Optical Imaging Market Size, Share & Industry Analysis, By Type (Hardware [Imaging Systems, Cameras, Illumination Systems, and Others] and Software), By Technology (Optical Coherence Tomography (OCT), Near Infrared Spectroscopy, Hyperspectral Imaging, and Photoacoustic Tomography), By Application (Oncology, Ophthalmology, Cardiology, Neurology, and Others), By End User (Hospitals & ASCs, Diagnostic Imaging Centers, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Optical Imaging Market Size and Industry Overview

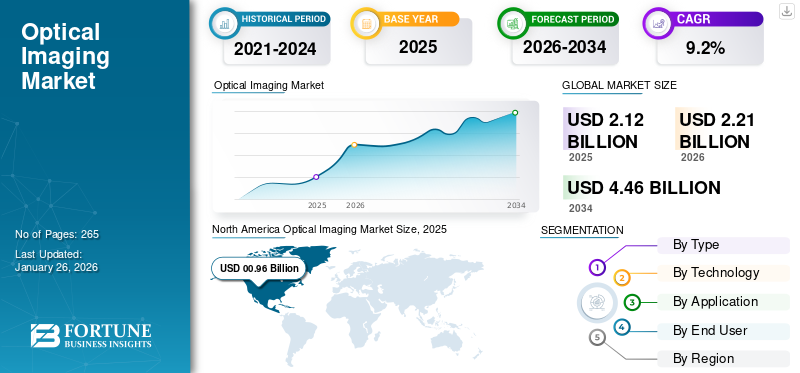

The global optical imaging market size was valued at USD 2.12 billion in 2025 and is projected to grow from USD 2.21 billion in 2026 to USD 4.46 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. North America dominated the optical imaging market with a market share of 45.1% in 2025.

Optical imaging is a non-invasive research and diagnostic technique that uses light to obtain images of internal body structures, molecules, and cells for detecting anomalies within body tissues. The growing prevalence of chronic conditions, including diabetes, cancer, and others, is resulting in an increasing number of patient admissions in clinical settings. The expanding patient pool and the benefits associated with this technology, such as radiation-free, and others, are further augmenting the demand for diagnostic tests, thereby contributing to the adoption of optical imaging systems in the market.

- For instance, according to the 2025 statistics published by the International Diabetes Federation (IDF), about 590 million people are living with diabetes worldwide.

Furthermore, the growing geriatric population is also a major factor contributing to the increasing number of test volumes in the market. This, coupled with increasing technological advancements such as digital cameras and advanced sensors is driving the focus of key players, including Abbott, Koninklijke Philips N.V., and others, and is expected to support the growth of the global optical imaging market.

Download Free sample to learn more about this report.

Optical Imaging Market Key Takeaways

- 2025 Market Size: USD 2.12 billion

- 2026 Market Size: USD 2.21 billion

- 2034 Forecast Market Size: USD 4.46 billion

- CAGR: 9.2% from 2026–2034

- North America dominated the optical imaging market with a 45.10% share in 2025.

- The hardware segment accounted for 85.97% of the global market share in 2026.

- The optical coherence tomography (OCT) segment held a 57.92% market share in 2026.

North America

North America generated USD 0.96 billion in revenue and accounted for 45.10% of the global market in 2025.

Europe

Europe held a 26.60% market share and reached USD 0.57 billion in 2025.

Asia Pacific

Asia Pacific accounted for 21.00% of global demand with a market value of USD 0.45 billion in 2025.

U.S.

The optical imaging market was valued at USD 0.88 billion in 2025, supported by rising diagnostic testing volumes and product innovation.

Japan

The market is driven by increasing adoption of advanced diagnostic imaging technologies and growing healthcare investments.

Read More

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Disorders to Fuel Market Growth

The rising prevalence of chronic disorders, including cancer, cardiovascular diseases, ocular diseases, and others, is supporting the increasing demand for diagnostic tests and treatment monitoring among the patient population, consequently boosting the adoption rate of these products in the market.

- For instance, according to data published by the International Diabetes Federation (IDF) in 2025, approximately 589 million adults worldwide are affected by diabetes.

Additionally, the increasing geriatric population is a crucial factor contributing to the increasing prevalence of chronic disorders among patients, further fueling the demand for these products worldwide. Optical imaging is a non-invasive technique that offers several benefits, including cost-effectiveness, high resolution, and others. Therefore, the factors mentioned above, coupled with the increasing focus of prominent players on R&D activities to launch innovative products, are anticipated to fuel the adoption rate, thereby supporting the global optical imaging market growth.

