Olefins Market Size, Share & Industry Analysis, By Type (Ethylene, Propylene, Butadiene, and Others), By Application (Polyolefins, Base Chemical Intermediates, Synthetic Rubber, and Others), and Regional Forecast, 2026-2034

OLEFINS MARKET SIZE AND FUTURE OUTLOOK

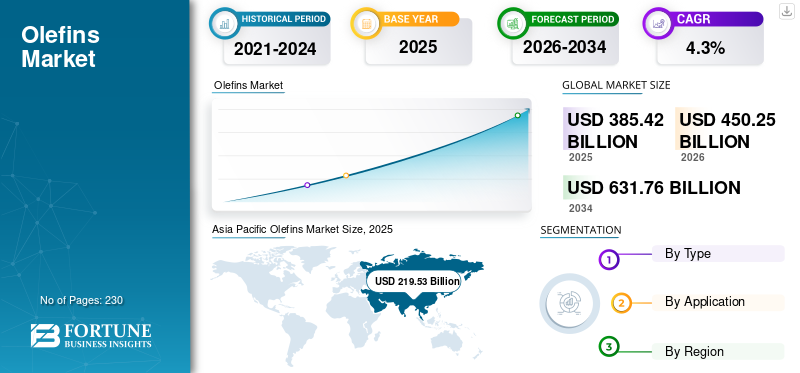

The global olefins market size was valued at USD 385.42 billion in 2025. The market is projected to grow from USD 450.25 billion in 2026 to USD 631.76 billion by 2034, exhibiting a CAGR of 4.3% during the forecast period. Asia Pacific dominated the olefins market with a market share of 56.96% in 2025.

Olefins are unsaturated hydrocarbons containing at least one carbon-carbon double bond, with key commercial examples including ethylene, propylene, and butadiene. They are the foundational building blocks of the petrochemical industry as they are converted into high-volume products such as polyethylene, polypropylene, synthetic rubber, and multiple chemical intermediates used across packaging, construction, textiles, automotive, and consumer goods. A major demand driver is the sustained growth in plastics consumption, especially for packaging, as petrochemical demand continues to outpace many other bulk materials and remains closely linked to rising urbanization, industrialization, and consumer-product usage in developing economies. Sinopec, ExxonMobil, LyondellBasell, SABIC, and Shell are the key players operating in the market.

Download Free sample to learn more about this report.

Olefins Market KEY TAKEAWAYS

- 2025 Market Size: USD 385.42 billion

- 2026 Market Size: USD 450.25 billion

- 2034 Forecast Market Size: USD 631.76 billion

- CAGR: 4.3% from 2026–2034

- Asia Pacific dominated the olefins market with a 56.96% share in 2025.

- The propylene segment is projected to grow at a CAGR of 4.6% during the forecast period.

- The base chemical intermediates segment is projected to grow at a CAGR of 4.1% during the forecast period.

Asia Pacific

USD 5.47 billion in 2025, USD 5.81 billion in 2026. Polyolefins-driven demand from packaging, electronics, and manufacturing.

North America

USD 2.30 billion in 2026. Driven by polyolefins demand in packaging, healthcare, and industrial applications.

Europe

Driven by base chemical intermediates used in coatings, detergents, automotive materials, and construction chemicals.

U.S.

USD 41.07 billion in 2025. Large-scale polyethylene and polypropylene consumption across key end-use sectors.

China

USD 2.89 billion in 2026. Strong demand from plastics processing, coatings, packaging, and automotive electronics.

Read More

OLEFINS MARKET TRENDS

Capacity Expansion Reshapes the Competitive Landscape

A major trend in the global industry is the widening gap between capacity additions and demand absorption. New plants continue to come online in feedstock-advantaged regions, while mature markets are seeing weaker utilization and slower recovery. This is creating a more polarized industry structure, where low-cost producers are strengthening their position and higher-cost regions are being pushed toward consolidation, restructuring, or selective shutdowns. At the same time, companies are increasingly focusing on downstream integration, circular product offerings, and lower-carbon production pathways. As a result, the industry is moving beyond pure scale competition toward a model shaped by cost position, integration depth, and sustainability alignment.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Plastics Consumption to Sustain Core Olefins Demand and Drive Market Growth

The primary demand driver for the industry is the continued expansion of plastics and petrochemical consumption across packaging, consumer goods, construction, automotive, and industrial applications. Olefins remain essential feedstocks for producing versatile, lightweight, and cost-effective materials that are embedded in modern supply chains and everyday products. The product demand is particularly supported by urbanization, rising income levels, industrial development, and the need for affordable materials in developing economies. Even as sustainability pressures increase, the functional importance of olefin-based derivatives remains strong. This makes demand growth resilient, especially in markets where manufacturing activity, infrastructure development, and consumer consumption continue to expand, driving olefins market growth.

