Oil & Gas Cybersecurity Market Size, Share & Industry Analysis, By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Industrial Control System (ICS)), By Solution Type (Risk & Compliance Management, Identity & Access Management (IAM), Threat Intelligence & Analytics, Encryption & Data Protection, Security Information & Event Management (SIEM)), By Deployment Mode (On-Premise, Cloud-Based, & Hybrid), By Application (Upstream (Exploration & Production), Midstream (Pipelines, Storage), Downstream (Refining & Distribution)), & Regional Forecast, 2026-2034

Oil & Gas Cybersecurity Market Size and Future Outlook

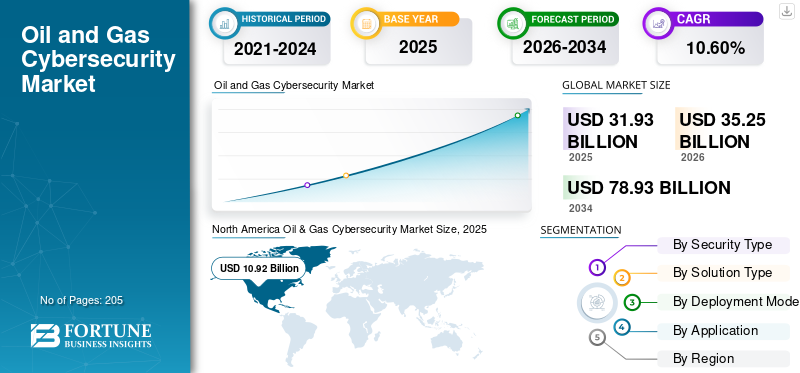

The global oil and gas cybersecurity market size was valued at USD 31.93 billion in 2025. The market is projected to grow from USD 35.25 billion in 2026 to USD 78.93 billion by 2034, exhibiting a CAGR of 10.60% during the forecast period. North America dominated the oil & gas cybersecurity market with a market share of 34.19% in 2025.

Oil & gas cybersecurity focuses on protecting industrial control systems (ICS), supervisory control and data acquisition (SCADA) networks, pipelines, refineries, and digital oilfield platforms from increasingly sophisticated cyber threats that can disrupt physical operations. As the industry transitions toward connected and automated environments, legacy operational technology (OT) systems originally designed for isolated operations are now integrated with information technology (IT) networks, creating new vulnerabilities. This convergence has made cybersecurity a critical component of operational continuity, safety, and asset integrity across upstream, midstream, and downstream segments.

Key factors driving the market include the rising frequency of targeted cyberattacks on pipeline and refinery infrastructure, which have demonstrated the potential to cause large-scale supply disruptions. In addition, the expansion of remote monitoring systems, Internet of Things (IoT)-enabled sensors, and cloud-based analytics in oilfield operations is significantly increasing the attack surface. Regulatory enforcement for critical infrastructure protection, particularly in pipeline networks and offshore assets, is also compelling operators to invest in advanced cybersecurity frameworks. Furthermore, the growing reliance on third-party vendors and digital service providers is driving demand for robust identity and access management solutions.

- For instance, in May 2021, a major cyberattack targeted the Colonial Pipeline in the U.S., where a ransomware attack infiltrated the company’s IT systems, forcing a shutdown of pipeline operations as a precautionary measure to protect operational technology (OT) systems. This disruption led to significant fuel supply shortages across the East Coast, highlighting the vulnerability of interconnected IT and industrial systems. The incident accelerated investments in pipeline cybersecurity, including enhanced monitoring, segmentation between IT and OT networks, and stricter regulatory oversight.

Some of the leading companies operating in the global oil & gas cybersecurity industry include Honeywell International Inc., Siemens AG, Schneider Electric SE, ABB Ltd., and others. Honeywell International Inc. is a U.S.-based multinational conglomerate specializing in industrial automation, aerospace, building technologies, and performance materials. The company is a key player in the oil & gas sector, offering advanced industrial control systems (ICS) and robust cybersecurity solutions to enhance operational efficiency and asset protection. Honeywell’s integrated platforms are widely deployed across refineries, pipelines, and offshore facilities.

Download Free sample to learn more about this report.

OIL and GAS CYBERSECURITY MARKET TRENDS

Expansion of Managed Security Services (MSS) and Outsourced SOC Operations is the Key Market Trend

Oil and gas companies are increasingly adopting Managed Security Services (MSS) and outsourcing Security Operations Center (SOC) functions to address the shortage of skilled professionals in Operational Technology OT cybersecurity. Managing complex environments that include Industrial Control Systems (ICS) and SCADA networks requires specialized expertise, which many operators lack internally.