Market Restraints

High Cost Associated with Advanced Products and Software to Limit Market Growth

There is an increasing demand for these products owing to their distinct benefits, such as non-invasive and others. However, the high cost associated with technologically advanced products and software is expected to limit the adoption rate for these products, especially in emerging countries such as Brazil, China, India, and others.

The high ownership cost and total cost of capital investment represent a huge expenditure, especially for resource-limited healthcare settings. Moreover, the additional costs associated with this technology, such as software upgrades, periodic maintenance, or calibration of devices, further add to the financial burden.

- For instance, according to data published by Medilex LLC in 2025, the price of optical coherence tomography (OCT) systems ranges from USD 35,000 to USD 100,000.

Furthermore, modern optical coherence tomography (OCT) systems generate large amounts of imaging information, which requires robust infrastructure and standardized protocols, including image management systems, servers, and other components, all of which demand additional technical expertise and investment.

Therefore, limited healthcare infrastructure, high upfront costs, software and maintenance expenses, coupled with financial sustainability, are anticipated to limit the penetration rate of this technology in the market.

Beyond the initial purchase, additional expenses related to software upgrades, periodic maintenance, and device calibration further elevate the financial burden. According to Medilex LLC in 2025, OCT systems ranges from USD 35,000 to USD 100,000, underscoring the substantial upfront investment required.

Market Opportunities

Technological Advancements in these Systems to Create Market Opportunities

There is an increasing focus on integrating technological advancements into these systems in the market. Innovations, such as handheld and point-of-care devices, are expanding access and increasing utilization volumes for disease diagnosis and treatment monitoring among patients.

These technologically advanced devices enable imaging in mobile screening vans, remote clinics, and other settings, further driving the demand for these products in the market. This, coupled with the growing focus of key players on research and development activities to integrate artificial intelligence and image analytics into these products, is anticipated to boost their adoption in the market.

- According to a 2025 news release published by Theia Imaging LLC, the company is developing the Theia T2 Handheld OCT System, which comprises a cart-mounted OCT engine, a flexible tether, and a lightweight handheld probe that accepts interchangeable lenses for imaging different regions of the eye.

Other Prominent Opportunities

- The increasing adoption in emerging economies presents opportunities for market penetration and cost-effective imaging solutions.

- Expansion into new areas such as neuroscience, dermatology, and intraoperative imaging represents untapped growth potential.

Market Challenges

Limited Diagnosis in Emerging Countries to Limit Market Growth

There is a growing focus on initiatives among national organizations to raise awareness about early diagnosis of chronic disorders among the patient population. However, there is a growing prevalence of delayed detection of chronic conditions owing to distinct factors, limited professional expertise and awareness, delayed referrals of patients with chronic diseases, coupled with inadequate reimbursement policies, especially in emerging nations.

The limited number of healthcare settings and the availability of specialized imaging rooms, among other factors, contribute to the delayed detection of chronic disorders, ultimately leading to the postponement of diagnosis among patients, particularly in emerging countries such as Mexico and Brazil.

- For instance, according to data published by HelpMeSee in 2025, it was reported that there are only 2.5 ophthalmologists per million people in Sub-Saharan Africa.

Other Prominent Challenges

- The limited tissue penetration depth in optical imaging modalities restricts their applicability for imaging deeper organs.

- Regulatory barriers and lengthy approval processes slow down the commercialization of new technologies.

Optical Imaging Market Trends

Shifting Preference Toward Non-Invasive Techniques to Boost Product Demand

There is an increasing trend toward non-invasive techniques and real-time modalities that can be incorporated into surgical, diagnostic, and interventional workflows. Prominent players are emphasizing technologies that provide safety and accurate visualization without exposing patients to radiation.

This shift is augmenting the demand for these imaging systems, such as optical coherence tomography (OCT) systems, photoacoustic imaging systems, and others across various clinical applications. These advancements are streamlining workflows by reducing the need for post-operative imaging checks and improving patient outcomes. Moreover, the integration of advanced analytics and hardware miniaturization is further anticipated to fuel the adoption of optical imaging technology in clinical settings worldwide.

- For instance, in August 2023, Kauvery Hospital Alwarpet adopted the Ultreon OCT-ACR artificial intelligence system, which assists in performing angioplasties with precision and safety, thereby strengthening the hospital’s technological capabilities in India.

Other Prominent Trends

- Rapid adoption of optical coherence tomography (OCT) in ophthalmology for the early detection of retinal diseases and glaucoma.

- Expanding use of optical imaging in oncology for tumor detection and real-time surgical guidance applications.

- Rising adoption of multimodal imaging platforms combining optical, ultrasound, and fluorescence modalities for comprehensive visualization.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Increasing Product Launches Encouraged Hardware Segment Growth

Based on type, the market is classified into hardware and software. Hardware is further divided into imaging systems, cameras, illumination systems, and others.

