Oncology Nutrition Market Size, Share & Industry Analysis, By Product (Immunonutrition, EPA-Enriched/Cachexia Nutrition, High-Protein/High-Calorie Formulas, and Others), By Cancer Type (Head and Neck Cancer, Stomach and Gastrointestinal Cancer, Colorectal Cancer, Lung Cancer, Hematologic Cancer, Breast Cancer, and Others), By Route of Administration (Oral, Enteral, and Parenteral), By End User (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Online Pharmacies, and Others), and Regional Forecast, 2026-2034

Oncology Nutrition Market Size and Future Outlook

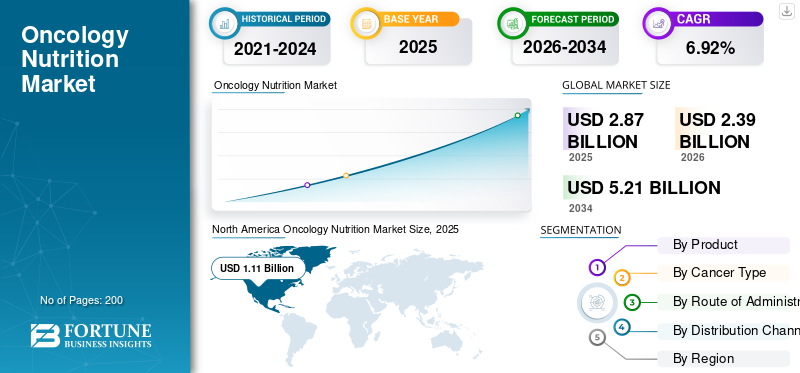

The global oncology nutrition market size was valued at USD 2.87 billion in 2025. The market is projected to grow from USD 3.05 billion in 2026 to USD 5.21 billion by 2034, exhibiting a CAGR of 6.92% during the forecast period. North America dominated the global oncology nutrition market with a market share of 38.68% in 2025.

Oncology nutrition is a significant part of cancer treatments and plays a crucial role in nourishing patients and helping them stay stronger throughout treatment. Proper nutrition plays a critical role in minimizing side effects from treatments such as chemotherapy, immunotherapy, hormonal medications, transplants, and surgery. These advanced therapies adversely impact the appetite and may lead to cancer cachexia, i.e., severe weight and muscle loss. With the rising incidence and prevalence of cancer worldwide, the global oncology nutrition is also anticipated to grow.

-

For instance, in 2022, the International Agency for Research on Cancer reported an incidence of 19,976,499 cancer cases. Such a high incidence drives the market demand.

The market is dominated by various key operating players, including Abbott, Nestlé Health Science, Nutricia, and Fresenius Kabi AG, which direct their resources toward strategic mergers and acquisitions and new product launches to diversify their product offerings.

Download Free sample to learn more about this report.

Oncology Nutrition Market Key Takeaways

- 2025 Market Size: USD 2.87 billion

- 2026 Market Size: USD 3.05 billion

- 2034 Forecast Market Size: USD 5.21 billion

- CAGR: 6.92% from 2026–2034

- North America dominated the oncology nutrition market with a 38.68% share in 2025.

- The colorectal cancer segment is expected to grow at a CAGR of 8.28% during the forecast period.

- The others segment is projected to expand at a CAGR of 8.74% during the forecast period.

North America

North America maintained its leading position with a market value of USD 1.11 billion in 2025.

Europe

Europe is projected to reach USD 0.84 billion by 2026, growing at a CAGR of 6.47%.

Asia Pacific

Asia Pacific is expected to reach USD 0.73 billion by 2026, making it the third-largest regional market.

U.S.

The oncology nutrition market is estimated to reach USD 1.10 billion.

Japan

Rising cancer prevalence and increasing adoption of specialized nutritional support are driving market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Disease Burden of Cancer to Drive Market Growth

One of the principal factors contributing to the growth of the market is the rising cancer burden, increasing the demand for patients who need oncology nutrition care. An ageing population, particularly in developed markets, is further boosting demand, as older cancer patients are more at risk of malnutrition. Growing research and clinical evidence suggest that early nutrition intervention shortens the duration of hospital stays. The expansion of outpatient and home-based cancer care is also expanding demand for oncology nutritional supplements. These factors are driving higher uptake of oncology-focused nutrition products.

