Paper Chemicals Market Size, Share & Industry Analysis, By Type (Pulp Chemicals, Process Chemicals, and Functional Chemicals), By Form (Specialty Chemicals and Commodity Chemicals), By Application (Packaging & Board, Tissue & Hygiene, Graphic & Printing Papers, Specialty Papers, and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

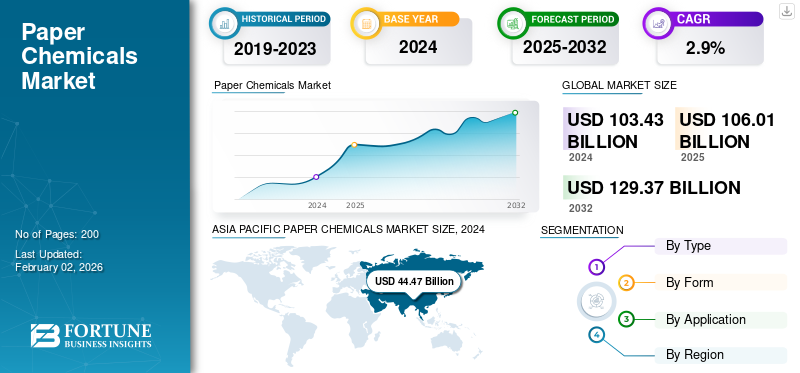

The global paper chemicals market size was valued at USD 103.43 billion in 2024. The market is projected to grow from USD 106.01 billion in 2025 to USD 129.37 billion by 2032, exhibiting a CAGR of 2.9% during the forecast period. The Asia Pacific dominated global market with a share of 43.% in 2024.

Paper chemicals are a diverse group of chemical formulations used at various stages of paper manufacturing to enhance the quality, performance, and appearance of paper and paperboard products. Market growth is propelled by increasing demand for packaging materials, tissue papers, and specialty paper products in emerging economies such as India, China, and Southeast Asia. As e-commerce and food delivery services expand, the demand for high-performance packaging paper with barrier properties has increased. This is leading to a greater use of sizing agents, strength additives, and coating chemicals. Moreover, sustainability concerns are driving manufacturers toward eco-friendly, biodegradable, and low-VOC (volatile organic compound) chemical formulations, resulting in a shift from conventional synthetic additives to bio-based and waterborne solutions.

Furthermore, the market encompasses several major players, including Shandong Bluesun Chemicals Co., Ltd, Anshika Polysurf Limited, NIPPON PAPER INDUSTRIES CO., LTD., Thermax Limited, and Solenis. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Specialty and Functional Papers to Propel Market Growth

The growing demand for specialty and functional papers, including papers used in labels, filters, décor, currency, and electrical insulation, drives market growth. These niche paper grades require precise formulations of specialty chemicals to achieve high strength, thermal stability, chemical resistance, or optical performance.

- For instance, conductive coatings, flame-retardant additives, and anti-static agents are used in technical and industrial papers. In contrast, optical brightening agents and coating binders are essential for high-quality decorative and printing papers. The expansion of industries such as electronics, automotive, and construction is contributing to the rising demand for these papers.

Moreover, the growing popularity of premium packaging and luxury printing in the cosmetics, beverages, and fashion industries has increased the demand for high-gloss and textured paper surfaces, thereby further boosting the market for coating and surface treatment chemicals.

- Manufacturers such as Clariant, BASF, and SNF Floerger are developing specialized polymer dispersions and performance additives specifically tailored for these applications.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions to Restrict Market Expansion

Fluctuations in crude oil prices, geopolitical tensions, and supply chain disruptions can significantly increase production costs and impact profitability for chemical manufacturers. For example, during the 2022–2023 period, the global energy crisis and supply disruptions resulting from the Russia–Ukraine conflict led to sharp increases in raw material and logistics costs, which were subsequently reflected in the pricing of paper chemicals. Additionally, supply chain bottlenecks, such as shortages of specialty chemicals from China or shipping delays, have disrupted production schedules for both paper mills and chemical suppliers.

Furthermore, the lack of reliable raw material availability in developing regions limits the ability of local producers to scale operations. The recent emphasis on sustainability has also increased dependency on bio-based feedstocks, such as starch and lignin, which face their own challenges, including inconsistent quality and supply. Consequently, volatile input costs and logistical uncertainties continue to restrain profitability and market stability, making raw material management a critical risk factor for the global industry.