To know how our report can help streamline your business, Speak to Analyst

The hardware segment led the market accounting for 85.97% market share in 2026. The growth is owing to the increasing prevalence of chronic disorders such as ophthalmologic disorders and other related conditions, resulting in a growing number of diagnostic test volumes globally. Additionally, the increasing focus of major players on research and development initiatives to launch novel products is further expected to contribute to the segment’s growth.

- In May 2025, OZ Optics launched the In-Line Multimode Fiber Speckle Homogenizer, which significantly reduces modal noise and provides enhanced image quality, thereby strengthening the company’s product portfolio.

By Technology

Increasing Number of Optical Coherence Tomography (OCT) Examinations Led to the Dominance of the Segment

Based on technology, the market is categorized into optical coherence tomography (OCT), near-infrared spectroscopy, hyperspectral imaging, and photoacoustic tomography.

The optical coherence tomography (OCT) segment is projected to dominate the market with a share of 57.92% in 2026. The dominant share is attributed to the increasing number of OCT examinations, which has led to a growing demand for advanced products integrated with this technology. This, coupled with growing focus among prominent players toward R&D activities to launch advanced optical imaging products, is likely to support the segment’s growth in the market.

- According to 2025 statistics published by Oregon Health & Science University, optical coherence tomography (OCT) is used in more than 30 million eye procedures annually in the U.S.

The photoacoustic tomography segment is expected to grow at a CAGR of 8.4% over the forecast period.

By Application

Increasing Prevalence of Cancer Led to the Dominance of the Oncology Segment

On the basis of application, the market is segmented into oncology, ophthalmology, cardiology, neurology, and others.

The oncology segment is expected to lead the market, contributing 40.72% globally in 2026. The growth is primarily due to the increasing prevalence of various forms of cancer, including lung cancer, bowel cancer, among others, resulting in increasing demand for innovative devices such as hyperspectral imaging systems, and others in the market.

- For instance, according to 2025 statistics published by the American Cancer Society, about 2.0 million new cancer cases are projected to occur in the U.S.

The ophthalmology segment is set to flourish with a growth rate of 7.3% during the forecast period.

By End-user

Increasing Number of Hospitals & ASCs Led to the Segment’s Dominance

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, diagnostic imaging centers, and others.

The hospitals and ASCs segment will account for 57.92% market share in 2026. The growing prevalence of chronic diseases, the increasing number of diagnostic and treatment monitoring tests, and the rising number of hospitals & ASCs are some of the vital factors supporting the growth of the segment in the market.

- For instance, according to statistics published by the Ambulatory Surgery Center Association (ASCA) in 2025, there are approximately 6,500 Medicare-certified ambulatory surgery centers in the U.S.

In addition, the specialty clinics segment is projected to grow at a CAGR of 7.3% during the study period.

Optical Imaging Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Optical Imaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 0.96 billion in 2025, representing 45.10% of total market revenue, and is projected to reach USD 1 billion in 2026. The dominance of the region is attributed to several factors, including the rising prevalence of chronic diseases, increasing diagnostic test volumes, robust healthcare infrastructure, strategic government initiatives, growing product launches among key players, and the widespread adoption of advanced diagnostic systems. In 2025, the U.S. market is estimated to reach USD 0.88 billion. The country's growth is due to growing number of diagnostic tests among patients resulting in increasing focus of key players toward R&D activities to launch technologically advanced products in the market.

- For instance, according to 2025 statistics published by the Glaucoma Research Foundation, it was reported that about 4.22 million people are suffering from glaucoma in the U.S.

Europe and Asia Pacific

Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth in the forecast period. During the study period, Europe contributed approximately USD 0.57 billion to the global market in 2025, accounting for 26.60% share, and is expected to reach USD 0.59 billion in 2026. In 2025, the Asia Pacific market stood at USD 0.45 billion, representing 21.00% of global demand, and is projected to grow to USD 0.46 billion in 2026. This growth is due to the increasing number of healthcare settings, the rising prevalence of chronic diseases, and the growing focus of governmental organizations on funding medical research and development activities in the region. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.1 billion, Germany to record USD 0.13 billion in 2026, France to record USD 0.09 billion in 2025. After Europe, the market in the Asia Pacific is estimated to reach USD 0.46 billion in 2026 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.06 billion while China is estimated to reach USD 0.17 billion in 2026.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market accounted for USD 0.09 billion in 2025, representing 4.20% of the global industry, and is expected to reach USD 0.09 billion in 2026. Middle East & Africa maintained a strong presence in the global market, reaching USD 0.07 billion in 2025, accounting for 3.10% share, and is expected to reach USD 0.07 billion in 2026. The increasing prevalence of chronic disorders, improvement in healthcare infrastructure, and demand for innovative products and software are expected to boost product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.04 billion in 2025.