MARKET RESTRAINTS

Cost Pressure on High-Cost Production Regions to Restrain Market Growth

A key restraint in the global industry is the pressure faced by producers operating in structurally higher-cost regions. Energy costs, feedstock disadvantages, weaker domestic demand, and lower operating efficiency can reduce competitiveness and compress margins. This becomes especially challenging in a commodity market where customers are highly price sensitive and low-cost producers can capture share more aggressively. In such an environment, even if the global demand continues to grow, not all assets benefit equally. Producers in disadvantaged markets may struggle to maintain utilization, justify reinvestment, or compete effectively against regions with better integration, cheaper raw materials, and stronger export economics.

MARKET OPPORTUNITIES

Circular and Low-Carbon Olefins to Create Market Growth Opportunities

One of the major opportunities in the olefins industry lies in the development of circular and lower-carbon solutions. As customers, regulators, and investors place greater emphasis on sustainability, producers have an opportunity to differentiate themselves through recycled-feedstock products, lower-emission manufacturing routes, and certified circular material offerings. This shift can open new premium segments and strengthen customer relationships in industries increasingly focused on decarbonization and responsible sourcing. It also allows producers to move beyond pure commodity competition and build more resilient value propositions. Over time, companies that successfully align olefins production with circularity and emissions reduction are likely to improve both strategic relevance and long term commercial positioning.

MARKET CHALLENGES

Geopolitical Uncertainty May Create Challenges for Long Term Investment Decisions

A major challenge for the global industry is the growing uncertainty created by geopolitical tensions, trade disruptions, policy shifts, and volatile global supply chains. Olefins production is highly capital intensive and depends on long term decisions around plant location, feedstock access, logistics, and downstream integration. When trade flows become less predictable and regulatory environments shift, planning new investments becomes far more complex. Producers must consider cost competitiveness and resilience to tariffs, energy shocks, regional conflicts, and policy changes. In this environment, the challenge is no longer merely operating efficiently, but making the right strategic decisions in a market that is becoming more fragmented and less predictable.

SEGMENTATION ANALYSIS

By Type

Ethylene Segment to Lead the Market Owing to Major Role in Polyethylene Production

Based on type, the market is segmented into ethylene, propylene, butadiene, and others.

The ethylene segment is anticipated to hold the dominant olefins market share during the forecast period. The main factor driving the demand for ethylene is its central role in producing polyethylene, the world’s most widely used plastic. Growth in flexible packaging, food and beverage containers, industrial films, household products, and healthcare packaging continues to support strong polyethylene consumption, which in turn lifts ethylene demand. This driver is especially powerful in developing economies, where rising urbanization, manufacturing activity, and consumer goods consumption are expanding the need for affordable and versatile plastic materials. As packaging remains one of the most resilient and essential end-use sectors, it continues to anchor long term growth in ethylene demand.

The propylene segment is anticipated to rise at a CAGR of 4.6% over the forecast period. The demand for propylene is due to the continued expansion of polypropylene consumption across packaging, automotive, appliances, textiles, and consumer goods. Propylene is a critical feedstock for polypropylene, which is valued for its lightweight properties, durability, and cost efficiency in a wide range of industrial and everyday applications. The product demand is being reinforced by automotive lightweighting, growth in consumer products, and increasing use of rigid and flexible packaging. In Asia especially, continued investment in polypropylene capacity and downstream manufacturing is strengthening propylene demand, making it one of the fastest-growing segments globally.

By Application

To know how our report can help streamline your business, Speak to Analyst

Expansion of Packaging and High-Volume Plastics Applications to Drive Polyolefins Segment Growth

Based on application, the market is segregated into polyolefins, base chemical intermediates, synthetic rubber, and others.

