedures require imaging capabilities, hybrid operating rooms, and multidisciplinary teams, which are predominantly available in hospital settings. The gradual shift of select procedures to ASCs is enhancing efficiency while maintaining hospitals’ leadership in complex interventions. Furthermore, the segment is set to hold a 78.9% share in 2026.

Additionally, specialty clinics' end users are projected to grow at a CAGR of 11.6% during the study period.

Occlusion Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Occlusion Devices Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2025, valued at USD 4.22 billion, and maintained its leading position in 2026, with a value of USD 4.67 billion. North America represents the largest and most mature market for occlusion devices, with growth driven primarily by high procedural volumes and early adoption of advanced interventional therapies. The region has a high prevalence of atrial fibrillation, structural heart disorders, and peripheral vascular diseases, which directly supports demand for cardiac and vascular occlusion devices. Additionally, the strong presence of leading device manufacturers and continuous product innovation contribute to market expansion.

U.S. Occlusion Devices Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 4.27 billion in 2026, accounting for roughly 60.5% of global occlusion devices sales.

Europe

Europe is projected to record a growth rate of 6.6% in the coming years, which is the third highest among all regions, and reach a valuation of USD 1.01 billion by 2026. An aging population and the increasing burden of cardiovascular and neurovascular diseases are supporting growth in Europe. The region has well-established public healthcare systems that facilitate access to interventional procedures, particularly for treatments of structural heart defects and congenital conditions. Adoption of occlusion devices is increasing as minimally invasive approaches gain preference over open surgical interventions. Western European countries, such as Germany, France, and U.K., continue to drive demand due to their strong clinical expertise and reimbursement coverage for select indications.

U.K. Occlusion Devices Market

The U.K. market in 2025 is estimated to be around USD 0.15 billion, representing approximately 2.3% of global occlusion devices revenues.

Germany Occlusion Devices Market

Germany’s market is projected to reach approximately USD 0.18 billion in 2025, equivalent to around 2.8% of global occlusion devices sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.04 billion in 2026 and secure the position of the third-largest region in the market. Asia Pacific is the fastest-growing region in the market, driven by a large patient pool and rapid improvements in healthcare infrastructure. The region has a high prevalence of congenital heart defects and a rapidly aging population, particularly in countries such as China and Japan, which is increasing demand for cardiac and vascular interventions. Rising healthcare expenditure, expanding insurance coverage, and growing investments in cath lab infrastructure are enabling greater access to minimally invasive procedures.

Japan Occlusion Devices Market

The Japan market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 2.0% of global occlusion devices revenues.

China Occlusion Devices Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.30 billion, representing roughly 4.2% of global occlusion devices sales.

India Occlusion Devices Market

The India market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 2.2% of global occlusion devices revenues.

Latin America and Middle East & Africa

Growth in Latin America and the Middle East & Africa is driven by improving access to advanced medical technologies and the gradual expansion of private healthcare facilities. Countries such as Brazil and Mexico are witnessing rising adoption of minimally invasive vascular and cardiac procedures due to increasing physician expertise and patient awareness.

GCC Occlusion Devices Market

The GCC market is projected to reach approximately USD 0.07 billion by 2026, accounting for roughly 1.0% of global occlusion devices revenues.

Competitive Landscape

Key Industry Players

Increasing Focus on New Product Launches by Prominent Companies to Support Their Domination

The global market is moderately to highly consolidated, with a small group of multinational medical device companies accounting for a significant share of global revenues, particularly in cardiac and vascular occlusion segments. Companies such as Boston Scientific and Abbott dominate the cardiac occlusion segment through well-established left atrial appendage and septal closure platforms, supported by extensive clinical evidence and regulatory approvals across major markets. Meanwhile, players such as Medtronic, Stryker, Terumo, and Cook Medical maintain strong positions in vascular and neurovascular occlusion through the use of embolization coils, plugs, and adjunctive systems.

- For instance, in July 2025, Boston Scientific received FDA approval expanding Watchman FLX and FLX Pro labels to include post-ablation patients, potentially adding 1-2 million patients globally to their market.