For instance, in June 2023, Shell expanded its collaboration with external cybersecurity providers to strengthen 24/7 monitoring across global assets. Similarly, in January 2024, Abu Dhabi National Oil Company (ADNOC) enhanced its centralized SOC capabilities to monitor upstream and midstream operations. Also, the growing need for real-time threat intelligence, faster response times, and cost optimization makes MSS a critical component of cybersecurity solutions for geographically dispersed, high-risk energy infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Adoption of Edge Computing in Oilfield Operations is the Key Market Driver

The increasing deployment of edge computing across oil & gas operations is emerging as a key driver for cybersecurity investments. Oil & gas cybersecurity is processing data closer to the source, such as drilling rigs, pipelines, and offshore platforms, to enable real-time decision-making and reduce latency. However, this decentralization introduces multiple new endpoints beyond traditional OT environments, making them vulnerable to localized cyber threats. As a result, operators are investing in secure edge architectures, endpoint protection, and decentralized threat intelligence monitoring systems.

For instance, in August 2023, upstream operators such as Equinor, BP, and Shell in the North Sea expanded edge-based monitoring systems for predictive maintenance, requiring enhanced security layers at remote sites. Additionally, edge computing systems often operate in harsh, isolated environments, underscoring the need for autonomous cybersecurity capabilities that can operate without constant human intervention. This shift is driving demand for advanced solutions that ensure data integrity, secure device communication, and protection against edge-level intrusions, making cybersecurity a critical enabler of next-generation oilfield digitalization.

MARKET RESTRAINTS

Complexity of Securing Legacy OT Infrastructure to Hamper Market Growth

A key restraint in the oil & gas cybersecurity market growth is the complexity associated with securing legacy Operational Technology (OT) systems that were not originally designed with cybersecurity in mind. Many upstream and downstream facilities still rely on decades-old Industrial Control Systems (ICS) and Supervisory Control and Data Acquisition (SCADA) networks that lack basic security features, such as encryption, authentication, and patching. Integrating modern cybersecurity solutions into these environments is challenging due to risks of operational disruption and downtime.

For instance, in April 2022, several European refinery operators delayed cybersecurity upgrades due to concerns over system compatibility with existing control infrastructure. Additionally, the need to maintain continuous operations limits the ability to perform frequent system updates or security testing. This creates persistent vulnerabilities that are difficult to address without large-scale infrastructure replacement.

MARKET OPPORTUNITIES

Integration of Cybersecurity in Carbon Capture and Energy Transition Infrastructure is Creating New Growth Avenues

The expansion of Carbon Capture, Utilization, and Storage (CCUS) and hydrogen-linked oil & gas infrastructure is creating new opportunities for cybersecurity deployment. These emerging assets rely heavily on interconnected systems, including Industrial Control Systems (ICS) and advanced monitoring platforms, to manage CO₂ injection, storage integrity, and transport networks. As these facilities are often integrated with existing pipelines and storage systems, they introduce additional cyber-physical risk layers.

For instance, in September 2023, Equinor advanced digital monitoring capabilities at its Northern Lights CO₂ storage project, requiring enhanced cybersecurity frameworks to protect cross-border data flows and storage operations. Similarly, growing integration between traditional oil & gas assets and low-carbon technologies is driving demand for secure data exchange, real-time monitoring, and anomaly detection systems. These developments are opening opportunities for cybersecurity vendors to provide specialized solutions tailored to hybrid energy infrastructure.

MARKET CHALLENGES

Limited Visibility across Distributed and Remote Assets is a Key Market Challenge

A major challenge in the market is the limited visibility across highly distributed and remote assets such as offshore platforms, pipelines, and storage facilities. These operations rely on geographically dispersed OT environments, including Industrial Control Systems (ICS) and SCADA networks, which are often difficult to monitor in real time. In many cases, inconsistent network connectivity and reliance on satellite communications restrict continuous threat detection capabilities. For instance, in February 2023, operators in remote upstream fields in Africa reported delays in identifying anomalies due to fragmented monitoring systems. Additionally, integrating data from multiple assets into centralized Security Operations Centers (SOC) remains complex due to interoperability issues.

Segmentation Analysis

By Security Type

Network Security Dominated Due to Critical Infrastructure Protection Needs

Based on security type, the market is classified into network security, endpoint security, application security, cloud security, industrial control system (ICS), and others.

In 2025, network security dominated the oil & gas cybersecurity market share due to the extensive reliance on interconnected systems across upstream, midstream, and downstream operations. Critical assets such as pipelines, refineries, and offshore platforms depend on secure communication between Operational Technology (OT) and Information Technology (IT) networks. As these environments become increasingly connected through Industrial Control Systems (ICS) and Supervisory Control and Data Acquisition (SCADA) systems, they are exposed to external threats. Network security solutions such as firewalls, intrusion detection systems, and network segmentation play a vital role in preventing unauthorized access and lateral movement within systems.

