Oxo Chemicals Market Size, Share & Industry Analysis, By Product Type (N-Butyraldehyde, Isobutyraldehyde, C7–C13 Plasticizer Oxo Alcohols, Propionaldehyde, Heptanoic & Pelargonic Acids (C7–C9 Oxo Acids), and Others), By Application (Plasticizers, Acrylates, Acetates, Solvents, Ether, Esters, Resins, and Others), and Regional Forecast, 2026-2034

Oxo Chemicals Market Size and Future Outlook

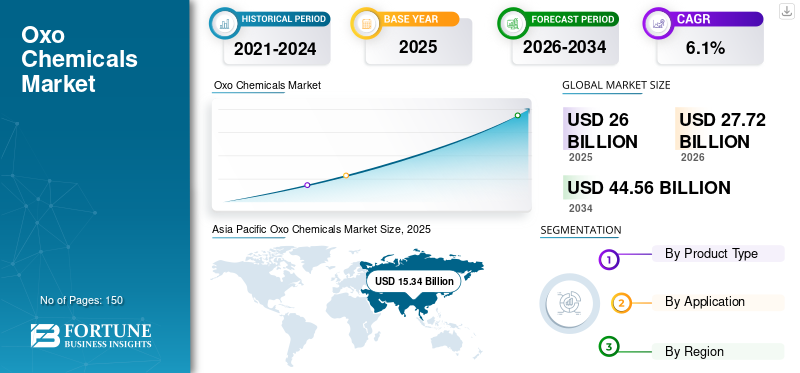

The global oxo chemicals market size was valued at USD 26.00 billion in 2025. The market is projected to grow from USD 27.72 billion in 2026 to USD 44.56 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period. Asia Pacific dominated the oxo chemicals market, with a market share of 59.00% in 2025.

Oxo chemicals are aldehydes, alcohols, and acids produced through the hydroformylation (oxo process) of olefins using synthesis gas (carbon monoxide and hydrogen). These chemicals serve as critical intermediates in the production of plasticizers, acrylates, solvents, resins, coatings, and specialty chemicals. The market plays a vital role in the petrochemical value chain, linking upstream olefin production to downstream consumer and industrial applications. Among product categories, N-butyraldehyde holds the leading share due to its extensive use in plasticizer alcohol production. The rising demand for flexible PVC, coatings, and construction materials continues to drive market growth.

Additionally, expansion in automotive, packaging, and infrastructure sectors supports consumption of oxo derivatives. The market is characterized by integrated producers with strong feedstock access, ensuring supply stability and cost efficiency across global regions. The major players operating in the market are BASF SE, Eastman Chemical Company, Dow Inc., and others.

Download Free sample to learn more about this report.

OXO CHEMICALS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 26.00 Billion

- 2026 Market Size: USD 27.72 Billion

- 2034 Forecast Market Size: USD 44.56 Billion

- CAGR: 6.1% from 2026–2034

- Asia Pacific dominated the oxo chemicals market with a 59.00% share in 2025.

- The isobutyraldehyde segment is projected to grow at a CAGR of 6.1% during 2026–2034.

- The acetates segment is expected to grow at a CAGR of 5.5% during the forecast period.

North America

North America accounted for USD 3.90 billion in 2025, driven by strong petrochemical infrastructure and steady industrial demand.

Europe

Europe reached USD 11.10 billion in 2025, supported by established petrochemical networks and demand for specialty chemicals.

Asia Pacific

Asia Pacific led the market with a 59.00% share in 2025, driven by strong demand from construction, automotive, and consumer goods industries.

U.S.

The market reached USD 3.59 billion in 2025, supported by shale-based feedstock advantages and strong demand from coatings and construction sectors.

Japan

The market benefits from expanding petrochemical capacity and strong demand for oxo alcohols and plasticizers in industrial applications.