MARKET OPPORTUNITIES

Technological Advancements in Papermaking Processes to Create Lucrative Growth Opportunities

Paper manufacturers are adopting advanced chemical formulations and automated process control technologies to enhance production efficiency, reduce water consumption, and achieve superior product quality. Modern papermaking relies on optimized chemical interactions for fiber modification, retention, drainage, and coating.

- For instance, the use of cationic polymers and retention aids has enabled better bonding between fibers and fillers, as well as improved machine runnability, thereby minimizing production downtime.

Similarly, enzyme-based pulping and bleaching technologies are replacing chlorine-based chemicals, cutting both energy use and environmental impact. Industry players such as Ecolab, Ashland, and Buckman Laboratories have introduced smart chemical dosing systems and real-time monitoring tools that precisely control the amount and timing of chemical applications.

MARKET CHALLENGES

Stringent Environmental Regulations and Compliance Costs to Hamper Growth

Many conventional paper chemicals, such as formaldehyde-based resins, optical brighteners, and certain surfactants, pose risks of toxicity, water pollution, and non-biodegradability. Regulatory authorities, such as the European Chemicals Agency (ECHA) under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), and the U.S. Environmental Protection Agency (EPA), have imposed strict controls on hazardous chemical substances. This has compelled manufacturers to reformulate their products using eco-friendly, bio-based alternatives, an effort that involves substantial R&D investment and process reengineering costs.

- For example, replacing alkylphenol ethoxylates (APEs), which are non-biodegradable, with plant-derived surfactants significantly increases formulation costs.

PAPER CHEMICALS MARKET TRENDS

Rising Demand for Sustainable and Eco-Friendly Paper Products is One of the Significant Market Trends

Growing environmental awareness and stricter government regulations on plastic usage have shifted consumer and industrial preferences toward biodegradable paper-based packaging. As single-use plastics are being phased out globally in Europe, North America, and parts of Asia Pacific, demand for paper packaging materials has surged. This transition directly boosts the consumption of paper chemicals that enable recyclability, biodegradability, and reduced environmental impact.

- For instance, bio-based sizing agents, natural polymers, and enzymatic bleaching chemicals are being adopted to replace petroleum-derived additives. Companies such as BASF SE and Kemira Oyj have developed water-based and low-VOC chemical formulations that improve paper strength and printability without compromising sustainability standards.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Pulp Chemicals Led Market Due to Their Essential Role in Improving Pulp Quality, Yield, and Fiber Processing Efficiency

The market is segmented by type into pulp chemicals, process chemicals, and functional chemicals.

The pulp chemicals segment held the largest paper chemicals market share in 2024 and is expected to experience substantial growth. The segment growth is driven by the rising demand for high-brightness and low-contaminant pulp in packaging and printing papers. The increasing adoption of elemental chlorine-free (ECF) and totally chlorine-free (TCF) bleaching processes aligns with environmental compliance trends. Furthermore, the expansion of recycled fiber-based production in the Asia Pacific region necessitates the use of effective de-inking and dispersing chemicals, thereby bolstering demand. Innovations in eco-friendly pulping agents, such as enzymes and oxygen-based bleaches, are also fueling sustainable growth.

The process chemicals segment witnesses considerable growth. The growth of the segment is associated with the industry’s push for operational optimization and water conservation. As mills modernize toward closed-loop systems, the need for efficient process aids such as retention agents, defoamers, and biocides rises sharply. Additionally, increasing costs of raw materials and energy drive mills to seek process chemicals that enhance yield and reduce downtime. Sustainability trends are fostering the adoption of biodegradable and low-VOC process chemicals.

The growth of the functional chemicals segment is driven by the increasing demand for high-quality packaging and specialty papers that require superior coating, sizing, and strength enhancement. Functional chemicals, such as starches, latex binders, and optical brightening agents, are experiencing increased demand due to the surge in e-commerce packaging and premium printing applications. Additionally, the push toward sustainable packaging solutions, including recyclable and biodegradable barrier coatings, is boosting the segment’s growth.