The polyolefins segment is anticipated to hold the dominant olefins market share during the forecast period. The primary factor driving the product demand for polyolefins is the continued expansion of packaging and high-volume plastic applications. Polyolefins, especially polyethylene and polypropylene, are widely used as they are lightweight, durable, cost-effective, and versatile across food packaging, consumer goods, household products, healthcare items, and industrial films. Ethylene and propylene remain the key feedstocks for these resins and packaging continues to outperform many other material applications globally. This makes polyolefins the strongest demand anchor in the value chain, driving market growth.

The base chemical intermediates segment is anticipated to surge at a CAGR of 4.1% over the forecast period. The product demand is due to the broad expansion of downstream manufacturing sectors that rely on olefin-based chemicals beyond plastics alone. Olefins are converted into intermediates used in fibers, solvents, coatings, detergents, automotive materials, construction chemicals, and consumer formulations. As these products feed multiple industries at once, the demand is supported by overall industrialization, urban growth, and rising manufacturing intensity. This diversified downstream pull makes base chemical intermediates one of the fastest-growing and most strategically important olefin application segments.

OLEFINS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Olefins Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounts for the largest market share and is expected to maintain its dominance during the forecast period. In this region, the largest demand driver is polyolefins, supported by the region’s scale in packaging, consumer goods, appliances, electronics, and general manufacturing. Rapid urbanization, rising income levels, and expanding industrial output continue to strengthen the demand for polyethylene and polypropylene across both domestic and export-oriented markets. Base chemical intermediates also play a major supporting role as the region has a deep and expanding downstream chemical manufacturing base. However, polyolefins remain the primary engine given that they are at the center of both consumer-driven and industrial demand growth.

Japan Olefins Market

The Japan market reached a value of approximately USD 16.88 billion in 2025, equivalent to around 4.4% of the global sales.

China Olefins Market

The China market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 130.70 billion, representing roughly 33.9 % of the global sales.

India Olefins Market

The India market reached approximately USD 26.84 billion in 2025, equivalent to around 7.0% of the global sales.

North America

In North America, the primary driver of product demand is polyolefins, supported by strong consumption in packaging, consumer products, healthcare materials, and industrial applications. The region has a well-developed plastics conversion base and a mature downstream market that continues to absorb large volumes of polyethylene and polypropylene. Base chemical intermediates also provide support, especially in construction, industrial chemicals, and performance materials. However, the broad and resilient use of polyolefins across every day and industrial applications makes them the major driver of product demand in the region.

U.S. Olefins Market

The U.S. market can be analytically approximated at around USD 41.07 billion in 2025, accounting for roughly 10.7% of the global sales.

Europe

In Europe, the strongest demand driver is base chemical intermediates, as the region has a diversified downstream industrial structure that depends heavily on olefin-derived chemicals. These intermediates support applications across coatings, detergents, solvents, automotive materials, construction chemicals, and specialty manufacturing. While polyolefins remain important, the Europe market is less driven by pure volume expansion in plastics and other categories by the breadth of its industrial chemical ecosystem. Synthetic rubber also contributes through automotive and industrial demand, but the broadest and most durable pull comes from the intermediates chain.

U.K. Olefins Market

The U.K. market reached approximately USD 4.23 billion in 2025, equivalent to around 1.1% of the global sales.

Germany Olefins Market

The Germany market reached approximately USD 13.08 billion in 2025, equivalent to around 3.4% of the global sales.

Latin America

In Latin America, the key driver of product demand is polyolefins, especially through packaging, household products, flexible plastics, and consumer applications. The region’s demand profile is closely linked to the need for affordable, versatile plastic materials in everyday use, making polyethylene and polypropylene the most important downstream products. Base chemical intermediates provide secondary support in industrial and construction-related applications, but they are not as broad-based as polyolefins. The practical and widespread use of polyolefin materials across packaging and consumer driven sectors is anticipated to propel market growth.

Brazil Olefins Market

The Brazil market reached approximately USD 11.34 billion in 2025, equivalent to around 2.9% of the global sales.

Middle East & Africa

In the Middle East & Africa, the main demand driver is polyolefins, reflecting both the region’s production orientation and the growing importance of packaging, infrastructure-related plastics, and consumer applications. In the Middle East, integrated petrochemical systems support strong polyethylene and polypropylene chains, while in Africa, the demand is increasingly tied to packaging and basic plastic products. Base chemical intermediates are an important supporting driver, particularly as the region seeks broader industrial diversification.