Read More

OXO CHEMICALS MARKET TRENDS

Sustainability Regulations and Downstream Diversification to Drive Market Evolution

The market is evolving in response to sustainability regulations and diversification of downstream applications. One key trend is the gradual shift toward non-phthalate plasticizers, which influences the demand patterns for specific oxo alcohols. Another important trend is the integration of bio-based feedstocks and process efficiency improvements to reduce carbon emissions in oxo production. Producers are investing in advanced catalyst technologies to enhance hydroformylation efficiency and selectivity. Additionally, growing demand for high-performance coatings, adhesives, and specialty resins is expanding application diversity. Regional production shifts toward Asia Pacific, supported by petrochemical capacity expansion, are reshaping trade flows. These trends reflect structural adjustments in production efficiency, regulatory compliance, and downstream innovation within the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Strong Plasticizer Demand and Industrial Activity to Boost Product Consumption

The oxo chemicals market growth is primarily driven by strong demand from plasticizer production and industrial chemical processing. Plasticizers derived from oxo alcohols are widely used in flexible PVC products, including cables, flooring, automotive interiors, and packaging materials. Rapid urbanization, infrastructure development, and automotive production directly support consumption. Additionally, acrylate and solvent manufacturing depends on oxo intermediates, reinforcing multi-sector demand. Stable feedstock availability from petrochemical complexes ensures continuous supply. Rising global manufacturing activity and growth in consumer goods further contribute to baseline demand. These structural industrial requirements ensure sustained consumption of oxo chemicals across applications, maintaining long-term market stability.

MARKET RESTRAINTS:

Environmental Regulations and Feedstock Volatility to Limit Market Expansion

The market faces restraints related to environmental regulations and feedstock price volatility. Stringent policies on phthalate plasticizers and VOC emissions impact certain downstream applications, influencing product demand patterns. Additionally, oxo chemicals production relies heavily on petrochemical feedstocks, exposing manufacturers to crude oil and natural gas price fluctuations. High capital costs for hydroformylation plants and catalyst systems further limit new capacity additions. Regulatory compliance requirements increase operational costs in developed regions. These factors collectively constrain profitability and expansion flexibility, moderating global market growth.

MARKET OPPORTUNITIES:

Infrastructure Growth and Specialty Chemical Expansion to Create Demand Potential

The market presents significant opportunities driven by infrastructure development and growth in specialty chemical applications. The expansion of construction and automotive sectors increases demand for plasticizers and coatings derived from oxo intermediates. The rising consumption of acrylates in paints, adhesives, and textiles further supports market potential. Another opportunity lies in emerging markets, where industrialization and urbanization drive the demand for flexible PVC and specialty solvents. The development of high-purity oxo derivatives for niche chemical applications also expands revenue potential. Furthermore, technological advancements in hydroformylation catalysts enhance production efficiency and open new product grades. These factors collectively expand the addressable application base, strengthening long-term growth prospects for the market.

MARKET CHALLENGES:

Competitive Substitution and Regulatory Pressure to Affect Market Dynamics

A key challenge in the market is substitution by alternative chemical intermediates and bio-based plasticizers. Regulatory pressure on traditional plasticizer formulations encourages downstream industries to explore alternative chemistries. Additionally, managing process safety and catalyst efficiency remains critical in hydroformylation operations. Global trade disruptions and shifting regional capacities create competitive pressure among producers. Balancing sustainability goals with cost competitiveness presents ongoing challenges. Addressing these issues requires continuous innovation and optimization of supply chains, influencing long-term competitive positioning in the market.

RESEARCH AND DEVELOPMENT ACTIVITIES

R&D efforts focus on improving hydroformylation catalysts to enhance selectivity, reduce by-products, and improve energy efficiency. The development of sustainable feedstock alternatives and low-carbon production processes is also gaining attention. These advancements strengthen competitiveness and environmental compliance.

Segmentation Analysis

By Product Type

N-Butyraldehyde Segment Dominates with Major Role in Plasticizer Alcohol Production

By product type, the market is segmented into N-butyraldehyde, isobutyraldehyde, C7–C13 plasticizer oxo alcohols, propionaldehyde, heptanoic & pelargonic acids (C7–C9 oxo acids), and others.

The N-butyraldehyde segment holds the leading oxo chemicals market share due to its central role as a precursor in the production of 2-ethylhexanol, n-butanol, and other plasticizer alcohols. These derivatives are extensively used in manufacturing flexible PVC products such as cables, flooring, automotive interiors, and packaging films. Strong infrastructure development and growth in construction activities globally continue to sustain the demand for flexible PVC materials, directly reinforcing N-butyraldehyde consumption. Additionally, its use in solvents, coatings, and chemical intermediates broadens its industrial relevance. Integrated petrochemical producers benefit from economies of scale and feedstock availability, further supporting production stability. Continuous investments in hydroformylation efficiency also enhance output and cost competitiveness. These structural industrial linkages ensure high-volume and consistent consumption, maintaining N-butyraldehyde’s dominant position in the global market.