Competitive Landscape

Key Industry Players

Growing Number of Product Launches Among the Major Players to Support Their Market Dominance

A robust and diversified product portfolio of advanced devices and software, along with a significant global presence, is one of the key factors supporting the dominance of leading companies in the market. Abbott, CANON MEDICAL SYSTEMS CORPORATION, and Topcon Corporation were among the major players in the market in 2024. Furthermore, the growing focus of key players on receiving regulatory approval for their innovative products is likely to aid the global optical imaging market share.

For instance, in August 2021, Abbott received U.S. FDA approval for its optical coherence tomography (OCT) imaging platform driven by the company's Ultreon Software. This innovative imaging software combines OCT with artificial intelligence (AI) to provide physicians with a more comprehensive view of coronary blood flow and blockages, thereby enhancing clinical decision-making.

Other key players, including Carl Zeiss AG, and others, are also growing in the market, primarily due to their increasing focus on collaborations among the other players to strengthen their brand presence in the market.

List of Key Optical Imaging Companies Profiled

- Abbott (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Topcon Corporation (Japan)

- Carl Zeiss AG (Germany)

- Danaher Corporation (U.S.)

- Heidelberg Engineering Inc. (Germany)

- Visionix (U.S.)

- MILabs B.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- January 2025 – Lumicell Inc. launched LumiSystem, consisting of two FDA-approved products: LUMISIGHT and the Lumicell Direct Visualization System (DVS), with the aim of strengthening its product portfolio.

- October 2024 – Siloton, a Bristol-based health tech start-up, secured USD 930,735.9 to develop its Akepa optical coherence tomography (OCT) chip technology, with the aim of catering to the growing demand among patients suffering from age-related macular degeneration (AMD).

- October 2024 – Gentuity, LLC, received U.S. FDA approval for its Gentuity HF-OCT Imaging System, featuring the Vis-Rx Micro-Imaging Catheter, for use both before and after percutaneous coronary intervention (PCI).

- May 2024 – Carl Zeiss AG launched the CIRRUS 6000, supported by the OCT reference database, with the aim of widening its product portfolio in the U.S.

- June 2022 – MicroPort Scientific Corporation launched the MicroPort Argus OCT System, aiming to strengthen its brand presence in the market.

REPORT COVERAGE

The market report provides a detailed global optical imaging market analysis, focusing on key aspects such as leading companies, types, technologies, applications, and end-users. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Technology, Application, End User, and Region |

|

By Type |

· Hardware o Imaging Systems o Cameras o Illumination Systems o Others · Software |

|

By Technology |

· Optical Coherence Tomography (OCT) · Near Infrared Spectroscopy · Hyperspectral Imaging · Photoacoustic Tomography · Others |

|

By Application |

· Oncology · Ophthalmology · Cardiology · Neurology · Others |

|

By End User |

· Hospitals & ASCs · Specialty Clinics · Diagnostic Imaging Centers · Others |

|

By Region |

· North America (By Type, By Technology, By Application, By End User, and by Country) o U.S. (By Technology) o Canada (By Technology) · Europe (By Type, By Technology, By Application, By End User, and by Country/Sub-region) o U.K. (By Technology) o Germany (By Technology) o France (By Technology) o Italy (By Technology) o Spain (By Technology) o Scandinavia (By Technology) o Rest of Europe (By Technology) · Asia Pacific (By Type, By Technology, By Application, By End User, and by Country/Sub-region) o China (By Technology) o Japan (By Technology) o India (By Technology) o Australia (By Technology) o Southeast Asia (By Technology) o Rest of Asia Pacific (By Technology) · Latin America (By Type, By Technology, By Application, By End User, and by Country/Sub-region) o Brazil (By Technology) o Mexico (By Technology) o Rest of Latin America (By Technology) · Middle East & Africa (By Type, By Technology, By Application, By End User, and by Country/Sub-region) o GCC (By Technology) o South Africa (By Technology) o Rest of the Middle East & Africa (By Technology) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.12 billion in 2025 and is projected to reach USD 4.46 billion by 2034.

In 2025, the North America regional market value stood at USD 0.96 billion.

Growing at a CAGR of 9.2%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the hardware segment led the market in 2026.

Technological advancements are the major factor driving the market's growth.

Abbott and CANON MEDICAL SYSTEMS CORPORATION are the major players in the global market.

North America dominated the market share in 2026.

The growing prevalence of chronic disorders and the increasing number of product launches are anticipated to fuel the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 265

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us