- For instance, in February 2024, the WHO estimated over 35.0 million new cancer cases in 2050, witnessing a 77.0% increase from the estimated 20 million cases in 2022.

MARKET RESTRAINTS:

High Cost of Specialized Oncology Nutrition Products Limits Market Growth

The high cost associated with specialized oncology nutrition products acts as a key restraint for the adoption of these oncology nutrition products. In many regions, oncology nutritional products are not fully reimbursed, resulting in out-of-pocket expenditure, leading to underuse or early discontinuation. Hospitals and cancer centers with tight budgets often prioritize core drugs and procedures over premium nutrition products. As a result, clinical guidelines recommending early nutritional support are not consistently implemented. These factors emerge as barriers and slow market penetration.

- For instance, in December 2021, NIH published a study titled ‘Cost-Effectiveness of Nutrient Supplementation in Cancer Survivors’ which acknowledged the financial challenges associated with cancer treatment, including the cost of nutrition products.

MARKET OPPORTUNITIES:

Rising Investment by Key Companies to Offer Lucrative Growth Opportunities in the Market

One of the prominent factors driving the growth of the market is the rising investment by major players operating in the global market to expand their oncology nutrition portfolios. This increasing investment is creating strong growth opportunities, with increasing R&D to develop therapy-specific formulas and immunonutrition blends, tailored for different cancer stages. This broader portfolio addresses more clinical use cases for different cancer indications. Additionally, higher investment supports clinical trials, strengthening scientific backing.

- For instance, in May 2024, Danone invested USD 64.7 million into its production line focused on medical nutrition for disease-related malnutrition, such as in cancer. The investment will be utilized for the production of nearly 30 recipes of the company’s oral nutritional supplement for patients.

ONCOLOGY NUTRITION MARKET TRENDS:

New Product Launches for Cancer Patients Is a Prominent Market Trend Observed

A global oncology nutrition market trend observed is the increasing number of new product launches to cater to the increasing demand. With increasing research and development, these new product offerings are tailored in accordance with cancer patients undergoing different therapies. These factors have encouraged key players to focus on better palatability, texture, and improving adherence in patients with poor appetite. Novel product launches, along with digital support apps and monitoring tools, aim to strengthen clinical integration, thereby reinforcing oncology nutrition market growth.

- For instance, in June 2024, the Department of Atomic Energy, in collaboration with M/s. IDRS Labs Pvt. Ltd. Bengaluru launched a Food Supplement/Nutraceutical AKTOCYTE aimed at enhancing the quality of life for cancer patients undergoing radiotherapy.

MARKET CHALLENGES:

Regulatory Complexity Related to Medical Foods, Clinical Nutrition, And Therapeutic Claims to Pose a Significant Market Challenge

Regulatory complexity around medical foods and clinical nutrition is a major challenge for market growth as companies in this space operate at the intersection of food and drug regulations. These oncology nutrition products must meet strict safety, labelling, and composition standards, and yet cannot make therapeutic claims such as a drug. Regulatory guidelines differ considerably by region, requiring companies to create multiple formulations, labels, and dossiers for the same product. These factors raise development costs and delay launches, posing a significant challenge for the market.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product

New Product Launches Boosted Immunonutrition Segment Growth

Based on product, the global oncology nutrition market is segmented into immunonutrition, EPA-enriched/cachexia nutrition, high-protein/high-calorie formulas, and others. In 2025, the immunonutrition segment captured the dominant oncology nutrition market share. The dominance of the segment is attributed to better clinical outcomes in treatment protocols. Additionally, these immunonutrition products, aimed at enhancing immunity, contain formulas enriched with arginine, omega-3 fatty acids, nucleotides, and specific micronutrients known to reduce postoperative infections, support immune function, and shorten hospital stay in cancer. These factors encourage key players to invest in developing new products and launching them in the market.