The isobutyraldehyde segment is poised to grow at a CAGR of 6.1% during 2026-2034 and serves as a critical intermediate in the production of isobutanol, neopentyl glycol, and specialty resins. These derivatives are widely used in coatings, adhesives, lubricants, and plastic additives, particularly in high-performance applications requiring chemical stability and resistance properties. Growth in construction coatings and industrial adhesives continues to support the demand for isobutyraldehyde-derived products.

C7–C13 oxo alcohols are essential intermediates in the production of plasticizers used in flexible PVC applications. These alcohols are particularly important for non-phthalate and specialty plasticizer formulations developed to comply with evolving environmental regulations. Rising infrastructure investments, electrical cable production, and automotive interior manufacturing continue to drive consumption of flexible PVC, thereby supporting the demand for C7–C13 oxo alcohols. The segment is set to grow at a CAGR of 5.9% during the forecast period.

By Application

Plasticizers Segment Leads Owing to Expanding Flexible PVC Demand

By application, the market is segmented into plasticizers, acrylates, acetates, solvents, ether, esters, resins, and others.

The plasticizers segment represents the leading application segment in the market due to their critical role in producing flexible polyvinyl chloride (PVC) products. Oxo alcohols such as 2-ethylhexanol are key intermediates in plasticizer production, widely used in cables, flooring, roofing membranes, automotive interiors, and packaging films. Rapid urbanization, infrastructure development, and increasing automotive production continue to drive the demand for flexible PVC materials globally. Additionally, the transition toward non-phthalate plasticizers in response to regulatory pressure has sustained the importance of oxo-derived alcohols in alternative formulations.

To know how our report can help streamline your business, Speak to Analyst

The acetates segment is anticipated to grow at a CAGR of 5.5% during the forecast period. Acetates derived from oxo chemicals are widely used as solvents and intermediates in coatings, inks, pharmaceuticals, and specialty chemical formulations. These compounds provide desirable properties such as controlled evaporation rates, solvency strength, and compatibility with various resin systems. Growth in packaging, printing, and industrial coatings industries supports consistent demand for acetate-based solvents.

Oxo-derived solvents are utilized across coatings, adhesives, chemical processing, and cleaning formulations. Their chemical stability and solvency characteristics make them suitable for dissolving resins, pigments, and additives in industrial formulations. The demand is closely linked to manufacturing output and construction activity. Growth in automotive refinishing, industrial coatings, and specialty chemical production supports consistent solvent consumption. The solvent segment is anticipated to grow at a CAGR of 6.1% during the forecast period.

Oxo Chemicals Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Oxo Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest share in the global market, supported by expanding petrochemical capacity and strong downstream demand from automotive, construction, and consumer goods industries. Countries such as China, India, South Korea, and Japan have significantly increased production capacity for aldehydes and oxo alcohols due to integrated refinery and petrochemical complexes. Rapid urbanization and infrastructure expansion drive the high consumption of plasticizers used in flexible PVC applications such as cables, pipes, and flooring.

China Oxo Chemicals Market

The China market reached a value of USD 7.36 billion in 2025, accounting for approximately 28.3% of global revenues. Growth is driven by large-scale expansion of petrochemical and oxo alcohol production capacity, strong demand from flexible PVC manufacturing, and rising consumption in coatings, adhesives, and infrastructure-related applications.

To know how our report can help streamline your business, Speak to Analyst

India Oxo Chemicals Market

The India market reached a value of around USD 1.53 billion in 2025. Growth is supported by expanding construction and infrastructure projects, increasing flexible PVC demand, and rising domestic manufacturing of plasticizers and specialty coatings.

North America

North America remains a significant regional market and reached USD 3.90 billion in 2025. The region represents a mature yet significant market, driven by integrated petrochemical infrastructure and steady industrial demand. The U.S. leads regional production due to strong access to shale-derived feedstocks, ensuring cost competitiveness in hydroformylation processes. Demand from construction, automotive, packaging, and coatings sectors supports the consistent consumption of plasticizers, acrylates, and solvents.

U.S. Oxo Chemicals Market

In 2025, the U.S. market touched a value of USD 3.59 billion, representing approximately 13.8% of regional revenues. In the country, the market expansion is supported by feedstock cost advantage from shale gas, strong export competitiveness of oxo derivatives, and resilient demand from industrial maintenance and renovation activities.