By Form

Specialty Chemicals Dominated Market Owing to Increasing Adoption in Paper Packaging Manufacturing

The market is segmented by form, classified into specialty chemicals and commodity chemicals.

The specialty chemicals segment held the largest market share in 2024 and is expected to experience substantial growth, driven by the increasing shift toward customized, high-performance paper grades. These include barrier papers for food packaging, decorative laminates, security papers, and technical papers used in filtration and insulation. The segment benefits from technological advancements that enable enhanced durability, smoothness, and resistance to moisture or grease. Rising environmental regulations are pushing manufacturers to adopt bio-based specialty chemicals derived from renewable raw materials.

The commodity chemicals segment is projected to experience significant growth in the coming years. The growth of the segment is volume-driven, closely linked to global paper output levels in the packaging and tissue segments. The steady rise in paperboard and corrugated packaging consumption, driven by e-commerce expansion, supports a strong baseline demand.

By Application

To know how our report can help streamline your business, Speak to Analyst

Packaging & Board Segment Takes the Lead Owing to Increasing Demand from Various Industries

Based on application, the market is segmented into packaging & board, tissue & hygiene, graphic & printing papers, specialty papers, and others.

The packaging & board segment dominates the market and is expected to register significant growth during the forecast period. The rapid expansion of e-commerce, food delivery, and consumer goods sectors drives the growth of the segment. The demand for paper-based packaging as a sustainable alternative to plastics is at an all-time high, driving the need for strength additives, sizing agents, and coating chemicals. Innovations in water- and grease-resistant functional coatings are enabling broader use of paper in food and beverage packaging. Furthermore, the segment is set to hold a 33.5% share in 2025.

The tissue & hygiene segment is witnessing favorable growth. This expansion is attributed to the increasing demand for personal care and sanitation products in emerging markets. Population growth, urbanization, and heightened hygiene awareness post-pandemic have spurred the consumption of tissue papers, napkins, and wipes. This growth drives demand for softening agents, strength enhancers, and chemicals that improve absorbency. In addition, tissue & hygiene applications are projected to grow at a CAGR of 3.0% during the study period.

The graphic & printing papers segment is also experiencing favorable growth. The growth of this segment is associated with the demand for high-quality coated papers used in commercial printing, magazines, and advertising materials. Growth in emerging economies and niche applications, such as art papers and luxury catalogs, sustains market activity. The segment relies heavily on optical brighteners, coating binders, and surface sizing agents to ensure superior printability and gloss.

The specialty papers segment is driven by innovation in advanced functional coatings, microfibrillated cellulose (MFC) additives, and nanotechnology-based formulations. The rising use of sustainable barrier papers in food and industrial packaging also supports segment expansion.

Paper Chemicals Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

ASIA PACIFIC PAPER CHEMICALS MARKET SIZE, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2023, valued at USD 44.14 billion, and also maintained the leading position in 2024, with a value of USD 44.47 billion. The factors fostering the dominance of the region include rapid e-commerce growth, expanding FMCG and foodservice sectors, and large-scale investments in new pulp & packaging capacity (including integrated pulp-to-packaging projects), which are the primary demand drivers for retention aids, sizing agents, coating/starch chemistries, and specialty additives.

In 2025, the Chinese market is estimated to reach USD 18.09 billion.

- China is the fastest-growing market, and the transition from plastic to paper-based packaging across e-commerce, food delivery, and consumer goods is a significant catalyst for the consumption of functional and coating chemicals. Investments in high-capacity, integrated pulp-paper mills in Shandong, Zhejiang, and Guangxi provinces are boosting the use of pulp and process chemicals, including bleaching agents, retention aids, and de-inking formulations.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 2.8%, the second-highest among all regions, and reach a valuation of USD 22.39 billion by 2025. The market's growth is driven by the demand for recyclable, low-VOC, and bio-based paper chemicals. Growth focuses on specialty and high-performance functional additives (barrier coatings, fluorine-free repellents, enzymatic pulping aids) as brands shift to paper alternatives. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 1.48 billion, Germany to record USD 6.09 billion, and France to record USD 2.71 billion in 2025.