Saudi Arabia Olefins Market

The Saudi Arabia market touched a value of approximately USD 10.19 billion in 2025, equivalent to around 2.6% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Extensive Derivative Portfolios for an Edge over Rival Players

The global olefins industry is highly concentrated, capital intensive, and driven by scale, feedstock access, and downstream integration. Competition is centered among large integrated petrochemical and energy companies that benefit from strong production economics, global operating footprints, and broad derivative portfolios. The industry is becoming more polarized, with feedstock-advantaged regions strengthening their position while higher-cost regions face pressure on margins and investment. Competitive differentiation is also shifting toward circular products, lower-carbon production pathways, and deeper integration into downstream value chains. Competitive landscape includes key players such as Sinopec, ExxonMobil, LyondellBasell, SABIC, and Shell, among others.

LIST OF KEY OLEFINS COMPANIES PROFILED

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Exxon Mobil Corporation (U.S.)

- SABIC (Saudi Arabia)

- INEOS (U.K.)

- Shell (U.K.)

- Chevron Phillips Chemical Company LLC (U.S.)

- Braskem (Brazil)

- Borealis GmbH (Austria)

- China Petrochemical Corporation (China)

- PTT Global Chemical Public Company Limited (Thailand)

KEY INDUSTRY DEVELOPMENTS

- September 2025: INEOS upgraded its Lavera cracker in France to use pyrolysis oil from hard-to-recycle plastic waste, producing recycled ethylene and propylene for virgin-quality polyethylene and polypropylene. Manufactured at its plants in France and Italy, these materials are suitable even for food and medical packaging, marking a significant step in building Europe’s advanced recycling value chain.

- September 2025: INEOS Project ONE in Antwerp reached 70% completion, marking a major milestone in the development of Europe’s first new ethane cracker in a generation. With over 2,500 people working on site, the construction is progressing rapidly, with full plant start-up planned for early 2027.

- April 2025: Aramco, Sinopec, and Yasref signed a Venture Framework Agreement to study a major petrochemical expansion at Yasref in Yanbu, Saudi Arabia. The plan includes a 1.8 million tons per annum steam cracker and 1.5 million tons per annum aromatics complex, strengthening Saudi-China energy cooperation and boosting Yasref’s integrated refining and petrochemical capabilities.

- April 2025: BASF, SABIC, and Linde started the world’s first large-scale electrically heated steam cracking furnace at BASF’s Ludwigshafen site. Powered by 6 MW of renewable electricity, the demonstration plant is used to test two heating concepts under industrial conditions and is likely to cut CO2 emissions by at least 90%, marking a major step toward decarbonizing petrochemical

- March 2025: LyondellBasell approved a major propylene capacity expansion at its Channelview Complex near Houston. The construction was set to begin in the third quarter of 2025, with startup targeted for late 2028. The new 400 kiloton metathesis unit would improve supply self-sufficiency, support demand growth, create 750 peak construction jobs and 25 permanent roles, and strengthen key downstream product chains.

- January 2025: CSPC, the Shell-CNOOC joint venture, approved a major expansion of its Daya Bay petrochemical complex in Huizhou, China. The project includes a 1.6 million tons per annum ethylene cracker, downstream derivatives, and a 320,000 tons per annum specialty chemicals facility. The investment will strengthen domestic supply, deepen site integration, and support China’s growing demand.

- January 2024: SABIC approved the final investment decision for its SABIC Fujian Petrochemical Complex in China’s Fujian province, a USD 6.4 billion joint venture with Fujian Fuhua Gulei Petrochemical. The project will feature a 1.8 million-ton ethylene cracker and downstream units for EG, PE, PP, and PC, strengthening SABIC’s China footprint and supporting high-end chemical demand.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Volume (Kiloton), Value (USD Billion) |

| Growth Rate | CAGR of 4.3% during 2026-2034 |

| Segmentation | By Type, By Application, and By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size stood at USD 385.42 billion in 2025 and is projected to record a valuation of USD 631.76 billion by 2034.

In 2025, Asia Pacific stood at USD 219.53 billion.

The market will exhibit steady growth at a CAGR of 4.3% during the forecast period of 2026-2034.

By application, the polyolefins segment is expected to lead this market during the forecast period.

The rising plastics consumption sustaining core olefins demand is a key factor driving market growth.

Sinopec, ExxonMobil, LyondellBasell, SABIC, and Shell are the major players operating in the market.

Asia Pacific dominates the market in terms of share.

The rising demand for affordable, versatile plastics across packaging and industrial applications is anticipated to drive wider product adoption.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us