Europe

The Europe market, which reached a valuation of USD 11.10 billion in 2025, is projected to record modest growth in the market. The regional market is characterized by strong regulatory oversight and emphasis on sustainability. Stringent environmental policies influence production technologies and plasticizer formulations, encouraging transition toward non-phthalate and environmentally compliant derivatives. Countries such as Germany, France, and the Netherlands maintain established production capacity supported by integrated petrochemical networks. Demand from automotive coatings, industrial resins, and specialty chemical sectors remains stable. Additionally, innovation in catalyst efficiency and low-emission production processes supports competitiveness.

Germany Oxo Chemicals Market

The Germany market reached a value of around USD 1.03 billion in 2025, representing approximately 4.0% of regional demand. In this country, the growth is influenced by high-value specialty resin production, innovation in sustainable oxo derivatives, and demand from premium automotive and industrial coating applications.

U.K. Oxo Chemicals Market

In 2025, the U.K. market reached a value of USD 0.66 billion, accounting for roughly 2.5% of regional revenues. The market momentum is linked to refurbishment-driven construction demand, growth in packaging materials, and stable specialty chemical consumption across manufacturing sectors.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in the market over the forecast period. Latin America represents an emerging growth region in the market, primarily driven by expanding construction and manufacturing sectors. Countries such as Brazil and Mexico show increasing demand for plasticizers and coatings used in infrastructure development and automotive production. While local production capacity remains limited compared to major global regions, imports support downstream manufacturing industries. The Middle East & Africa region is gaining prominence in the market due to strong petrochemical feedstock availability and industrial diversification initiatives. Countries such as Saudi Arabia and the UAE benefit from abundant hydrocarbon resources, supporting cost-effective production of oxo intermediates. Increasing investments in downstream chemical manufacturing and construction projects drive the demand for plasticizers, solvents, and resins. The Middle East & Africa market reached a value of USD 1.50 billion in 2025.

GCC Oxo Chemicals Market

The GCC market accounted for a value of around USD 0.55 billion in 2025, representing approximately 2.1% of regional revenues. Expansion is anchored in new integrated petrochemical complexes, strategic downstream diversification programs, and increasing regional capacity for oxo alcohol exports.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vertical Integration and Feedstock Advantage of Leading Players to Strengthen their Edge

The oxo chemicals market is moderately consolidated, characterized by the presence of large, vertically integrated petrochemical companies with strong control over upstream olefin feedstocks and downstream oxo derivative production. Competition is primarily driven by production scale, catalyst efficiency, operational optimization, and long-term supply agreements with plasticizer, coatings, and resin manufacturers. Access to competitively priced propylene and synthesis gas provides a strategic cost advantage, particularly in regions with integrated refinery–petrochemical complexes. Companies are also focusing on environmentally compliant and non-phthalate plasticizer alcohols to align with regulatory requirements. Ongoing capacity expansions in Asia Pacific and the Middle East further intensify competition. High capital investment and technical expertise requirements create entry barriers, reinforcing competitive concentration within the market.

LIST OF KEY OXO CHEMICALS COMPANIES PROFILED:

- BASF SE (Germany)

- Eastman Chemical Company (U.S.)

- Dow Inc. (U.S.)

- OXEA GmbH (Germany)

- Perstorp Holding AB (Sweden)

- Evonik Industries AG (Germany)

- LG Chem Ltd. (South Korea)

- Sasol Limited (South Africa)

- Formosa Plastics Corporation (Taiwan)

- PetroChina Company Limited (China)

KEY INDUSTRY DEVELOPMENTS:

- August 2024: BASF entered into a Memorandum of Understanding (MoU) with UPC Technology Corporation, strengthening their long-standing partnership. The agreement is designed to enhance long-term regional collaboration, particularly in the supply of plasticizer alcohols and catalysts used in phthalic anhydride (PA) and maleic anhydride (MA) production. In addition, both companies aim to jointly advance sustainable initiatives focused on reducing carbon emissions across their operational processes and product portfolios.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, and Region |

|

By Product Type |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 26.00 billion in 2025 and is projected to reach USD 44.56 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 6.1% during the forecast period of 2026-2034.

The plasticizers segment leads the market by application.

Asia Pacific holds the highest market share.

Strong plasticizer demand and industrial activity are key factors propelling market growth.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us