North America

After Europe, the market in North America is estimated to reach USD 22.87 billion in 2025 and secure the position of the third-largest region in the market. The market is anticipated to grow due to the premium packaging demand (brand protection, retail-ready packaging), investment in automation/quality (raising per-unit chemical intensity), and strong tissue & hygiene consumption. Sustainability regulations and corporate net-zero commitments are driving mills to adopt lower-emission chemistries, bio-based additives, and recyclable barrier alternatives, creating a market for higher-value specialty chemistries despite overall mature volumes. In 2025, the U.S. market is estimated to reach USD 19.75 billion.

- In the U.S., the market’s growth is driven by strong consumer demand for sustainable and functional packaging solutions. The ongoing substitution of plastics with paper in retail and e-commerce packaging continues to drive demand for functional additives, including strength enhancers, sizing agents, and barrier coatings. Additionally, the U.S. paper industry’s focus on energy efficiency, water reuse, and process optimization drives the uptake of advanced process chemicals, including retention aids, biocides, and defoamers.

Latin America

The Latin America market in 2025 is set to record USD 8.82 billion in valuation. The market's growth is concentrated in commodity and mid-value functional chemistries for packaging and tissue; specialty uptake is increasing but constrained by capex cycles and logistics.

Middle East & Africa

In the Middle East & Africa, Saudi Arabia is expected to reach a value of USD 1.89 billion in 2025. The market’s growth is attributed to regulatory moves away from single-use plastics, growth in the foodservice/retail sectors, and infrastructure/industrial projects that drive demand for construction-related paper chemicals.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Focus on Geographical Expansion and Broaden Their Market Presence

This market is concentrated, with key manufacturers operating in the industry such as Shandong Bluesun Chemicals Co., Ltd, Anshika Polysurf Limited, NIPPON PAPER INDUSTRIES CO., LTD., Thermax Limited, and Solenis. Industry players have integrated raw material production and sales activities to maintain product quality and expand their regional presence. This gives businesses a competitive edge in the form of a cost advantage, which improves profit margins. Additionally, to boost their market share and achieve a competitive advantage, several major players are engaging in numerous strategic alliances to promote their brand and sales.

LIST OF KEY PAPER CHEMICAL COMPANIES PROFILED

- Shandong Bluesun Chemicals Co., Ltd (China)

- Anshika Polysurf Limited (India)

- NIPPON PAPER INDUSTRIES CO., LTD. (Japan)

- Thermax Limited (India)

- Solenis (U.S.)

- BASF (Germany)

- Buckman (U.S.)

- DOW (U.S.)

- Pon Pure Chemicals Group (India)

- Ivax (India)

- Suman Chemical Industries Limited (India)

KEY INDUSTRY DEVELOPMENTS

- February 2023: Solenis completed the acquisition of the KLK Kolb Group's paper process chemicals business, adding product breadth and securing long-term manufacturing/supply arrangements for process chemistries.

- October 2022: Solenis opened two new Centers of Excellence to serve the growing consumer paper-packaging market (including a customer support, analytical & applications lab in Mönchengladbach and virtual lab capability), signalling R&D and application focus on fiber-based packaging.

- July 2021: Platinum Equity signed a definitive agreement to acquire Solenis (transaction announced July 6, 2021), marking a major ownership change for one of the largest specialty paper/process chemicals suppliers.

- April 2021: BASF launched Joncryl high-performance barrier dispersions, targeting water-based barrier coatings for paper packaging (China launch), underscoring the growth of water-based barrier solutions for packaging.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 2.9% from 2025-2032 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Segmentation |

By Type, By Form, By Application, and By Region |

|

By Type |

|

|

By Form |

|

|

By Application |

|

|

By Region |

o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 103.43 billion in 2024 and is projected to reach USD 129.37 billion by 2032.

In 2024, the market value stood at USD 44.47 billion.

The market is expected to exhibit a CAGR of 2.9% during the forecast period of 2025-2032.

The pulp chemicals segment led the market by type.

The key factors driving the market are the rising demand for sustainable and high-quality paper products and rising consumption of packaging and tissue papers.

Shandong Bluesun Chemicals Co., Ltd, Anshika Polysurf Limited, NIPPON PAPER INDUSTRIES CO., LTD., Thermax Limited, and Solenis are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

The major factors expected to favor product adoption include the shift toward bio-based and recyclable paper solutions and the expansion of the packaging and hygiene industries.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us