The cloud security segment is experiencing the highest growth and is expected to grow at a CAGR of 12.31% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Solution Type

Threat Intelligence & Analytics Led Market Due to Real-Time Threat Detection Demand

Based on solution type, the market is classified into risk & compliance management, identity & access management (IAM), threat intelligence & analytics, encryption & data protection, security information & event management (SIEM), and others.

In 2025, the threat intelligence & analytics segment dominated the global market due to the increasing need for real-time visibility into complex and distributed threat environments. Advanced analytics tools leverage Artificial Intelligence (AI) and machine learning to detect anomalies, identify potential breaches, and predict cyber threats before they impact operations. Additionally, geographically dispersed assets such as pipelines and offshore platforms require centralized monitoring capabilities.

The Security Information & Event Management (SIEM) segment is expected to grow at a CAGR of 12.20% over the forecast period.

By Deployment Mode

On-Premise Commanded Market Due to Legacy Infrastructure Dependence

On the basis of the deployment mode, the market is classified into on-premise, cloud-based, and hybrid.

In 2025, the on-premise segment dominated the global market. Many operators prefer on-premise solutions to maintain full control over security protocols, minimize latency, and reduce exposure to external networks. Additionally, regulatory requirements and internal risk policies often mandate localized data storage and processing. The need to ensure uninterrupted operations in remote and high-risk environments further reinforces the preference for on-premise cybersecurity frameworks across upstream and refining facilities.

The cloud-based segment is expected to grow at a CAGR of 12.13% over the forecast period.

By Application

Upstream (Exploration & Production) Led Market Due to High Asset Connectivity Exposure

On the basis of application, the market is classified into upstream (exploration & production), midstream (pipelines, storage), downstream (refining & distribution), and others.

In 2025, the upstream (exploration & production) segment dominated the global market due to extensive deployment of connected and remote operational systems across drilling sites and offshore platforms. The increasing use of Internet of Things (IoT) sensors, seismic data platforms, and remote monitoring solutions significantly expands the attack surface. Additionally, upstream assets are often located in geographically isolated environments, making them more vulnerable to cyber threats and harder to monitor continuously.

The midstream (pipelines, storage) segment is expected to grow at a CAGR of 11.63% over the forecast period.

Oil & Gas Cybersecurity Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Oil & Gas Cybersecurity Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market in 2025 was valued at USD 10.92 billion and also takes the lead in 2026 with USD 11.99 billion. North America’s cybersecurity in the oil and gas industry is driven by strict enforcement of pipeline cybersecurity regulations, particularly mandates from agencies such as the Transportation Security Administration (TSA), which require continuous monitoring and risk management. The region’s extensive pipeline network and large refining capacity increase exposure to cyber threats, necessitating advanced protection measures.

U.S. Oil & Gas Cybersecurity Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 9.31 billion in 2025, accounting for roughly 29.17% of global revenues.

Europe

Europe is projected to record a growth rate of 8.88% in the coming years, which is the second-highest among all regions, and was valued at USD 7.85 billion in 2025. Europe’s market is driven by the implementation of strict regulatory frameworks, such as the NIS2 Directive, which mandate enhanced protection of critical energy infrastructure. Increasing cybersecurity investments in aging North Sea offshore assets and refining infrastructure are also contributing to market growth.

Germany Oil & Gas Cybersecurity Market

The German market was valued at USD 1.97 billion in 2025 and is estimated at around USD 2.16 billion in 2026, representing roughly 6.17% of global revenues. Market growth in Germany is driven by a strong emphasis on industrial cybersecurity standards and integration with advanced manufacturing systems, particularly in refining and petrochemical operations. Additionally, increasing focus on protecting interconnected energy infrastructure and digital control systems is accelerating cybersecurity investments.

Asia Pacific

Asia Pacific was valued at USD 6.99 billion in 2025. In the region, India and China were valued at USD 1.44 billion and USD 2.13 billion, respectively, in 2025. The rapid expansion of refining capacity, pipeline infrastructure, and LNG terminals in countries such as China and India drives the market. Increasing adoption of digital oilfield technologies and automated control systems is expanding the cyber risk landscape.

India Oil & Gas Cybersecurity Market

The India market accounted for roughly 4.50% of global revenues. India’s market is driven by expanding pipeline networks and refinery capacity, increasing exposure to cyber risks across interconnected infrastructure. The growing adoption of digital monitoring systems and SCADA-based operations by public sector oil companies is further accelerating demand for advanced cybersecurity solutions.

China Oil & Gas Cybersecurity Market

The market in China accounts for roughly 6.66% of global revenues.

Japan Oil & Gas Cybersecurity Market

The Japan market in 2025 was valued at around USD 1.11 billion, accounting for roughly 3.47% of global revenues.