-

For instance, in August 2024, GN Corporation launched Nichi BRITE Beta-glucan for enhancing immunity and reducing biomarkers of pancreatic cancer and its recurrence in patients undergoing surgical resection of malignant pancreatic tumors.

To know how our report can help streamline your business, Speak to Analyst

The others segment is expected to grow at a CAGR of 8.74% during the forecast period.

By Cancer Type

Rising Awareness Programs Encouraged the Stomach and Gastrointestinal Cancer Segment Growth

On the basis of cancer type, the market is classified into head and neck cancer, stomach and gastrointestinal cancer, colorectal cancer, lung cancer, hematologic cancer, breast cancer, and others.

The stomach and gastrointestinal cancer segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 24.29% share. Stomach and gastrointestinal cancers have a direct impact on eating and nutrient absorption. Tumors, surgeries, and treatments in this area result in severe side effects such as severe dysphagia, vomiting, and diarrhea, which rapidly drive malnutrition and weight loss. This results in higher consumption of oncology nutrition by stomach and gastrointestinal cancer. As nutritional status strongly influences surgical outcomes in the cancer type, tolerance to chemo/radiotherapy is shown to improve significantly.

Additionally, the rising number of awareness programs highlighting these advantages for stomach cancer is anticipated to support the growth of the segment.

-

For instance, in November 2021, Taiho Oncology, Inc. raised awareness to improve nutritional education for patients impacted by stomach cancer.

The colorectal cancer segment is expected to grow at a CAGR of 8.28% over the forecast period.

By Route of Administration

Ease of Administration of Oral Segment Fueled Segmental Growth

Based on route of administration, the market is segmented into oral, enteral, and parenteral.

The oral segment accounted for the largest share of the market in 2025 and is anticipated to dominate with a 68.63% share in 2026. The dominance of the segment is due to oral drugs being the least invasive way to deliver this medical nutrition to cancer patients. Many clinical guidelines recommend starting with dietary advice and oral nutritional supplements (ONS) for oncology patients at risk of malnutrition. These oral formulas offer greater ease of administration. Additionally, robust product offering through new product launches by key companies with multiple flavors and high-protein, immunonutrition variants, supports them to capture the largest share of revenue within oncology nutrition.

- For instance, in January 2023, Nutricia launched a ready-to-drink, oral nutritional supplement, Fortimel, formulated to meet the nutritional needs of people who are malnourished or at risk of malnutrition due to illness.

The enteral segment is expected to grow at a CAGR of 9.07% over the forecast period.

By Distribution Channel

Strategic Collaborations with Hospital Pharmacies Propelled Segmental Growth

Based on distribution channel, the market is categorized into hospital pharmacies, drug stores & retail pharmacies, online pharmacies, and others.

The hospital pharmacies segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 46.36% share, as most cancer diagnoses, along with active treatment consultation, occur in hospital-based cancer centers. These centers offer oncology nutrition as part of the care pathway. Additionally, manufacturers prioritize hospital contracts and tenders to secure bulk sales. These factors reinforce hospital pharmacies as the primary and most influential distribution channel for oncology nutrition products. Additionally, collaborations and key partnerships among key operating players in the market promote the adoption of these oncology drugs through strategic activities.

- For instance, in May 2023, Fresenius Kabi AG offered a USD 108,225.1 grant for clinical nutrition research in Latin America to advance nutritional care in hospitalized patients.

The online pharmacies segment is expected to grow at a CAGR of 10.92% over the forecast period.

Oncology Nutrition Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America captured the dominant share in 2024, valued at USD 1.04 billion, and also maintained its leading share in 2025, with USD 1.11 billion. The high market share in the region is attributed to a large and mature market driven by robust clinical adoption. Additionally, the region witnessed increasing research and development initiatives for new product launches and various nutraceutical products in clinical trials.

North America Oncology Nutrition Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- For instance, in September 2024, Promino Nutritional Sciences Inc., a nutraceutical company, completed the preclinical trial to demonstrate the effectiveness of the Promino patented IP for the retention of muscle mass in cancer patients undergoing aggressive chemotherapy treatment.

In the U.S., high cancer prevalence and favorable reimbursement for enteral nutrition drive market growth and supporting the country’s dominance in the region. In 2026, the U.S. market is estimated to reach USD 1.10 billion.