Other key players, including Johnson & Johnson, W. L. Gore & Associates, and others, are also expanding in the market, primarily due to their increasing emphasis on developing advanced products and strengthening their market presence.

List of Key Occlusion Devices Companies Profiled

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Terumo Corporation (Japan)

- Cook Medical (U.S.)

- Johnson & Johnson (CERENOVUS) (U.S.)

- L. Gore & Associates (U.S.)

- MicroPort Scientific Corporation (China)

- Braun Melsungen AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Penumbra launched its SwiftSET Coil, a new complex coil solution designed for adaptive embolization. SwiftSET is engineered to optimize vessel wall apposition through its shape configuration and facilitate smooth deployment, ensuring natural conformity to tight spaces for dense occlusion in small vessels.

- September 2025: Penumbra Inc. has secured the CE Mark for its SwiftPAC neuro embolization coil, which is part of the Swift Coil System and is now commercially available in Europe.

- June 2025: Penumbra, Inc. announced the U.S. Food and Drug Administration (FDA) clearance and launch of the Ruby XL System, the longest, largest, and softest coil on the market.

- March 2025: MicroPort CardioAdvent, a subsidiary of MicroPort CardioFlow, has received EU Medical Device Regulation (MDR) certification for its AnchorMan Left Atrial Appendage Closure System (AnchorMan LAAC system), securing market approval in just 14 months from registration.

- August 2022: Boston Scientific Corporation announced the acquisition of Obsidio, Inc., a privately held company that has developed the Gel Embolic Material (GEM) technology used for embolization of blood vessels in the peripheral vasculature.

REPORT COVERAGE

The market report provides a detailed global occlusion devices market analysis and focuses on key aspects such as leading companies, product type, material, indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Material, Indication, End User, and Region |

|

By Product Type |

· Cardiac Occlusion Devices · Vascular Occlusion Devices · Gastrointestinal (GI) Occlusion Devices |

|

By Material |

· Metal-Based Occlusion Devices · Polymer-Based Occlusion Devices · Hybrid (Metal + Polymer) Devices |

|

By Indication |

· Congenital Heart Defects · Structural Heart Disorders · Peripheral Vascular Diseases · Neurovascular Disorders · Gastrointestinal Disorders · Others |

|

By End User |

· Hospitals & ASCs · Specialty Clinics · Others |

|

By Region |

· North America (By Product Type, By Material, By Indication, By End User, and by Country) o U.S. (By Product Type) o Canada (By Product Type) · Europe (By Product Type, By Material, By Indication, By End User, and by Country/Sub-region) o U.K. (By Product Type) o Germany (By Product Type) o France (By Product Type) o Italy (By Product Type) o Spain (By Product Type) o Scandinavia (By Product Type) o Rest of Europe (By Product Type) · Asia Pacific (By Product Type, By Material, By Indication, By End User, and by Country/Sub-region) o China (By Product Type) o Japan (By Product Type) o India (By Product Type) o Australia (By Product Type) o Southeast Asia (By Product Type) o Rest of Asia Pacific (By Product Type) · Latin America (By Product Type, By Material, By Indication, By End User, and by Country/Sub-region) o Brazil (By Product Type) o Mexico (By Product Type) o Rest of Latin America (By Product Type) · Middle East & Africa (By Product Type, By Material, By Indication, By End User, and by Country/Sub-region) o GCC (By Product Type) o South Africa (By Product Type) o Rest of the Middle East & Africa (By Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 6.44 billion in 2025 and is projected to reach USD 13.24 billion by 2034.

In 2025, the North America regional market value stood at USD 4.22 billion.

Growing at a CAGR of 8.2%, the market will exhibit steady growth over the forecast period.

By product type, the vascular occlusion devices segment is the leading segment in this market.

The rising minimally invasive cardiac and vascular procedures is one of the major factors driving the markets growth.

Boston Scientific Corporation, Abbott Laboratories, Medtronic plc, and Stryker Corporation are the major players in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us