Latin America

Latin America is expected to see moderate growth in this market over the long term. The market was valued at USD 1.71 billion in 2025. The market is driven by the modernization of offshore exploration and pipeline infrastructure, increasing the need for secure digital and operational systems.

Brazil Oil & Gas Cybersecurity Market

The Brazilian market was valued at USD 0.85 billion in 2025, accounting for roughly 2.67% of global revenues.

Middle East & Africa

The Middle East & Africa region is expected to witness significant growth in this market during the forecast period. The Middle East & Africa market was valued at USD 4.46 billion in 2025, driven by large-scale investments in digital oilfields, smart refineries, and export infrastructure, particularly by national oil companies. The increased focus on protecting critical assets, such as pipelines, LNG terminals, and offshore operations, is accelerating cybersecurity adoption across the region.

GCC Oil & Gas Cybersecurity Market

The GCC market was valued at USD 2.83 billion in 2025, representing roughly 8.87% of the global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Partnerships, Business Expansion, And Technological Advancements by Leading Companies to Boost Their Market Share

The global oil & gas cybersecurity market is highly consolidated, with prominent players including Honeywell International Inc., Siemens AG, Schneider Electric SE, ABB Ltd., and others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in April 2023, Honeywell expanded its cybersecurity offerings for the oil & gas sector by enhancing its Industrial Cybersecurity portfolio, focusing on protecting Operational Technology (OT) environments such as refineries and pipelines. The company introduced advanced threat detection and risk management capabilities integrated with its control systems. This initiative aimed to help operators secure legacy Industrial Control Systems (ICS) while ensuring compliance with evolving regulatory requirements across critical energy infrastructure.

Other key players in the global market include Cisco Systems, Inc., Palo Alto Networks, Inc., Fortinet, Inc., and IBM Corporation. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY OIL & GAS CYBERSECURITY COMPANIES PROFILED

- Honeywell International Inc. (U.S.)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- ABB Ltd. (Switzerland)

- Cisco Systems, Inc. (U.S.)

- Palo Alto Networks, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Kaspersky Industrial Cybersecurity (KICS) (Russia)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Schneider Electric enhanced its EcoStruxure Cybersecurity platform for oil & gas applications, focusing on securing connected industrial assets. The update introduced improved network segmentation and endpoint protection for ICS and SCADA systems. This development supported oil & gas operators in strengthening resilience against cyber threats while maintaining operational efficiency across upstream and downstream facilities.

- August 2023: IBM strengthened its cybersecurity services for the oil & gas sector by integrating AI-driven threat intelligence and analytics into its security operations center (SOC) offerings. The initiative focused on improving real-time threat detection across industrial and enterprise systems, enabling energy companies to manage cyber risks and enhance operational resilience proactively.

- July 2023: Cisco expanded its industrial cybersecurity portfolio by introducing enhanced network security solutions tailored for oil & gas infrastructure. The company focused on securing pipeline networks and remote operational sites through advanced threat detection and secure connectivity solutions.

- June 2023: Siemens strengthened its oil & gas cybersecurity capabilities by integrating advanced OT security solutions into its digital energy platforms. The company focused on securing SCADA and industrial automation systems used in pipeline and refining operations. This move enabled real-time monitoring and threat detection across distributed assets, helping energy operators mitigate cyber risks associated with increased digitalization and remote operations.

- May 2023: Fortinet expanded its OT security platform to address cybersecurity needs in oil & gas operations. The company introduced enhanced network segmentation and intrusion prevention systems tailored for SCADA and industrial networks. This helped protect pipeline and refining infrastructure from increasingly sophisticated cyber threats.

- September 2022: ABB deployed advanced cybersecurity solutions for a major oil refinery project, focusing on securing distributed control systems (DCS) and industrial networks. The company integrated real-time monitoring and anomaly detection tools to protect critical operations. This initiative aimed to enhance operational safety and reduce the risk that a cyber incident response would impact refining processes.

REPORT COVERAGE

The global oil & gas cybersecurity market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.60% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Security Type, Solution Type, Deployment Mode, Application, and Region |

| By Security Type |

|

| By Solution Type |

|

| By Deployment Mode |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 31.93 billion in 2025 and is projected to reach USD 78.93 billion by 2034.

In 2025, the market value in North America stood at USD 10.92 billion.

The market is expected to exhibit a CAGR of 10.60% during the forecast period of 2026-2034.

The network security segment led the market by security type.

Growing adoption of edge computing in oilfield operations is driving the market.

Honeywell International Inc., Siemens AG, Schneider Electric SE, and ABB Ltd. are some of the prominent players in the market.

North America dominated the market in 2025.

The expansion of connected ICS/SCADA systems, stricter critical infrastructure regulations, and the growing reliance on remote and cloud-based operations are major factors expected to favor oil & gas cybersecurity adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us