The Asia Pacific and Europe are poised to witness notable growth in the coming years. During the forecast period, the region is projected to record a growth rate of 6.47%, the second-highest among all regions, and reach a valuation of USD 0.84 billion by 2026. The growth in Europe is due to strong demand for oncology nutrition products along with robust cancer care infrastructure and government-driven nutrition protocols. Backed by these factors, countries including the U.K. are likely to record the valuation of USD 0.18 billion, Germany to record USD 0.20 billion, and France to record USD 0.13 billion in 2026. The market in Asia Pacific is estimated to reach USD 0.73 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.24 billion and USD 0.09 billion each in 2026.

The Latin America and Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market in 2026 is set to reach a valuation of USD 0.17 billion and is witnessing moderate growth. The region is experiencing an improvement in the adoption of oncology nutritional products. In the Middle East & Africa, the GCC is set to reach a value of USD 0.07 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

New Product Launches by Key Players supported their Leading Position

The global oncology nutrition market exhibits a semi-consolidated structure, with a few companies actively operating worldwide. These players are actively involved in numerous strategic activities such as capacity expansion, innovative product launches, and strategic acquisitions. They actively invest in technology advancement and offer a wide array of product offerings for innovative products.

Abbott, Nestlé Health Science, Nutricia, and Fresenius Kabi AG are some of the significant players in the market. These companies offer a wide range of product offerings and focus on enhancing research and development. They participate in strategic acquisitions to strengthen market positions.

- For instance, in July 2024, Nutricia launched Forticare Advanced, a nutritional drink with anti-inflammatory effects to reduce inflammation in patients with cancer, cachexia, and chronic catabolic diseases such as COPD.

Other notable players in the market include Baxter, B. Braun SE, Hormel Foods Corporation, Danone, and others. These companies are undertaking various strategic initiatives, such as investments to expand their product offering.

LIST OF KEY ONCOLOGY NUTRITION COMPANIES PROFILED:

- Abbott (U.S.)

- Nestlé Health Science(Switzerland)

- Nutricia (North Holland)

- Fresenius Kabi AG (Germany)

- Baxter (U.S.)

- B. Braun SE (Germany)

- Hormel Foods Corporation (U.S.)

- Danone (France)

KEY INDUSTRY DEVELOPMENTS:

- January 2025: Prosoma secured USD 48.1 million in a Pre-Series A funding round. The company aimed to utilize the investment to broaden its offerings and provide a comprehensive suite of services, including nutrition and coaching, to address the needs of cancer patients.

- November 2023: Danone launched Fortimel in China and entered the medical nutrition category. The product offering is designed to meet the nutritional needs of patients recovering after surgery or non-communicable diseases such as cancer and stroke.

- January 2024: Danone partnered with digital oncology company Resilience to improve nutritional care for cancer patients. The partnership aims to develop a novel nutrition and oncology module integrated into Resilience’s digital oncology solution.

- September 2019: Nestlé Health Science launched BOOST Soothe, a clear nutritional drink for patients with cancer. The drink provided protein and calories and a cooling, soothing effect to help patients get the nutrition they need while dealing with certain side effects of cancer treatment, such as oral discomfort and taste changes.

- October 2025: Nestlé Health Science collaborated with the University of California, Davis Innovation Institute for Food & Health (IIFH), to accelerate the development of innovative, nutrition-based solutions.

REPORT COVERAGE

The global oncology nutrition market analysis provides a detailed study of market size & forecast by all segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers & acquisitions, and strategic insights into market growth. The global market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.92% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Product

By Cancer Type

By Route of Administration

By Distribution Channel

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.87 billion in 2025 and is projected to reach USD 5.21 billion by 2034.

In 2025, the market value stood at USD 1.11 billion.

The market is expected to exhibit a CAGR of 6.92% during the forecast period (2026-2034).

The immunonutrition segment is expected to lead the market in terms of product.

The increasing prevalence of various forms of cancer is the key factor driving market growth.

Abbott, Nestlé Health Science, Nutricia, and Fresenius Kabi AG are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us